프로필렌옥사이드 시장 : 용도별, 최종 이용 산업별, 제조 공정별, 지역별 - 세계 예측(-2030년)

Propylene Oxide Market by Production Process (Chlorohydrin Process, Styrene Monomer Process), Application (Polyether Polyols, Propylene Glycol), End-use Industry (Automotive, Building & Construction), and Region - Global Forecast to 2030

상품코드:1931749

리서치사:MarketsandMarkets

발행일:2026년 02월

페이지 정보:영문 272 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

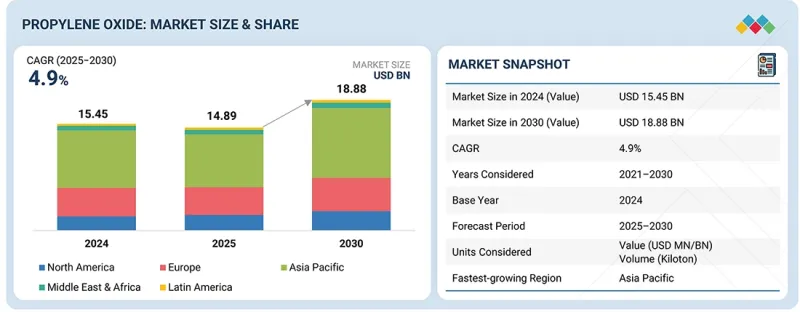

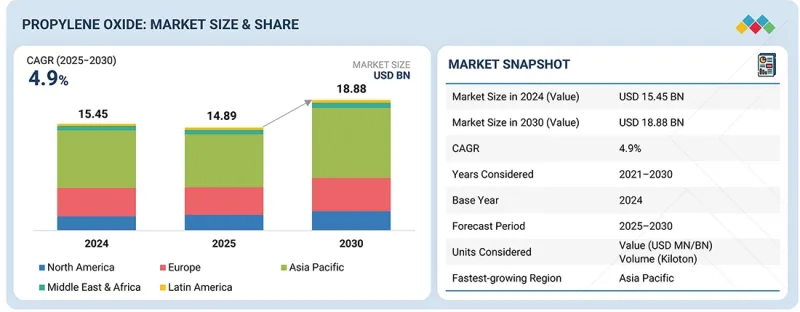

프로필렌옥사이드 시장 규모는 예측 기간 동안 CAGR 4.9%로 성장하여 2025년 148억 9,000만 달러에서 2030년까지 188억 8,000만 달러에 달할 것으로 전망됩니다. 경질 및 연질폼에서 폴리에테르 폴리올 형태의 폴리우레탄 생산에서 폴리우레탄 생산에 이 물질의 중요한 용도를 고려할 때 프로필렌옥사이드 시장의 주요 원동력은 폼 생산에 프로필렌옥사이드를 사용하는 것이며, 이는 프로필렌옥사이드 생산량을 직접 자극합니다.

조사 범위

조사 대상 기간

2022-2030년

기준 연도

2024년

예측 기간

2025-2030년

대상 단위

가치(100만/10억 달러) 량(킬로톤)

부문

용도별, 최종 이용 산업별, 제조 공정별, 지역별

대상 지역

아시아태평양, 유럽, 북미, 중동 및 아프리카, 남미

아시아, 북미, 유럽 시장을 포함한 전 세계 도시화가 진행됨에 따라 효율적인 단열성과 더불어 경량 건축 구조재의 사용이 증가하고 있습니다. 주요 촉진요인으로는 폴리우레탄 유도체가 가져오는 구조적 수요를 들 수 있습니다.

폴리에테르 폴리올 시장은 양 중심의 최종 용도 분야에서 광범위하게 사용되고 프로필렌옥사이드의 소비량이 가장 많기 때문에 예측 기간 동안 가장 큰 수량 점유율을 차지할 것으로 예상됩니다. 건축용 단열재, 자동차 시트 및 내장재, 가구, 침구, 포장재 등에 널리 사용되는 경질 및 연질 폴리우레탄 폼은 주로 폴리에테르 폴리올을 사용하여 제조됩니다. 폴리에테르 폴리올 폼의 수요는 건설 프로젝트 수의 급증, 에너지 절약형 건축물에 대한 수요 확대, 자동차(특히 경량 자동차 및 전기자동차) 생산 증가에 따른 수요 증가에 의해 크게 견인되고 있습니다. 또한, 폴리에테르 폴리올은 유연성, 강도, 가공성 등의 우수한 특성으로 대체재 대비 우위를 점하고 있습니다. 대규모의 지속적인 생산으로 폴리에테르 폴리올은 항상 가장 큰 시장 규모를 유지하고 있으며, 이는 프로필렌옥사이드의 높은 수준의 사용량을 뒷받침합니다.

