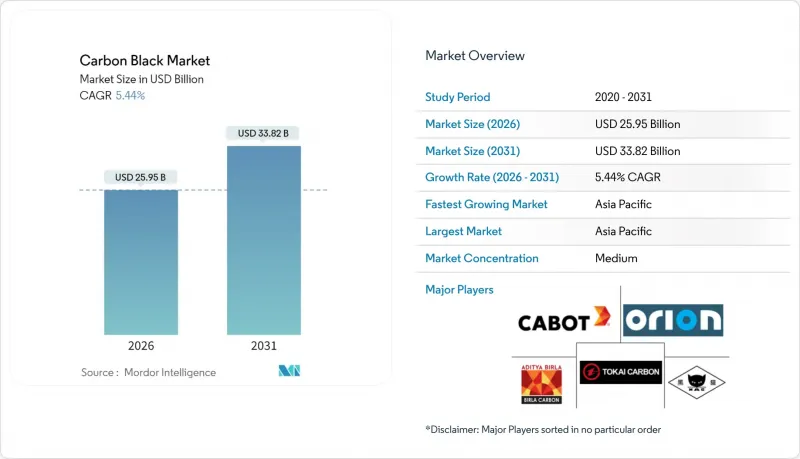

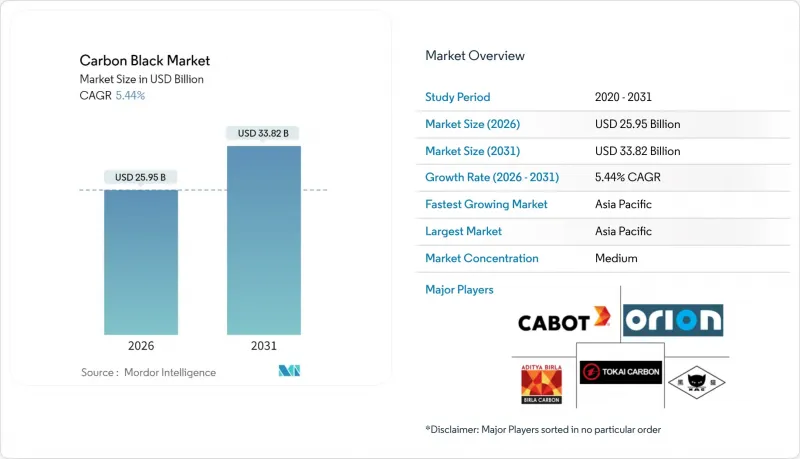

카본블랙 시장은 2025년 246억 1,000만 달러에서 2026년에는 259억 5,000만 달러로 성장하며, 2026-2031년에 CAGR 5.44%로 추이하며, 2031년까지 338억 2,000만 달러에 달할 것으로 예측되고 있습니다.

타이어 보강재, 플라스틱 컴파운딩, 배터리 전극, 고성능 코팅에 대한 강한 수요가 꾸준한 물량 성장을 지원하는 동시에 프리미엄 특수 등급의 단계적 믹스 시프트를 가능하게 하고 있습니다. 아시아태평양의 생산능력 확대가 생산 확대의 기반이 되고 있지만, 원자재 가격의 변동성과 지속가능성 요구사항 증가로 인해 생산업체들은 보다 엄격한 비용 관리와 공정 혁신을 도입해야 하는 상황입니다. 전기화의 진전은 전도성 등급의 채택을 가속화하고, 플라즈마 메탄 열분해와 같은 공정 혁신은 경쟁적 위치를 재구축하고 있습니다. 카본블랙 시장은 전통적 모빌리티 및 신흥 에너지 저장 밸류체인에서 중요한 재료 투입물로서 지속적으로 가치를 창출하고 있습니다.

중국, 인도, 동남아시아의 신규 타이어 공장은 다년간의 카본블랙 오프테이크 계약을 지속적으로 체결하여 예측 가능한 수요 패턴을 지원하고 있습니다. 요코하마 고무의 중국내 지속적인 생산능력 증설은 대규모 타이어 복합시설이 인근 카본블랙 생산시설에 대한 병행투자를 촉진하고 물류비용을 절감하는 동시에 적기 공급 모델을 촉진하는 좋은 사례입니다. 지역적 집적은 카본블랙 수요 밀도를 높이고, 용광로 흑색 안료 제조업체에 유리한 규모의 경제를 지원합니다. ISO 14001 인증을 획득한 공급업체는 우선 공급업체로서의 지위를 확보하고, 환경규제를 준수하는 시설들 사이에서 점유율을 공고히 하고 있습니다. 따라서 타이어 생산량과 카본블랙 소비량의 구조적 연동성은 매출 사이클을 평준화하고 장기적인 자본 계획을 지원하는 수요를 지원할 수 있습니다.

