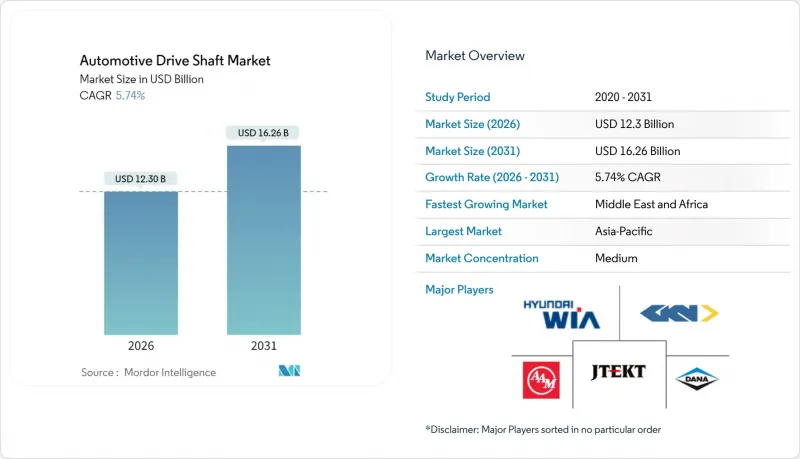

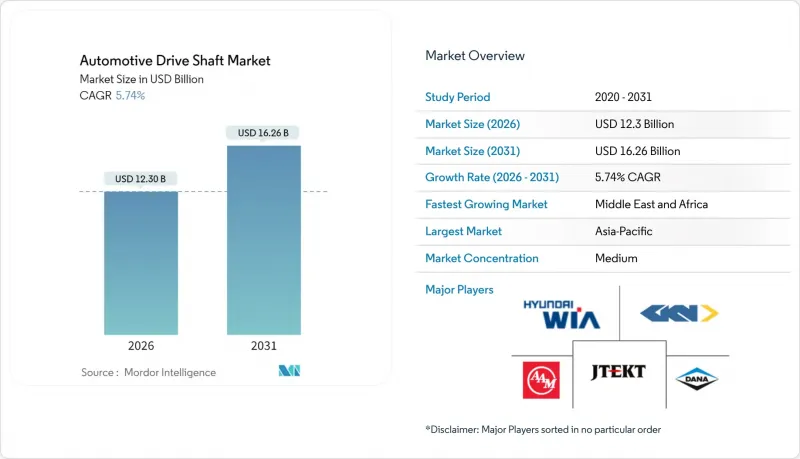

자동차용 드라이브 샤프트 시장 규모는 2026년에 123억 달러로 추정되고 있습니다. 2025년 116억 3,000만 달러에서 성장하며, 2031년에는 162억 6,000만 달러에 달할 것으로 예측되고 있습니다. 2026-2031년에는 CAGR 5.74%로 성장할 전망입니다.

이러한 성장 궤적은 기존 파워트레인의 견고한 성능을 유지하면서 전동화 수요에 적응하는 시장의 태도를 반영하고 있습니다. 자동차 제조업체들이 다양한 차량 아키텍처에서 비용 압박과 성능 요구사항의 균형을 맞추기 위해 다양한 부품으로 구성된 기존 샤프트에서 고정밀 경량 대체품으로 전환하는 것은 혼란과 기회를 동시에 가져오고 있습니다.