프로필렌옥사이드 시장의 자동차 응용 분야는 자동차 산업에서 경량 및 고성능 소재의 사용이 확대됨에 따라 예측 기간 동안 가장 빠른 속도로 성장할 것으로 예상됩니다. 프로필렌옥사이드 기반 폴리에테르 폴리올은 주로 폴리우레탄 폼의 제조에 사용되며, 좌석, 머리 받침, 팔걸이, 커튼 라이너, 트렁크 라이너 등의 용도로 설계되었습니다. 이는 탑승자의 편안함, 그리고 전기자동차로의 급속한 전환이 수요를 촉진하고 있으며, 자동차 제조업체들은 전기자동차의 효율성과 주행거리를 향상시키기 위해 경량 소재의 사용을 촉진하고 있습니다. 또한, 개발도상국의 자동차 생산량 증가와 보다 엄격한 공해 방지 및 연비 기준의 도입으로 폴리우레탄 부품의 사용 확대가 가속화되고 있습니다. 프로필렌옥사이드 시장은 승객의 편안함에 대한 관심이 높아지면서 자동차 내장재 분야의 괄목할 만한 성장세를 견인하고 있습니다.

스티렌 모노머 공정은 스티렌 생산과 밀접한 관련이 있고 전 세계 대규모 생산능력으로 인해 예측 기간 동안 프로필렌옥사이드 시장에서 가장 큰 생산량 점유율을 차지할 것으로 추정됩니다. 프로필렌옥사이드와 스티렌 모노머를 동시에 생산할 수 있는 SM 공정을 통해 기업은 규모의 경제, 고효율, 최적의 비용을 실현할 수 있습니다. 주요 기업들은 다양한 소비재, 건설, 포장 분야에서 스티렌에 대한 수요가 확립되어 있는 것에 의존하여 이 공정을 채택하는 경향이 있습니다. 공정 갱신 및 변경에 따른 막대한 설비투자를 고려할 때, 기존 시설의 대부분은 아직 스티렌 모노머 공정에서 전환하지 않은 상태입니다. 이 공정의 장점은 안정성과 용량, 그리고 스티렌 분야의 수요에 대한 적합성으로 인해 전체 프로필렌옥사이드 생산에서 대규모 생산량을 유지하고 있다는 점입니다.

본 보고서의 주요 참여 기업 개요:

프로필렌옥사이드 시장의 주요 참여업체로는 Dow(미국), LyondellBasell Industries Holdings B.V.(네덜란드), Shell(네덜란드), Indorama Ventures Public Company Limited(태국), SABIC(사우디아라비아) 등을 들 수 있습니다. 이들 기업은 시장 점유율과 사업 수익 확대를 위해 계약 체결, 합작 투자, 사업 확장 등 다양한 전략을 채택하고 있습니다.

조사 범위

이 보고서는 제조 공정, 용도, 최종 사용 산업 및 지역을 기반으로 프로필렌옥사이드 시장의 부문을 정의하고 시장 규모를 예측합니다. 주요 진입기업을 전략적으로 프로파일링하고 시장 점유율과 핵심 경쟁력을 종합적으로 분석합니다. 또한, 시장 내 확장, 계약, 인수 등의 경쟁 동향을 추적 및 분석합니다.

본 보고서 구매 이유

이 보고서는 프로필렌옥사이드 시장 및 해당 부문의 수익 수치에 대한 가장 정확한 추정치를 제공함으로써 시장 리더와 신규 진입자에게 도움이 될 것으로 기대됩니다. 또한, 이해관계자들이 시장 경쟁 상황을 깊이 이해하고, 사업적 입지를 강화할 수 있는 귀중한 인사이트를 얻고, 효과적인 시장 진입 전략을 수립하는 데 도움이 될 것으로 기대됩니다. 또한, 시장 동향을 파악하고 주요 시장 촉진요인, 억제요인, 도전과제, 기회요인에 대한 정보를 제공합니다.

