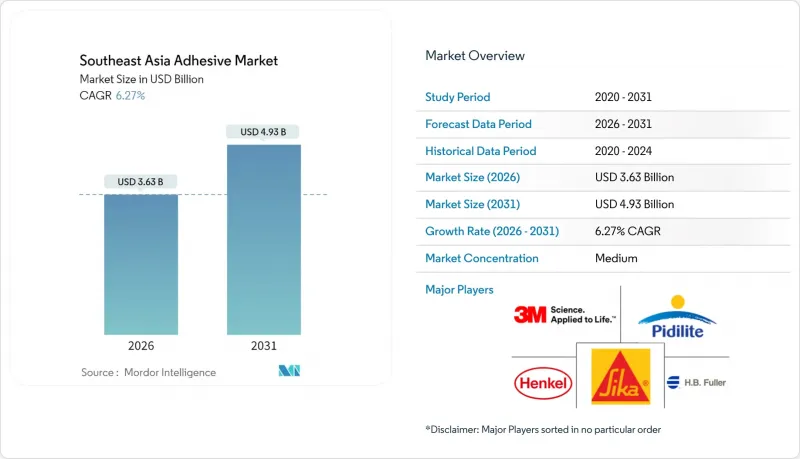

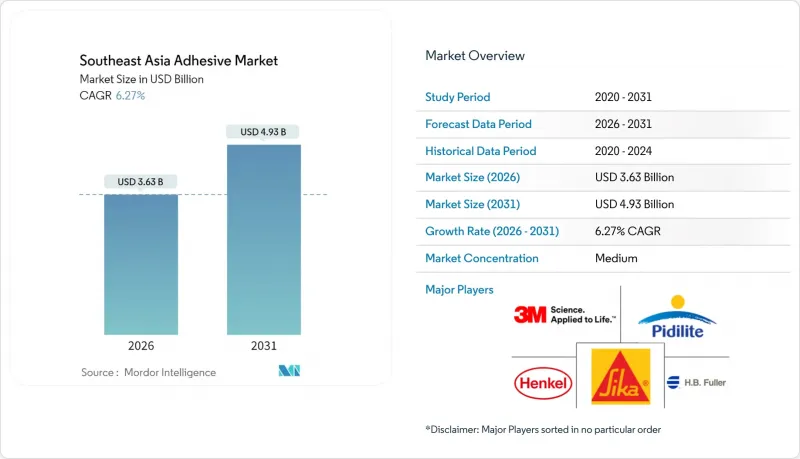

동남아시아의 접착제 시장 규모는 2026년에 36억 3,000만 달러에 달할 것으로 예측되고 있습니다. 이는 2025년 34억 2,000만 달러에서 성장한 수치이며, 2031년에는 49억 3,000만 달러에 달할 것으로 전망되고 있습니다. 2026-2031년의 연평균 성장률(CAGR)은 6.27%로 예측되고 있습니다.

인도네시아와 베트남의 건설 지출 증가, 태국과 인도네시아의 전기자동차 배터리 투자 가속화, 저VOC 수성 화학물질로의 전환이 이러한 성장세를 지원하고 있습니다. 전자제품, 신발, 의료용 일회용 제품 제조 분야에 대한 외국인 직접투자는 지역 고객 기반을 확대하고, 수지 및 배합 자산의 다운스트림에서 현지화를 촉진합니다. 베트남의 화학물질법(65/2025/QH15) 및 싱가포르의 NEA VOC 규제와 같은 규제 프레임워크는 기술 선택을 재정의하고 순환 경제 목표에 따라 수성, 반응성, UV 경화 시스템에 대한 수요를 유도하고 있습니다. 석유화학 원료의 가격 변동은 단기적으로 이익률을 압박하는 요인이지만, 안정적 공급계약과 수직계열화를 실현한 생산자는 매출을 보호하고, 시카사 부카시 공장의 생산라인 증설과 같은 증산투자를 할 수 있습니다. 현지 생산 체제, 규제에 부합하는 화학제품, 응용 기술 교육을 결합한 접착제 공급업체는 인프라, 포장, EV 공급망 프로젝트에서 신규 수주를 확보하는 데 유리한 위치에 있습니다.