E-axle의 통합은 기존의 다중 부품 구성을 없애는 동시에 후륜구동 전기자동차 아키텍처에서 고정밀 경량 프로펠러 샤프트에 대한 수요를 창출함으로써 구동축 요구 사항을 근본적으로 변화시킬 것입니다. 테슬라의 Model S Plaid와 BMW iX는 통합형 모터-기어박스 유닛이 부품 수를 줄이면서 토크 벡터링 용도를 위한 특수 탄소섬유 프로펠러 샤프트를 필요로 하는 실례를 보여주고 있습니다. 이러한 아키텍처 전환은 차량당 샤프트 사용량이 감소할 가능성이 있음에도 불구하고 BEV 부문이 14.25%의 연평균 복합 성장률(CAGR)로 성장할 수 있는 이유를 설명합니다. 쉐플러가 2025년 4월부터 중국 전기자동차 제조업체를 위한 볼 스크루 드라이브를 생산하기 시작한 사례는 공급업체가 기존 드라이브라인 용도에서 전기 파워트레인에 정밀 제조 역량을 적용하는 방법을 보여줍니다. 이러한 전환은 첨단 소재에 대한 전문성을 갖춘 공급업체에게는 기회를 가져다주지만, 전통적 철강 중심 제조업체에게는 도전이 될 수 있습니다.

경량화 요구와 NVH 개선 요구를 배경으로 탄소섬유 복합재 샤프트의 채용은 고급차 영역을 넘어 고성능 지향의 양산차까지 확대되고 있습니다. 포드의 최신형 F-150 시리즈와 BMW 3시리즈는 고토크 조건에서 내구성을 유지하면서 연비 목표를 달성하기 위해 탄소섬유 프로펠러 샤프트를 채택하고 있습니다. 강철 대비 60%의 경량화를 실현하는 이 소재는 임계 속도 제한 없이 샤프트 길이를 연장할 수 있으며, 특히 패키징 제약이 심한 사륜구동(AWD) 구성에서 그 가치를 발휘합니다. 생산 규모 확대에 따라 탄소섬유 샤프트의 비용은 연간 약 15-20% 절감되어 기존 프리미엄 부문 중심에서 대량 생산용으로의 경제적인 채택이 가능해졌습니다. 이러한 추세는 하이브리드 및 전기 파워트레인의 배터리 무게 증가를 상쇄하기 위해 OEM 업체들이 경량화 전략을 우선시함에 따라 가속화되고 있습니다.

탄소섬유와 특수강 가격 변동은 드라이브 샤프트 공급망 전체에 이익률 압박을 가져왔습니다. 탄소섬유 가격은 항공우주 수요 사이클과 에너지 비용에 따라 분기별로 25-30% 변동합니다. 탄소섬유 생산이 소수의 세계 공급업체(도레이, SGL카본, 헥셀)에 집중되어 있으며, 항공우주 수요 회복 및 재생에너지 적용에 따른 수요 급증시 공급 병목현상이 발생할 수 있습니다. 고성능 응용 분야용 특수강 등급도 비슷한 가격 변동에 직면하고 있으며, 광산 산업의 혼란과 지정학적 긴장으로 인한 원료 공급의 영향으로 크롬 몰리브덴 합금 가격은 2024년 18% 상승했습니다. 이러한 변동성으로 인해 공급업체는 동적 가격 책정 메커니즘과 헤지 전략을 도입해야 하며, 이는 장기 OEM 계약을 복잡하게 만들고 있습니다. 이로 인해, 비용 중심의 응용 분야에서 첨단 소재의 도입이 늦어질 수 있습니다.

중공축은 2025년 56.63% 시장 점유율을 차지할 것으로 예상되며, 이는 솔리드 축에 비해 무게 감소와 제조 비용 효율성의 최적 균형을 반영합니다. 설계상의 장점으로는 최적화된 벽 두께 설계로 동등한 토크 용량을 유지하면서 솔리드 축 대비 40-50% 경량화를 실현합니다. 복합재/CFRP 샤프트는 고급차량의 채택과 경량화가 재료비 상승을 정당화할 수 있는 성능 중심의 응용 분야에 힘입어 2031년까지 연평균 복합 성장률(CAGR) 12.62%로 확대될 것으로 예측됩니다. 이중 분할/슬립 인 튜브 구조는 특히 공간 제약으로 인해 일체형 샤프트 설치가 어려운 전륜 구동 차량과 같은 소형 차량 구조의 특정 패키징 요구 사항을 충족합니다.

