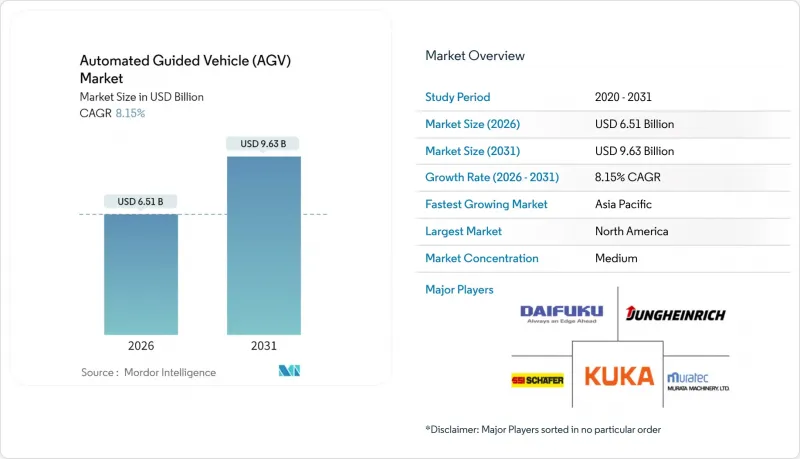

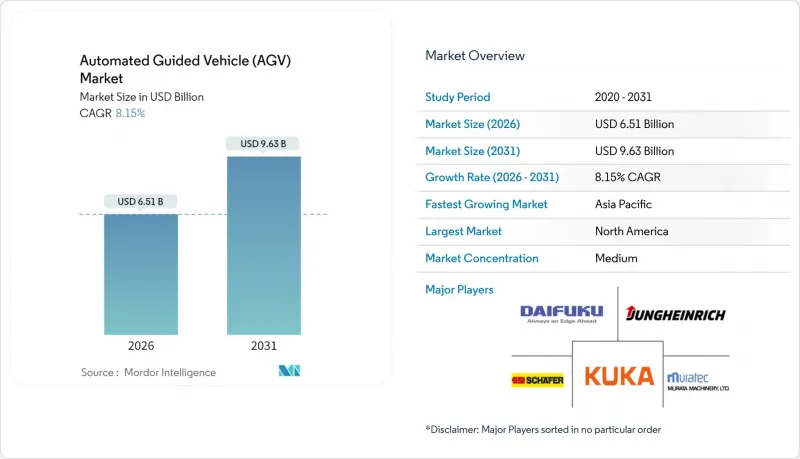

무인운반차(AGV) 시장은 2025년 60억 2,000만 달러에서 2026년에는 65억 1,000만 달러로 성장하며, 2026-2031년에 CAGR 8.15%로 추이하며, 2031년까지 96억 3,000만 달러에 달할 것으로 예측됩니다.

이러한 성장 궤적을 지원하는 것은 E-Commerce의 주문 폭증, 지속적인 인력 부족, 그리고 24시간 오류 없는 자재 운반의 필요성입니다. 성수기에는 주문량이 300-400% 증가할 수 있고, 기존의 수동 프로세스으로는 대응할 수 없는 수준이기 때문에 사업자들은 자율 이동 차량군 도입에 눈을 돌리고 있습니다. 프라이빗 5G 네트워크는 AGV가 요구하는 확정적인 연결성을 제공하며, 도입 초기 단계에서 Wi-Fi 대비 20%의 생산성 향상과 15%의 설비 투자 절감을 실현합니다. AI 기반 내비게이션, 특히 시각적 SLAM은 도입 시간을 20% 단축하고, 물리적 가이드 없이 레이아웃을 재구성할 수 있게 해줍니다. 사이버 보안에 대한 관심 증가와 희토류 공급 제약에 대한 우려로 인해 열기가 식었지만, 이 두 가지 위험은 지금까지의 조달 속도를 늦추지 않았습니다.

옴니채널 리테일의 발전으로 AGV 시장은 효율성 향상을 넘어 비즈니스 연속성 영역으로 확대되고 있습니다. 피킹 작업이 창고 비용의 약 55%를 차지하므로 크로거, 오카도 등 대형 유통업체들은 당일 배송 약속을 지키기 위해 상품 운반 로봇의 보유 대수를 4배로 늘리고 있습니다. AGV와 창고 관리 소프트웨어의 실시간 연동으로 자재관리 비용이 70% 절감되었습니다. 1,000평방미터 미만의 도심형 마이크로 풀필먼트 거점은 좁은 통로에서도 이동이 가능한 소형 AGV의 등장으로 가능해졌습니다. 모듈식 조달 모델을 통해 소규모 사업자도 주문량 증가에 따라 차량을 추가할 수 있으며, 막대한 선투자 리스크를 피할 수 있습니다. 이러한 변화로 인해 자동운반차 시장은 EC의 성장을 배경으로 계속 확대되고 있습니다.

