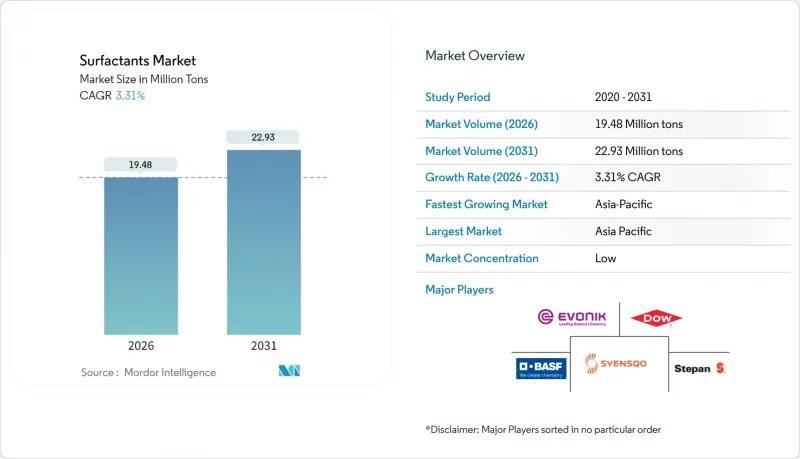

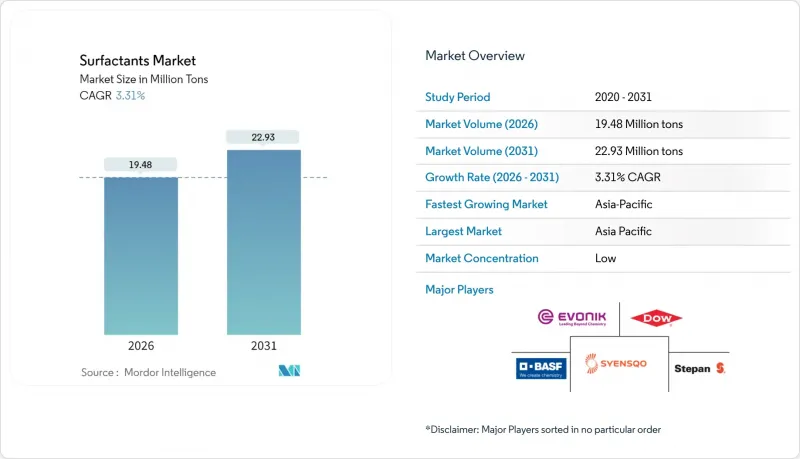

2026년 계면활성제 시장 규모는 1,948만 톤으로 추정되며, 2025년 1,886만 톤으로부터 성장이 전망됩니다.

2031년에는 2,293만 톤에 달할 것으로 예상되며, 2026-2031년 연평균 복합 성장률(CAGR) 3.31%로 성장할 전망입니다.

프리미엄 퍼스널케어 제품에 다기능성 순한 계면활성제, 에너지 절약형 냉수 세탁 세제, 강화되는 지속가능성 규제를 충족하는 바이오 원료의 활용이 경쟁의 초점이 되고 있습니다. 한편, 중국의 주기적인 과잉 생산 능력 사이클과 장쇄 알코올 공급 변동에 따른 가격 변동이 지속되고 있으며, 생산자들에게는 비용 관리가 최우선 과제로 떠오르고 있습니다. 통합형 기업은 세계 공급망과 R&D의 깊이를 활용하여 점유율을 지키고 있지만, 특수 바이오 계면활성제 공급업체와 아시아태평양의 민첩한 지역 기업은 기존의 우위를 꾸준히 잠식하고 있습니다.

