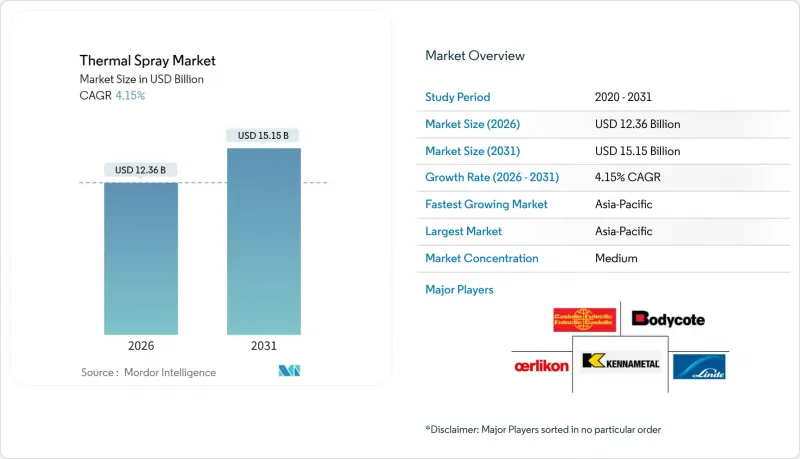

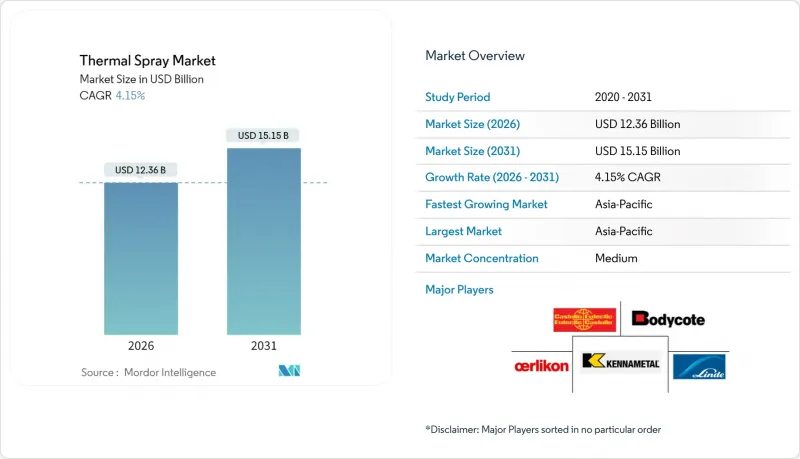

서멀 스프레이 시장은 2025년 118억 7,000만 달러에서 2026년에는 123억 6,000만 달러로 성장하며, 2026-2031년에 CAGR 4.15%로 추이하며, 2031년까지 151억 5,000만 달러에 달할 것으로 예측되고 있습니다.

항공우주, 의료기기, 차세대 자동차 제조업체들이 부품 수명 연장 및 열 관리 개선을 위해 기존 표면 처리를 고성능 코팅으로 대체하려는 움직임이 수요 증가의 요인으로 작용하고 있습니다. 자동화 설비와 실시간 공정 모니터링에 대한 투자는 숙련된 인력 부족을 완화하는 데 지속적으로 기여하고 있으며, 전기 에너지 분사 기술로의 전환은 점점 더 엄격해지는 환경 규제에 대한 대응과 일치합니다. 아시아태평양의 제조 기지는 빠르게 확장되고 있으며, 전자 및 전자 파워트레인 부품용 코팅 재료와 턴키 스프레이 셀의 지역 소비를 주도하고 있습니다.

