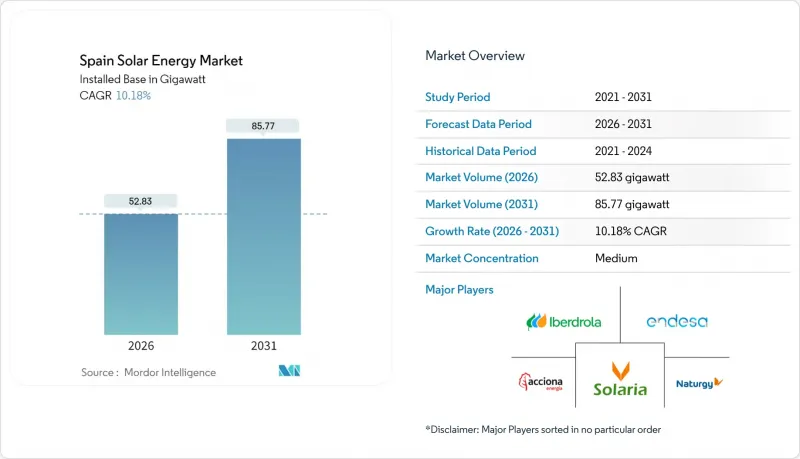

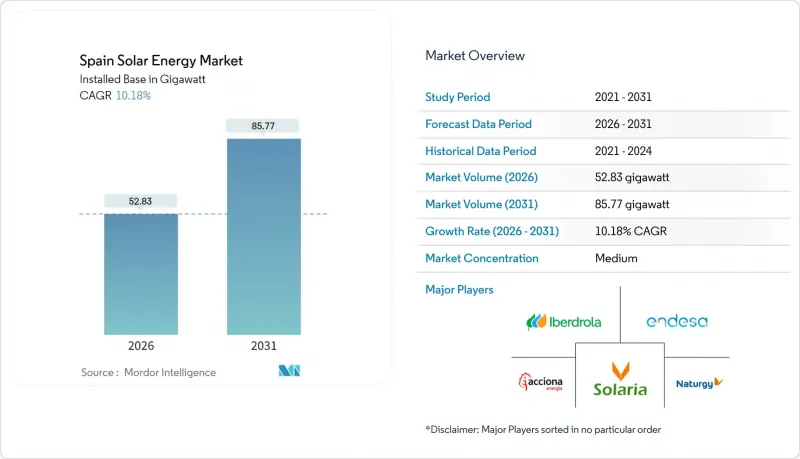

스페인의 태양에너지 시장은 2025년에 47.95 기가와트로 평가되었으며, 2026년 52.83 기가와트에서 2031년까지 85.77 기가와트에 달할 것으로 예측됩니다.

예측 기간(2026-2031년) 동안 CAGR은 10.18%로 예상됩니다.

급속한 용량 확장으로 태양광 에너지는 이미 국내 발전량의 21%를 차지하여 유럽연합(EU) 평균을 크게 상회하고 있습니다. 이로써 국가 에너지 및 기후 계획 개정에 따른 76기가와트 태양광 에너지 목표 달성을 위한 뚜렷한 궤도에 올라섰습니다. 모듈 가격 하락, EU의 'Fit for 55' 지침에 따른 신속한 허가 절차, 기업의 전력 구매 계약(PPA)에 대한 강력한 수요는 스페인의 전체 태양에너지 시장의 성장을 촉진하고 있습니다. 특히 일사량이 많은 지역에서는 출력 억제와 가격 경쟁으로 인한 수익 감소에 대한 대책으로 태양광 에너지와 축전을 결합한 하이브리드 구성이 부상하고 있습니다. 토탈에너지의 세비야 클러스터(263MW)와 프레니튜드의 레노풀 프로젝트(330MW)에서 알 수 있듯이, 국제적인 개발업체들의 진출이 가속화되고 있는 반면, 송전망 혼잡과 나투라 2000에 의한 토지이용 제한이 단기적인 도입 규모를 억제하고 있습니다.

