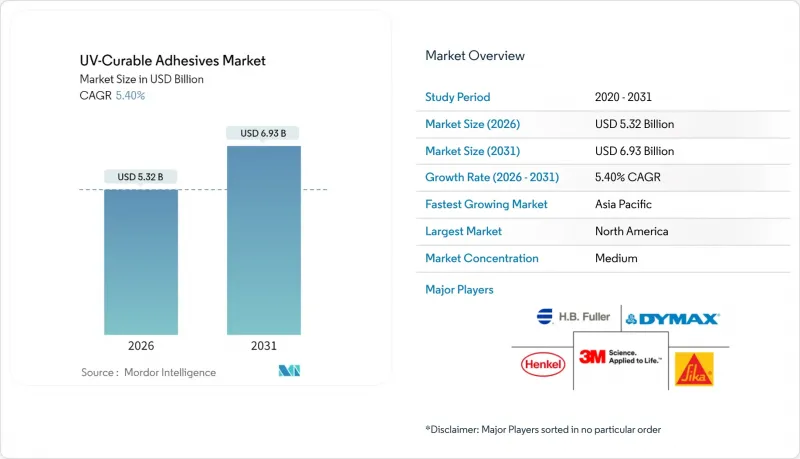

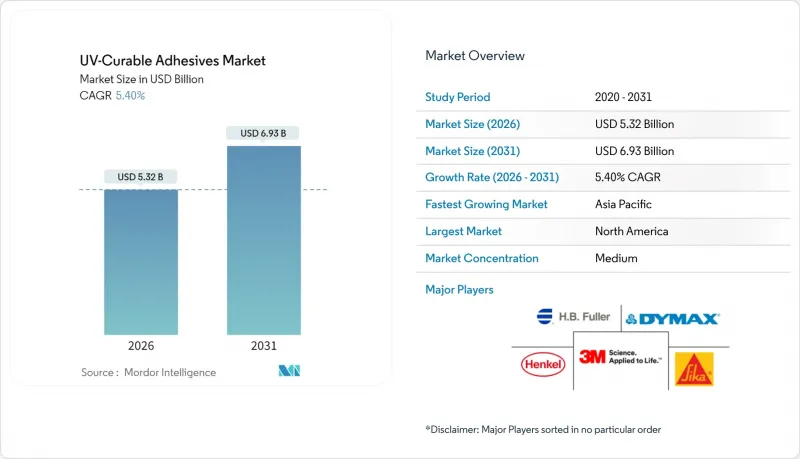

UV 경화 접착제 시장은 2025년 50억 5,000만 달러에서 2026년에는 53억 2,000만 달러로 성장하며, 2026-2031년에 CAGR 5.4%로 추이하며, 2031년까지 69억 3,000만 달러에 달할 것으로 예측되고 있습니다.

의료기기, 가전제품, 자동차 복합재, 포장 등 모든 주요 최종 용도 분야에서 UV 경화 접착제 시장은 틈새 시장에서 필수적인 생산 투입물로 진화하고 있습니다. 이는 주로 주문형 즉시 경화를 통해 오븐 체류 시간을 없애고 휘발성 유기화합물(VOC) 배출을 줄여 경량 복합재 조립을 실현할 수 있기 때문입니다. 성장 모멘텀은 반도체 미세화, 무용매 화학을 촉진하는 유럽과 미국의 엄격한 VOC 규제, 광개시제의 안정적인 공급을 보장하는 수직 통합형 공급망의 덕을 톡톡히 보고 있습니다. 북미는 첨단 의료기기 제조 및 자동차 산업에서 광경화성 구조용 접착제를 조기에 채택하여 기술적 우위를 유지하고 있으며, 아시아태평양은 반도체 패키징 역량 강화에 힘입어 성장을 가속화하고 있습니다. 경쟁 환경에서는 제품 혁신과 규제 대응 전문성, 특히 ISO 10993 및 REACH 가이드라인에 부합하는 배합 기술을 보유한 기업이 우위를 점하고 있습니다.

