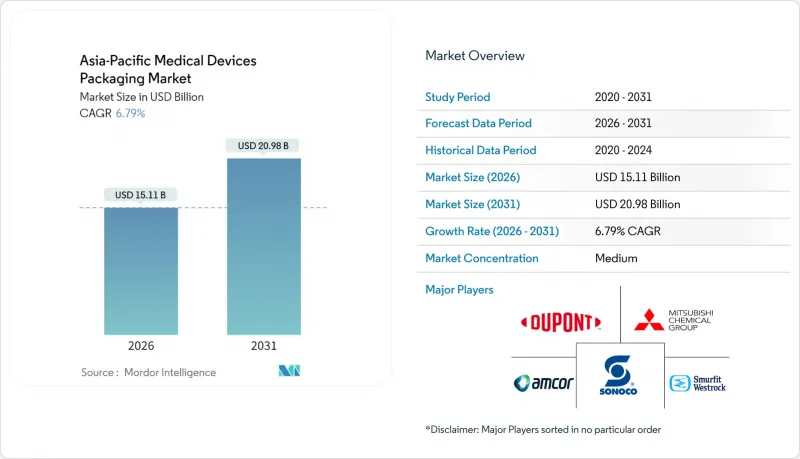

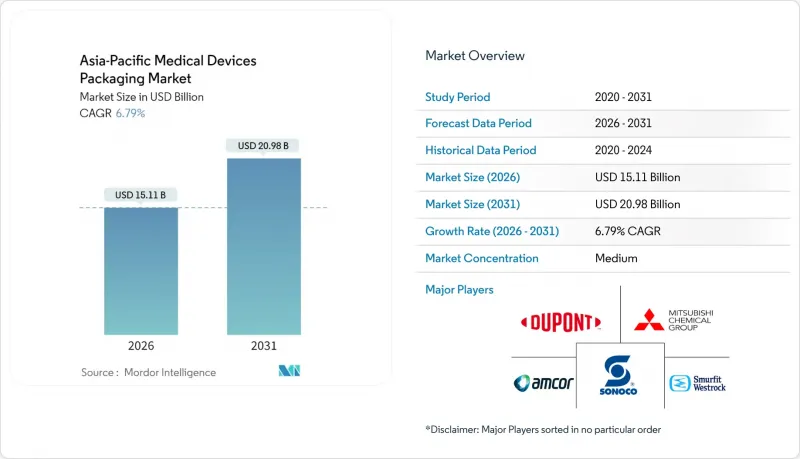

아시아태평양의 의료기기 포장 시장 규모는 2026년에 151억 1,000만 달러로 추정되고 있습니다. 이는 2025년 141억 5,000만 달러에서 성장한 수치이며, 2031년에는 209억 8,000만 달러에 달할 것으로 예측되고 있습니다. 2026-2031년에는 CAGR 6.79%로 성장이 전망되고 있습니다.

중국, 인도, 동남아시아의 견고한 제조업 성장, 일본, 호주 등 선진국의 의료비 지출 증가, 스마트 및 센서 지원 포장으로의 꾸준한 전환이 아시아태평양 의료기기 포장 시장의 주요 성장 요인으로 작용하고 있습니다. 비용 효율성이 높은 지역 생산기지가 플라스틱의 대규모 수요를 창출하는 한편, 바이오 대체품은 규제 측면에서 진전을 보이고 있습니다. 병원, 진료소, 계약 서비스 프로바이더가 가장 큰 구매층을 차지하고 있는 가운데, 환자 직접 배송형 EC 유통이 확대됨에 따라 소포의 무결성을 보장하기 위한 3차 포장의 재설계가 요구되고 있습니다. 경쟁의 격화는 멸균 장벽 검증, 지속가능성 대응, 디지털 추적성을 중심으로 전개되고 있으며, 이러한 능력을 습득한 공급업체는 아시아태평양 의료기기 포장 시장에서 고매출 계약을 체결할 수 있습니다.

다국적 의료기기 제조업체는 2024년 아시아로의 생산 이전을 가속화했습니다. 중국의 생산량은 12.3% 증가, 인도는 생산연동형 인센티브 제도 도입 후 생산능력이 18.7% 확대되었습니다. 베트남과 말레이시아에 집적된 공장군은 현재 검증된 배리어 소재를 경쟁력 있는 비용으로 요구되는 멸균 포장 라인을 공급하고 있습니다. 이러한 규모 확장을 통해 포장 가공업체는 자동화 투자를 상각하면서 여러 관할권에 걸친 수출 경로에서 ISO 11607을 만족시킬 수 있습니다. 그러나 지역적 수지 공급 제약으로 인해 이중 조달이 불가피한 상황에서 가공업체들은 동남아시아의 석유화학 파트너로 눈을 돌리고 있습니다. 그 결과, 아시아태평양 의료기기 포장 시장에서 트레이, 파우치, 라벨의 안정적인 수주를 지원하는 제조 생태계가 형성되고 있습니다.