인도네시아와 베트남 정부의 막대한 예산으로 호치민시 순환도로 3호선 등 메가 프로젝트에 시멘트, 철강, 엔지니어링 패널이 역대 최대 규모로 투입되고 있습니다. 타일 시공, 단열재, 커튼월, 모듈형 프리캐스트 부재의 경우 접착제가 기계식 체결재를 대체하여 현장 작업 시간을 단축하고 기밀성을 향상시키고 있습니다. 건설업체들은 아세안 그린 빌딩의 VOC 상한선인 50g/L를 준수하는 수성 아크릴계 및 반응성 폴리우레탄계 등급을 선호하고 있습니다. 자카르타 및 호치민시 인근의 조립식 공장에서는 고온 다습한 열대 기후에서 오븐 없이도 경화 가능한 2액형 에폭시 수지를 사용하여 파사드 모듈을 24시간 이내에 납품할 수 있습니다.

동남아시아 전역의 온라인 소매점에서는 핫멜트 접착제 또는 수성 접착제를 사용한 골판지 우편 봉투, 파우치 및 박리가 쉬운 라벨을 요구하고 있습니다. 에이버리데니슨의 CleanFlake와 같은 감압성 접착제 제품은 세척 과정에서 완전히 분리되므로 PET의 재활용률을 향상시켜 브랜드 소유자가 아세안 순환 경제 프레임워크의 재활용 목표를 달성할 수 있도록 돕습니다. 헨켈의 테크노멜트 스프라115를 사용하는 골판지 가공업체는 분당 최대 120개의 골판지 상자를 밀봉할 수 있으며, 솔벤트 유형에 필요한 에너지를 절약할 수 있습니다. 소비자들이 친환경 포장에 대해 프리미엄 가격을 지불할 의향이 있으므로 바이오 또는 솔벤트 프리 라인을 인증하는 가공업체들의 이익률이 향상될 것입니다. 이러한 추세와 함께 동남아시아 접착제 시장에서 지속가능한 등급의 잠재적 수요층이 확대되고 있습니다.

중규모 제조업체들은 현재 제품 라인별로 재배합, 안전성 시험, 재등록에 많은 투자를 요구받고 있으며, 이는 모두 새로운 VOC 기준치 규제에 대한 대응책입니다. 싱가포르의 배출량 보고 의무로 인해 연간 관리비용이 증가하여 일부 중소기업은 생산을 아웃소싱하거나 규제가 심한 부문에서 철수할 수밖에 없는 상황입니다. 수성 시스템은 VOC 문제를 해결하지만, 건조 주기가 길어지기 때문에 제습 설비를 도입하지 않는 한 생산 시간이 증가합니다. 이는 비용을 중시하는 공장에 장벽이 될 수 있습니다. APEC(아시아태평양경제협력체)의 규제 조화는 국경 간 무역을 촉진하지만, 단계적 도입 기간의 차이로 인해 일시적인 차익거래가 발생하여 공급망 계획을 복잡하게 만들고 있습니다.

폴리우레탄은 6.57%의 연평균 복합 성장률(CAGR)을 달성하여 수지 중 가장 빠른 성장세를 보였습니다. 이는 EV 배터리 및 무용제 신발 제조 라인에서 VOC 배출을 배제하는 단면 PU 접착제가 지정되었기 때문입니다. 아크릴 수지는 연포장용 라미네이트와 타일용 모르타르에서 비용과 성능의 균형으로 31.18%의 점유율을 유지하며 여전히 지배적인 위치를 차지하고 있습니다. 에폭시 수지는 배터리 팩 조립과 같은 구조적 틈새 시장에 대응합니다. SikaPower-4720은 실온 경화에서 25MPa의 인장 강도를 달성했습니다. 의료기기용 실리콘 수지는 ISO 10993 규격에 부합하는 Wacker의 새로운 아시아 생산 능력으로 인해 수요가 증가했습니다.

지속가능성에 대한 압박이 커지면서 피마자유를 원료로 한 바이오 폴리우레탄 개발이 추진되고 있는 가운데, BASF의 부틸아크릴레이트 공급 계약은 원료 확보의 중요성을 강조하고 있습니다. 폴리우레탄으로 알루미늄과 탄소섬유를 접합하는 것은 OEM(Original Equipment Manufacturer)의 경량화 목표를 달성하고 차량 중량을 줄일 수 있게 함으로써 동남아시아 접착제 시장에서 그 역할을 더욱 확대하고 있습니다.