이 보고서는 다음 사항에 대한 인사이트를 제공합니다:

주요 촉진요인(폴리우레탄 제조용 폴리에테르폴리올 수요 증가, 기타 최종 사용 산업에서의 수요 증가), 억제요인(프로필렌옥사이드의 건강 위험 분류 및 독성, 산업 안전 및 규제 준수 제약), 기회 요인(청정 생산 기술 개발 및 채택, 개발도상국 시장 확대), 도전 요인(원재료의 변동성, 석유에서 유래한 바이오 기반 폴리우레탄 폼의 채택) 기회, 의료 산업에서의 신흥 용도), 과제(원료 가격의 변동성, 석유 기반이 아닌 바이오 기반 원료를 사용한 폴리우레탄 폼의 채택)가 프로필렌옥사이드 시장 성장에 미치는 영향에 대한 자료입니다.

제품 개발/혁신 : 프로필렌옥사이드 시장의 향후 기술 동향, 연구개발 활동에 대한 상세 분석

시장 개발 : 수익성 높은 시장에 대한 종합적인 정보 : 이 보고서는 다양한 지역의 프로필렌옥사이드 시장을 분석합니다.

시장 다각화 : 프로필렌옥사이드 시장의 신제품, 각종 유형, 미개척 지역, 최근 동향, 투자에 관한 종합적인 정보

경쟁사 평가 : 프로필렌옥사이드 시장의 주요 기업인 Dow(미국), LyondellBasell Industries Holdings B.V.(네덜란드), Shell(네덜란드), Indorama Ventures Public Company Limited(태국), SABIC(사우디아라비아) 등의 시장 점유율, 성장 전략, 제품 제공에 대한 상세 평가

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

시장 역학

성장 촉진요인

성장 억제요인

기회

과제

미충족 수요와 공백

상호 접속된 시장과 분야 횡단적인 기회

새로운 비즈니스 모델과 생태계의 변화

티어1/2/3 진출 기업의 전략적 활동

제5장 업계 동향

Porter's Five Forces 분석

거시경제 전망

밸류체인 분석

생태계 분석

가격 분석

무역 분석

2025-2026년의 주요 회의와 이벤트

고객 비즈니스에 영향을 미치는 동향/혼란

투자와 자금 조달 시나리오

사례 연구 분석

2025년 미국 관세가 프로필렌옥사이드 시장에 미치는 영향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 그리고 향후 응용

주요 신기술

보완적 기술

인접 기술

특허 분석

향후 응용

AI/생성형 AI가 프로필렌옥사이드 시장에 미치는 영향

제7장 지속가능성과 규제 상황

지역 규제와 컴플라이언스

지속가능성에 대한 대처

지속가능성에 대한 영향과 규제 정책의 대처

인증, 라벨, 환경기준

제8장 고객 상황과 구매 행동

의사결정 프로세스

구매자 이해관계자와 구입 평가 기준

채용 장벽과 내부 과제

다양한 최종 이용 산업의 미충족 수요

시장 수익성

제9장 프로필렌옥사이드 시장(용도별)

폴리에테르 폴리올

프로필렌 글리콜

글리콜 에테르

기타

제10장 프로필렌옥사이드 시장(최종 이용 산업별)

자동차

건축·건설

화학·의약품

텍스타일 및 가구

포장

일렉트로닉스

기타

제11장 프로필렌옥사이드 시장(제조 공정별)

클로로히드린 공정

스티렌 모노머 공정

TBA 연산 공정

과산화수소 공정

쿠멘 기반 공정

제12장 프로필렌옥사이드 시장(지역별)

아시아태평양

중국

일본

인도

한국

태국

호주

기타

북미

미국

캐나다

멕시코

유럽

독일

프랑스

영국

이탈리아

스페인

네덜란드

러시아

기타

중동 및 아프리카

사우디아라비아

아랍에미리트

GCC의 나머지 국가

남아프리카공화국

기타

남미

브라질

아르헨티나

칠레

기타

제13장 경쟁 구도

주요 진출 기업의 전략/강점

매출 분석, 2024년

시장 점유율 분석, 2024년

브랜드/제품 비교

기업 평가와 재무 지표

기업 평가 매트릭스 : 주요 진출 기업, 2024년

기업 평가 매트릭스 : 스타트업/중소기업, 2024년

경쟁 시나리오

제14장 기업 개요

주요 진출 기업

DOW

LYONDELLBASELL INDUSTRIES HOLDINGS B.V.