중량급 상용차 및 오프로드용은 내구성에 대한 요구사항이 무게에 대한 고려를 능가하므로 솔리드 샤프트가 지속적으로 채택되고 있습니다. 이 부문의 안정성은 첨단 소재보다 검증된 신뢰성을 우선시하는 상용차 제조업체의 보수적인 태도를 반영합니다. 하이드로포밍 및 첨단 용접 기술을 포함한 중공 샤프트 제조의 혁신으로 비용 경쟁력을 유지하면서 차량 부문 전반에 걸쳐 설계 적용성이 지속적으로 확대되고 있습니다.

2025년 기준 기존형 강재가 67.32% 시장 점유율을 유지하고 있으며, 이는 비용 효율성과 세계 공급망에 구축된 제조 인프라가 반영된 결과입니다. 그러나 탄소섬유/CFRP 소재는 2031년까지 14.33%의 연평균 복합 성장률(CAGR)로 급성장할 것으로 예상되며, 프리미엄 용도를 넘어 경량화 솔루션으로 근본적인 전환이 이루어지고 있음을 보여주고 있습니다. 고강도 합금강은 경량화 요구가 기존 강재의 능력을 초과하지만, 비용 제약으로 인해 탄소섬유 채택이 제한되는 중간 용도에 사용됩니다. 알루미늄의 적용은 내식성과 적당한 무게 감소가 철강 대체재에 대한 재료 프리미엄을 정당화하는 특정 이용 사례에 초점을 맞추었습니다.

이러한 소재 전환은 연비 규제와 전기자동차 항속거리 최적화에 따른 자동차 산업 전반의 경량화 요구를 반영하고 있습니다. 자동 섬유 배치 및 수지 이송 성형을 포함한 탄소섬유 제조 규모 확대는 생산 비용 절감과 품질 안정성 향상을 동시에 실현할 수 있습니다. 이러한 기술적 진보로 인해 기존에는 강철 소재가 주류를 이루었던 대량 생산 분야, 특히 길이와 임계 속도 요구 사항으로 인해 경량 소재가 유리한 프로펠러 샤프트 분야에 탄소섬유를 채택할 수 있게 되었습니다.

2025년에는 아시아태평양이 45.72% 시장 점유율을 차지할 것으로 예상되며, 중국의 대규모 자동차 생산 규모와 아세안 국가의 상용차 생산 능력 확대가 견인차 역할을 할 것입니다. 이 지역의 성장은 인프라 개발 계획에 따른 상용차 수요 증가에 기인하며, 특히 인도네시아, 태국, 베트남의 산업 회랑 개발은 지속적인 화물 운송 수요를 창출하고 있습니다. 2025년 2월 중국의 상용차 생산량은 31만 8,000대(전년 대비 36.6% 증가)에 달하고, 지역내 샤프트 수요의 규모를 보여줍니다. 이 지역공급업체들은 주요 OEM 생산 시설과의 근접성과 확립된 공급망 관계로 인해 물류 비용과 리드타임을 절감할 수 있는 이점을 누리고 있습니다.

북미와 유럽은 성숙된 시장으로, 다양한 차량 부문의 구동축 부품에 대한 안정적인 수요를 견인하는 탄탄한 자동차 제조 거점들이 있습니다. 북미의 성장은 SUV 및 픽업트럭 부문에 집중되어 있으며, 사륜구동(AWD)의 보급으로 차축간 프로펠러 샤프트에 대한 수요가 창출되고 있습니다. 한편, 유럽 시장에서는 엄격한 배기가스 규제를 배경으로 경량화 소재의 채택이 강조되고 있습니다. 두 지역 모두 프리미엄 응용 분야와 첨단 소재에 대한 집중은 탄소섬유 기술 및 정밀 제조 능력을 갖춘 공급업체에게 기회를 제공합니다. 미국의 섹션 48C 프로그램, 유럽연합의 그린딜 산업 정책 등 두 지역의 정부 인센티브는 국내 부품 생산을 촉진하는 현지 제조 개발을 지원하고 있습니다.

