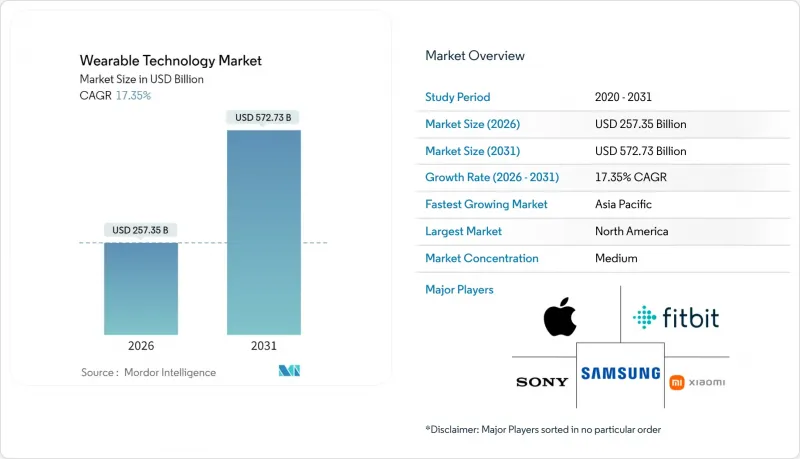

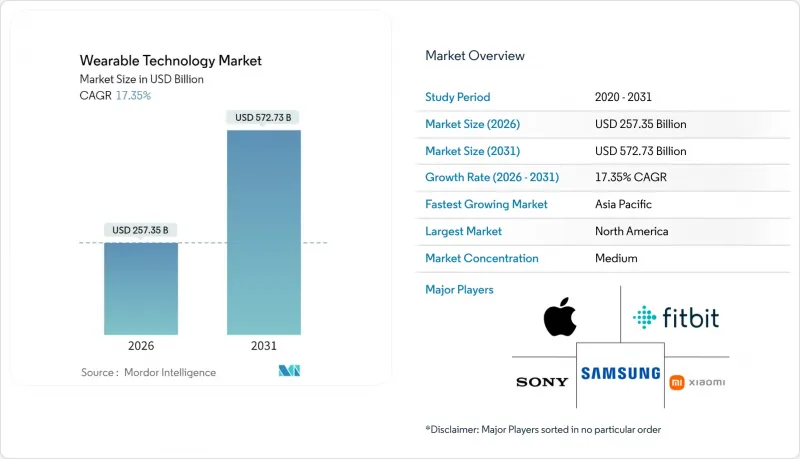

웨어러블 테크놀러지 시장은 2025년 2,193억 달러에서 2026년에는 2,573억 5,000만 달러로 성장하며, 2026-2031년에 CAGR 17.35%로 추이하며, 2031년까지 5,727억 3,000만 달러에 달할 것으로 예측됩니다.

이는 이 분야의 급속한 규모 확대와 센서가 풍부한 커넥티드 디바이스의 상업적 타당성을 지원합니다. 이 모멘텀은 AI 기반 의료용 웨어러블 기기의 FDA 승인, 증강현실 헤드셋에 대한 기업 지출, 수년간의 전력 밀도 제약을 완화하는 고체 배터리의 획기적인 발전에 기인합니다. 북미가 가장 큰 수입원을 차지하고 있지만, 부품 제조의 현지화 및 정부의 의료 서비스 제공의 디지털화가 진행되고 있는 아시아태평양이 가장 빠르게 성장하고 있습니다. 디바이스 분야에서는 스마트 워치가 선두를 지키고 있지만, 일선 종사자들의 도입에 힘입어 헤드마운트 디스플레이의 보급률이 가장 가파르게 성장하고 있습니다. 경쟁은 하드웨어 차별화에서 생태계 지배로 옮겨가고 있으며, 칩, 소프트웨어, 서비스를 가장 긴밀하게 통합하는 기업이 가치의 대부분을 차지하고 있습니다.

규제 당국은 AI 기반 바이오센서의 승인을 앞당기고 있으며, 웨어러블을 예방 의료의 의사결정 지원 툴로 인식하고 있습니다. FDA의 디지털 헬스 우수성 센터는 심사 과정을 간소화하고, 트리니티 바이오텍(Trinity Biotech)과 같은 혁신 기업은 대사 데이터와 예측 분석을 결합한 지속형 혈당 모니터를 출시했습니다. 한국과학기술원(KAIST)과 홍콩대학의 학술 그룹은 카프리스 혈압 측정 모듈과 유기 트랜지스터 어레이의 상용화를 추진하고 있습니다. 이는 데이터를 로컬에서 처리하므로 지연을 줄이고 프라이버시를 보호합니다. 이러한 발전으로 소비자 피트니스 장비와 임상 진단 장비의 차이가 줄어들고 보험사도 원격 모니터링 서비스에 대한 보험금 지급에 대한 확신을 가질 수 있게 되었습니다. 병원은 이 기술을 조기 개입과 비용 절감의 수단으로 인식하고 있으며, 웨어러블 기술 시장의 잠재적 고객 기반을 더욱 확대하고 있습니다.

