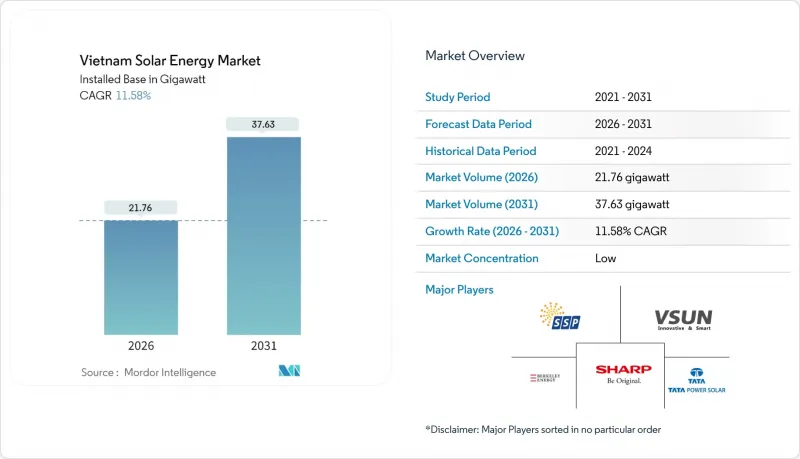

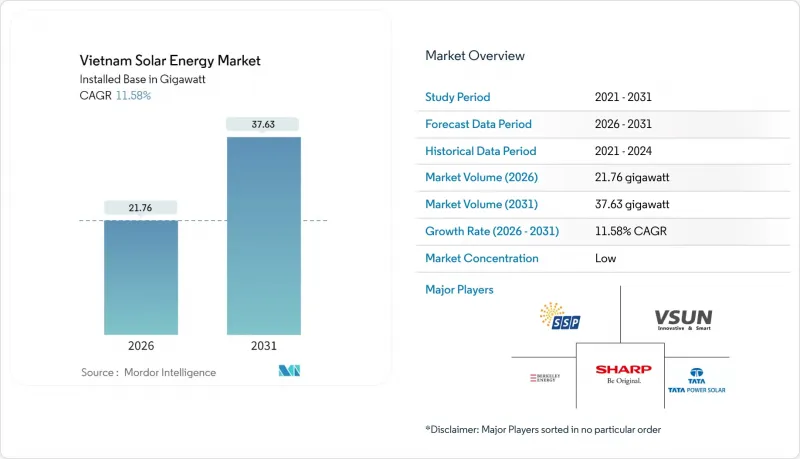

베트남의 태양에너지 시장은 2025년에 19.5 기가와트로 평가되었으며, 2026년 21.76 기가와트에서 2031년까지 37.63 기가와트에 달할 것으로 예측됩니다.

예측 기간(2026-2031년) 동안 CAGR은 11.58%로 예상됩니다.

이러한 상승세는 2020년 고정가격매입제도(FIT) 종료에 따른 정책 재검토, 제8차 전력개발계획(PDP8)의 확대, 지속적인 모듈 비용 하락을 반영하고 있습니다. 수상태양광 경쟁입찰, 직접 전력구매계약(DPPAs) 도입, 24시간 365일 청정 전력을 원하는 데이터센터의 조달 수요가 성장의 원동력이 되는 반면, 송전망 정비와 FIT 제도의 불확실성이 단기적인 운영 리스크를 억제하고 있습니다. 2020년부터 2024년까지 모듈 설비투자는 36% 감소했고, 일조량이 많은 지역의 대규모 발전소 균등화발전원가(LCOE)는 1kWh당 0.04달러 이하로 떨어졌습니다. 또한, 특혜성 기후금융 파이프라인은 민간부문의 투자 의욕을 더욱 높이고 있습니다. 남부 지역의 전력망 혼잡과 대규모 프로젝트 실행에 병목현상, 태양광과 축전 하이브리드화 의무화 및 기업의 전력구매계약(PPA) 약속으로 인해 베트남 태양광 시장은 2030년까지 두 자릿수 성장을 유지할 것으로 예상됩니다.

2025년 4월에 발표된 결정 768호에 따라 PDP8이 개정되어 2030년 태양광 에너지 상한이 46.5-73.4GW로 상향 조정되었습니다. 이에 따라 정격 출력의 10% 이상, 2시간 이상 지속가능한 축전지 에너지 저장설비 설치가 의무화되었습니다. 개발업체는 현재 kWh당 200-250달러의 리튬이온 축전지 시스템을 도입하고 있으며, 100MW 플랜트에 4천만-5천만 달러를 추가 투자하여 낮 시간대보다 30-40% 높은 저녁 피크 요금을 활용할 수 있게 됩니다. 닌투언성과 빈투언성에서는 전력 저장 용량 기준을 초과하는 프로젝트의 허가 절차를 간소화했지만, 북부 지역에서는 송전망 인프라가 취약하여 지연이 발생하고 있습니다. Electricity Vietnam은 PDP8 계획의 전력량을 흡수하기 위해 150억 달러의 신규 송전망 투자가 필요하다고 추정하고 있지만, 연간 평균 투자액은 12억 달러에 불과해 계획의 하한선에 맞춰 전개될 가능성이 높다고 지적하고 있습니다. 그러나 이 정책은 베트남 태양광 시장의 장기적인 전망을 확고히 하고, 각 성의 토지 입찰과 민간 부문의 자금 조달 구조를 안내하는 지침이 되고 있습니다.