열분무 방식의 하이드록시아파타이트 코팅은 뼈의 성장을 크게 촉진하고 거부반응률을 감소시켜 하중부하형 정형외과용 스크류, 인공고관절 스템, 치과용 픽스처의 표면 가공제로 최적입니다. 공정 제어를 통해 해면골 형태에 맞는 미세공 구조를 설계할 수 있으며, 골 결합을 가속화하고 재활 기간을 단축할 수 있습니다. 미국 FDA Class II 의료기기 및 CE 마킹 프레임워크의 규제 승인은 전 세계 임플란트 제조업체의 빠른 채택을 촉진하고 있습니다. 미국, 독일, 일본의 고령화 인구 증가에 따라 수술 건수는 지속적으로 증가하고 있으며, 인산칼슘 분말의 원료 수요는 지속적으로 증가하고 있습니다. 장비 공급업체는 현재 폐쇄 루프 로봇과 인라인 두께 게이지를 결합한 솔루션을 제공하여 반복성을 보장함으로써 외과 의사가 우려하는 코팅 박리 문제를 해결하고 있습니다. 병원이 감염 지표를 더욱 엄격하게 추적하는 가운데, 하이드록시아파타이트 표면의 생물학적 활성 특성은 추가적인 임상적 이점을 제공하여 열 스프레이 시장을 꾸준한 성장 궤도에 올려놓았습니다.

육가크롬에 대한 REACH 규제와 OSHA 규정이 강화됨에 따라 OEM 업체들은 대체 기술을 찾아야 하며, 고속 산소 연료(HVOF) 코팅은 지속가능한 대체 기술로서 자리매김하고 있습니다. HVOF 층은 일반적으로 60 HRC 이상의 경도를 달성하는 동시에 다공성을 1% 미만으로 감소시켜 유압 샤프트 및 압축기 임펠러의 부품 수명을 2배 이상 연장시킵니다. 유지보수 감소는 공정 산업에서 다운타임 비용 감소로 이어져 열 스프레이 시장 도입을 지원하는 총소유비용(TCO) 이점을 강화합니다. 자동 붐 매니퓰레이터에 의한 HVOF의 난접근공내 적용이 가능해져 대응 가능한 부품 범위가 확대되었습니다. 북미 석유 및 가스 시추 선단의 초기 전환 프로그램에서 18개월 미만의 투자 회수 기간을 입증하여 아시아 파운드리에서의 광범위한 도입을 촉진했습니다. ESG 감사 기관이 공급망 평가 기준을 강화하는 가운데, 크롬 욕조에서 무용제 스프레이 부스로의 전환은 배출량 감소에 있으며, 즉각적인 효과를 가져다 줄 수 있습니다.

차세대 삼가크롬욕은 보급형 HVOF 셀의 3분의 1의 투자로 50 HRC의 경도를 달성할 수 있으며, 비용에 민감한 소규모 유압로드 재생업체에게 매력적인 가치 제안이 될 수 있습니다. 공급업체는 기존 지그와의 호환성을 강조하며, 새로운 환기 시스템이나 집진 시스템 도입이 필요하지 않음을 강조하고 있습니다. 초기 현장 테스트 결과, 200℃ 이하에서 작동하는 기어 샤프트에 대한 허용 가능한 내식성이 확인되어, 이러한 틈새 시장에서 열 스프레이 시장의 단기적인 대체 수요를 둔화시키고 있습니다. 그러나 3가 크롬은 후막화가 어려워 연소 가스에 노출되는 부품에는 적용할 수 없습니다. 따라서 항공우주 분야와 석유 및 가스 펌프에서 내열 배리어 층과 내마모성 오버레이의 우위를 유지할 수 있습니다. 따라서 본 기술은 보편적인 위협이라기보다는 선택적 제약 요인으로 작용합니다.

장비 카테고리는 2031년까지 연평균 복합 성장률(CAGR) 6.06%로 확대될 것으로 예상되며, 2025년 전체 열 스프레이 시장에서 76.82%의 점유율을 유지한 코팅재를 능가하는 성장세를 보일 것으로 예측됩니다. 6축 로봇과 폐쇄 루프 질량 유량 제어를 갖춘 자동화 셀은 코팅 간 편차를 2µm 이하로 줄입니다. 이는 계획되지 않은 다운타임 제로를 목표로 하는 터빈 OEM(Original Equipment Manufacturer)가 설정한 요구 사항입니다.

