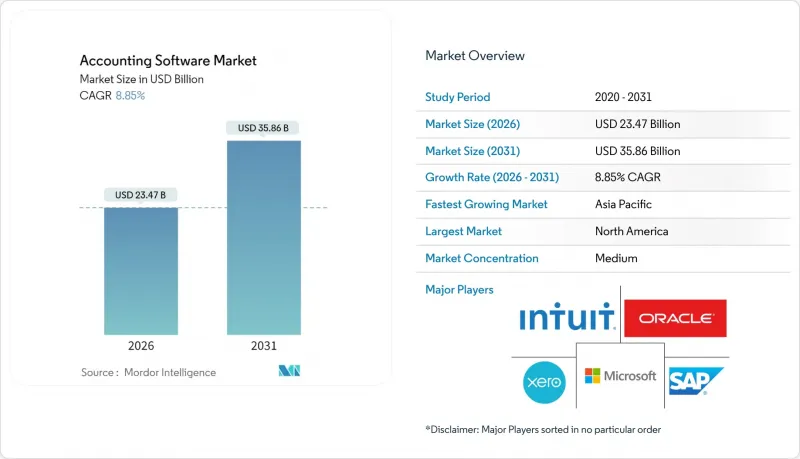

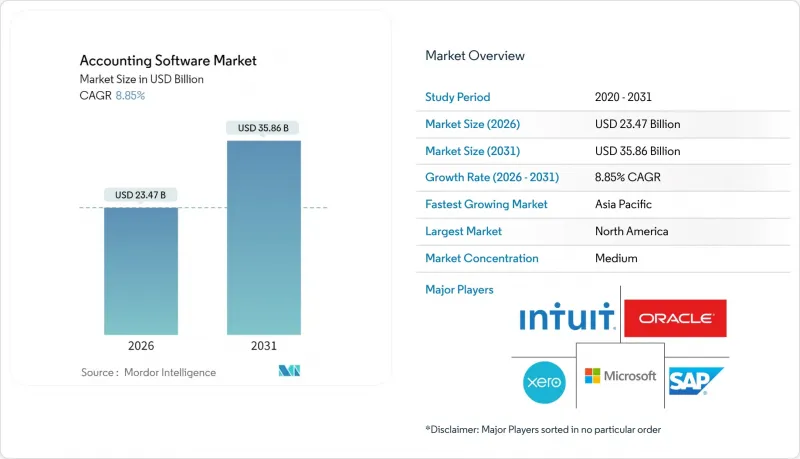

회계 소프트웨어 시장은 2025년에 215억 6,000만 달러로 평가되며, 2026년 234억 7,000만 달러에서 2031년까지 358억 6,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 8.85%로 예상됩니다.

클라우드 우선 전략, 실시간 규제 보고 의무, 임베디드 인공지능 기능은 경쟁 우위를 계속 재정의하고 있으며, 클라우드 배포는 2024년 현재 이미 매출의 67.43%를 차지하고 있습니다. 각 벤더들은 은행 업무, 재무 관리, 지출 관리 기능을 통합한 모바일 지원 및 API 중심의 제품군을 확장하고 있으며, 이를 통해 기업은 월별 결산 주기를 단축하고 운전 자본에 대한 인사이트을 확보할 수 있습니다. 동시에 재무부서내 인력 부족이 소프트웨어 도입을 가속화하고 있으며, 자동화가 반복적인 장부업무를 대체하고 있기 때문입니다. 마지막으로 새로운 ESG 감사 추적 요구사항으로 인해 조직은 환경 및 사회 공시를 지속적으로 생성하는 솔루션으로 전환하기 위해 레거시 시스템을 개편해야 합니다.

조직은 On-Premise형 도입에서 벗어나 회계, 재무, 업무 데이터를 실시간으로 동기화하는 클라우드 아키텍처를 채택하고 있습니다. 이를 통해 인프라 비용 절감과 현금 흐름 가시성을 향상시킬 수 있습니다. 이 전환은 기존 시스템에서는 불가능했던 원활한 핀테크 연계(결제, 경비카드, 단기 유동성 관리)도 가능하게 합니다.