OEM(Original Equipment Manufacturer)가 요구하는 낮은 구름 저항과 높은 전도성으로 인해 타이어 제조업체는 범용 노내 흑색 안료보다 40-60% 더 비싼 엔지니어링 등급을 채택할 수밖에 없습니다. 이러한 특수 배합은 연비 향상과 트레드 수명 연장을 실현하여 추가 비용보다 측정 가능한 성능 향상을 가져옵니다. 독자적인 표면 개질 기술 및 초청정 노 설계에 투자하는 제조업체는 고매출 틈새 시장에서 지속가능한 우위를 확보할 수 있습니다. 기술적 차별화와 고객 인증 프로토콜은 전환 비용을 발생시키고, 공급자의 락인(Lock-in)을 강화합니다. 한편, 카본블랙 시장에서 특수품 출하 비중은 매년 꾸준히 증가하고 있습니다. 연구개발팀과 타이어 설계자의 긴밀한 협력으로 고급 등급으로의 전환을 가속화하고 있습니다.

카본블랙 생산은 석탄 타르, 잔류 연료유 등 탄소계 원료에 크게 의존하고 있으며, 총 운영비용의 최대 50%를 차지할 수 있습니다. 탄소 및 흑연 제품 생산자 물가지수는 2024년 말까지 급등하여 계약상 전가 조항이 발효되기 전에 마진을 압박했습니다. 수입에 의존하는 공장은 추가적인 운임 리스크에 직면하여 지역 간 가격 차이가 확대되고 무역 흐름의 차익 거래에 영향을 미치고 있습니다. 장기 공급 계약을 맺은 통합 생산자는 매출을 부분적으로 보호할 수 있지만, 현물 구매자는 이익 변동에 영향을 받아 정비 계획과 가동률에 영향을 미칩니다. 따라서 카본블랙 시장 전체에서 현금흐름을 안정화하기 위해서는 효과적인 헤지 및 조달 전략이 여전히 필수적입니다.

노내 흑색은 2025년 매출의 76.30%를 차지할 것으로 예상되며, 타이어 및 고무품과 같은 핵심 분야에서 범용성과 경쟁력 있는 경제성을 보여주고 있습니다. 그러나 특수 공정이 보급됨에 따라 용광로 응용 분야의 카본블랙 시장 규모는 점진적으로 점유율이 감소하고 있습니다. 램프 블랙은 2031년까지 7.35%의 견고한 연평균 성장률(CAGR)을 보일 것으로 예상되며, 전자기기 및 에너지 저장 코팅에서 우수한 전기 전도성을 발휘하는 고유한 고표면적 형태가 장점입니다. 가스 블랙은 미세분산 잉크에 사용되며, 서멀 블랙은 낮은 구조를 필요로 하는 틈새 폴리머 블렌드에 활용됩니다. 플라즈마 메탄 기술의 혁신적인 도입은 OEM의 탄소 회계 프레임워크에 부합하는 저배출 경로를 제공하고 공정 선택권을 확대합니다.

경쟁 대응책으로는 기존 원자로 라인 내에서 세미 스페셜티 등급 생산이 가능한 모듈형 원자로 개조가 있습니다. 캐봇과 빌라카본은 새로운 공정을 도입하지 않고도 입자 크기 분포를 엄격하게 하고 구조 지수를 향상시키는 첨단 원료 주입 제어 기술을 시험하고 있습니다. 이러한 성공적인 적응을 통해 규모의 우위를 유지하면서 스페셜티 제품으로의 가치 전환을 포착할 수 있습니다. ASTM이 재생 카본블랙에 대한 통일된 분류를 개발함에 따라 용광로 제조업체는 화합물 성능을 손상시키지 않고 순환성 목표를 달성하기 위해 rCB(재생 카본블랙) 블렌딩 전략을 통합할 수 있습니다. 전반적으로 범용품 공정과 특수품 공정의 공존이 카본블랙 시장의 두 가지 성장 모델을 촉진하고 있습니다.