산업용 증강현실(AR) 헤드셋은 위험한 환경이나 분산된 환경에서 효율성을 향상시킵니다. 코르게이트 팔몰리브는 63건의 가상 협업을 통해 출장 비용과 다운타임을 줄였습니다. 쉘은 12개국에서 본질안전 방폭형 AR 웨어러블을 도입하여 폭발 위험 지역에서의 유지보수를 지원했습니다. 후지쯔, AR 가이던스 도입으로 조립 작업 19% 절감. 철강 제조업체 KSP는 헬멧 착용형 시각화 기술로 생산성을 40% 향상시켰습니다. 투자 회수 기간이 1년 미만인 경우가 많아 운용팀의 도입 판단을 용이하게 하고 있습니다. 원격 전문가 용도이 확대됨에 따라 기업은 규모에 따른 주문을 진행하고 있으며, 이는 웨어러블 기술 시장의 성장을 가속하고 있습니다.

웨어러블 단말기는 생체인식 데이터를 수집하므로 GDPR(EU 개인정보보호규정), 일리노이주 BIPA 등 엄격한 규제의 적용을 받습니다. 제조업체들은 동의 관리 기능이나 단말기내 익명화 기술을 내장해야 하므로 개발 비용 증가와 출시 일정 지연을 초래하고 있습니다. 국경 간 데이터 전송의 제한은 클라우드 분석을 더욱 복잡하게 만들고 있습니다. 법적 자원이 부족한 소규모 벤더들은 높은 컴플라이언스 비용 장벽으로 인해 신규 진입률을 억제하고 웨어러블 기술 시장의 성장을 둔화시키고 있습니다.

헤드 마운트 디스플레이는 2026-2031년 19.02%의 가장 빠른 CAGR을 기록했으나, 2025년 기준 스마트 워치는 웨어러블 기술 시장 점유율 45.60%로 가장 큰 비중을 차지했습니다. 이러한 모멘텀은 기업이 유지보수, 교육, 물류 관리에 핸즈프리 디스플레이를 도입함에 따라 전체 웨어러블 기술 시장 전체를 끌어올리고 있습니다. Meta는 2023년 하반기부터 200만 개의 Ray-Ban 스마트 글래스를 판매하여 연간 1,000만 개까지 규모를 확대하여 눈에 잘 띄지 않는 아이웨어에 대한 소비자 수요를 지원하고 있습니다. 구글이 워비 파커(Warby Parker)와 1억 5,000만 달러 규모의 제휴를 통해 스타일 선택의 폭을 넓히면서 패션 측면의 도입 장벽이 낮아지고 있습니다.

애플의 특허는 손목 착용형 기기에 대한 의존도를 낮출 수 있는 인이어형 건강진단 장치를 제안하고 있습니다. 스마트 의류는 아직 개발 단계에 있지만, 존스 홉킨스 대학의 섬유 배터리는 전자 섬유를 주류로 만들 수 있는 세탁 가능한 에너지 저장 장치를 제안하고 있습니다. 스마트 워치의 평균 판매 가격이 하락하는 가운데, 손목 밴드는 상품화 위험에 직면하고 있지만, 신경 입력 밴드는 AR 제어에 대한 틈새 수요를 유지하고 있습니다. 이러한 변화로 인해 웨어러블 기술 시장은 더욱 풍요로워지고 있습니다.

2세대 스마트 글래스는 휴대폰의 무선 기능과 마이크로 LED 디스플레이를 통합하여 휴대폰로 연결하지 않고도 알림 우선순위 지정, 내비게이션 오버레이, 실시간 번역을 할 수 있습니다. OEM은 대상 사용자층을 확대하기 위해 경량화 및 처방 렌즈 지원에 주력하고 있습니다. 이 카테고리의 급속한 규모 확대로 인해 디바이스의 다양성은 높게 유지될 것이며, 웨어러블 기술 시장은 계속 성장할 것입니다.

2025년 기준 웨어러블 기술 시장 규모에서 센서가 28.70%로 가장 큰 비중을 차지했습니다. 이는 멀티모달 데이터 스트림에 대한 수요를 반영합니다. 동시에, 고체 배터리는 19.85%의 연평균 복합 성장률(CAGR)로 모든 구성 요소를 능가하는 성장률을 보일 것으로 예상되며, 첨단 이용 사례를 지원하는 에너지 기반을 제공할 것입니다. TDK의 칩 스케일 배터리와 삼성의 1주일 지속형 프로토타입은 보다 안전한 화학적 구성으로 얇은 케이스를 구현할 수 있는 좋은 예입니다. 프로세서와 메모리는 3D 적층 기술의 물결에 편승하여 TSMC는 CPU, GPU, 메모리를 단일 기판에 통합하는 패널 레벨 패키징을 계획하고 있습니다.

