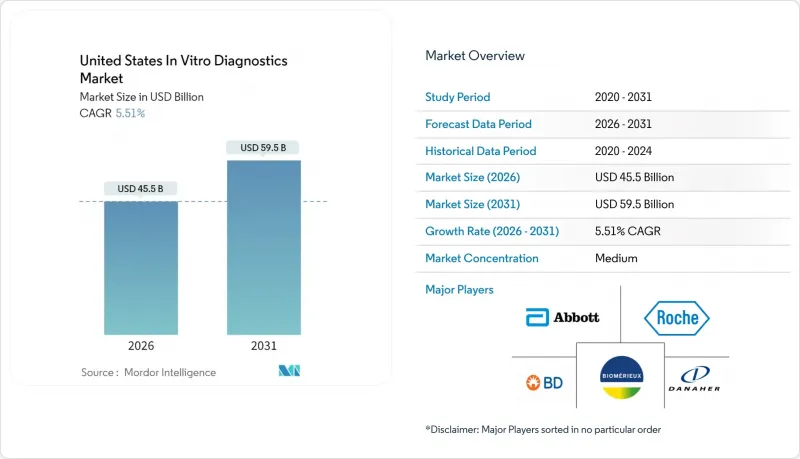

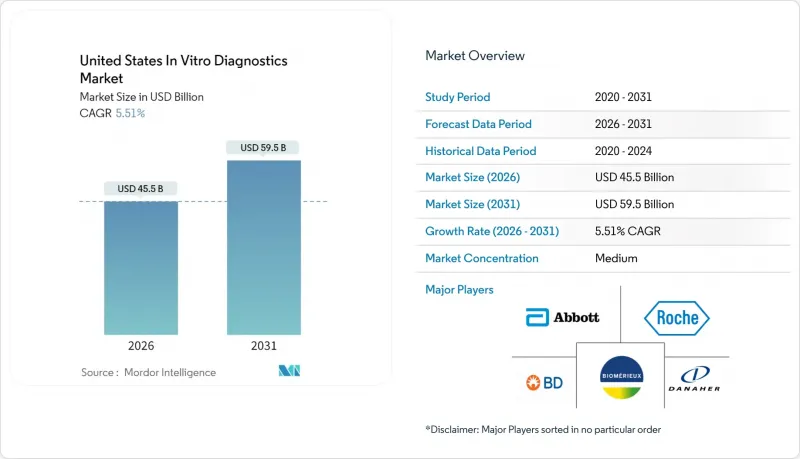

2026년 미국 체외진단약 시장 규모는 455억 달러로 추정되며, 2025년 431억 3,000만 달러에서 계속 성장하고 있습니다.

2031년까지의 예측은 595억 달러에 달할 것으로 예상되며, 2026-2031년 연평균 복합 성장률(CAGR) 5.51%로 확대될 것으로 예측됩니다.

고령화 인구 증가, 만성질환 부담 확대, POC(Point-of-Care) 기술 정착 등의 요인이 복합적으로 작용하여 꾸준한 성장을 지원하고 있습니다. 병원, 진료소, 그리고 빠르게 성장하고 있는 재택 검사 채널에서 분자진단 및 면역학 검사가 일상적인 진료에 통합되고 있습니다. 한편, 실험실 개발 검사(LDT)에 대한 새로운 FDA 규제는 향후 경쟁 진입 및 컴플라이언스 관련 지출의 방향을 결정하고 있습니다. 검사 데이터를 실시간으로 해석하는 인공지능(AI) 모델, 클라우드 네이티브 검사 정보 시스템, 검사 소요 시간을 단축하는 멀티플렉스 패널은 인력 부족에도 불구하고 검사량 증가에 대응할 수 있는 검사실 운영을 지원합니다. 이를 통해 미국 체외진단 시장은 정밀의료, 감염병 모니터링, 분산형 의료 제공의 중요한 기반으로서 입지를 강화하고 있습니다.

당뇨병은 현재 미국 성인의 15.8%가 앓고 있으며, 2050년까지 심혈관 질환이 1억 8,400만 명에게 영향을 미칠 수 있다는 예측이 있습니다. 여러 만성질환이 이미 성인의 76.4%에게 영향을 미치고 있으며, 중복되는 대사, 심장, 염증 바이오마커를 모니터링하는 통합 패널에 대한 수요는 계속 증가하고 있습니다. 분자진단 및 면역측정이 조기 발견에 가져다주는 이점은 더 빠른 개입, 건강 수명 연장, 재입원율 감소로 이어집니다. 베이비붐 세대가 고발병 연령대에 접어들면서 검사기관은 고처리량 화학검사, 헤모글로빈 A1c, 트로포닌 검사 역량을 확대하고 있으며, 미국 체외진단 시장은 예방의료의 중요한 축으로 입지를 강화하고 있습니다.