분말과 와이어의 지속적인 매출은 여전히 매우 중요합니다. 왜냐하면, 증착되는 1kg마다 교체용 노즐과 플라즈마 전극에 대한 흡입 효과가 발생하기 때문입니다. 텅스텐 카바이드와 코발트 카바이드 분말은 마모 보호용 배합에서 여전히 주류이지만, 공급 부족과 가격 변동으로 인해 팁 수명을 연장하는 공정 레시피와 오버스프레이를 재활용하는 방법이 주목받고 있습니다. 공급업체는 현재 10분 이내에 미립자와 거친 입자를 전환할 수 있는 모듈식 피더 유닛을 홍보하고 있으며, 공장의 유연성을 높이고 있습니다. 소음저감부스와 사이클론식 집진기는 두 자릿수 성장률을 기록하고 있으며, 독일과 한국의 공장 안전 규제에 부합하는 부수적이면서도 수익성 높은 틈새 시장을 형성하고 있습니다.

열분무 보고서는 제품 유형별(코팅, 재료, 열분무 장비), 열분무 코팅 및 마감(연소 에너지 및 전기 에너지), 최종사용자 산업별(항공우주, 산업용 가스 터빈, 자동차, 전자, 석유 및 가스 등), 지역별(아시아, 북미, 유럽, 아시아태평양, 북미, 유럽, 중동 및 아프리카)), 지역(아시아태평양, 북미, 유럽, 유럽, 남미, 중동 및 아프리카)으로 분류됩니다. 시장 예측은 금액(USD)으로 제공됩니다.

아시아태평양은 2025년 열 스프레이 시장의 34.20%를 차지하며 4.98%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 이는 중국의 반도체 공장의 적극적인 국내 회귀와 일본의 첨단 배터리 공장의 진출이 반영된 결과입니다. 지역 정부는 스마트 기계 수입에 보조금을 투입하여 자동화 스프레이 부스 도입 장벽을 낮추고 있습니다. 그러나 숙련된 인력 부족은 여전히 존재하며, OEM 업체들은 ISO 14924 표준에 따라 운영자 인증을 제공하는 인도 및 말레이시아의 직업 훈련 기관과의 제휴를 추진하고 있습니다.

북미와 유럽은 기존 항공기 기체군 및 크롬 프리 도장을 권장하는 엄격한 산업 안전 가이드라인에 의해 지원되고 있습니다. 미국은 여전히 텅스텐 카바이드 분말의 최대 단일 국가 구매국이며, 독일은 플라즈마 토치 수출에서 선도적 인 위치에 있습니다. 두 지역 모두 수소 대응 코팅에 초점을 맞춘 연구개발에 투자하고 있습니다.

남미, 중동 및 아프리카는 절대적인 매출은 뒤쳐져 있지만, 석유화학 플랜트 업그레이드 및 광산 컨베이어 개조와 관련하여 꾸준히 두 자릿수 설비 수주를 기록하고 있습니다. 따라서 각 지역마다 최종 시장 요인에 따라 다른 방향으로 전개되고 있지만, 전 세계 열 스프레이 시장은 디지털화 및 환경 규제에 부합하는 표면 처리 솔루션이라는 공통된 궤도로 수렴하고 있습니다.

The Thermal Spray market is expected to grow from USD 11.87 billion in 2025 to USD 12.36 billion in 2026 and is forecast to reach USD 15.15 billion by 2031 at 4.15% CAGR over 2026-2031.

Demand is rising as aerospace, medical-device, and next-generation automotive manufacturers replace legacy surface treatments with high-performance coatings that extend part life and improve thermal management. Investments in automated equipment and real-time process monitoring continue to ease skilled-labor constraints, while the shift to electric energy spray techniques aligns with tightening environmental regulations. The Asia-Pacific manufacturing base is expanding rapidly, driving regional consumption of both coating materials and turnkey spray cells aimed at electronics and e-powertrain components.

Thermally-sprayed hydroxyapatite coatings significantly improve bone ingrowth and reduce rejection rates, making them the preferred surface finish for load-bearing orthopedic screws, hip stems, and dental fixtures. Process control enables tailored porosity that matches cancellous bone morphology, accelerating osseointegration and shortening rehabilitation periods. Regulatory acceptance under U.S. FDA class II devices and CE marking frameworks supports rapid adoption among global implant makers. Growing geriatric populations in the United States, Germany, and Japan keep procedural volumes expanding, sustaining raw-material demand for calcium-phosphate powders. Equipment suppliers now bundle closed-loop robots and inline thickness gauges that assure repeatability, addressing surgeon concerns regarding coating delamination. As hospitals track infection metrics more closely, the bioactive nature of hydroxyapatite surfaces provides an additional clinical advantage that keeps the thermal spray market on a steady upswing.