아시아태평양은 중국의 타이어 제조 집중과 인도의 특수 등급 확대에 힘입어 2025년 세계 매출의 61.85%를 차지하며 2031년까지 연평균 5.85%의 성장률을 보일 것으로 예측됩니다. 중국에서는 대규모 타이어 공장에 인접한 카본블랙 생산단지를 통합하여 원료 조달 및 물류 효율화를 통해 지역 경쟁력을 강화하고 있습니다. 인도의 히마돌리 스페셜티 케미칼(Himadri Specialty Chemicals)은 2024년 연간 7만 톤의 프리미엄 생산능력을 추가하여 범용 제품 공급에서 고성능 타이어 및 배터리 부품용 고부가가치 분말로의 전환을 시사하고 있습니다. 일본과 한국은 기술 리더십을 제공하고, 동남아시아 국가들은 비용 효율적인 노동력과 확대되는 국내 자동차 수요를 공급하고 있습니다.

북미에서는 교체용 타이어 수요, 고성능 코팅, 저배출 공정의 조기 도입으로 인해 성숙하면서도 안정적인 소비가 기록되고 있습니다. 모노리스 매트리얼즈의 네브래스카 플라즈마 시설은 친환경 조달 목표에 부합하는 대체 공급 기반을 도입하고, 캐봇 코퍼레이션은 미국 특수 공장을 활용하여 물량 감소 없이 인플레이션 비용을 전가하고 있습니다. 인플레이션 억제법의 배터리 우대 정책은 간접적으로 전도성 등급의 성장을 지원하여 이 지역의 카본블랙 시장에 구조적인 순풍을 가져다주었습니다.

유럽에서는 지속가능성과 특수 용도를 중시하고, 탄소 국경 조정 메커니즘을 통해 현지 생산 및 저탄소 공급업체로부터의 우선 조달을 장려하고 있습니다. 다환방향족탄화수소(PAH) 및 이산화탄소 배출량 제한으로 인해 구식 용광로의 현대화 또는 폐쇄가 가속화되고 있습니다. 첨단 후처리 시스템을 갖춘 생산자는 시장 접근성을 유지하고 규제 대응 비용을 상쇄하는 가격 프리미엄을 협상하고 있습니다.

남미, 중동, 아프리카는 총 점유율은 작지만, 자동차 조립 확대 및 광범위한 산업화에 따른 고성장 지역이 존재합니다. 브라질의 자동차 회복은 현지 타이어 생산을 견인하고 국내 카본블랙 생산 투자를 자극하고 있습니다. 중동의 기업은 석유화학 원료와의 통합을 활용하여 새로운 용광로 유닛을 제안하고 있지만, 다운스트림 수요는 여전히 아시아태평양 규모에 미치지 못하고 있습니다. 남아공의 도료 및 광업 분야에서는 특수 분산용 카본블랙에 대한 수요가 있지만, 환율 변동이 자본 계획에 영향을 미치고 있습니다. 이들 지역은 종합적으로 주요 시장이 성숙함에 따라 확장할 수 있는 옵션을 제공하고, 다각화된 생산자들이 세계 카본블랙 시장에서 지역적 순환의 균형을 맞출 수 있도록 합니다.

The Carbon Black market is expected to grow from USD 24.61 billion in 2025 to USD 25.95 billion in 2026 and is forecast to reach USD 33.82 billion by 2031 at 5.44% CAGR over 2026-2031.

Strong demand from tire reinforcement, plastics compounding, battery electrodes, and high-performance coatings anchors steady volume growth while enabling a gradual mix shift toward premium specialty grades. Capacity additions across Asia-Pacific underpin output expansion, yet feedstock volatility and rising sustainability requirements force producers to adopt tighter cost control and process innovation. Heightened electrification accelerates conductive grade uptake, and process breakthroughs such as plasma methane pyrolysis reshape competitive positioning. The carbon black market continues to capture value as a critical material input for traditional mobility and emerging energy storage supply chains.

New tire plants across China, India, and Southeast Asia continue to lock in multi-year carbon black off-take contracts that underpin predictable demand patterns. Yokohama's ongoing Chinese capacity additions exemplify how large tire complexes stimulate parallel investments in nearby carbon black units, lowering logistics costs and encouraging just-in-time delivery models. Regional clustering raises carbon black demand density and supports economies of scale that benefit furnace black producers. Suppliers with ISO 14001-certified operations secure preferred vendor status, consolidating share among environmentally compliant facilities. The structural link between tire output and carbon black consumption therefore provides a demand floor that smooths revenue cycles and aids long-range capital planning.

