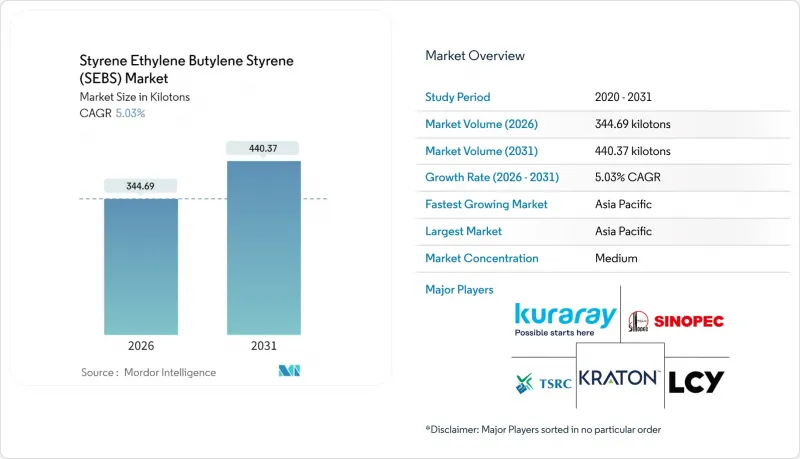

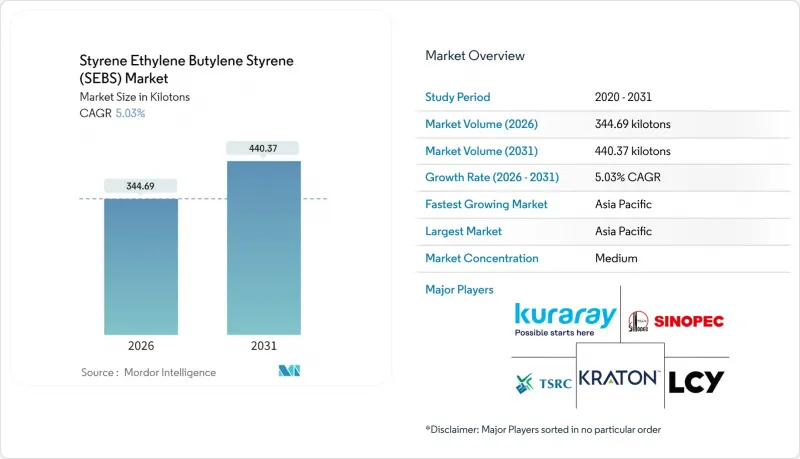

스티렌 에틸렌 부틸렌 스티렌(SEBS) 시장은 2025년에 328.19 킬로톤으로 평가되며, 2026년 344.69 킬로톤에서 2031년까지 440.37 킬로톤에 달할 것으로 예측되고 있으며, 예측 기간(2026-2031년)의 CAGR은 5.03%로 전망되고 있습니다.

핫멜트 접착제, 자동차 실링 시스템, 아스팔트 개질제의 견고한 수요가 단기적인 물량 증가를 견인할 것으로 예측됩니다. 아시아태평양은 중국의 급속한 자동차 생산량 증가와 포장용 접착제 수요 급증에 힘입어 비용 및 수요 측면에서 결정적인 우위를 점하고 있습니다. 분말 형태의 SEBS는 고처리량 믹서에서 깨끗하게 계량할 수 있으므로 아스팔트 및 접착제 컴파운딩 분야에서 주류가 되고 있습니다. 한편, 펠릿 등급은 품질이 중요한 사출성형의 틈새 시장을 지키고 있습니다. 규제 측면의 촉진요인, 특히 의료기기의 프탈레이트 금지와 건축용 접착제의 저VOC 규제는 대체 수요를 더욱 촉진하고 있습니다. 경쟁의 초점은 생산 능력 확대에서 자동차 제조업체의 재활용성 요구 사항과 브랜드 소유자의 Scope 3 배출량 목표를 충족하는 기능성 등급 및 바이오 유래 등급으로 이동하고 있습니다.