아세안 규제 당국은 2024년 ISO 11607에 대한 조정을 추진하고 있으며, OEM(Original Equipment Manufacturer)는 필 파우치 및 열성형 트레이에 대한 검증을 강화해야 합니다. 감마선, 에틸렌옥사이드, 과산화수소 증기 멸균의 가동이 가속화됨에 따라 위탁 멸균업체의 가동률이 23% 상승했습니다. 항균 코팅을 한 배리어 기판은 멸균 주기를 변경하지 않고도 의료기기의 보존 기간을 연장할 수 있으며, 많은 사랑을 받고 있습니다. 여러 멸균 방법에 대한 밸리데이션을 제공하는 공급업체는 여러 국가에 걸친 계약을 체결하는 사례가 증가하고 있으며, 아시아태평양의 의료기기 포장 시장에서 입지를 강화하고 있습니다. 마찬가지로 의료기관도 의료 관련 감염을 억제하기 위해 변조 방지 기능을 갖춘 멸균 장벽을 의무화하고 있으며, 장기적인 수요를 지원하고 있습니다.

폴리에틸렌과 폴리프로필렌의 현물 가격 변동폭은 2024년 23%에 달하고, 고정가격 공급계약을 체결한 컨버터의 이익률을 떨어뜨렸습니다. 중국내 정유소 배출 규제 강화로 국내 수지 공급량이 감소함에 따라 지역 가격은 세계 평균보다 15% 이상 높았습니다. 대형 컨버터는 여러 국가에서 조달하거나 장기 계약을 통해 헤지하는 반면, 중소기업은 사업 통합의 압력에 직면해 있습니다. 수지 가격 리스크 증가는 가족 소유의 컨버터에 대한 설비투자를 억제하여 아시아태평양의 의료기기 포장 시장의 성장을 다소 억제할 것으로 예측됩니다.

플라스틱은 비용 효율성과 광범위한 멸균 대응성을 바탕으로 2025년 기준 아시아태평양 의료기기 포장 시장의 54.78%를 차지할 것으로 예측됩니다. 듀폰의 차세대 타이벡을 포함한 바이오 제품들은 여러 국가에서 허가를 받았으며, 2031년까지 연평균 복합 성장률(CAGR) 7.78%로 확대될 것으로 예측됩니다. 플라스틱 분야의 아시아태평양 의료기기 포장 시장 규모는 2025년 77억 5,000만 달러에 달할 것으로 예측됩니다. 그러나 일본과 호주의 규제상 탄소배출 상한선으로 인해 조달 부문은 재생원료로의 전환을 강요받고 있으며, 화학적 재생 폴리에틸렌을 이용한 파일럿 프로젝트가 가속화되고 있습니다. 금속과 호일은 임플란트 키트용 방사선 차폐층과 방습층에서 틈새 가치를 유지하고 있지만, 유리는 재사용 가능한 내시경과 고급 분석기기에만 제한적으로 적용되고 있습니다.

수지-필름 일관 생산 라인에 대한 투자는 주요 컨버터에게 공급의 연속성을 보장합니다. 재생 코어층과 버진 접촉면을 결합한 다층 공압출 기술은 ISO 10993을 준수하면서 버진 폴리머 사용량을 줄일 수 있습니다. 석유화학 공급업체와 매스밸런스 인증으로 제휴한 컨버터는 다국적 의료기기 입찰에서 유리한 고지를 점하고 있습니다. 따라서 지속가능성의 요구는 아시아태평양 의료기기 포장 시장에서 플라스틱 중심의 재료 포트폴리오를 개선하는 것이지, 플라스틱을 대체하는 것이 아닙니다.

파우치 및 백은 폼-필-실 방식의 경제성과 검증된 박리성으로 인해 2025년 매출의 36.05%를 차지할 것으로 예측됩니다. 아시아태평양의 의료기기 포장 시장에서 파우치 시장 규모는 2031년까지 연평균 6.04%의 연평균 복합 성장률(CAGR)로 확대될 것으로 예측됩니다. 한편, 열성형 트레이와 경질 용기는 로봇 수술 키트와 임플란트 시스템이 맞춤형 캐비티와 낙하 방지 기능을 필요로 하므로 연간 7.12%의 속도로 성장하고 있습니다. 소노코가 2024년에 출시한 재활용 가능한 트레이는 단단한 보호성과 지속가능한 수지 블렌드를 결합하여 병원의 폐기물 감소 목표에 부합하는 제품입니다.

블리스터팩은 인슐린 펜과 같은 의약품 및 의료기기 하이브리드 제품에 대응하며, 기존 블리스터 포장 인프라를 활용합니다. 골판지 상자는 병원 재고관리 소프트웨어와 연동되는 QR코드를 내장한 스마트 2차 포장재로 진화했습니다. 자동화 라인의 효율화로 포장 형태의 표준화가 진행되어 고속 실러의 처리 능력 극대화가 이루어지고 있습니다. 이러한 제품 유형의 혁신과 함께 아시아태평양의 의료기기 포장 시장은 다양한 선택권을 유지하고 있습니다.