각 브랜드들은 피부 친화성과 환경 보호를 우선시하고 있으며, 배합 설계자들은 기존의 황산계에서 글루카미드나 이세티오네이트 등으로 전환하고 있습니다. 이들은 농축형 고체 비누, 스틱, 파우더 제품에서 순한 세정력과 컨디셔닝 효과를 발휘합니다. 클라리언트의 연구에 따르면 이 분자들은 소비자들이 중요시하는 거품감을 유지하면서 헹굼 물과 에너지 사용량을 줄여주는 것으로 나타났습니다. 북미와 유럽 소비자들은 이러한 제품 형태에 프리미엄 가격을 지불하는 경향이 있으며, BASF는 석유 유래 제품 대비 제품 탄소발자국을 최대 30%까지 줄이는 '에코밸런스 베타인' 라인의 확장을 추진하고 있습니다. 원료의 신속한 개선과 수자원 관리를 중심으로 한 타겟 마케팅으로 아시아 소비자들이 고체 세제에 대한 선호도가 높아지면서 지속적인 보급이 예상되는 계면활성제 시장의 기반이 마련되고 있습니다.

인도네시아의 B35 바이오디젤 의무화 정책 및 유사 프로그램으로 인해 나프타계 지방산과 동등한 경쟁력을 가진 풍부한 중쇄 지방산이 공급되어 재생 계면활성제 루트의 경제성이 향상되고 있습니다. 유럽 제조업체들은 자산 재구축을 수반하지 않는 바이오매스 밸런싱 방식을 통해 화석 탄소를 재생한 원료로 대체하고 있습니다. 한편, 에보닉의 슬로바키아 신람노리피드 공장은 유럽산 옥수수를 이용한 확장형 발효 기술을 입증했습니다. EU의 삼림파괴 방지 규제와 Scope 3 탄소 회계와 같은 정책적 요인으로 인해 화석 원료의 지속적 사용으로 인한 비용이 현실화되고 있으며, 기존 합성 원료 제조업체들은 브랜드 지속가능성 약속에 따라 혼합 원료 포트폴리오로 전환하고 있습니다.

EU 및 미국 규제 당국은 과불화 알킬 물질 및 폴리불화 알킬 물질(PFAS)에 대한 규제를 빠르게 진행하고 있으며, 이는 현재 계면활성제 최종 용도의 약 38%에 직접적인 영향을 미치고 있습니다. DIC는 이미 기존과 동등한 성능의 PFAS 프리 전기자동차 윤활유용 소포제를 상용화하고 있지만, 필요한 연구개발 투자로 인해 여러 다운스트림 시장에서 단가가 상승하고 있습니다. 재배합의 연쇄는 새로운 안정제 및 가공 공정의 도입을 강요하고, 중소기업의 기술 자원을 압박하고, 산업 구조조정을 가속화하고 있습니다. 조기에 대응하여 적합성 인증을 받은 업체는 가격 프리미엄이 지속되더라도 우선 공급업체로 선정되어 계면활성제 시장에 영향을 미치고 있습니다.

2025년에도 음이온 계면활성제는 47.80%의 압도적인 시장 점유율을 유지했습니다. 이는 선형 알킬벤젠 설포네이트(LAS)가 비용 효율성이 뛰어나고 가정용 세제용으로 널리 승인되었기 때문입니다. LAS의 생산량은 400만 톤을 넘어섰으며, 규모의 경제와 확립된 공급망의 혜택을 누리고 있습니다. 그러나 베타인과 아미노산화물과 같은 양성 분자는 pH 범위에 관계없이 순한 특성과 고급 퍼스널케어 제품에서 복잡한 배합을 안정화시키는 능력을 바탕으로 전체 유형 중 가장 높은 4.30%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 계면활성제 시장에서는 이미 주요 기업이 소매업체의 클린뷰티 기준을 충족시키면서 고매출을 보장하는 친환경 인증 베타인을 내세우고 있습니다.

양이온 부문은 규모는 작지만 유연제 및 항균성 4급 염화물 블렌드에서 필수적인 존재입니다. 한편, 실리콘계 계면활성제는 연신성이 탄소계 유사제품보다 우수하여 섬유가공, 증진채유, 고신축성 폴리우레탄 폼 등 틈새 시장을 개발하고 있습니다.