머신러닝을 통한 데이터 추출과 로봇 프로세스 자동화를 통해 거래 분류, 은행 대조, 인보이스 처리가 98%의 정확도로 이루어지고 있습니다. 이를 통해 회계법인은 인력을 비례적으로 늘리지 않고도 더 많은 고객을 수용할 수 있습니다. 이러한 생산성 향상은 중소기업의 총소유비용을 절감하고 업계 전반의 인력 부족을 상쇄할 수 있습니다.

GDPR(EU 개인정보보호규정) 등의 규제로 인해 데이터 현지 보관이 의무화되면서 벤더들은 여러 지역의 클라우드를 유지해야 하고, 도입 예산이 늘어나는 추세입니다. 기업은 암호화, 액세스 제어, 국내 스토리지 옵션을 보장하는 계약 조항이 마련될 때까지 민감한 원장의 마이그레이션을 주저하고 있으며, 이로 인해 프로젝트 일정이 지연되고 있습니다.

클라우드 솔루션은 2025년 68.08%의 매출을 창출할 것이며, 10.15%의 연평균 복합 성장률(CAGR)은 On-Premise 점유율이 지속적으로 감소할 것임을 시사합니다. 성장에 따른 과금 모델은 자본 지출이 필요 없고, 보안 태세를 강화하는 자동 업데이트 기능을 내장하고 있습니다. 은행 및 급여 프로바이더와의 원활한 API 연동은 도입을 더욱 촉진합니다. 레거시 ERP에 의존하는 대기업은 지연에 민감한 워크플로우를 위해 여전히 하이브리드 전략을 선호하지만, 결산주기 단축을 위해 클라우드 자회사 도입 시험도 진행하고 있습니다. 데이터 거주지 옵션의 확대와 지역별 데이터센터 구축으로 기존의 컴플라이언스 우려는 완화되고, 회계 소프트웨어 시장에서 클라우드의 점유율은 10년 이내에 포화상태에 가까워질 것으로 예측됩니다.

On-Premise형 플랫폼은 오프라인 처리가 필수적인 고도로 규제된 분야나 맞춤형 커스터마이징으로 시스템이 고착화된 분야에서 틈새 시장으로 존재감을 유지하고 있습니다. 그러나 유지보수 비용 부담과 메인프레임 기술자 부족으로 인해 CFO는 현대화 예산을 확보하기 위해 노력하고 있습니다. 벤더들은 이러한 전환기를 포착하여 과거 원장 데이터를 멀티테넌트 아키텍처로 매핑하는 마이그레이션 툴키트을 제공합니다. 이를 통해 전환 기간을 몇 주 만에 단축할 수 있었습니다. 그 결과, 업계 전체가 확대되는 가운데 On-Premise 구축과 관련된 회계 소프트웨어 시장 규모는 축소될 것으로 예측됩니다.

대기업은 세계 연결 결산 스위트를 도입하여 2025년 매출의 54.10%를 차지할 것으로 예측됩니다. 반면, 중소기업은 직관적인 클라우드 모듈과 AI 기반 데이터 수집으로 전담 IT 인력의 필요성이 줄어들면서 10.85%의 가장 빠른 CAGR을 기록했습니다. 구독 계층은 거래량에 따라 비용을 조정하므로 성장 초기에도 저렴한 가격을 유지할 수 있습니다.

아시아태평양 및 라틴아메리카의 기업이 생태계는 의무화된 전자 송장 발행이 디지털화 추진을 촉진하여 중소기업 수요를 더욱 가속화할 것입니다. 벤더들이 챗봇 기능이 포함된 스타터 패키지를 제공함으로써 도입 장벽을 낮추고, 수동 스프레드시트 사용자를 가입자로 전환하고 있습니다. 그 결과, 중소기업이 차지하는 회계 소프트웨어 시장 점유율은 꾸준히 상승하고, 기존 대기업 도입과의 격차는 줄어들 것으로 예측됩니다.