이번 팬데믹은 병상 진단이 선별진료 시간을 몇 시간에서 몇 분으로 단축할 수 있다는 점을 부각시켰습니다. FDA의 2024년 가정용 성병 검사 패널과 인플루엔자/COVID-19 복합 검사 키트의 승인은 분산형 검사 모델의 유효성을 입증했습니다. 대도시 지역의 네트워크에서 POC 트로포닌 D 다이머 CRP 검사가 센트럴 랩 워크플로우를 대체할 경우, 응급실에서의 판단 시간이 35-45분 단축된 것으로 보고되었습니다. 전자 건강 기록과 동기화되는 AI 기반 리더기는 실시간 병원체 식별과 가이드라인에 따른 치료 권장 사항을 대조하여 항균제의 올바른 사용을 지원함으로써 사이클 타임을 더욱 단축할 수 있습니다. 미국 체외진단 시장에서는 상환 코드가 정비됨에 따라 당뇨병, 심부전, 신장 질환에 대한 만성 치료 경로에 POC 검사가 포함되고 있습니다.

2024년 4월 최종 규칙에 따라 일반 집행 재량권이 단계적으로 폐지되고 LDT 제조업체는 시판 전 신청서 제출, 품질 시스템 유지, 부작용 보고가 의무화됩니다. 규제 준수 비용은 연간 35억 6,000만 달러에 달할 수 있으며, 소규모 전문 실험실에 미치는 영향이 가장 심각할 것으로 예측됩니다. 2025년 5월부터 시행되는 1단계 규정에서 검사실은 이미 민원 파일과 장비 보고를 공식화하도록 요구받고 있습니다. 업계 단체의 법적 이슈는 불확실성을 야기하고, 투자 결정을 지연시키며, 일반적으로 시장의 혁신 주기를 혁신하는 틈새 유전자 패널의 출시를 늦추고 있습니다. 단기적으로는 등록 절차의 병목현상이 미국 체외진단 시장 연평균 성장률(CAGR)을 낮출 것으로 예측됩니다.

분자진단은 2025년 미국 체외진단 시장 점유율의 31.62%를 차지하며 COVID-19 모니터링, 종양 프로파일링, 항균제 내성 추적에서 핵심적인 역할을 할 것으로 예상했습니다. 면역 진단은 8.32%의 예상 CAGR을 나타낼 것으로 예측됩니다. 자가면역질환, 신경퇴행성 질환 및 치료 모니터링의 확대로 항체 기반 검사 포트폴리오가 확대되고 있기 때문입니다. 임상화학은 기초대사 패널을 지원하고, 혈액학은 자동응고검사 및 세포 이미징 모듈의 보급으로 성장이 예상됩니다. 미생물학은 감염관리 판단의 기반이 되는 신속한 병원체 동정을 통해 그 중요성을 유지하고 있습니다.

차세대 시퀀싱의 지속적인 비용 절감, 방울 디지털 PCR의 정확도 향상, AI를 활용한 변이체 분석으로 분자 플랫폼은 빠른 혁신의 속도를 유지하고 있습니다. 극히 낮은 알레르기의 빈도로 유리 DNA 단편을 검출하는 액체생검 패널과 같은 획기적인 기술은 침습적인 조직 생검에 대한 의존도를 낮춰줍니다. 이러한 모멘텀으로 미국 체외진단 시장은 정밀진단의 세계 벤치마킹 시장으로 자리매김하고 있습니다. 한편, 면역진단 분야에서는 다중 비드 어레이 및 화학발광 분석법을 활용한 바이오마커 검출의 확대로 자가면역질환 및 신경질환 영역에서 두 자릿수 성장세를 유지하고 있습니다.

시약 및 키트는 2025년 미국 체외진단 시장 규모의 61.78%를 차지할 것으로 예상되며, 검사량 증가에 따라 제조업체에 예측 가능한 보충 매출을 가져다 줄 것입니다. 장비는 검사실 자동화 사이클에 힘입어 두 번째로 큰 기여를 하는 분야가 되었습니다. 그러나 소프트웨어 서비스는 9.41%의 연평균 복합 성장률(CAGR)을 보이고, 시장을 선도하고 있습니다. 이는 검사실이 처리 능력과 인력 배치의 제약에 대응하기 위해 클라우드 분석, 원격 교정, AI를 통한 품질관리 대시보드를 활용하기 시작했기 때문입니다.

독립형 미들웨어는 검체 접수 조정, 시약 로트 추적, 전자 건강 기록에 대한 실시간 결과 전송을 통합하는 실험실 정보 관리 시스템(LIMS)으로 진화하고 있습니다. 벤더는 위험값 플래그 지정, 동향 비교, 반사적 검사 경로를 제안하는 구독 가격 의사결정 지원 알고리즘을 번들로 제공합니다. 이 디지털 계층은 공급업체 간 차별화와 전환 비용의 심화를 가져왔고, 미국 체외진단 시장에서 장기적인 고객 충성도를 정착시키고 있습니다.