본 계면활성제 보고서는 유형별(음이온 계면활성제, 양이온 계면활성제 등), 유래별(합성 계면활성제, 바이오 계면활성제), 용도별(가정용 비누/세제, 퍼스널케어, 윤활유/연료 첨가제, 산업/시설용 세정제 등), 지역별(아시아태평양, 북미, 유럽 등)로 분류하여 조사했습니다. 로 분류되어 있습니다. 시장 예측은 톤 단위로 제공됩니다.

아시아태평양은 2025년 전체 계면활성제 시장의 48.40%를 차지할 것으로 예상되며, 중국의 압도적인 제조거점, 인도의 중산층 확대, 동남아시아의 급속한 도시화를 배경으로 2031년까지 연평균 복합 성장률(CAGR) 4.24%로 확대될 것으로 전망됩니다. 중국은 전 세계 라 우릴황산나트륨(LAS) 생산량의 절반 이상을 공급하고 있으며, 공격적인 가격 책정으로 국내 세제 시장과 해외 수출을 모두 지원하고 있습니다.

EU의 삼림파괴 없는 조달 규정과 현재 수립 중인 환경 주장 지침에 따라 브랜드 소유자는 원료의 추적가능성을 검증해야 하며, 기업의 지속가능성 예산으로 자금을 조달하는 바이오 계면활성제 시범사업이 촉진되고 있습니다. 미국에서는 특히 농축 세탁용 액체 세제 및 포장 폐기물을 줄이는 다목적 물티슈의 성능 개선에 중점을 두고 있습니다. 두 지역 모두 PFAS 대체 비용에 대한 부담이 있는 반면, 규제 적합 대체품의 신속한 개발이 가능한 연구 거점을 보유하고 있으며, 계면활성제 시장에서 차세대 화학제품의 출발점 역할을 강화하고 이후 신흥 시장으로 확장하고 있습니다.

아부다비와 오만의 계면활성제-고분자 플러딩 캠페인은 고온, 고염분 환경용 블렌드의 고부가가치 시장을 개발하고 있습니다. 한편, 나이지리아와 케냐에서는 도시화가 진행됨에 따라 포장 세제 소비가 증가하고 있습니다. 브라질에서는 콩과 사탕수수 바이오연료에서 얻을 수 있는 풍부한 지방산 제품을 활용하여 재생 계면활성제의 백인팅을 추진하고 있습니다. 이를 통해 환율 변동 리스크에 대한 비용 절감 효과를 실현하고 있습니다. 인프라 부족, 물류비용, 경기순환 등의 과제는 여전히 남아있지만, 현지 위탁제조업체 및 유통업체와 제휴하는 제조업체는 리스크를 줄이고 계면활성제 시장에서의 존재감을 높이고 있습니다.

Surfactants market size in 2026 is estimated at 19.48 Million tons, growing from 2025 value of 18.86 Million tons with 2031 projections showing 22.93 Million tons, growing at 3.31% CAGR over 2026-2031.

Adoption of multifunctional mild surfactants in premium personal-care formats, cold-water laundry detergents that cut energy use, and bio-based feedstocks that satisfy tightening sustainability rules are setting the competitive agenda. Meanwhile, persistent price volatility tied to China's periodic overcapacity cycles and long-chain alcohol supply swings keeps cost discipline front-of-mind for producers. Integrated players leverage global supply chains and research and development depth to defend share, but specialty biosurfactant suppliers and agile regional firms in Asia-Pacific are steadily eroding historical advantages.

Brands are prioritizing skin compatibility and environmental credentials, prompting formulators to shift from traditional sulfate systems to glucamides and isethionates that deliver gentle cleansing and conditioning in concentrated bars, sticks, and powders. Clariant's studies show these molecules cut rinse-water volume and energy use while maintaining foaming sensory cues valued by consumers. North American and European shoppers pay premiums for such formats, encouraging BASF to widen its EcoBalanced betaine line that trims product carbon footprints by as much as 30% compared with petro-based counterparts. Rapid ingredient iteration and targeted marketing around water stewardship are preparing the surfactants market for sustained adoption once Asian consumers gravitate toward solid cleansers.