SHELL

BASF

AGC INC.

REPSOL

TOKUYAMA CORPORATION

SUMITOMO CHEMICAL CO., LTD.

SKC

EVONIK

SABIC

BALCHEM CORP.

INDORAMA VENTURES PUBLIC COMPANY LIMITED

TOKYO CHEMICAL INDUSTRY CO., LTD.

기타 기업

PCC SE

WANHUA

OLTCHIM S.A.

WUDI XINYUE CHEMICAL

S-OIL CORPORATION

BEFAR GROUP CO., LTD.

CNOOC SHELL PETROCHEMICALS CO., LTD.

제15장 조사 방법

제16장 부록

KSM

영문 목차

영문목차

The propylene oxide market is projected to grow from USD 14.89 billion in 2025 to USD 18.88 billion by 2030, at a CAGR of 4.9% during the forecast period. The prime driving force in the propylene oxide market, given the substance's vital use in the production of polyurethane in the form of polyether polyols in rigid and flexible foams, is propylene oxide's use in the production of foams, which directly stimulates the volume of propylene oxide production.

Scope of the Report

Years Considered for the Study

2022-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Million/Billion) Volume (Kiloton)

Segments

Production Process, Application, End-use Industry, and Region

Regions covered

Asia Pacific, Europe, North America, the Middle East & Africa, and South America

The increasing rate of urbanization in the world, including the Asian, North American, and European markets, is increasing the use of lightweight building structure material, in addition to efficient thermal insulation. The principal driving force is often regarded as the structural pull provided by derivatives of polyurethane.

"By application, the polyether polyols segment is estimated to account for the largest share, in terms of volume, during the forecast period."

The polyether polyols market is expected to account for the largest volume share during the forecasted period due to its wide usage in volume-driven end-use applications and its highest consumption of propylene oxide. Rigid and flexible polyurethane foams, which are widely used in building insulation, car seats, and interior trims, furniture, bedding, and packaging, respectively, are mainly produced using polyether polyols. The demand for polyether polyol foam is being largely stimulated by the rising demand due to the fast-growing number of construction projects, the increasing demand for energy-efficient buildings, and the rising production levels of automobiles, particularly lightweight and electric cars. Additionally, polyether polyols offer an edge over alternatives because of their superior properties, including flexibility, strength, and ease of processing. The polyether polyols continuously hold the highest volume market due to large and continuous production, which in turn supports high use levels of propylene oxide.

"By end-use industry, the automotive segment is estimated to be the fastest-growing segment of the propylene oxide market during the forecast period."

The automotive application segment of the propylene oxide market is expected to grow at the most prominent pace through the forecast period due to the growing use of lightweight and high-performance materials in the car industry, propylene oxide-based polyether polyols are primarily used to make polyurethane foams intended for applications related to the creation of seating, head rests, arm rests, and curtain and trunk linings with a focus on promoting passenger comfort, safety, and noise reduction capabilities within a vehicle. Further driving the demand is the rampant shift toward the use of electric cars, with car manufacturers exemplifying the use of lightweight materials to boost the efficiency and range of electric cars. The rising use of polyurethane parts is also gaining impetus with the growing production volumes of autos within developing countries and more stringent pollution and fuel economy norms. The propylene oxide market is also being driven by the marked growth trajectory illustrated by the car interior sector, with more focus on passenger comfort.

"By production process, the styrene monomer process segment is estimated to hold the largest share, in terms of volume, during the forecast period."

The styrene monomer process is estimated to account for the largest volume share within the propylene oxide market during the forecast period due to its strong link with styrene manufacture and its large worldwide capacity. By aiding the simultaneous manufacture of propylene oxide and styrene monomer, the SM process allows companies to leverage economies of scale, high efficiency, and optimal costs. Large players often resort to this process, which relies on the well-known demand for styrene from various consumer products, construction, and packaging sectors. Assuming the large capital expenditure requirements involved with upgrading or changing processes, most old facilities have yet to shift from the styrene monomer process. To its credit, the process holds large-scale volumes within collective propylene oxide manufacture due to its well-proven reliability, capabilities, and matching demand within the styrene segment.