세계 공급과잉으로 인해 모듈 가격은 지속적으로 하락하고 있으며, 카스티야 라 만차 및 에스트레마두라 주에서는 낮은 품질의 토지에서도 경쟁력 있는 균등화발전원가(LCOE)를 달성할 수 있게 되었습니다. 양면 수광 패널과 단축 트래커의 조합으로 현재 25% 이상의 설비 이용률을 달성할 수 있어 대규모 지상 설치형 발전소의 경제적 여지가 확대되고 있습니다. 토탈에너지와 같은 국제적인 전력회사들은 2023년 대비 최대 15%의 설비투자(Capex) 절감 효과를 언급하고 있습니다. 비용 패리티를 달성함으로써 확보된 자본을 시스템 주변기기 업그레이드 및 에너지 관리 소프트웨어에 재분배할 수 있어 축전지와의 하이브리드화를 촉진하고 있습니다. 현지 엔지니어링 회사들은 케이블 손실과 노동력 투입을 줄이는 1,500VDC 시스템 설계로 눈에 띄게 전환하고 있다고 보고하고 있습니다. 그 결과, 스페인의 태양에너지 시장 파이프라인은 경제적으로 불리한 지역에서도 확대되고 있습니다.

2030년 탈탄소화의 법적 구속력 있는 목표는 개발자들에게 규제적 확실성을 제공하고, 입찰 참여와 자금 조달 가능성을 가속화할 수 있습니다. 스페인은 2024년에 22,326MW의 태양광 에너지 건설을 승인했고, 2025년 1분기에 3,019MW를 추가로 승인했습니다. 규제 정합성은 축전 분야에도 적용되어 가정용 축전지 역시 용량 수익의 대상이 되어 분산형 자산의 현금흐름이 개선되었습니다. 지방정부도 국가 정책에 호응하여 안달루시아 주정부는 2025년까지 1.4GW 규모의 프로젝트에 대한 송전망 연결을 가속화했습니다. 명확한 정책 일정은 시장 가격 리스크를 최소화하고 스페인 태양광 시장에 대한 외국인 직접투자를 촉진하고 있습니다.

보호구역은 스페인 국토의 약 30%를 차지하며, 5헥타르 이상의 프로젝트에는 완전한 환경영향조사가 의무화되어 있습니다. 무르시아 주에서만 2030년까지 3만 헥타르의 태양에너지를 계획하고 있으며, 그 중 60%가 농업 협동조합 조직의 조직적인 반대에 직면한 구 경작지에 위치하고 있습니다. 개발업체들은 폐광 등 브라운필드 부지를 점점 더 많이 선택하고 있으며, 1MW당 5만-10만 유로의 복구비용이 추가됩니다. 분쟁이 적은 지역으로의 집중은 송전망의 취약성으로 인해 이미 제약이 있는 지역에 용량을 집중시키고, 그 결과 출력 억제 리스크를 증폭시키고 있습니다.

2025년 기준 태양에너지는 스페인 태양에너지 시장의 94.45%를 차지하며 2031년까지 CAGR 10.45%로 확대될 것으로 예상됩니다. 한편, CSP(집광형 태양열 발전)의 PNIEC 목표는 4.8GW로 하향 조정되었습니다. 리튬이온 배터리는 2024년 140달러/kWh 이하로 가격이 하락하고, 용융염 시스템 대비 절반의 비용으로 2-4시간 동안 전기를 저장할 수 있기 때문에 개발업체들은 태양광+축전지 하이브리드를 우선시합니다. 이에 따라 스페인의 태양에너지 시장 규모는 2025년부터 2030년까지 31GW 이상 증가할 것으로 예상됩니다.

CSP(집광형 태양열 발전)는 여전히 20-50유로/MWh로 산업용 공정열을 공급할 수 있으며, 변동이 심한 천연가스 가격보다 저렴합니다. 스페인에는 2.3GW의 가동중인 발전소가 있습니다. 그러나 2024년 신규 유틸리티 규모의 CSP 프로젝트가 파이낸싱 클로징에 성공한 사례는 없었습니다. 전력회사가 n형 셀을 이용한 양면수광형 태양에너지(발전량 10-15% 향상)에 자본을 재분배하면서 CSP의 점유율은 더욱 축소될 것으로 예상됩니다.