OEM requirements for lower rolling resistance and higher conductivity push tire makers to adopt engineered grades that command 40-60% premiums over commodity furnace blacks. These specialty formulations enhance fuel economy and extend tread life, thereby generating measurable performance benefits that outweigh incremental cost. Producers investing in proprietary surface modification and ultra-clean furnace configurations gain sustainable advantages in a higher-margin niche. Technical differentiation and customer qualification protocols create switching costs that strengthen supplier lock-in, while the share of specialty shipments in the carbon black market rises steadily each year. Tight integration between research and development teams and tire designers accelerates the pivot toward advanced grades.

Carbon black production relies heavily on carbonaceous feedstocks such as coal tar and residual fuel oil that can represent up to 50% of total operating cost. The Producer Price Index for carbon and graphite products climbed sharply through late 2024, squeezing margins before contractual pass-through clauses could take effect. Import-dependent plants face added freight exposure that widens regional price differentials and influences trade flow arbitrage. Integrated producers with long-term supply agreements partially shield earnings, whereas spot buyers endure profit swings that influence maintenance turnarounds and capacity utilization. Effective hedging and procurement strategies, therefore, remain essential to stabilize cash flows across the carbon black market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Furnace black accounted for 76.30% of 2025 revenue, highlighting its versatility and competitive economics across core tire and rubber goods. Nonetheless, the carbon black market size in furnace applications confronts a gradual share drift as specialty processes gain traction. Lamp black, supported by a 7.35% forecast CAGR through 2031, benefits from an inherent high-surface-area morphology that delivers superior conductivity in electronics and energy storage coatings. Gas black maintains usage in fine-dispersion inks, whereas thermal black serves niche polymer blends requiring low structure. The disruptive entrance of plasma methane technology extends the process palette by offering a low-emission pathway that can align with OEM carbon accounting frameworks.

Competitive responses include modular reactor retrofits that enable production of semi-specialty grades within existing furnace lines. Cabot Corporation and Birla Carbon are piloting advanced feed-injection controls to tighten particle size distribution and boost structure indices without needing new processes. Successful adaptation preserves scale advantages while capturing value migration toward specialty products. As ASTM develops a unified classification for recovered carbon black, furnace producers may incorporate rCB blending strategies to meet circularity targets without jeopardizing compound performance. Overall, the coexistence of commodity and specialty processes drives a dual-track growth model within the carbon black market.

The Carbon Black Market Report is Segmented by Process Type (Furnace Black, Gas Black, Thermal Black, and Lamp Black), Application (Tire and Industrial Rubber Product, Plastic, Toner and Printing Ink, Coating, Textile Fiber, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific held 61.85% of global revenue in 2025, supported by China's tire manufacturing concentration and India's specialty grade expansion, and is forecast to log a 5.85% CAGR to 2031. China integrates large tire plants with adjacent carbon black units, achieving feedstock and logistics efficiencies that bolster regional competitiveness. India's Himadri Speciality Chemical added 70,000 MTPA of premium capacity in 2024, signaling a shift from commodity supply toward higher-margin powders for performance tires and battery components. Japan and South Korea contribute technology leadership, while Southeast Asian economies supply cost-effective labor and growing domestic auto demand.

North America records mature yet stable consumption, driven by replacement tire demand, high-performance coatings, and early adoption of low-emission processes. Monolith Materials' Nebraska plasma facility introduces an alternative supply base aligned with green procurement objectives, while Cabot Corporation leverages its U.S. specialty plants to pass through inflationary costs without significant volume attrition. The Inflation Reduction Act's battery incentives indirectly support conductive grade growth, providing a structural tailwind for the carbon black market in the region.

Europe emphasizes sustainability and specialty applications, with the Carbon Border Adjustment Mechanism encouraging localized production or preferential sourcing from low-carbon suppliers. Caps on PAH and CO2 emissions accelerate modernization or closure of legacy furnaces. Producers with advanced after-treatment systems maintain market access and negotiate price premiums that offset compliance expenditures.

South America, the Middle East, and Africa collectively account for a smaller share but exhibit pockets of high growth linked to expanding automotive assembly and broader industrialization. Brazil's automotive recovery drives localized tire output that stimulates domestic carbon black production investment. Middle Eastern players leverage petrochemical raw material integration to propose new furnace units, though downstream demand still lags Asia-Pacific scale. South Africa's coatings and mining sectors require specialty dispersion blacks, yet currency volatility clouds capital planning. Combined, these regions offer expansion optionality as primary markets mature, allowing diversified producers to balance regional cycles within the global carbon black market.