법령 80/2024에 따라월 20만kWh 이상의 소비자는 DPPA(전력구매계약)를 체결할 수 있게 되었으며, 6개월 이내에 총 1.77GW 규모의 24개 프로젝트가 승인 대기자 명단에 추가되었습니다. 섬유, 전자제품, 식품 가공업체들은 요금 헤지 및 ESG 인증을 추구하고 있으며, 1km당 50만-200만 달러의 전용선 건설 비용을 피할 수 있는 가상 PPA를 선호하고 있습니다. 세계은행은 2024년 재생에너지 통합을 위해 5억 달러의 자금을 지원하기로 약속했고, 아시아개발은행은 2023년부터 2024년까지 지붕 설치형 태양광 에너지와 마이크로그리드에 17억 달러를 지출했습니다. 구글, 마이크로소프트 등 하이퍼스케일러 기업들은 24시간 365일 카본프리 목표를 달성하기 위해 2027년까지 약 300MW의 전용 태양광 에너지 계약을 체결할 것으로 예상됩니다. 20만kWh 기준은 중소기업의 진입을 제한하지만, 이 법령은 베트남 태양광 시장의 상업적 전환을 가속화할 것입니다.

닌투언성 및 빈투언성의 태양광 에너지량은 이미 지역 수요를 초과하고 있으며, 500kV 간선은 열적 한계에 가깝게 운영되고 있기 때문에 2020년 베트남전력공사(EVN)는 잉여 발전량의 최대 60%를 억제해야 했습니다. 건기 성수기에는 평균 15-25%의 억제율이 발생하여 프로젝트 수익성을 저해하는 상황이 발생합니다. 계획된 150억 달러 규모의 HVDC(고압직류송전) 증설은 2027년까지 완전히 가동되지 않을 것이며, 신규 설비는 송전 조정 위험에 노출된 채로 남아있을 것입니다. 현재 금융기관들은 출력 억제 보험 가입을 요구하고 있으며, 이로 인해 부채 스프레드가 50-75bp 확대되고 있습니다. 의무화된 10%의 축전지 도입은 에너지의 시간적 조정에 기여하지만, 며칠 동안 지속되는 공급과잉을 상쇄할 수 없으며, 이 제약은 베트남 태양광 시장에서 눈에 띄는 걸림돌로 작용하고 있습니다.

태양광 에너지 시스템은 2025년 19.5GW의 전체 기반을 지배할 것이며, 설비투자의 지속적인 감소로 2031년까지 CAGR 11.58%를 유지할 것입니다. 베트남에서는 열역학적 효율에 필요한 직달 일사량이 부족하기 때문에 집광형 태양열 발전은 상업적으로 실현 불가능한 상태입니다. 닌투언성의 유틸리티 규모 지상 설치형은 단축 추적기를 채택하여 12-18%의 발전량 향상을 실현하고 있으며, 도심지 옥상 설치는 모듈 수준의 전력 전자장치를 활용하여 음영 손실을 최소화하고 있습니다. 수력발전댐의 부유식 태양에너지는 설치 장소의 선택권을 넓히고, 기존 송전망을 활용합니다. TOPCon 및 이종접합 모듈의 급속한 보급(2024년 출하량의 35%를 차지)은 전체 시스템 비용 절감에 기여할 것입니다. 반면 CSP(집광형 태양에너지)는 태양광 에너지의 550-650달러/kW에 비해 3,000-4,000달러/kW의 높은 자본집약도와 습도에 의한 광학적 손실의 영향으로 2031년까지 전망이 어려운 상황입니다. 이를 통해 베트남 태양에너지 시장에서 태양광 에너지의 우위를 확고히 하고 있습니다.

개발업체들이 하이브리드 인버터를 통해 양면 모듈과 직류 결합형 배터리를 도입하면서 92-94%의 왕복 효율을 달성하는 기술 혁신이 가속화되고 있습니다. 50MW 이상의 발전소에서는 스트링 인버터 방식이 중앙집중형 유닛을 대체하고 있으며, 내결함성 향상과 단계적 용량 증설을 가능하게 하고 있습니다. 저장설비 의무화로 조달 형태 변화: 45MW/90MWh의 저장시스템과 450MW의 태양광발전소를 결합한 프로젝트는 피크시간대 요금 차익으로 투자 장벽을 해소하여 베트남 태양광 시장의 하이브리드화를 위한 길을 보여주고 있습니다.

베트남 태양에너지 시장 보고서는 기술별(태양에너지 및 집광형 태양열 발전), 계통연계 유형별(계통연계형 및 독립형), 최종사용자별(대규모 사업용, 상업용 및 산업용, 주거용)로 분류되어 있습니다. 시장 규모와 예측은 설치 용량(GW) 단위로 제공됩니다.