Tightening REACH and OSHA rules on hexavalent chromium have forced OEMs to seek alternatives, positioning high-velocity oxygen fuel (HVOF) coatings as the sustainable successor. HVOF layers routinely exceed 60 HRC hardness while slashing porosity below 1%, more than doubling component lifetimes for hydraulic shafts and compressor impellers. Reduced maintenance translates into lower down-time costs for process industries, bolstering the total cost-of-ownership argument in favor of thermal spray market adoption. Automated boom manipulators now apply HVOF inside hard-to-reach bores, extending the addressable part universe. Early conversion programs in North American oil-and-gas drill fleets demonstrated payback periods under 18 months, spurring wider replication in Asian foundries. As ESG auditors tighten supply-chain scorecards, the switch from chrome baths to solvent-free spray booths provides an immediate emissions win.

Next-generation trivalent chrome baths provide 50 HRC hardness at investment levels one-third those of an entry-level HVOF cell, a value proposition that appeals to small hydraulic-rod refurbishers in cost-sensitive markets. Suppliers emphasize drop-in compatibility with existing fixtures, eliminating the need for new ventilation or dust-collection systems. Early field results confirm acceptable corrosion resistance for gear shafts operating below 200 °C, blunting near-term replacements by the thermal spray market in those niches. However, trivalent chrome struggles at higher thicknesses and cannot serve components exposed to combustion gases, which preserves the advantage for thermal barrier and wear-resistant overlays in aerospace as well as oil-and-gas pumps. The technology therefore acts as a selective restraint rather than a universal threat.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The equipment category is projected to expand at a 6.06% CAGR through 2031, surpassing consumables in growth momentum even though coatings retained a 76.82% share of the overall thermal spray market in 2025. Automated cells equipped with six-axis robots and closed-loop mass-flow control reduce coat-to-coat variance below 2 µm, a requirement set by turbine OEMs aiming for zero unplanned downtime.

Recurring revenues from powders and wires remain pivotal, as every kilogram deposited creates a pull-through effect for replacement nozzles and plasma electrodes. Tungsten carbide-cobalt powders continue to dominate wear-protection formulas, but scarcity and price volatility have sparked process recipes that extend tip life or recycle overspray. Suppliers now promote modular feeder units that switch between fine and coarse fractions in under 10 minutes, enhancing shop flexibility. Noise-attenuating booths and cyclone-based dust collectors clock double-digit growth rates, an ancillary but lucrative niche aligned with factory-safety mandates in Germany and South Korea.

The Thermal Spray Report is Segmented by Product Type (Coatings, Materials, and Thermal-Spray Equipment), Thermal Spray Coatings and Finishes (Combustion and Electric Energy), End-User Industry (Aerospace, Industrial Gas Turbines, Automotive, Electronics, Oil and Gas, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific contributed 34.20% of the thermal spray market in 2025 and is forecast to climb at a 4.98% CAGR, reflecting aggressive onshoring of semiconductor fabs in China and advanced battery plants in Japan. Regional governments channel subsidies into smart-machinery imports, lowering payback barriers for automated spray booths. Still, the skilled-labor gap persists, pushing OEMs to partner with vocational institutes in India and Malaysia that offer operator certification under ISO 14924 standards.

North America and Europe are underpinned by legacy aerospace fleets and strict occupational safety guidelines favoring chrome-free overlays. The United States remains the largest single-country buyer of tungsten carbide powders, while Germany leads in plasma-torch exports. Both regions invest in research and development focused on hydrogen-compatible coatings.

South America and the Middle East and Africa trail in absolute revenues but post steady double-digit equipment orders linked to petrochemical plant upgrades and mining conveyor refurbishments. Each geography therefore plays to distinct end-market triggers, yet converges on a common trajectory of digitalized and environmentally compliant surface-engineering solutions within the global thermal spray market.