창고업계의 이직률은 항상 75% 이상이며, 2030년까지 전 세계에서 8,500만 명의 인력이 부족할 것으로 예상되고 있습니다. 일본에서는 1,500만 엔에 달하는 자율주행 지게차가 노동력 공급망 붕괴로 인해 여전히 수동식 유닛을 능가하는 경쟁력을 발휘하고 있습니다. 도입 사례에서 최단 8개월 만에 투자 회수가 확인되어 AGV의 내부이익률(IRR)의 우수성을 입증하고 있습니다. 피로감 없는 24시간 가동은 추가적인 부가가치를 창출하고, 인간과 로봇이 결합된 하이브리드 노동력은 처리 능력과 직원 만족도를 모두 향상시킵니다. 이러한 인력 부족으로 인해 많은 물류센터에서는 AGV 도입이 선택에서 필수로 전환되어 AGV 시장 전체의 성장을 촉진하고 있습니다.

초기 도입 비용은 5만-50만 달러에 달하며, 특히 차입 비용이 높을 경우 이익이 적은 기업에게는 부담이 될 수 있습니다. 그러나 AGV 도입시 IoT 재고 관리를 병행할 경우, 노동집약적인 이용 사례에서 8-18개월 만에 손익분기점에 도달하는 것으로 확인되었습니다. 서비스형 로봇(RaaS) 모델은 설비 투자를 크게 줄이고 지속적인 기술 지원을 통합합니다. Agility Robotics와 같은 벤더가 풀서비스 계약을 주도하고 있습니다. 북미와 EU에서는 최대 10%의 R&D 세액 공제 및 청정산업 가이드라인에 따른 가속 상각 일정으로 자금 부담을 더욱 줄일 수 있습니다. 단기적인 마찰은 있지만, 자금 조달 혁신을 통해 중소기업은 이전 사이클보다 더 일찍 자동 운반차 시장에 진입할 수 있습니다.

유닛로드 플랫폼은 2025년 매출의 31.48%를 차지하며, 다목적 시설내 팔레트-컨테이너-토트 이동 능력으로 자동운반차 시장을 주도하고 있습니다. 자동 지게차 모델은 현재 규모가 작은 모델이며, 수직 운반 능력과 기존 랙 시스템과의 호환성에 대한 수요를 반영하여 8.54%의 연평균 복합 성장률(CAGR)이 예상됩니다. 견인 트랙터형은 중량감 있는 프레임 부품의 순차적 이송이 필요한 자동차 공장에서 보급되고 있으며, 조립라인 차량은 입자 없는 동작이 요구되는 전자기기 클린룸에서 입지를 다지고 있습니다.

토지가 제한된 도시 지역에서는 다층 창고가 증가하고 있으며, 듀얼 모드(수동/자율) 작동이 변경 관리 장벽을 완화하므로 수요는 지게차 유형 차량에 기울어지고 있습니다. 팔레트 트럭 AGV는 소매업체의 입고화물 처리의 첫 번째 자동화 단계이며, 카트 및 소하중 설계는 고빈도 EC 피킹에 적합합니다. 방폭 사양 및 제약 등급 유닛의 틈새 시장도 지속되고 있습니다. 이러한 추세는 전 제품군에 걸쳐 자동운반차 시장의 지속적인 성장을 지원하고 있습니다.

자동차 제조업체는 2025년 매출의 34.63%를 차지할 것으로 예상되며, AGV를 활용하여 적시 조립 공급 및 작업 완충을 위해 AGV를 활용하고 있습니다. 그러나 당일 배송이 소비자들에게 필수 조건이 되면서 소매 및 EC 유통센터는 8.18%의 연평균 복합 성장률(CAGR)로 타 업종을 상회하는 성장이 예상됩니다. 식품 및 음료 사업자들은 저온 환경에서의 인력 부족을 피하기 위해 냉장 구역에 AGV 도입을 확대하고 있습니다. 한편, 전자기기 제조업체들은 AGV에 mm 단위의 정밀한 서브 어셈블리의 포지셔닝을 활용하여 AGV의 광범위한 보급을 촉진하고 있습니다.