The Southeast Asia Adhesive Market size in 2026 is estimated at USD 3.63 billion, growing from 2025 value of USD 3.42 billion with 2031 projections showing USD 4.93 billion, growing at 6.27% CAGR over 2026-2031.

Rising construction outlays in Indonesia and Vietnam, accelerating EV-battery investments in Thailand and Indonesia, and the shift toward low-VOC waterborne chemistries collectively underpin this momentum. Foreign direct investment in electronics, footwear, and medical disposables manufacturing expands the regional customer base and stimulates the downstream localization of resin and formulation assets. Regulatory frameworks, such as Vietnam's Law on Chemicals (65/2025/QH15) and Singapore's NEA VOC limits, are redefining technology choices, steering demand toward water-borne, reactive, and UV-cured systems that align with circular economy goals. Price volatility in petrochemical feedstocks creates short-term margin pressure; however, producers with secured supply contracts or vertical integration can protect their earnings and invest in capacity expansions, such as Sika's Bekasi line doubling. Adhesive suppliers that combine localized production, compliant chemistries, and application training are best placed to capture new orders from infrastructure, packaging, and EV supply-chain projects.

Significant government budgets in Indonesia and Vietnam channel record volumes of cement, steel, and engineered panels into megaprojects such as the Ho Chi Minh City Ring Road 3. Adhesives replace mechanical fasteners in tile setting, insulation, curtain wall, and modular precast elements, shortening on-site labor and improving airtightness. Contractors prefer water-borne acrylic and reactive polyurethane grades that comply with ASEAN Green Building VOC caps of 50 g/L. Prefabrication plants situated near Jakarta and Ho Chi Minh City utilize two-component epoxies that cure in humid tropical climates without the need for ovens, allowing for a 24-hour turnaround of facade modules.

Online retail across Southeast Asia requires corrugate mailers, pouches, and easy-peel labels that rely on hot-melt and water-borne adhesives. Pressure-sensitive products, such as Avery Dennison's CleanFlake, enhance PET recycling rates by detaching cleanly during wash cycles, enabling brand owners to meet recycling targets under the ASEAN Circular Economy framework. Corrugate converters running Henkel Technomelt Supra 115 seal up to 120 cartons per minute, saving energy required by solvent types. Consumer willingness to pay a premium for eco-friendly packaging elevates margins for converters that certify bio-based or solvent-free lines. These trends collectively widen the addressable pool for sustainable grades within the Southeast Asia adhesive market.

Mid-sized producers are now required to invest significantly per product line for reformulation, safety testing, and re-registration, all in response to new VOC threshold compliance mandates. Singapore's mandatory emissions reporting adds annual administrative expenses, prompting some SMEs to outsource production or exit high-compliance segments. Water-borne systems solve VOC challenges but extend drying cycles, increasing production time unless dehumidification is installed, a barrier for cost-sensitive workshops. Harmonization under APEC facilitates cross-border trade, but varying phase-in periods create temporary arbitrage, complicating supply chain planning.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Polyurethane achieved a 6.57% CAGR, the fastest among resins, as EV batteries and solvent-free footwear lines specify single-sided PU adhesives that eliminate VOC emissions. Acrylic stayed dominant with a 31.18% share owing to its balanced cost and performance in flexible packaging laminates and tile-setting mortars. Epoxy addressed structural niches, such as battery-pack assembly. SikaPower-4720 reaches a tensile strength of 25 MPa while curing at room temperature. Silicone volumes in medical devices increased, supported by Wacker's new Asian capacity that meets ISO 10993 standards.

Intensifying sustainability pressure drives the development of bio-based polyurethanes derived from castor oil, while BASF's butyl-acrylate supply agreement highlights feedstock security priorities. Polyurethane's bonding of aluminum-to-carbon-fiber joints satisfies OEM lightweighting goals, enabling reduction in vehicle mass, thereby further expanding its role in the Southeast Asia adhesive market.

The Southeast Asia Adhesive Market Report is Segmented by Resin (Polyurethane, Epoxy, Acrylic, Silicone, Cyanoacrylate, and More), Technology (Water-Borne, Solvent-Borne, Reactive, Hot-Melt, and UV Cured), End-User Industry (Aerospace, Automotive, and More), and Geography (Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, and Rest of South-East Asia). The Market Forecasts are Provided in Terms of Value (USD).