전기자동차 생산이 증가함에 따라 자동차 제조업체들은 알루미늄과 탄소섬유와 같은 이종 기판을 열 변형 없이 접합할 필요가 있으며, UV 경화 접착제 시장은 몇 초 만에 완전히 경화되면서도 높은 중첩 전단 강도를 유지하는 배합을 제공합니다. Polestar 1과 런던의 TX5 택시 플랫폼은 이 방식을 통한 양산 가능성을 입증하여 경량화와 차량내 소음 관리를 모두 달성했습니다. 항공우주 생산에서도 UV 경화 기술이 오토클레이브 공정의 단축과 복합재 적층판의 에너지 소비 감소를 실현하므로 자동차 산업과 유사한 추세를 볼 수 있습니다. 세계 배터리 팩 생산이 확대됨에 따라 이해관계자들은 2030년까지 고온 내성 UV 경화 에폭시 수지에 대한 수요가 더욱 증가할 것으로 예상하고 있습니다.

2023년 8월 EU의 디이소시아네이트 함량 0.1% 이상 규제는 컨버터가 무공해 솔루션으로 전환하도록 강요하고, UV 경화 접착제 시장에 즉각적인 규제 강화 효과를 가져왔습니다. 2024년 1월 캐나다의 VOC 규제 상한선은 이를 반영하여 북미 연포장 라인의 채택을 더욱 촉진할 것입니다. 수명주기 평가 지표가 조달 기준이 되는 가운데, 무용매 경화 기술은 우수한 환경 라벨을 획득하여 브랜드의 ESG 평가를 높입니다. 헨켈과 같은 주요 공급업체들은 현재 CO2 포집 원료 공정을 상용화하여 완성된 접착제에 포함된 탄소량을 줄이고 있습니다. APAC 지역에서도 유사한 VOC 지침이 검토되고 있으며, 2년 이내에 무용매 기준의 세계 조화가 실현되어 경쟁하는 이액형 에폭시 수지에 앞서 UV 기술의 보급이 가속화될 것으로 예측됩니다.

산업용 LED 어레이의 가격은 5만-50만 달러에 달하며, 전력 비용 절감으로 대량 생산시 투자 회수가 가능하지만, 중소기업은 설비 교체 자금 조달에 어려움을 겪으며 전체 라인 전환이 지연되고 있습니다. 파장 변경에 따른 공정 재검증은 다운타임 리스크를 수반하며, 빠른 기술 혁신 주기로 인해 투자 회수 전 노후화가 우려됩니다. 벤더들은 리스 모델과 모듈형 헤드유닛에 대응하고 있지만, 전 세계에서 금융 환경은 여전히 불균등합니다. EU와 미국의 에너지 절약 보조금 연동형 인센티브가 격차 해소에 기여할 가능성이 있지만, 보급이 확대되기 전까지는 설비비용이 일부 접착제 수요를 억제하는 요인이 될 것입니다.

아크릴계 배합은 성숙한 공급망과 다기판 대응력으로 2025년 UV 경화 접착제 시장 점유율 47.10%를 차지할 것으로 예측됩니다. 아크릴계 제품 시장 규모는 가격 안정화와 세계 조달이 가능한 범용 규모의 원료 공급으로 지원되고 있습니다. 그러나 2031년까지 연평균 복합 성장률(CAGR) 5.55%로 예측되는 에폭시계 제품이 높은 탄성률과 내열 사이클 성능이 필수적인 자동차 구조용 접합부 및 반도체 언더필 분야에서 아크릴계 제품의 우위를 잠식하고 있습니다.