캘리포니아주 AB 2300 법안에 따라 2030년부터 대부분의 의료기기에 디(2-에틸헥실) 프탈레이트 사용이 금지됩니다. 이로 인해 튜브 및 가방 제조업체들은 PVC의 유연성을 유지하면서 전환 위험이 없는 가소제가 없는 SEBS로 전환해야 하는 상황에 처해 있습니다. 유럽화학물질청(ECHA)이 단계적 퇴출 시기를 통일함에 따라 전 세계 의료기기 OEM 업체들의 재배합 프로그램이 가속화되고 있습니다. ISO 10993 및 미국 FDA 510(k) 요건에 따른 검증 프로토콜은 다년간의 적격성 확인 주기를 규정하고 있지만, 의료용 제품군을 보유한 공급업체는 이미 초기 단계의 전환을 보장하고 있습니다. 일회용 제품에서는 PVC와의 가격 차이가 여전히 존재하지만, 2028년까지 상업적 규모의 생산량이 확대되면 총 비용의 균형이 맞추어질 것으로 예측됩니다. 따라서 주요 의료 시장에서 규제 기한이 집중되는 가운데, 이러한 촉진요인은 중기 성장에 측정 가능한 성장 촉진 효과를 가져다 줄 것입니다.

중국의 접착제 생산량은 증가할 것으로 예상되며, 카톤 실링, 신발 조립, 조립식 건축에서 SEBS 소비를 견인할 것으로 예측됩니다. 양쯔강 삼각주 및 주강 삼각주의 대기질 규제는 휘발성 유기화합물(VOC) 배출을 제한하고, 무용제 SEBS 블렌드 채택을 촉진하고 있습니다. 브랜드 소유주들이 바이오 유래 성분을 요구함에 따라 접착제 배합 제조업체들은 SEBS 골격과 효율적으로 결합할 수 있는 질량 균형 인증을 받은 액체 폴리부타디엔을 사용하게 되었습니다. 150℃ 이상의 우수한 내열성으로 SEBS 핫멜트는 고속 생산 라인에서 폴리올레핀계 경쟁 제품보다 우수한 성능을 발휘합니다. 이러한 요인들이 단기 수요에 가장 큰 긍정적인 영향을 미칩니다.

원자재 가격 변동에 따른 가격 변동이 생산자의 이익률을 압박하고 있습니다. 2024년 아시아 지역의 크래커 설비 과잉과 지역 수요 둔화가 겹치면서 스티렌 현물 가격은 톤당 800-1,400달러 사이를 오갔습니다. 주요 SEBS 공급업체들은 2022-2025년까지 원자재 가격 상승을 상쇄하기 위해 톤당 총 300달러가 넘는 여러 차례의 가격 인상을 발표했습니다. 장기 단량체 계약이 없는 생산자들은 분기별로 200-300bp의 이익률 하락을 경험하며 단기 매출과 계획 주기에 부담이 되었습니다.

분말 등급은 아스팔트 및 접착제 배합업체들이 정확한 계량 및 혼합 시간 단축을 위해 유동성이 높은 입자를 선호함에 따라 2025년 스티렌-에틸렌-부틸렌-스티렌(SEBS) 시장 수요의 86.62%를 차지하며 CAGR 5.29%로 확대될 것으로 예측됩니다. 펠릿 등급도 분진 없는 취급과 내부 부품에 균일한 용융 유동성을 제공함으로써 사출성형업체의 부가가치를 높이고 있습니다. 공급업체는 분산성을 향상시키기 위해 D50이 200µm 미만인 초미세 분말을 개발하고 있습니다. 한편, 펠릿은 5-8%의 가격 프리미엄이 책정되어 있지만, 엄격한 공차가 요구되는 부품의 경우 구매자도 이를 용인하고 있습니다. 그 결과, 분말은 대량 생산 및 비용 중심의 부문에서 계속 주류를 이루고 있으며, 펠릿은 품질이 중요한 틈새 시장에서 수요가 증가하고 있습니다.

고분자 개질 아스팔트의 분말 수요는 견고합니다. SEBS를 3% 첨가하면 연화점이 65℃에서 85℃로 상승하고, 탄성회복률이 50% 이상 향상되어 고온 기후하에서 포장 수명이 연장되기 때문입니다. 펠릿화 특수 등급은 분진 오염이 허용되지 않는 자동차 실, 스마트폰 오버몰드, 소프트 터치 가전제품을 타겟으로 하고 있습니다. 주요 가공업체들의 설비 투자 동향은 두 가지 형태 모두 전략적 중요성을 유지하고 있지만, 분말 형태가 2030년까지 스티렌-에틸렌-부틸렌-스티렌 시장의 대부분을 차지할 것으로 예측됩니다.