The Vietnam Solar Energy Market was valued at 19.5 gigawatt in 2025 and estimated to grow from 21.76 gigawatt in 2026 to reach 37.63 gigawatt by 2031, at a CAGR of 11.58% during the forecast period (2026-2031).

The upward curve reflects policy recalibration following the 2020 feed-in tariff (FIT) sunset, the expansion of Power Development Plan VIII (PDP8), and ongoing module-cost deflation. Competitive land auctions for floating arrays, the rollout of direct power-purchase agreements (DPPAs), and data-center procurement for 24X7 clean power underpin demand momentum, while transmission build-outs and FIT uncertainty temper near-term commissioning risk. Module capex fell 36% between 2020 and 2024, compressing utility-scale levelized costs below USD 0.04 per kWh in high-insolation provinces, and concessional climate-finance pipelines are amplifying the private sector's appetite. Despite grid congestion in the south and execution bottlenecks for large projects, hybrid solar-plus-storage mandates and corporate offtake commitments position the Vietnam solar energy market for double-digit growth through 2030.

Decision 768, issued in April 2025, reset the PDP8, raising the 2030 solar ceiling to 46.5-73.4 GW and mandating battery energy storage equal to at least 10% of the nameplate capacity with a 2-hour duration. Developers now finance lithium-ion arrays costing USD 200-250 per kWh, adding USD 40-50 million to a 100 MW plant, yet unlocking evening-peak tariffs 30-40% above midday rates. Ninh Thuan and Binh Thuan have streamlined permits for projects exceeding the storage threshold, whereas northern provinces lag due to weaker grid infrastructure. Electricity Vietnam estimates that USD 15 billion in new transmission is required to absorb PDP8 volumes, but the annual spend averages only USD 1.2 billion, implying that deployment will likely track the plan's lower bound. The policy nonetheless anchors long-term visibility for the Vietnam solar energy market, guiding provincial land auctions and private-sector financing structures.

Decree 80/2024 unlocked DPPAs for consumers topping 200,000 kWh per month, and within six months, 24 projects totaling 1.77 GW entered the approval queue. Textile, electronics, and food processors are chasing tariff hedges and ESG credentials, favoring virtual PPAs that avoid private-line build costs of USD 0.5-2 million per kilometer. The World Bank committed USD 500 million in 2024 for renewable integration, while the Asian Development Bank disbursed USD 1.7 billion during 2023-24 for rooftop solar and microgrids. Hyperscalers such as Google and Microsoft expect to contract close to 300 MW of dedicated solar by 2027 to meet 24X7 carbon-free goals. Although the 200,000 kWh threshold limits SME participation, the decree accelerates the commercial pivot within the Vietnam solar energy market.

Solar output in Ninh Thuan and Binh Thuan already exceeds local demand, and the 500 kV backbone operates near thermal limits, forcing Electricity Vietnam to curtail up to 60% of excess generation in 2020. Curtailment averages 15-25% during dry-season peaks, undermining project returns. The planned HVDC reinforcement, worth USD 15 billion, will not be fully online until 2027, leaving new capacity exposed to dispatch risk. Lenders now insist on curtailment insurance, adding 50-75 basis-point spreads to debt. Mandatory 10% battery storage helps time-shift energy but cannot offset multi-day oversupply events, keeping this restraint a prominent drag on the Vietnam solar energy market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Solar photovoltaic systems controlled the entire 19.5 GW base in 2025, and continued capex declines support an 11.58% CAGR to 2031. Concentrated solar power remains commercially unviable in Vietnam because the country lacks the direct-normal irradiance required for thermodynamic efficiency. Utility-scale ground mounts in Ninh Thuan utilize single-axis trackers to achieve 12-18% yield gains, whereas urban rooftops rely on module-level power electronics to minimize shading losses. Floating PV on hydropower reservoirs broadens the siting palette and leverages existing transmission. The rapid uptake of TOPCon and heterojunction modules, already accounting for 35% of 2024 shipments, reduces balance-of-system costs. CSP's higher capital intensity of USD 3,000-4,000 per kW, compared to USD 550-650 for PV, together with humidity-driven optical losses, negates its prospects through 2031, cementing photovoltaic primacy in the Vietnam solar energy market.

Innovation accelerates as developers deploy bifacial modules and DC-coupled batteries via hybrid inverters that yield round-trip efficiencies of 92-94%. String-inverter architectures are replacing central units in plants exceeding 50 MW, enhancing fault tolerance and facilitating incremental capacity additions. Battery mandates reshape procurement: 45 MW/90 MWh stacks paired with 450 MW solar farms now clear investment hurdles under peak-tariff spreads, signaling a hybridized roadmap for Vietnam's solar energy market.

The Vietnam Solar Energy Market Report is Segmented by Technology (Solar Photovoltaic and Concentrated Solar Power), Grid Type (On-Grid and Off-Grid), and End-User (Utility-Scale, Commercial and Industrial, and Residential). The Market Sizes and Forecasts are Provided in Terms of Installed Capacity (GW).