자동차용 드라이브 샤프트 시장 : 시장 기회, 성장 요인, 산업 동향 분석 및 예측(2026-2035년)

Automotive Drive Shaft Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1936515

리서치사:Global Market Insights Inc.

발행일:2026년 01월

페이지 정보:영문 250 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

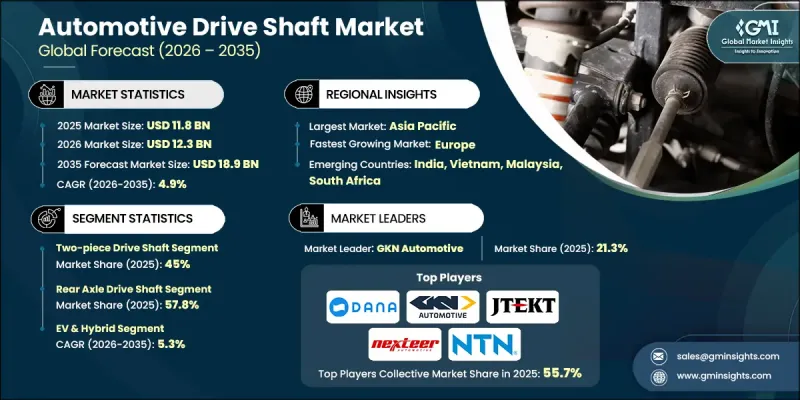

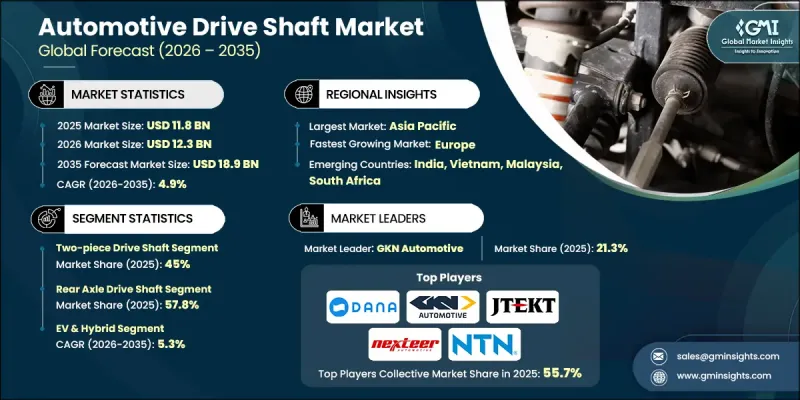

세계의 자동차 드라이브 샤프트 시장은 2025년에 118억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 4.9%로 성장할 전망이며, 189억 달러에 이를 것으로 예측됩니다.

시장 성장은 승용차 및 상용차 카테고리에서 세계 자동차 생산량 증가와 밀접한 관련이 있습니다. 차량 생산이 증가함에 따라 필수 구동 시스템 구성 요소에 대한 수요도 지속적으로 증가하고 있으며, 드라이브 샤프트는 현대 자동차 구조에서 중요한 요소로 자리잡고 있습니다. 이러한 구성 요소는 동력 전달에서 매우 중요한 역할을 하며 차량의 드라이브 라인 및 변속기 시스템에 필수적인 요소입니다. 자동차 업계 전체에서의 전동화의 확대는 시장 성장의 기세를 더욱 뒷받침하고 있습니다. 전기자동차 및 하이브리드 자동차 플랫폼은 독특한 토크 특성과 컴팩트한 파워트레인 레이아웃을 지원하는 설계 드라이브 샤프트가 필요하기 때문입니다. 기존 차량과 전동화 차량의 제조가 지속적으로 증가하고 있는 것은 장기적인 수요를 강화하는 요인이 되고 있습니다. 자동차 제조업체 각사는 규제 압력 및 효율 목표에 대한 대응으로서 경량화를 우선하고 있으며, 이것이 구동계 부품 전체의 기술 혁신을 가속시키고 있습니다. 병행하여 애프터마켓 분야도 시장 확대에 크게 기여하고 있습니다. 노후화된 차량에는 교체 부품이 필요하기 때문에 기존 및 첨단 드라이브 샤프트 솔루션에 대한 수요가 지속적으로 유지되고 있습니다.