태양에너지 시장 보고서는 기술별(태양에너지 및 집광형 태양열 발전), 계통연계 유형별(계통연계형 및 독립형), 최종사용자별(대규모, 상업용 및 산업용, 주거용)로 분류되어 있습니다. 시장 규모와 예측은 설치 용량(GW) 단위로 제공됩니다.

The Spain Solar Energy Market was valued at 47.95 gigawatt in 2025 and estimated to grow from 52.83 gigawatt in 2026 to reach 85.77 gigawatt by 2031, at a CAGR of 10.18% during the forecast period (2026-2031).

Rapid capacity growth already lifts solar to 21% of national electricity generation, well ahead of the European Union average, and places the country on a clear trajectory to meet its 76 GW solar PV target under the revised National Energy and Climate Plan. Declining module prices, accelerated permitting aligned with EU Fit-for-55 mandates, and strong corporate PPA appetite underpin momentum across the Spain solar energy market. Hybrid solar-and-storage configurations, especially in high-irradiance provinces, are emerging as a hedge against curtailment and price cannibalization. International developers are deepening commitments, as illustrated by TotalEnergies' 263 MW Sevilla cluster and Plenitude's 330 MW Renopool project, while grid congestion and Natura-2000 land constraints temper short-term volumes.

Module prices continue to fall due to global oversupply, allowing projects in Castilla-La Mancha and Extremadura to reach competitive levelized costs even on lower-grade land. Bifacial panels paired with single-axis trackers now achieve capacity factors above 25%, widening the economic envelope for large ground-mounted plants. International utilities such as TotalEnergies cite capex savings of up to 15% compared with 2023 figures. Cost parity encourages hybridization with battery storage because freed capital can be reallocated to balance-of-system upgrades and energy management software. Local engineering firms report a notable shift toward 1,500 VDC system designs that cut cable losses and labor inputs. The net effect is an enlarged Spain solar energy market pipeline in regions previously on the economic margin.

Binding 2030 decarbonization targets give developers regulatory certainty, accelerating auction participation and bankability. Spain authorized 22,326 MW of PV construction in 2024 and cleared an additional 3,019 MW in Q1 2025. Regulatory alignment extends to storage: behind-the-meter batteries now qualify for capacity revenues, improving cash flows for distributed assets. Regional authorities echo the national stance; the Junta de Andalucia fast-tracked grid interconnection for 1.4 GW of projects in 2025. Clear policy timelines minimize merchant-price risk, drawing foreign direct investment into the Spain solar energy market.

Protected zones cover about 30% of Spain and trigger full environmental impact studies for any project footprint larger than 5 hectares. Murcia alone plans 30,000 ha of PV by 2030, yet 60% lies on former cropland that faces organized opposition from farm cooperatives. Developers increasingly target brownfield sites such as disused mines, adding EUR 50,000-100,000/MW in remediation costs. Concentration in low-conflict land funnels capacity into regions already constrained by weak transmission, thereby amplifying curtailment risk.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Solar photovoltaic commanded 94.45% of the Spain solar energy market in 2025 and is expanding at a 10.45% CAGR to 2031, whereas CSP's PNIEC target has fallen to 4.8 GW. Lithium-ion batteries cost below USD 140/kWh in 2024 and enable two-to-four-hour storage at half the cost of molten-salt systems, so developers prioritise PV-plus-battery hybrids. Spain's solar energy market size for photovoltaic additions will therefore increase by more than 31 GW between 2025 and 2030.

CSP still offers industrial process heat at EUR 20-50/MWh, cheaper than volatile natural gas prices, and Spain hosts 2.3 GW of operating plants. Yet no new utility-scale CSP projects reached financial close in 2024. As utilities redeploy capital into bifacial PV with n-type cells that lift yield by 10-15%, CSP's share will shrink further.

The Solar Energy Market Report is Segmented by Technology (Solar Photovoltaic and Concentrated Solar Power), Grid Type (On-Grid and Off-Grid), and End-User (Utility-Scale, Commercial and Industrial, and Residential). The Market Sizes and Forecasts are Provided in Terms of Installed Capacity (GW).