USA in vitro diagnostics market size in 2026 is estimated at USD 45.5 billion, growing from 2025 value of USD 43.13 billion with 2031 projections showing USD 59.5 billion, growing at 5.51% CAGR over 2026-2031.

A balanced mix of demographic aging, wider chronic-disease burden, and permanent adoption of point-of-care (POC) technologies supports this steady climb. Hospitals, clinics, and a fast-growing home-testing channel now embed molecular and immuno-based assays into routine care, while new FDA regulations around laboratory-developed tests (LDTs) shape future competitive entry and compliance spending. Artificial intelligence (AI) models that interpret assay data in real time, cloud-native laboratory information systems, and multiplex panels that shorten turnaround times all help laboratories manage rising test volumes despite workforce shortages. Together, they reinforce the USA in vitro diagnostics market as a critical foundation for precision medicine, infection surveillance, and decentralized care delivery.

Diabetes now affects 15.8% of US adults, while projections indicate that cardiovascular disease could impact 184 million people by 2050. As multiple chronic conditions already touch 76.4% of adults, demand for integrated panels that monitor overlapping metabolic, cardiac, and inflammatory biomarkers continues to rise. The edge that molecular and immuno-assays provide in early detection translates into faster intervention, longer healthy life expectancy, and lower hospital readmission rates. With baby-boomers entering ages of higher disease incidence, laboratories expand capacity for high-throughput chemistry, hemoglobin A1c, and troponin testing, reinforcing the USA in vitro diagnostics market as an essential pillar of preventive medicine.

The pandemic underscored how bedside diagnostics can shorten triage times from hours to minutes. FDA's 2024 authorization of home STI panels and combination flu/COVID-19 kits validated distributed testing models. Large urban networks report emergency-department decision time savings of 35-45 minutes when POC troponin, D-dimer, and CRP tests replace central-lab workflows. AI-enabled readers that sync to electronic health records further compress cycle times and support antimicrobial stewardship by matching real-time pathogen identification with guideline-based therapy recommendations. As reimbursement codes catch up, the USA in vitro diagnostics market embeds POC testing into chronic-care pathways for diabetes, heart failure, and kidney disease.

The April 2024 final rule phases out general enforcement discretion, requiring LDT makers to file pre-market submissions, maintain quality systems, and report adverse events. Compliance costs could reach USD 3.56 billion annually, hitting small specialty labs hardest. Stage 1 rules that take effect in May 2025 already force labs to formalize complaint files and device reports. Legal challenges by trade groups inject uncertainty, delaying investment decisions and slowing the roll-out of niche genetic panels that normally refresh market innovation cycles. Over the near term, registration bottlenecks trim the USA in vitro diagnostics market CAGR.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Molecular diagnostics delivered 31.62% of USA in vitro diagnostics market share in 2025, underscoring its centrality to COVID-19 surveillance, oncology profiling, and antimicrobial resistance tracking. Immuno-diagnostics follows with an 8.32% forecast CAGR as auto-immune disorders, neuro-degenerative conditions, and companion therapeutic monitoring expand antibody-based testing portfolios. Clinical chemistry anchors basic metabolic panels, while hematology gains from automated coagulation and cell-imaging modules. Microbiology retains relevance through rapid pathogen identification that feeds infection-control decisions.

Continual next-generation sequencing cost compression, droplet digital PCR accuracy gains, and AI-powered variant interpretation keep molecular platforms on a rapid innovation cadence. Breakthroughs such as liquid biopsy panels that detect cell-free DNA fragments at very low allele frequencies reduce reliance on invasive tissue biopsies. This momentum positions the USA in vitro diagnostics market as a global benchmark for precision diagnostics, while immuno-diagnostics leverages multiplexed bead arrays and chemiluminescent assays for expanded biomarker detection, sustaining double-digit growth across autoimmune and neuro-logical applications.

Reagents and kits provided 61.78% of the USA in vitro diagnostics market size in 2025, generating predictable replenishment revenue for manufacturers as test volumes climb. Instruments represent the second-largest contribution, driven by laboratory automation cycles. Software & services, however, register a market-leading 9.41% CAGR because laboratories now tap cloud analytics, remote calibration, and AI-guided quality-control dashboards to address throughput and staffing constraints.

Standalone middleware morphs into integrated laboratory information management systems (LIMS) that orchestrate sample accessioning, track reagent lots, and push results to electronic health records in real time. Vendors bundle subscription-priced decision-support algorithms that flag critical values, compare trends, and suggest reflex testing pathways. This digital layer differentiates suppliers and deepens switching costs, embedding long-term loyalty within the USA in vitro diagnostics market.

The United States in Vitro Diagnostics Market Report is Segmented by Test Type (Clinical Chemistry, Molecular Diagnostics, Hematology, and More), Product (Instruments, Reagents & Kits, and More), Usability (Disposable IVD and Reusable IVD), Application (Infectious Diseases, Diabetes, Oncology, and More), and End User (Diagnostic Laboratories, Hospitals & Clinics, and More). The Market Forecasts are Provided in Terms of Value (USD).