최근 양이온성 광개시제의 혁신으로 유리 전이 온도를 손상시키지 않고 에폭시 경화 시간을 몇 분에서 몇 초로 단축할 수 있으며, 고속 라인 택트를 실현할 수 있습니다. 실리콘과 폴리우레탄은 극한의 온도 변화와 높은 유연성이 인장 강도의 필요성을 능가하는 틈새 시장에서 존재감을 유지하고 있습니다. 예측 기간 중 특정 아크릴레이트 모노머에 대한 REACH 규제에 대한 지속적인 모니터링으로 인해 아크릴 수지의 비용 우위가 축소될 수 있습니다. 이를 통해 특수 에폭시 수지가 UV 경화 접착제 시장의 주류 용도에 더욱 진출할 수 있습니다.

UV 경화 접착제 보고서는 수지 유형(실리콘, 아크릴, 폴리우레탄, 폴리우레탄, 에폭시, 기타 수지 유형), 최종사용자 산업(의료, 전기/전자, 운송, 포장, 가구, 기타 최종사용자 산업), 지역(아시아태평양, 북미, 유럽, 남미, 중동/아프리카) 별로 분류되어 있습니다. 분류되어 있습니다. 시장 예측은 금액(USD)으로 제공됩니다.

북미는 2025년 전 세계 매출의 42.80%를 차지했습니다. 미네소타, 캘리포니아, 온타리오의 OEM(Original Equipment Manufacturer)들이 카테터와 진단용 센서에 FDA 승인 등급을 채택한 반면, 디트로이트의 전기자동차 공장에서는 배터리 팩에 UV 구조용 접착제를 도입했기 때문입니다. 또한 이 지역은 투명성이 높은 규제 경로를 통해 신규 화학물질 시장 출시 기간을 단축하여 공급업체의 R&D 투자를 촉진하고 있습니다.

아시아태평양은 중국, 대만, 한국의 반도체 패키징 능력의 급격한 증가를 배경으로 5.65%의 가장 빠른 CAGR을 달성했습니다. 장홍폴리머의 16억 달러 규모의 아크릴산 단지와 니가타에 위치한 듀폰의 포토레지스트 증설은 이 지역의 원자재 및 첨단 소재 생태계를 지원하고 있습니다. 자동차 수요는 일본과 중국의 자동차 제조업체들이 복합재 섀시 채택을 확대함에 따라 증가하여 고탄성률 UV 에폭시 수지에 대한 새로운 수요를 창출하고 있습니다.

유럽에서는 솔벤트 계열의 경쟁 제품을 배제하고 규제 준수 비용을 증가시키는 엄격한 REACH 규제의 영향으로 균형이 확대되고 있습니다. 지속가능성에 대한 요구는 헨켈 세라네스의 CO2 유래 원료와 사페라테크의 기술을 활용한 접착제 재활용과 같은 순환형 설계의 채택을 촉진하고 있습니다. 중동, 아프리카 및 남미는 신흥 시장이지만, 식품 수출용 연포장 설비 도입이 활발해지면서 UV 경화 접착제 시장에 추가 수요를 창출하고 있습니다.

The UV-Curable Adhesives Market is expected to grow from USD 5.05 billion in 2025 to USD 5.32 billion in 2026 and is forecast to reach USD 6.93 billion by 2031 at 5.4% CAGR over 2026-2031.

Across every major end-use domain, such as medical devices, consumer electronics, automotive composites, and packaging, the UV-curable adhesives market is evolving from niche usage to an essential production input, primarily because instant on-demand curing eliminates oven dwell time, removes volatile organic compound emissions, and supports lightweight mixed-material assemblies. Growth momentum also benefits from semiconductor miniaturization, stricter VOC caps in Europe and North America that favor solvent-free chemistries, and vertically integrated supply chains that secure photoinitiator availability. North America keeps its technological edge through advanced medical manufacturing and early automotive adoption of light-curing structural bonds, while Asia-Pacific accelerates on the back of semiconductor packaging capacity additions. Competitive dynamics reward firms that pair product innovation with regulatory expertise, especially in formulations meeting ISO 10993 and REACH guidelines.