시장 범위

시작 연도

2025년

예측 연도

2026-2035년

시작 시 가치

118억 달러

예측 금액

189억 달러

CAGR

4.9%

제조업체 각사는 효율성 및 차량 다이나믹스를 향상시키는 대체 재료의 채용에 의해 경량 구조로의 이행을 가속하고 있습니다. 부품 중량 감소는 배출 가스 규제 준수를 지원하면서 연비 및 성능 향상에 기여합니다. 이러한 고급 재료의 채택은 특히 엄격한 효율성 요구 사항이 부과되는 지역에서 두드러집니다. 애프터마켓은 차량의 장수명화에 의해 혜택을 받고 있으며, 다양한 재료 유형에 걸친 안정된 교환 수요를 견인하고 있습니다.

2025년 현재, 투피스 드라이브 샤프트 부문은 45%의 점유율을 차지하였으며, 53억 달러 시장 규모를 창출했습니다. 이 구조는 특히 수요가 높은 유틸리티 차량 및 상용 차량 부문에서 연장된 드라이브 라인 길이가 필요한 차량에 널리 채택됩니다. 모듈형 구조는 설치의 용이성, 취급의 간소화, 효율적인 유지보수를 실현하여 세계 시장에서의 보급에 기여하고 있습니다.

리어 액슬용 드라이브 샤프트 부문은 2025년에 57.8%의 점유율을 차지했으며, 2035년까지 103억 달러에 달할 것으로 예측됩니다. 여러 차량 카테고리에서 후륜 구동 및 전륜 구동 아키텍처의 강력한 채택이 수요를 지속적으로 지원하고 있습니다. 리어 액슬 구성은 구조적 이점과 설계 복잡성을 줄이기 때문에 대형 차량, 특히 실용성에 중점을 둔 운송 수요가 강한 지역에서 선호되는 옵션입니다.

미국의 자동차용 드라이브 샤프트 시장은 2025년 12억 8,000만 달러에 달했습니다. 국내 제조업체는 강도 중량비와 종합 효율의 향상을 향해, 선진 재료 및 세련된 생산 기술의 채용을 계속하고 있습니다. 연비 효율 및 배출 가스 감소에 대한 규제 압력은 부품 설계 및 재료 선정에 영향을 미치는 주요 촉진요인으로 계속되고 있습니다.

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

세계 자동차 생산 및 판매 증가

배터리식 전기자동차(BEV)에 있어서 E-axle 통합

연비 효율 향상을 위한 경량 소재 채용

후륜 구동 및 사륜 구동(AWD) SUV로의 전환

업계의 잠재적 위험 및 과제

시장 포화 및 치열한 가격 경쟁

내연기관(ICE) 탑재 승용차의 판매 감소 경향

시장 기회

전기자동차 및 하이브리드 자동차용 드라이브 샤프트의 커스터마이즈

탄소섬유 복합재료 기술의 상업화

신흥국에서 애프터마켓의 성장

아프리카 및 라틴아메리카의 미개척 시장

성장 가능성 분석

규제 상황

북미

미국 도로교통안전국(NHTSA)

EPA(환경보호청)

자동차 기술회(SAE International)

캐나다 운수성

노동안전보건국(OSHA)

유럽

유럽위원회(EC)

유럽 자동차 공업회(ACEA)

유럽표준화위원회(CEN)

아시아태평양

국토교통성(MLIT)

중화인민공화국 공업정보화부(MIIT)

인도 자동차 연구협회(ARAI)

라틴아메리카

국립 계량, 품질 및 기술 연구소(INMETRO)

멕시코 경제성 사무국(SE)

아르헨티나 국가교통안전국(ANTSV)