의약품 물류에서는 적정유통기준(GDP)에 대응하기 위해 AGV 도입이 증가하고 있으며, 서드파티 물류기업은 로봇군 도입 후 노동시간을 42% 줄였다고 보고하고 있습니다. 항공우주 분야에서는 기체 섹션의 엄격한 공차 관리가 요구되어 초중량 하중 설계의 AGV가 탄생하고 있습니다. 이러한 산업 전반의 변화는 고객 기반이 확대되는 것을 의미하며, 단일 업종에 대한 의존도를 높이지 않고 AGV 시장을 강화하는 데 기여하고 있습니다.

북미는 2025년 AGV 시장에서 37.07%의 매출 점유율을 유지했습니다. 이는 창고 노동자의 시급이 25달러를 넘고, 높은 이동 속도를 요구하는 EC 네트워크가 뿌리 깊게 자리 잡았기 때문입니다. 아마존, 월마트 등 주요 고객이 대규모로 로봇을 도입하는 모습을 보여주었고, 이것이 다운스트림 공급업체 생태계를 형성하고 있습니다. 미국에서는 재정적 인센티브, R&D 세액공제, 특별 상각제도를 통해 금리 상승 국면에서도 지속적인 자본 유입을 보장하고 있습니다. 한편, 캐나다에서는 냉장창고 및 자원 부문의 물류 분야에서 AGV 도입이 진행되고 있습니다.

아시아태평양은 2031년까지 연평균 복합 성장률(CAGR) 8.36%로 가장 빠른 성장을 기록할 것으로 예측됩니다. 중국의 '다크 팩토리' 추진과 일본의 인구 구조로 인한 심각한 노동력 부족이 견인차 역할을 할 것입니다. 이 지역은 전 세계 955개 민간 5G 네트워크의 대부분을 보유하고 있으며, 지연에 민감한 AGV 제어를 지원하는 연결성에서 우위를 점하고 있습니다. 인도의 생산연계형 인센티브 제도와 아세안공급망 다변화가 자동화에 적합한 새로운 그린필드 사이트를 추가하고 있습니다.

유럽은 지속가능성을 중시하는 꾸준한 성장이 예상됩니다. 유럽연합 집행위원회의 '청정산업 전환 가이드라인'은 로봇 설비의 감가상각을 가속화하고 에너지 집약적인 수작업 공정을 대체하는 것을 촉진하고 있습니다. 독일의 자동차 및 기계 산업에서는 AGV를 핵심으로 하는 종합적인 인더스트리 4.0 아키텍처를 채택하고 있으며, 영국에서는 주요 도시권을 둘러싼 물류 허브의 정비가 우선시되고 있습니다. 중동, 아프리카, 남미는 개발도상국이지만 광업, 항만, 석유화학 분야에서의 안전성 이점이 투자를 정당화할 수 있는 매력적인 시장으로 세계 무인운반차(AGV) 시장 확대에 기여하고 있습니다.

The Automated Guided Vehicle market is expected to grow from USD 6.02 billion in 2025 to USD 6.51 billion in 2026 and is forecast to reach USD 9.63 billion by 2031 at 8.15% CAGR over 2026-2031.

Intensifying e-commerce order spikes, persistent labor shortages, and the need for round-the-clock, error-free material handling are underpinning this trajectory. Operators are turning to autonomous mobile fleets because peak-season order volumes can climb 300-400%, a level traditional manual processes cannot sustain. Private 5G networks now provide the deterministic connectivity AGVs require, delivering 20% productivity gains and 15% lower capex than Wi-Fi in early rollouts. AI-enabled navigation, most notably Visual SLAM, cuts commissioning time by 20% and allows layout re-configuration without physical guides. Heightened cybersecurity focus and looming rare-earth supply constraints temper enthusiasm, yet neither risk has slowed procurement to date.

Omnichannel retail has pushed the automated guided vehicle market beyond efficiency gains and into business-continuity territory. Picking functions absorb roughly 55% of warehousing costs, prompting Kroger, Ocado and other large retailers to quadruple their fleets of goods-to-person robots to keep same-day-delivery promises. Real-time links between AGVs and warehouse-management software are trimming material-handling expenses by 70%. Urban micro-fulfillment sites, often below 1,000 m2, have become viable thanks to slimmer AGV form factors that maneuver in tight corridors. Modular procurement models allow smaller merchants to add vehicles as order volumes escalate, insulating them from large upfront bets. Collectively, these changes ensure the automated guided vehicle market continues scaling on the back of e-commerce growth.