Asia-Pacific medical devices packaging market size in 2026 is estimated at USD 15.11 billion, growing from 2025 value of USD 14.15 billion with 2031 projections showing USD 20.98 billion, growing at 6.79% CAGR over 2026-2031.

Robust manufacturing expansion across China, India, and Southeast Asia, rising healthcare spending in developed economies such as Japan and Australia, and a steady shift toward smart, sensor-enabled packs form the core growth drivers of the Asia-Pacific medical devices packaging market. Cost-efficient regional production hubs stimulate large-volume demand for plastics, even as bio-based alternatives gain regulatory traction. Hospitals, clinics, and contract service providers represent the largest buyers, while direct-to-patient e-commerce distribution urges tertiary pack redesign for parcel integrity. Competitive intensity revolves around sterile barrier validation, sustainability credentials, and digital traceability, allowing suppliers that master these capabilities to capture higher-margin contracts in the Asia-Pacific medical devices packaging market.

Multinational device makers intensified production migration to Asia in 2024, with China's output rising 12.3% and India's capacity climbing 18.7% after Production Linked Incentive funding. Clustered factories in Vietnam and Malaysia now feed sterile-pack volume lines that demand validated barrier materials at competitive cost. Such scaling enables packaging converters to amortize automation investment while satisfying ISO 11607 across multijurisdiction export lanes. Regional resin supply constraints nonetheless force dual-sourcing, nud,ging converters toward Southeast Asian petrochemical partners. The result is a manufacturing ecosystem that underpins steady orders for trays, pouches and labels in the Asia-Pacific medical devices packaging market.

ASEAN regulators harmonized toward ISO 11607 in 2024, prompting OEMs to upgrade peel-pouch and thermoformed tray validation. Contract sterilizers saw a 23% capacity-utilization jump as gamma, ethylene oxide, and vaporized hydrogen peroxide runs accelerated. Barrier substrates with antimicrobial coatings gain favor because they extend device shelf life without altering sterilization cycles. Suppliers that provide cross-method validation increasingly win multi-country contracts, boosting their footprint in the Asia-Pacific medical devices packaging market. Hospitals likewise mandate tamper-proof sterile barriers to curb healthcare-associated infections, reinforcing long-term demand.

Polyethylene and polypropylene spot swings hit 23% in 2024, pulling converter margins downward on fixed-price supply deals. China's stricter refinery emissions rules shrank domestic resin availability, pushing regional prices 15% above global averages. Larger converters hedge through multi-country sourcing and long-term contracts, while small firms face consolidation pressure. Elevated resin risk tempers capital spending across family-owned converters, mildly restraining growth in the Asia-Pacific medical devices packaging market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Plastics held 54.78% of the Asia-Pacific medical devices packaging market share in 2025, underpinned by cost-efficiency and broad sterilization compatibility. Bio-based variants, including DuPont's next-generation Tyvek, earned multi-country clearance and drive a 7.78% CAGR through 2031. The Asia-Pacific medical devices packaging market size allocated to plastics reached USD 7.75 billion in 2025. Yet regulatory carbon caps in Japan and Australia push procurement teams toward renewable feedstocks, accelerating pilot projects with chemically recycled polyethylene. Metals and foils retain niche value in radiation shielding and moisture-barrier layers for implant kits, while glass remains confined to reusable scopes and premium analyzers.

Investment in integrated resin-to-film lines secures supply continuity for leading converters. Multilayer co-extrusion that combines recycled core layers with virgin contact surfaces reduces virgin-polymer intensity without jeopardizing ISO 10993 compliance. Converters partnering with petrochemical suppliers on mass-balance certification now bid advantageously on multinational device tenders. The sustainability mandate, therefore, refines, but does not overturn, the plastic-led material portfolio in the Asia-Pacific medical devices packaging market.

Pouches and bags contributed 36.05% to 2025 revenue, owing to the form-fill-seal economy and validated peelability. The Asia-Pacific medical devices packaging market size for pouches is projected to advance at a 6.04% CAGR to 2031. Thermoformed trays and rigid containers, however, are expanding 7.12% annually as robotic surgery kits and implant systems need custom cavities and drop resistance. Sonoco's 2024 recyclable tray launch married rigid protection with sustainable resin blends, aligning with hospital waste-reduction targets.

Blister packs bridge pharmaceutical-device hybrids like insulin pens, leveraging existing blistering infrastructure. Corrugated cartons evolve into smart secondary carriers, embedding QR codes that sync with hospital inventory software. Automated line efficiency drives pack geometry standardization to maximize throughput in high-speed sealers. Collectively, product-type innovation sustains broad option ranges within the Asia-Pacific medical devices packaging market.

The Asia-Pacific Medical Devices Packaging Market Report is Segmented by Material (Plastics, Paper and Paperboard, and More), Product Type (Pouches and Bags, Trays and Containers, and More), Application (Sterile Packaging, and More), End User (Hospitals and Clinics, Diagnostic and Imaging Centers, and More), Packaging Level (Primary, Secondary, Tertiary), and Country. The Market Forecasts are Provided in Terms of Value (USD).