중동 및 아프리카

GCC 표준화 기구(GSO)

남아프리카 표준국(SABS)

사우디아라비아 규격, 계량 및 품질 기구(SASO)

Porter's Five Forces 분석

PESTEL 분석

기술 및 혁신 동향

현재 기술 동향

신흥 기술

가격 동향

지역별

제품별

생산 통계

생산 거점

소비 거점

수출 및 수입

비용 내역 분석

지속가능성 및 환경 영향

환경 영향 평가

사회적 영향 및 지역사회에 대한 공헌

거버넌스 및 기업의 사회적 책임

지속 가능한 금융 및 투자 동향

제품 수명주기 분석

드라이브 샤프트의 라이프사이클 단계

재료별 라이프사이클

고장 모드 및 수명 주기 제한 요인

예지보전 및 라이프사이클 연장

사용한 차량의 폐기 및 재활용

전기자동차 및 하이브리드차에 대한 영향 분석

EV 구동계 아키텍처 및 드라이브 샤프트에 대한 영향

EV 특유의 드라이브 샤프트 요건

하이브리드 자동차 드라이브 샤프트의 복잡성

경쟁 구도의 변화

사례 연구

OEM 구동계 아키텍처의 매핑

시스템 레벨에서 구동계 컴포넌트의 상호작용

NVH 성능 및 차량 다이나믹스의 벤치마크

애프터마켓에 있어서 고장 모드 및 교환 경제성

전망 및 기회

제4장 경쟁 구도

서문

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

합병 및 인수

제휴 및 협업

신제품 발매

사업 확대 계획 및 자금 조달

제5장 시장 추계 및 예측 : 샤프트별(2022-2035년)

단일 구동 샤프트

투피스 드라이브 샤프트

슬립 인 튜브 구동 샤프트

제6장 시장 추계 및 예측 : 포지션별(2022-2035년)

프론트 액슬 드라이브 샤프트

리어 액슬 드라이브 샤프트

제7장 시장 추계 및 예측 : 설계 구조별(2022-2035년)

중공 드라이브 샤프트

강성 및 솔리드 드라이브 샤프트

제8장 시장 추계 및 예측 : 재료별(2022-2035년)

강재

알루미늄

탄소섬유

제9장 시장 추계 및 예측 : 차량별(2022-2035년)

승용차

SUV

세단

해치백

상용차

경상용차(LCV)

MCV

대형 상용차(HCV)

이륜차

제10장 시장 추계 및 예측 : 추진력별(2022-2035년)

내연기관(ICE)

전기자동차(EV) 및 하이브리드 자동차

배터리식 전기자동차(BEV)

하이브리드 전기자동차(HEV)

플러그인 하이브리드 전기자동차(PHEV)

제11장 시장 추계 및 예측 : 판매 채널별(2022-2035년)

OEM

애프터마켓

제12장 시장 추계 및 예측 : 지역별(2022-2035년)

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

러시아

체코 공화국

벨기에

네덜란드

아시아태평양

중국

인도

일본

한국

호주

싱가포르

말레이시아

인도네시아

베트남

태국

라틴아메리카

브라질

멕시코

아르헨티나

콜롬비아

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제13장 기업 프로파일

세계 기업

GKN Automotive

Dana

American Axle &Manufacturing(AAM)

NTN

Nexteer

JTEKT

Hyundai WIA

IFA

Neapco

Schaeffler

지역 제조업체

Wanxiang Qianchao

Xuchang Yuandong Driveshaft

TrakMotive Europe

EDS-ALL DRIVESHAFT

GuangZhou JunChi AutoParts

Drexler Automotive

Dorman Products

Quigley

신흥 제조업체

GSP Automotive

The Timken

Comer Industries

GNA Drivelines

Schaeffler

Elbe

Amalga Composites

AJY

영문 목차

영문목차

The Global Automotive Drive Shaft Market was valued at USD 11.8 billion in 2025 and is estimated to grow at a CAGR of 4.9% to reach USD 18.9 billion by 2035.