회계 소프트웨어 시장은 도입 형태(On-Premise, 클라우드), 조직 규모(대기업, 중소기업(SME)), 최종사용자 산업(은행, 금융서비스 및 보험(BFSI), 제조, 소매 및 E-Commerce, 전문 서비스, IT 및 통신, 의료), 용도(급여 관리, 청구 및 송장 발행, 기타), 지역별로 세분화되어 있습니다. 지역별로 세분화되어 있습니다. 시장 예측은 금액(USD) 기준으로 제공됩니다.

북미는 높은 클라우드 배포 준비도, 성숙한 결제 인프라, 충분한 기술 예산을 바탕으로 2025년 38.35%의 매출을 차지할 것으로 예측됩니다. 미국 기업은 금융 용도에 대한 직원 1인당 지출이 세계 평균을 상회하고 있으며, 벤더의 빠른 혁신과 파트너십 생태계를 촉진하고 있습니다. 캐나다도 비슷한 추세를 보이고 있으며, 국경 간 도입을 간소화하는 조화로운 세제 프레임워크가 이를 지원하고 있습니다.

유럽에서는 GDPR(EU 개인정보보호규정)(일반 데이터 보호 규정) 준수와 지속가능성 보고 의무가 플랫폼 업데이트를 촉진하고 있습니다. 다국어 인터페이스와 Peppol과 같은 유럽 전자 송장 표준이 제품 현지화를 촉진하고 있습니다. 다만, 의사결정 주기가 느린 점이 아시아태평양과 비교했을 때 성장을 저해하는 요인으로 작용하고 있습니다.

아시아태평양은 10.45%의 가장 빠른 CAGR을 기록했으며, 인도와 인도네시아의 전자 청구서 의무화 도입과 일본의 전자 장부 보관에 대한 소프트 의무화가 촉진요인으로 작용하고 있습니다. 중소기업은 데스크톱 소프트웨어를 뛰어넘어 국내 전자지갑과 QR코드 결제를 통합한 모바일 퍼스트의 클라우드 스위트를 채택하고 있습니다. 세계 벤더들의 현지 데이터센터 투자는 데이터 주권에 대한 우려를 완화하고 공공 부문의 조달 기회를 창출하고 있습니다.

라틴아메리카에서는 브라질과 멕시코에서 그 기세를 볼 수 있습니다. 양국은 수년간 실시간 인보이스 결제가 시행되어 왔으며, 기업은 세무보고를 넘어 자동화를 추진하고, ERP와 재무를 통합한 클라우드 시스템으로 전환하고 있습니다. 중동 및 아프리카은 경제 다각화 추진과 핀테크 생태계 확장에 따라 꾸준한 성장세를 보이고 있지만, 연결성 및 인력 부족으로 도입 속도가 느려지고 있습니다.

The accounting software market was valued at USD 21.56 billion in 2025 and estimated to grow from USD 23.47 billion in 2026 to reach USD 35.86 billion by 2031, at a CAGR of 8.85% during the forecast period (2026-2031).

Cloud-first strategies, real-time regulatory reporting mandates and embedded artificial-intelligence features continue to redefine competitive advantage, with cloud deployments already anchoring 67.43% of revenue in 2024. Vendors are expanding mobile, API-centric suites that integrate banking, treasury and spend-management functions, helping enterprises compress monthly close cycles and unlock working-capital insights. At the same time, talent shortages inside finance departments accelerate software adoption because automation substitutes repetitive bookkeeping labor. Finally, emerging ESG audit-trail requirements force organizations to refresh legacy systems in favor of solutions that generate immutable environmental and social disclosures.

Organizations are abandoning on-premise installations in favor of cloud architectures that synchronize accounting, treasury and operational data in real time, cutting infrastructure costs and improving cash-flow visibility. The shift also unlocks seamless fintech integrations-payments, expense cards and short-term liquidity-once unattainable on legacy systems.