디스플레이는 플렉서블 OLED와 마이크로 LED 형태로 전환하고, 곡면과 투명 표면을 구현하여 아이웨어와의 융합을 가능하게 합니다. 연결용 IC는 블루투스, Wi-Fi, UWB를 공동 실장하여 기판 레이아웃을 단순화하고 안테나 설치 면적을 줄였습니다. 소프트웨어 및 서비스는 가장 수익성이 높은 계층이며, 플랫폼 소유자는 구독을 통한 기능 제한을 강화하여 생태계를 공고히 하고 환승 비용을 높이고 있습니다. 따라서 웨어러블 기술 시장에서는 이익률과 판매량 모두 지속적으로 확대되고 있습니다.

북미는 2025년 매출의 31.70%를 차지할 것으로 예상되며, 이는 R&D 주도권, 벤처 자금의 두께, 유리한 상환 정책을 반영합니다. FDA는 2023년에 124개의 신규 기기를 승인하여 연간 최다 기록을 경신하며 상용화까지 걸리는 시간을 단축했습니다. 미국 다국적 기업의 기업용 AR 파일럿 사업은 하드웨어의 업데이트 주기를 안정화시키는 한 요인이 되고 있습니다. 그러나 높은 이탈률은 소비자 도입과 가치 제공에 있으며, 지속적인 과제를 보여주고 있습니다.

아시아태평양은 2026-2031년 연평균 20.25%의 성장률을 보이며 웨어러블 기술 시장의 주요 물량 견인차 역할을 할 것으로 예측됩니다. 중국의 디지털 헬스 정책 지원과 한국의 3nm 파운드리 및 고체전지 분야 리더십이 지역 공급망 자립화를 가속화하고 있습니다. 인도의 건강에 대한 의식이 높은 중산층과 일본의 고령화 인구가 수요 곡선을 더욱 끌어올리고 있습니다. TSMC의 애리조나 및 쿠마모토 신공장은 내결함성을 강화하는 동시에 주요 공정 노하우를 지역 내에 보유하고 있습니다.

유럽에서는 엄격한 개인정보 보호 및 지속가능성 규제와 강력한 산업 자동화 수요가 균형을 이루고 있습니다. GDPR(EU 개인정보보호규정)과 WEEE 지침은 컴플라이언스 부담을 증가시키지만, 강력한 거버넌스를 갖춘 벤더에게는 경쟁 우위를 창출할 수 있는 기회이기도 합니다. 독일의 스마트팩토리 계획과 영국의 국민보건서비스(NHS)의 원격 모니터링 시범운영은 안정적인 기업용 파이프라인을 제공합니다. 중동, 아프리카, 남미의 소규모 시장은 인프라와 가처분 소득에서 뒤쳐져 있지만, 연결 비용의 하락과 현지 앱 생태계의 성숙에 따라 옵션 가치를 가지고 있습니다.

The wearable technology market is expected to grow from USD 219.30 billion in 2025 to USD 257.35 billion in 2026 and is forecast to reach USD 572.73 billion by 2031 at 17.35% CAGR over 2026-2031.

underscoring the sector's rapid scale-up and the commercial viability of sensor-rich connected devices. Momentum stems from FDA clearances for AI-enabled medical wearables, enterprise spending on augmented reality headsets, and solid-state battery breakthroughs that ease long-standing power-density constraints. North America accounts for the largest revenue pool, yet Asia-Pacific is expanding the fastest as component manufacturing localizes and governments digitize healthcare delivery. Device leadership remains with smartwatches, although head-mounted displays record the steepest uptake, buoyed by frontline workforce deployments. Competition has shifted from hardware differentiation to ecosystem control; the companies that integrate chips, software, and services most tightly are capturing a disproportionate share of value.

Regulators continue to fast-track AI-driven biosensors, positioning wearables as decision-support tools in preventive medicine. FDA's Digital Health Center of Excellence has streamlined review pathways, and innovators such as Trinity Biotech have launched continuous glucose monitors that fuse metabolic data with predictive analytics. Academic groups at KAIST and the University of Hong Kong are commercializing cuff-less blood-pressure modules and organic transistor arrays that process data locally, reducing latency and safeguarding privacy. These advances narrow the gap between consumer fitness gadgets and clinical diagnostics, giving payers confidence to reimburse remote monitoring services. Hospitals view the technology as a route to earlier intervention and cost avoidance, further enlarging the addressable base for the wearable technology market.