Market growth is tied to rising global vehicle production across passenger and commercial categories. As vehicle output increases, demand for essential drivetrain components continues to rise, positioning drive shafts as a critical element in modern automotive architecture. These components play a vital role in power transmission, making them indispensable to vehicle driveline and transmission systems. Expanding electrification across the automotive industry further supports market momentum, as electric and hybrid platforms require drive shafts engineered to manage distinct torque profiles and compact powertrain layouts. Continued growth in both conventional and electrified vehicle manufacturing reinforces long-term demand. Automakers are also responding to regulatory pressure and efficiency targets by prioritizing weight reduction, which is accelerating innovation across drivetrain components. In parallel, the aftermarket segment contributes significantly to market expansion as aging vehicles require replacement parts, sustaining consistent demand for both traditional and advanced drive shaft solutions.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$11.8 Billion

Forecast Value

$18.9 Billion

CAGR

4.9%

Manufacturers are increasingly shifting toward lightweight construction by adopting alternative materials that improve efficiency and vehicle dynamics. Reduced component weight enhances fuel economy and performance while supporting compliance with emissions standards. Adoption of these advanced materials is particularly strong in regions with stringent efficiency requirements. The aftermarket continues to benefit from vehicle longevity, driving steady replacement demand across diverse material types.

The two-piece drive shafts segment held 45% share in 2025 and generated USD 5.3 billion. This configuration is widely adopted in vehicles requiring extended driveline lengths, particularly in higher-demand utility and commercial segments. Modular construction supports easier installation, simplified handling, and more efficient maintenance, contributing to its widespread acceptance across global markets.

The rear axle drive shafts segment accounted for 57.8% share in 2025 and is projected to reach USD 10.3 billion by 2035. Strong adoption of rear-wheel and all-wheel drive architectures across multiple vehicle categories continues to support demand. Rear axle configurations offer structural advantages and reduced engineering complexity, making them a preferred choice in larger vehicles, particularly in regions with strong demand for utility-focused transportation.

U.S. Automotive Drive Shaft Market reached USD 1.28 billion in 2025. Domestic manufacturers continue to adopt advanced materials and refined production techniques to enhance strength-to-weight ratios and overall efficiency. Regulatory pressure related to fuel efficiency and emissions reduction remains a key driver influencing component design and material selection.

Major companies operating in the Global Automotive Drive Shaft Market include GKN Automotive, Dana, American Axle & Manufacturing, NTN, Nexteer Automotive, Neapco, JTEKT, Hyundai WIA, Wanxiang Qianchao, and IFA. To strengthen their foothold, companies in the automotive drive shaft industry focus on material innovation, production efficiency, and strategic partnerships with vehicle manufacturers. Investment in lightweight engineering enables compliance with efficiency standards while improving performance. Portfolio diversification across vehicle types and drivetrain architectures allows suppliers to serve both conventional and electrified platforms. Expansion of aftermarket offerings supports recurring revenue streams. Manufacturers also prioritize automation and precision manufacturing to enhance quality and reduce costs.

Table of Contents

Chapter 1 Methodology

1.1 Research approach

1.2 Quality commitments

1.2.1 GMI AI policy & data integrity commitment

1.3 Research trail & confidence scoring

1.3.1 Research trail components

1.3.2 Scoring components

1.4 Data collection

1.4.1 Partial list of primary sources

1.5 Data mining sources

1.5.1 Paid sources

1.6 Base estimates and calculations

1.6.1 Base year calculation

1.7 Forecast model

1.8 Research transparency addendum

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Shaft

2.2.3 Position

2.2.4 Design Structure

2.2.5 Material

2.2.6 Vehicle

2.2.7 Propulsion

2.2.8 Sales Channel

2.3 TAM analysis, 2026-2035

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Increasing global vehicle production & sales

3.2.1.2 E-axle integration in battery electric vehicles (BEVs)

3.2.1.3 Lightweight material adoption for fuel efficiency