스티렌-에틸렌-부틸렌스티렌(SEBS) 시장 보고서는 형태별(펠릿 및 분말), 최종사용자 산업별(신발, 접착제 및 실란트, 플라스틱, 도로 및 철도, 자동차, 스포츠 및 완구, 전기 및 전자, 기타 최종사용자 산업), 지역별(아시아태평양, 북미, 유럽, 남미, 중동, 아프리카), 지역별로 분류되어 있습니다. 유럽, 남미, 중동 및 아프리카)로 분류됩니다. 시장 예측은 톤 단위로 제공됩니다.

아시아태평양은 2025년 스티렌-에틸렌-부틸렌-스티렌(SEBS) 시장에서 56.61%의 점유율을 차지하며 5.93%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 중국은 2023년 3,016만 대의 자동차를 생산하고 2025년까지 접착제 생산량이 855만 톤에 달할 것으로 예상되며, 이 지역에서 선도적인 위치를 차지하고 있습니다. 발린석유화학의 연간 10만톤 규모의 신규 라인을 포함한 국내 SEBS 생산능력 증설이 공급을 안정화시키는 한편, 인도의 대규모 인프라 계획과 2024년 174만대의 전기자동차 판매는 추가 수요를 촉진할 것으로 보입니다. 동남아시아의 무역 협정은 역내 유통을 더욱 효율화할 것입니다.

북미는 전 세계 생산량의 약 20%를 차지합니다. 성숙한 최종 시장에도 불구하고 리쇼어링 개념과 매스밸런스 인증이 완만한 성장을 지원하고 있습니다. 트린스테오의 스티렌 모노머 통합 사업 철수는 특수 컴파운딩 및 재생 원료로의 산업 전반의 전환을 강조하고 있습니다. 유럽은 수요의 약 17%를 차지하며, REACH 규제 대응과 DEHP 사용기한 연장으로 의료 및 소비재 분야에서의 SEBS 대체가 가속화되고 있습니다. 범용 폴리에틸렌에서 전환을 위한 베르살리스의 대규모 투자 계획은 고부가가치 SEBS 컴파운드 및 순환 경제 솔루션에 대한 새로운 노력을 보여주고 있습니다. 남미와 중동 및 아프리카은 전체 수요의 9%를 차지합니다. 브라질과 사우디아라비아의 인프라 프로젝트에서 아스팔트와 접착제에 SEBS가 사용되고 있지만, 환율 변동과 수입 의존도가 성장을 저해하고 있습니다. 전반적으로 아시아태평양이 여전히 주요 성장 동력이지만, 북미와 유럽의 규제 강화로 인해 지역 간 다양한 발전이 이루어지고 있습니다.

The Styrene Ethylene Butylene Styrene (SEBS) Market was valued at 328.19 kilotons in 2025 and estimated to grow from 344.69 kilotons in 2026 to reach 440.37 kilotons by 2031, at a CAGR of 5.03% during the forecast period (2026-2031).

Robust demand in hot-melt adhesives, automotive sealing systems, and asphalt modification is expected to drive near-term volume gains. The Asia-Pacific region holds a decisive cost and demand advantage, aided by China's rapidly growing vehicle output and surging package-adhesive needs. Powder-form SEBS dominates asphalt and adhesive compounding because it meters cleanly in high-throughput mixers, while pellet grades defend quality-critical injection-molding niches. Regulatory drivers-most notably phthalate bans in medical devices and low-VOC rules in construction adhesives-reinforce substitution tailwinds. Competitive focus has shifted from capacity additions to functionalized and bio-attributed grades that meet automaker recyclability and brand-owner Scope 3 emission targets.