Profile break-up of primary participants for the report:

By Company Type: Tier 1 - 30%, Tier 2 - 35%, and Tier 3 - 35%

By Designation: C-level Executives - 30%, Directors - 60%, and Others - 10%

By Region: North America - 30%, Asia Pacific - 15%, Europe - 40%, Middle East & Africa - 10%, and South America - 5%

Dow (US), LyondellBasell Industries Holdings B.V. (Netherlands), Shell (Netherlands), Indorama Ventures Public Company Limited (Thailand), and SABIC (Saudi Arabia) are among the key players in the propylene oxide market. These players have adopted various strategies, including agreements, joint ventures, and expansions, to increase their market share and business revenue.

Research Coverage

The report defines segments and projects the size of the propylene oxide market based on production process, application, end-use industry, and region. It strategically profiles the key players and comprehensively analyzes their market share and core competencies. It also tracks and analyzes competitive developments, such as expansions, agreements, and acquisitions undertaken by them in the market.

Reasons to Buy the Report

The report is expected to help the market leaders/new entrants by providing them with the closest approximations of revenue numbers of the propylene oxide market and its segments. This report is also expected to help stakeholders gain a deeper understanding of the market's competitive landscape, acquire valuable insights to enhance their business positions, and develop effective go-to-market strategies. It also enables stakeholders to understand the market's pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

Analysis of critical drivers (rising demand for polyether polyols for the production of polyurethanes, growing demand from other end use industries), restraints (health hazard classification and toxic nature of propylene oxide, occupational safety and compliance constraints), opportunities (development and adoption of cleaner production technologies, expanding opportunities in developing markets, emerging applications in healthcare industry), and challenges (price volatility of raw materials, use of bio-based feedstock for polyurethane foam instead of petroleum) influencing the growth of the propylene oxide market

Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities in the propylene oxide market

Market Development: Comprehensive information about lucrative markets: the report analyzes the propylene oxide market across varied regions

Market Diversification: Exhaustive information about new products, various types, untapped geographies, recent developments, and investments in the propylene oxide market

Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players such as Dow (US), LyondellBasell Industries Holdings B.V. (Netherlands), Shell (Netherlands), Indorama Ventures Public Company Limited (Thailand), SABIC (Saudi Arabia), and others are the key players in the propylene oxide market