Rising electric-vehicle production pushes automakers to bond dissimilar substrates such as aluminum and carbon fiber without inducing thermal distortion, and the UV-curable adhesives market supplies formulations that fully cure in seconds while retaining high lap-shear strength. Polestar 1 and London's TX5 taxi platforms demonstrate the mass-manufacturing viability of this approach, achieving both weight reduction and cabin noise management. Aerospace production mirrors automotive trends as UV-curing shortens autoclave schedules and lowers energy consumption for composite laminates. With global battery-pack production ramping, stakeholders expect demand for high-temperature-tolerant UV-curable epoxies to intensify through 2030.

The August 2023 EU restriction on diisocyanates above 0.1% content forces converters to shift toward zero-emission solutions, giving the UV-curable adhesives market an immediate regulatory tailwind. Canada's January 2024 VOC limits mirror these caps and further raise adoption in North American flexible-packaging lines. As life-cycle-assessment metrics become procurement criteria, zero-solvent curing scores superior eco-labels, and enhance brand ESG credentials. Leading suppliers like Henkel now commercialize CO2-captured raw-material routes, lowering the embedded carbon of finished adhesives. Because similar VOC directives are under review in APAC, global alignment on solvent-free standards is likely within two years, accelerating UV penetration ahead of competing two-part epoxies.

Industrial LED arrays cost USD 50,000-500,000, and although electricity savings recover cash over high-volume runs, small firms struggle to finance upgrades, slowing full-line conversions. Process re-validation for wavelength changes adds downtime risk, and fast innovation cycles create perceived obsolescence before payback concludes. Vendors respond with leasing models and modular head units, yet credit access remains uneven worldwide. Incentives linked to energy-efficiency grants in the EU and U.S. can close gaps, but until uptake broadens, equipment expense will restrain some adhesives volumes.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Acrylic formulations captured 47.10% of the UV-curable adhesives market share in 2025, owing to mature supply chains and multi-substrate compatibility. The UV-curable adhesives market size for acrylic grades benefits from commodity-scale raw materials that steady pricing and facilitate global sourcing. Yet epoxies, forecast to compound at 5.55% through 2031, are eroding acrylic headroom in automotive structural joints and semiconductor under-fills where high modulus and thermal cycling endurance are non-negotiable.

Recent innovations in cationic photoinitiators shorten epoxy cure from minutes to seconds without compromising glass-transition temperature, enabling high-speed line takt. Silicone and polyurethane niches persist where extreme temperature swing or high flexibility outweigh tensile strength needs. Over the forecast horizon, ongoing REACH scrutiny of certain acrylate monomers may narrow the acrylic cost advantage, potentially pushing specialty epoxies further into mainstream applications of the UV-curable adhesives market.

The UV-Curable Adhesives Report is Segmented by Resin Type (Silicon, Acrylic, Polyurethane, Epoxy, and Other Resin Types), End-User Industry (Medical, Electrical and Electronics, Transportation, Packaging, Furniture, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

North America retained 42.80% of global revenue in 2025 as OEMs in Minnesota, California, and Ontario relied on FDA-cleared grades for catheters and diagnostic sensors, while Detroit electric-vehicle plants adopted UV structural bonds for battery packs. The region also benefits from transparent regulatory pathways that shorten time-to-market for new chemistries, reinforcing supplier research and development investment.

Asia-Pacific delivers the fastest 5.65% CAGR on the back of surging semiconductor packaging capacity in China, Taiwan, and South Korea. Changhong Polymer's USD 1.6 billion acrylic-acid complex and DuPont's photoresist expansion in Niigata shore up regional raw-material and advanced-material ecosystems. Automotive demand rises as Japanese and Chinese OEMs scale mixed-material chassis, creating fresh pull for high-modulus UV epoxies.

Europe's balance grows under the weight of stringent REACH rules that both eliminate solvent competitors and add compliance costs. Sustainability mandates drive the adoption of Henkel-Celanese CO2-derived feedstocks and circular designs like Saperatec-enabled adhesive recycling. Middle East and Africa and South America remain emerging but show momentum in flexible-packaging installations targeting food exports, adding incremental volume to the UV-curable adhesives market