중동 및 아프리카은 인프라 개발 계획과 지역 전체의 자동차 보유율 증가에 힘입어 2031년까지 연평균 복합 성장률(CAGR) 8.77%로 가장 빠르게 성장하는 지역으로 부상하고 있습니다. 남아공의 자동차 생산 확대와 아랍에미리트(UAE)의 물류 허브 개발이 상용차 부품 수요를 창출하는 한편, 산유국의 경제 다각화 프로그램이 자동차 조립 사업을 지원하고 있습니다. 이 지역의 성장은 교통 인프라와 상용차 차량에 대한 지속적인 수요를 창출하는 광범위한 산업화 추세를 반영합니다. 다만, 정책적 지원과 제조능력의 차이에 따라 성장궤도가 다르기 때문에 국가별로 시장 편차가 존재합니다.

Automotive drive shaft market size in 2026 is estimated at USD 12.3 billion, growing from 2025 value of USD 11.63 billion with 2031 projections showing USD 16.26 billion, growing at 5.74% CAGR over 2026-2031.

This growth trajectory reflects the market's adaptation to electrification demands while maintaining robust performance in traditional powertrains. The transition from multi-piece conventional shafts to high-precision lightweight alternatives creates both disruption and opportunity, as OEMs balance cost pressures with performance requirements across diverse vehicle architectures.

E-axle integration fundamentally alters drive shaft requirements by eliminating traditional multi-piece configurations while creating demand for high-precision lightweight propeller shafts in rear-wheel-drive electric architectures. Tesla's Model S Plaid and BMW iX demonstrate how integrated motor-gearbox units reduce component count yet require specialized carbon-fiber propeller shafts for torque vectoring applications. This architectural shift explains why BEV segments grow at 14.25% CAGR despite potentially reducing per-vehicle shaft content. Schaeffler's April 2025 production launch of ball screw drives for Chinese EV manufacturers illustrates how suppliers adapt precision manufacturing capabilities from traditional driveline applications to electric powertrains. The transition creates opportunities for suppliers with advanced materials expertise while challenging traditional steel-focused manufacturers.

Carbon-fiber composite shaft adoption extends beyond luxury applications into performance-oriented mainstream vehicles, driven by weight reduction mandates and NVH improvement requirements. Ford's latest F-150 variants and BMW's 3-Series incorporate carbon-fiber propeller shafts to achieve fuel economy targets while maintaining durability under high-torque conditions. The material's 60% weight reduction compared to steel enables longer shaft lengths without critical speed limitations, particularly valuable in AWD configurations where packaging constraints intensify. Manufacturing scale improvements reduce carbon-fiber shaft costs by approximately 15-20% annually, making adoption economically viable for volume applications beyond the traditional premium segment focus. This trend accelerates as OEMs prioritize lightweighting strategies to offset battery weight penalties in hybrid and electric powertrains.

Carbon fiber and specialty steel price volatility creates margin pressure across the drive shaft supply chain, with carbon fiber prices fluctuating 25-30% quarterly based on aerospace demand cycles and energy costs. The concentration of carbon fiber production among few global suppliers (Toray, SGL Carbon, Hexcel) creates supply bottlenecks when demand surges from aerospace recovery and renewable energy applications. Specialty steel grades used in high-performance applications face similar volatility, with chromium-molybdenum alloy prices increasing 18% in 2024 due to mining disruptions and geopolitical tensions affecting raw material supply. This volatility forces suppliers to implement dynamic pricing mechanisms and hedge strategies that complicate long-term OEM contracts, potentially slowing adoption of advanced materials in cost-sensitive applications.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Hollow shafts command 56.63% market share in 2025, reflecting their optimal balance of weight reduction and manufacturing cost efficiency compared to solid alternatives. The design's advantages include 40-50% weight reduction versus solid shafts while maintaining equivalent torque capacity through optimized wall thickness engineering. Composite/CFRP shafts accelerate at 12.62% CAGR through 2031, driven by premium vehicle adoption and performance applications where weight savings justify higher material costs. Two-piece/slip-in tube configurations serve specific packaging requirements in compact vehicle architectures, particularly in front-wheel-drive applications where space constraints limit single-piece shaft installation.