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.4 INCLUSIONS & EXCLUSIONS

1.4.1 YEARS CONSIDERED

1.5 CURRENCY CONSIDERED

1.6 UNIT CONSIDERED

1.7 LIMITATIONS

1.8 STAKEHOLDERS

1.9 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

2.2 KEY MARKET PARTICIPANTS: INSIGHTS AND STRATEGIC DEVELOPMENTS

2.3 DISRUPTIVE TRENDS SHAPING THE MARKET

2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN PROPYLENE OXIDE MARKET

3.2 PROPYLENE OXIDE MARKET, BY TYPE AND REGION

3.3 PROPYLENE OXIDE MARKET, BY PRODUCTION PROCESS

3.4 PROPYLENE OXIDE MARKET, BY END-USE INDUSTRY

3.5 PROPYLENE OXIDE MARKET, BY COUNTRY

4 MARKET OVERVIEW

4.1 INTRODUCTION

4.2 MARKET DYNAMICS

4.2.1 DRIVERS

4.2.1.1 Rising demand for polyether polyols for production of polyurethanes

4.2.1.2 Growing demand from automotive and building & construction industries

4.2.2 RESTRAINTS

4.2.2.1 Health hazard classification and toxic nature of propylene oxide

4.2.2.2 Occupational safety and compliance constraints

4.2.3 OPPORTUNITIES

4.2.3.1 Development and adoption of cleaner production technologies

4.2.3.2 Expanding opportunities in developing markets

4.2.3.3 Emerging applications in healthcare industry

4.2.4 CHALLENGES

4.2.4.1 Price volatility of raw materials

4.2.4.2 Use of bio-based feedstock for polyurethane foam instead of petroleum

4.3 UNMET NEEDS AND WHITE SPACES

4.3.1 UNMET NEEDS IN PROPYLENE OXIDE MARKET

4.3.2 WHITE SPACE OPPORTUNITIES

4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

4.4.1 INTERCONNECTED MARKETS

4.4.2 CROSS SECTOR OPPORTUNITIES

4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

4.5.1 EMERGING BUSINESS MODELS

4.5.2 ECOSYSTEM SHIFTS

4.6 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

4.6.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

5.1 PORTER'S FIVE FORCES ANALYSIS

5.1.1 THREAT OF NEW ENTRANTS

5.1.2 THREAT OF SUBSTITUTES

5.1.3 BARGAINING POWER OF SUPPLIERS

5.1.4 BARGAINING POWER OF BUYERS

5.1.5 INTENSITY OF COMPETITIVE RIVALRY

5.2 MACROECONOMICS OUTLOOK

5.2.1 INTRODUCTION

5.2.2 GDP TRENDS AND FORECAST

5.2.3 OIL & GAS INDUSTRY

5.2.4 TRENDS IN GLOBAL AUTOMOTIVE INDUSTRY

5.2.5 TRENDS IN MANUFACTURING INDUSTRY

5.2.6 TRENDS IN GLOBAL ELECTRONICS INDUSTRY

5.3 VALUE CHAIN ANALYSIS

5.4 ECOSYSTEM ANALYSIS

5.5 PRICING ANALYSIS

5.5.1 AVERAGE SELLING PRICE TREND, BY REGION

5.5.2 AVERAGE SELLING PRICE TREND, BY APPLICATION, 2022-2025 (USD/TON)

5.6 TRADE ANALYSIS

5.6.1 IMPORT SCENARIO (HS CODE 291020)

5.6.2 EXPORT SCENARIO (HS CODE 291020)

5.7 KEY CONFERENCES AND EVENTS, 2025-2026

5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.9 INVESTMENT AND FUNDING SCENARIO

5.10 CASE STUDY ANALYSIS

5.10.1 HEALTH CLASSIFICATION DRIVING RISK MANAGEMENT IN PROPYLENE OXIDE MARKET

5.10.2 LOW TEMPERATURE DIRECT OXIDATION OF PROPANE TO PROPYLENE OXIDE USING SUPPORTED SUBNANOMETER CU CLUSTERS

5.10.3 GREEN SYNTHESIS OF PROPYLENE OXIDE DIRECTLY FROM PROPANE

5.11 IMPACT OF 2025 US TARIFF ON PROPYLENE OXIDE MARKET

5.11.1 INTRODUCTION

5.11.2 KEY TARIFF RATES

5.11.3 PRICE IMPACT ANALYSIS

5.11.4 IMPACT ON COUNTRIES/REGIONS

5.11.4.1 US

5.11.4.2 Europe

5.11.4.3 Asia Pacific

5.11.5 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGICAL ADANCEMENTS, AI-DRIVEN IMPACTS, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

6.1 KEY EMERGING TECHNOLOGIES

6.1.1 CHLOROHYDRIN PROCESS (CHPO)

6.1.2 ETHYLBENZENE HYDROPEROXIDE WITH STYRENE CO-PRODUCT (SMPO/POSM)

6.2 COMPLEMENTARY TECHNOLOGIES

6.2.1 TERT-BUTYL ALCOHOL CO PRODUCT PROCESS (TBA ROUTE)

6.2.2 EPOXIDATION WITH HYDROGEN PEROXIDE (HPPO)

6.2.3 CUMENE HYDROPEROXIDE (CHP) PROCESS

6.3 ADJACENT TECHNOLOGIES

6.3.1 GREEN SYNTHESIS OF PROPYLENE OXIDE DIRECTLY FROM PROPANE

6.4 PATENT ANALYSIS

6.4.1 INTRODUCTION

6.4.2 METHODOLOGY

6.4.3 DOCUMENT TYPE

6.4.4 INSIGHTS

6.4.5 LEGAL STATUS OF PATENTS

6.4.6 JURISDICTION ANALYSIS

6.4.7 TOP APPLICANTS

6.4.8 LIST OF MAJOR PATENTS

6.5 FUTURE APPLICATIONS

6.5.1 POLYURETHANE SYSTEMS: HIGH PERFORMANCE FOAMS AND ELASTOMERS FOR CONSTRUCTION, AUTOMOTIVE, AND INDUSTRIAL APPLICATIONS

6.5.2 ELECTRIC VEHICLE & BATTERY SAFETY MATERIALS: ADVANCED FOAMS AND ELASTOMERS FOR BATTERY THERMAL MANAGEMENT AND FIRE PROTECTION