Warehousing attrition routinely exceeds 75%, and a global shortfall of 85 million workers is expected by 2030. In Japan, autonomous forklifts priced at 15 million yen still outcompete manual units because the labor pipeline is crumbling. Documented installations show payback in as little as eight months, strengthening the internal-rate-of-return case for AGVs. Round-the-clock operation without fatigue adds further value, while hybrid workforces pairing people with robots improve both throughput and job satisfaction. Labor scarcity therefore shifts AGV adoption from discretionary to mandatory in many distribution centers, powering growth across the automated guided vehicle market.

Initial deployments range from USD 50,000 to USD 500,000 and can strain thin margins, especially where borrowing costs run high. Documented labor-intensive use cases, however, hit breakeven in 8-18 months when IoT inventory control accompanies the AGV rollout. Robots-as-a-Service models slash capex and embed ongoing technical support, with vendors such as Agility Robotics spearheading full-service contracts. R&D tax credits worth up to 10% and accelerated depreciation schedules under clean-industry guidelines further lighten cash burdens in North America and the EU. Despite near-term friction, financing innovations help SMEs enter the automated guided vehicle market sooner than in earlier cycles.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Unit-Load platforms captured 31.48% of 2025 sales, anchoring the automated guided vehicle market with their ability to move pallets, containers and totes across multipurpose facilities. Automated Forklift models, though smaller at present, are projected for an 8.54% CAGR, reflecting demand for vertical-reach capability and compatibility with existing racking systems. Tow-tractor variants thrive in automotive plants where heavy framed components require sequential transfer, whereas assembly-line vehicles gain ground in electronics clean rooms that favor particle-free motion.

Demand is tilting toward forklift-style vehicles because multilevel warehouses proliferate in land-constrained cities and because dual-mode manual/autonomous operation eases change-management hurdles. Pallet-truck AGVs remain the first automation step for retailers handling inbound freight, while cart and small-load designs suit high-frequency e-commerce picks. Niche opportunities endure for explosion-proof and pharmaceutical-grade units. Collectively, these dynamics underpin sustained growth of the automated guided vehicle market across all product lines.

Automotive manufacturers owned 34.63% of 2025 turnover, using AGVs to feed just-in-time assembly and reduce work-in-process buffers. Yet retail and e-commerce distribution centers should outpace every other vertical at an 8.18% CAGR as same-day delivery becomes non-negotiable for consumers. Food-and-beverage operators extend AGV use into refrigerated zones to sidestep labor shortages in cold environments, while electronics producers exploit millimeter-level positioning for fragile sub-assemblies, reinforcing broader adoption in the automated guided vehicles market.

Pharmaceutical logistics increasingly turns to AGVs to comply with Good Distribution Practices, and third-party logistics firms report 42% labor-hour savings after installing robot fleets. Aerospace adopters demand tight tolerance handling for fuselage sections, spawning ultra-heavy-duty designs. These cross-industry shifts indicate a broadening customer base that strengthens the automated guided vehicle market without over-reliance on any single vertical.

The Automated Guided Vehicle (AGV) Market Report is Segmented by Product Type (Automated Forklift, Tow/Tractor/Tug, and More), End-User Industry (Automotive, Food and Beverage, and More), Payload Capacity (Less Than 500 Kg, 500-1, 000 Kg, 1, 000-2, 000 Kg, and More), Application (Material Handling and Transportation, Order Picking and Sortation, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America retained 37.07% revenue share in 2025 in the AVG market due to hourly warehouse wages exceeding USD 25 and deeply entrenched e-commerce networks that demand high fulfillment velocity. Anchor customers such as Amazon and Walmart validate large-scale robotic deployments, which in turn create downstream supplier ecosystems. U.S. fiscal incentive, R&D credits and bonus depreciation schedules, ensure continued capital inflows even as interest rates rise, while Canada favors AGVs for cold-storage and resource-sector logistics.

Asia Pacific will log the fastest 8.36% CAGR through 2031, led by China's "dark factory" push and Japan's acute demographic-driven labor crunch. The region boasts the bulk of the world's 955 private 5G networks, a connectivity edge supporting latency-sensitive AGV controls. India's production-linked incentive schemes and ASEAN supply-chain diversification add new greenfield sites primed for automation.

Europe presents a steady, sustainability-oriented profile. The European Commission's Clean Industrial Transition guidelines extend accelerated depreciation to robotics, accelerating replacement of energy-intensive manual processes. Germany's automotive and machinery sectors adopt holistic Industry 4.0 architectures with AGVs at the core, while the United Kingdom prioritizes logistics hubs ringing major metropolitan areas. The Middle East, Africa and South America remain nascent but attractive for applications in mining, ports and petrochemicals where safety benefits justify investment, expanding the global automated guided vehicle market footprint.