Solid shaft applications persist in heavy-duty commercial vehicles and off-road applications where durability requirements outweigh weight considerations. The segment's stability reflects commercial vehicle manufacturers' conservative approach, prioritizing proven reliability over advanced materials. Manufacturing innovations in hollow shaft production, including hydroforming and advanced welding techniques, continue to expand the design's applicability across vehicle segments while maintaining cost competitiveness against solid alternatives.

Conventional steel maintains 67.32% market share in 2025, reflecting its cost-effectiveness and established manufacturing infrastructure across global supply chains. However, carbon-fiber/CFRP materials surge at 14.33% CAGR through 2031, indicating a fundamental shift toward lightweight solutions that extends beyond premium applications. High-strength alloy steel serves intermediate applications where weight reduction requirements exceed conventional steel capabilities but cost constraints limit carbon-fiber adoption. Aluminum applications focus on specific use cases where corrosion resistance and moderate weight reduction justify the material premium over steel alternatives.

The material transition reflects broader automotive lightweighting mandates driven by fuel economy regulations and electric vehicle range optimization. Carbon-fiber manufacturing scale improvements, including automated fiber placement and resin transfer molding, reduce production costs while improving quality consistency. This technological advancement enables carbon-fiber adoption in volume applications previously dominated by steel, particularly in propeller shaft applications where length and critical speed requirements favor lightweight materials.

The Automotive Drive Shaft Market Report is Segmented by Design Type (Hollow Shaft, Solid Shaft, Two-piece/Slip-in Tube, and More), Material (Conventional Steel, and More), Position Type (Rear Axle Shafts, and More), Vehicle Type (Passenger Cars, and More), Powertrain/Propulsion (ICE, Hybrid, BEV), Sales Channel (OEM, Aftermarket), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific dominates with 45.72% market share in 2025, driven by China's massive vehicle production scale and ASEAN's expanding commercial vehicle manufacturing capabilities. The region's growth stems from infrastructure development programs that boost commercial vehicle demand, particularly in Indonesia, Thailand, and Vietnam where industrial corridor development creates sustained freight transportation requirements. China's February 2025 commercial vehicle production of 318,000 units, representing 36.6% year-over-year growth, demonstrates the scale of demand driving regional shaft requirements. Regional suppliers benefit from proximity to major OEM production facilities and established supply chain relationships that reduce logistics costs and lead times.

North America and Europe represent mature markets with established automotive manufacturing bases that drive steady demand for drive shaft components across diverse vehicle segments. North American growth focuses on SUV and pickup truck segments where AWD proliferation creates demand for inter-axle propeller shafts, while European markets emphasize lightweight materials adoption driven by stringent emissions regulations. The regions' focus on premium applications and advanced materials creates opportunities for suppliers with carbon-fiber expertise and precision manufacturing capabilities. Government incentives in both regions support local manufacturing development, with the U.S. Section 48C program and European Union's Green Deal industrial policy encouraging domestic component production.

Middle-East and Africa emerges as the fastest-growing region at 8.77% CAGR through 2031, driven by infrastructure development programs and increasing vehicle ownership rates across the region. South Africa's automotive manufacturing expansion and UAE's logistics hub development create demand for commercial vehicle components, while oil-rich nations economic diversification programs support automotive assembly operations. The region's growth reflects broader industrialization trends that create sustained demand for transportation infrastructure and commercial vehicle fleets. However, the market is uneven across countries, with differing policy support and manufacturing capacity shaping growth trajectories.