California's AB 2300 prohibits di(2-ethylhexyl) phthalate in most medical devices from 2030, forcing tubing and bag makers toward plasticizer-free SEBS that matches PVC flexibility without migration risk. The European Chemicals Agency has synchronized phase-out dates, intensifying reformulation programs among global device OEMs. Validation protocols under ISO 10993 and U.S. FDA 510(k) requirements outline a multi-year qualification cycle; however, suppliers with medical-grade portfolios have already secured early-stage conversions. Price gaps versus PVC persist in single-use products, but total-cost parity is expected once commercial volumes reach scale by 2028. Accordingly, the driver adds a measurable uplift to mid-term growth as regulatory deadlines converge across major healthcare markets.

China's adhesive output is expected to increase, driving SEBS consumption in carton sealing, footwear assembly, and prefabricated construction. Provincial air-quality mandates in the Yangtze and Pearl River Deltas restrict volatile organic compound emissions, incentivizing solvent-free SEBS blends. Brand owners now request bio-attributed content, prompting adhesive formulators to use mass-balance-certified liquid polybutadienes that pair efficiently with SEBS backbones. Superior heat resistance above 150°C enables SEBS hot melts to outperform polyolefin competitors on fast-moving production lines. These factors generate the largest positive impact on short-term demand.

Feedstock-driven price swings compress producer margins. Spot styrene fluctuated between USD 800 and USD 1,400 per ton in 2024 as surplus Asian cracker capacity met slowing regional demand. Leading SEBS suppliers announced several price hikes totaling more than USD 300 per ton between 2022 and 2025 to offset higher raw-material costs. Producers without long-term monomer contracts experienced a quarter-on-quarter margin erosion of 200-300 basis points, which stressed short-term earnings and planning cycles.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Powder grades captured an 86.62% share of the styrene-ethylene-butylene-styrene market demand in 2025, expanding at a 5.29% CAGR, as asphalt and adhesive formulators favor free-flowing particles that meter accurately and reduce blend times. Pellet grades are also enhancing the value of injection molders, offering dust-free handling and homogeneous melt flow for interior trim parts. Suppliers have developed ultrafine powder variants with a D50 of less than 200 µm to improve dispersion, while pellets command a 5-8% price premium that buyers accept for tight-tolerance components. Consequently, powder continues to dominate high-volume, cost-sensitive segments, whereas pellets thrive in quality-critical niches.

The demand for powder in polymer-modified asphalt remains buoyant because a 3% SEBS dosage raises the softening point from 65°C to 85°C and boosts elastic recovery above 50%, thereby extending pavement life in hot climates. Pelletized specialty grades target automotive seals, smartphone over-molds, and soft-touch appliances, where dust contamination is unacceptable. Equipment investments by leading processors indicate that both forms retain strategic relevance, although powder drives the bulk of the styrene ethylene butylene styrene market volume through 2030.

The Styrene Ethylene Butylene Styrene (SEBS) Market Report is Segmented by Form (Pellets and Powder), End-User Industry (Footwear, Adhesives and Sealants, Plastics, Roads and Railways, Automotive, Sporting and Toys, Electrical and Electronics, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

The Asia-Pacific region held a 56.61% market share in the styrene ethylene butylene styrene (SEBS) market in 2025 and is expected to advance at a 5.93% CAGR. China anchors regional leadership with 30.16 million vehicles produced in 2023, and adhesive output projected to reach 8.55 million tons by 2025. Domestic SEBS capacity additions, including 100 kt/y of new lines at Baling Petrochemical, safeguard supply, while India's large-scale infrastructure program and 1.74 million electric vehicle sales in 2024 catalyze additional demand. Southeast Asian trade pacts further streamline intra-regional flows.

North America accounts for roughly 20% of global volume. Reshoring initiatives and mass-balance certifications support moderate growth despite mature end-markets. Trinseo's exit from styrene monomer integration spotlights a broader industry pivot toward specialty compounding and recycled feedstocks. Europe accounts for approximately 17% of demand; REACH compliance and DEHP sunset extensions are accelerating SEBS substitution in the medical and consumer goods sectors. Large-scale investment plans by Versalis to shift away from commodity polyethylene signal a renewed commitment to higher-value SEBS compounds and circular economy solutions. South America and the Middle East & Africa contribute a combined 9% of demand. Infrastructure projects in Brazil and Saudi Arabia use SEBS in asphalt and adhesives, but currency volatility and import reliance temper growth. Collectively, Asia-Pacific remains the primary engine, while regulatory accelerators in North America and Europe ensure diversified regional progress.