Industrial augmented reality headsets improve efficiency in hazardous or distributed settings. Colgate-Palmolive logged 63 virtual collaborations that trimmed travel expenses and downtime, while Shell deployed intrinsically safe AR wearables across 12 countries to support maintenance in explosive zones. Fujitsu cut assembly tasks by 19% after integrating AR guidance, and steelmaker KSP achieved 40% productivity gains through helmet-mounted visualization. The payback period often falls below one year, making procurement straightforward for operations teams. As remote-expert applications expand, enterprises are ordering at scale, propelling the wearable technology market.

Wearables harvest biometrics that fall under stringent rules such as GDPR and Illinois BIPA. Manufacturers must embed consent management and on-device anonymization, raising development costs and delaying launch schedules. Cross-border data-transfer limits further complicate cloud analytics. Small vendors lacking legal resources face a higher cost-of-compliance hurdle, tempering new-entry rates and trimming growth for the wearable technology market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Head-mounted displays posted the fastest 19.02% CAGR over 2026-2031, yet smartwatches retained the largest 45.60% slice of the wearable technology market share in 2025. This momentum lifts the overall wearable technology market as enterprises adopt hands-free displays for maintenance, training, and logistics. Meta sold 2 million Ray-Ban smart glasses since late 2023 and is scaling to 10 million units annually, validating consumer appetite for discreet eyewear. Google's USD 150 million partnership with Warby Parker expands style options, lowering the fashion barrier to adoption.

Diversification is also visible in ear-wearables, where Apple patents point to in-ear health diagnostics that could reduce reliance on wrist devices. Although smart clothing remains nascent, Johns Hopkins' fiber batteries hint at washable energy storage that could mainstream e-textiles. Wristbands risk commoditization as smartwatch ASPs fall, but neural-input bands maintain niche demand for AR control. Collectively, these shifts enrich the wearable technology market.

Second-generation smart glasses integrate cellular radios and micro-LED displays, allowing notification triage, navigation overlays, and real-time translation without tethering to phones. OEMs focus on weight reduction and prescription-lens support to widen the addressable audience. The category's rapid scale will keep device diversity high, ensuring the wearable technology market continues to grow.

Sensors captured the largest 28.70% contribution to the wearable technology market size in 2025, reflecting the need for multi-modal data streams. At the same time, solid-state batteries are forecast to outpace all components with a 19.85% CAGR, providing the energy foundation for advanced use cases. TDK's chip-scale cells and Samsung's week-long prototypes illustrate how safer chemistries unlock slimmer enclosures. Processors and memory ride the 3D-stacking wave, with TSMC planning panel-level packaging that blends CPUs, GPUs, and memory on a single substrate.

Displays are shifting to flexible OLED and micro-LED formats, enabling curved and transparent surfaces that merge with eyewear. Connectivity ICs co-package Bluetooth, Wi-Fi, and UWB to simplify board layouts and shrink antenna footprints. Software and services represent the highest margin layer, and platform owners increasingly gate features behind subscriptions, cementing ecosystems and elevating switching costs. Both margin pools and unit volumes, therefore, continue to widen for the wearable technology market.

The Wearable Technology Market Report is Segmented by Device Type (Smart Watches, Ear-Wearables, Head-Mounted Displays, and More), Component (Processors and Memory, Sensors, Displays, Batteries, and More), Connectivity Technology (Bluetooth and BLE, Cellular LTE/5G, and More), End-User Industry (Consumer Electronics, Healthcare and Medical, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America generated 31.70% of 2025 revenue, reflecting R&D leadership, venture funding depth, and favourable reimbursement policy. The FDA authorized 124 novel devices in 2023, its highest annual total, shortening commercialization timelines. Enterprise AR pilots run by U.S. multinationals contribute to steady hardware refresh cycles. Nonetheless, elevated abandonment rates reveal ongoing gaps in consumer onboarding and value delivery.

Asia-Pacific is projected to expand at a 20.25% CAGR over 2026-2031, making it the primary volume engine for the wearable technology market. China's policy support for digital health and Korea's leadership in 3 nm foundry and solid-state batteries accelerate regional supply-chain self-sufficiency. India's fitness-aware middle class and Japan's aging population further stretch demand curves. TSMC's new fabs in Arizona and Kumamoto add resilience yet keep key process know-how in the region.

Europe balances strict privacy and sustainability rules with strong industrial automation demand. GDPR and the WEEE directive increase compliance burden but also create competitive moats for vendors with robust governance. Germany's smart-factory programs and the U.K.'s National Health Service pilots on remote monitoring offer stable enterprise pipelines. Smaller markets in the Middle East, Africa, and South America trail in infrastructure and discretionary income, yet they represent option value as connectivity costs fall, and local app ecosystems mature.