Indonesia's B35 biodiesel mandate and similar programs unlock abundant medium-chain fatty acids priced competitively with naphtha-based chains, tipping the economics toward renewable surfactant routes. European producers deploy biomass-balance approaches that substitute fossil carbon with renewable inputs without rebuilding assets, while Evonik's new rhamnolipid plant in Slovakia demonstrates scalable fermentation on European corn sugar. Policy drivers such as the EU's Deforestation-Free Regulation and Scope 3 carbon accounting sharpen the cost of staying fossil-based, edging synthetic incumbents in the surfactants industry toward mixed portfolios that better align with brand sustainability pledges.

Regulators in the EU and the United States have fast-tracked restrictions on per- and polyfluoroalkyl substances, directly affecting roughly 38% of current surfactant end-uses. DIC has already commercialized PFAS-free defoamers for electric vehicle lubricants that match the legacy performance envelope, but the required research and development investment raises unit costs across multiple downstream markets. Reformulation cascades force new stabilizer and processing regimes, stretching technical resources at smaller firms and accelerating consolidation. Early-moving suppliers able to certify compliance win preferred-vendor status even if price premiums persist, influencing the surfactants market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Anionic surfactants retained a commanding 47.80% surfactant market share in 2025 as linear alkylbenzene sulfonate (LAS) remained cost-effective and widely approved for household detergents. LAS volumes surpassed 4 million tons, benefiting from scale economies and established supply chains. However, amphoteric molecules such as betaines and amino oxides are projected to record a 4.30% CAGR, the fastest among all types, propelled by their mildness across pH ranges and ability to stabilize complex formulations in premium personal care. The surfactants market is already witnessing major players brandishing eco-certified betaines that secure higher margins while meeting retailer clean-beauty scorecards.

Cationic segments remain small but indispensable in fabric softening and antimicrobial quaternary blends, whereas silicone surfactants carve out niches in textile finishing, enhanced oil recovery, and high-stretch polyurethane foams where their spreadability outperforms carbon-based analogs.

The Surfactants Report is Segmented by Type (Anionic Surfactants, Cationic Surfactants, and More), Origin (Synthetic Surfactants and Bio-Based Surfactants), Application (Household Soap and Detergent, Personal Care, Lubricants and Fuel Additives, Industry and Institutional Cleaning, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Volume (Tons).

Asia-Pacific held 48.40% of the total surfactants market share in 2025 and is projected to expand at a 4.24% CAGR to 2031, underpinned by China's dominant manufacturing base, India's rising middle class, and Southeast Asia's rapid urban migration. China alone supplies more than half of global LAS output, enabling aggressive pricing that feeds both domestic detergents and overseas exports.

The EU's deforestation-free sourcing rules and pending green-claim directives push brand owners to validate traceable feedstocks, bolstering biosurfactant pilots financed via corporate sustainability budgets. The United States emphasizes performance gains, particularly in concentrated laundry liquids and all-purpose wipes that trim packaging waste. Both regions bear the brunt of PFAS reformulation costs yet house the research hubs capable of fast-tracking compliant alternatives, reinforcing their roles as launch pads for next-generation chemistries that later migrate to emerging markets in the surfactants market.

Surfactant-polymer flooding campaigns in Abu Dhabi and Oman open premium avenues for high-temperature, high-salinity blends, while Nigeria and Kenya witness rising consumption of packaged detergents as urbanization accelerates. Brazil leverages its ample fatty-acid by-products from soy and sugarcane biofuels to back-integrate renewable surfactants, offering cost relief against foreign exchange volatility. Infrastructure gaps, logistics costs, and economic cycles remain hurdles, yet manufacturers partnering with local tollers and distributors mitigate exposure and deepen the surfactants market footprint.