Machine-learning extraction and robotic process automation now classify transactions, reconcile banks and process invoices with 98% accuracy, allowing accounting firms to absorb more clients without proportional head-count increases. The resulting productivity gains lower total ownership costs for small businesses and offset the industry-wide talent deficit.

Rules such as GDPR compel local data residency, forcing vendors to maintain multi-region clouds and inflating implementation budgets. Enterprises hesitate to migrate sensitive ledgers until contractual clauses guarantee encryption, access controls and in-country storage options, delaying project timelines .

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Cloud solutions generated 68.08% revenue in 2025, and their 10.15% CAGR signals that the on-premise share will continue to erode. The model's pay-as-you-grow pricing eliminates capital expenditure and embeds automatic updates that strengthen security posture. Seamless API connectivity with banks and payroll providers further cements adoption. Large enterprises wedded to legacy ERPs still favor hybrid strategies for latency-sensitive workflows, yet even they pilot cloud subsidiaries to reduce close cycles. Growing data-residency options and regional datacenters mitigate prior compliance objections, suggesting that the cloud slice of the accounting software market will near saturation by decade-end.

On-premise platforms retain niche relevance in highly regulated sectors where offline processing is mandatory or where bespoke customizations lock systems in place. However, maintenance overhead and scarce mainframe skills push CFOs to earmark modernization budgets. Vendors exploit this transition by offering migration toolkits that map historical ledgers into multi-tenant architectures, shortening cut-over periods to weeks. As a result, the accounting software market size tied to on-premise deployments is projected to contract despite overall industry expansion.

Large organizations captured 54.10% of 2025 revenue by deploying global-consolidation suites capable of multi-currency and multi-entity reporting. Yet SMEs drive the fastest 10.85% CAGR because intuitive cloud modules and AI-driven data capture reduce the need for dedicated IT staff. Subscription tiers align costs with transaction volume, ensuring affordability even during early growth stages.

Entrepreneurial ecosystems in Asia-Pacific and Latin America further catalyze SME demand as mandatory e-invoicing forces digital upgrades. Vendors releasing starter packages with embedded chatbot support lower adoption barriers and convert manual spreadsheet users into subscribers. Consequently, the accounting software market share commanded by SMEs will steadily rise, narrowing the historic gap with enterprise deployments.

Accounting Software Market is Segmented by Deployment Type (On-Premise, and Cloud-Based), Organization Size (Large Enterprises, and Small and Medium Enterprises (SMEs)), End-User Industry (BFSI, Manufacturing, Retail and E-Commerce, Professional Services, IT and Telecom, and Healthcare), Application (Payroll Management, Billing and Invoicing, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America contributed 38.35% revenue in 2025 on the back of high cloud readiness, mature payments rails and well-funded technology budgets. United States enterprises allocate larger per-employee spend on finance applications compared with global averages, spurring rapid vendor innovation and partnering ecosystems. Canada mirrors this trend, supported by harmonized taxation frameworks that simplify cross-border deployment.

Europe follows, where GDPR compliance and sustainability-reporting mandates stimulate platform refreshes. Multi-lingual interfaces and European e-invoicing standards such as Peppol drive product localization. However, slower decision cycles temper growth relative to Asia-Pacific.

Asia-Pacific charts the fastest 10.45% CAGR, propelled by India's and Indonesia's compulsory e-invoicing rollouts and by Japan's soft-mandate for electronic preservation of ledgers. SMEs leapfrog desktop software, adopting mobile-first cloud suites that integrate domestic e-wallets and QR code payments. Local datacenter investments by global vendors mitigate data-sovereignty hesitance and unlock public-sector procurements.

Latin America sees momentum in Brazil and Mexico, where real-time invoice clearance has existed for years, leading businesses to extend automation beyond tax reporting to full ERP-finance clouds. Middle East and Africa post steady gains aligned to economic diversification drives and expanding fintech ecosystems, though connectivity and talent shortages moderate adoption pace.