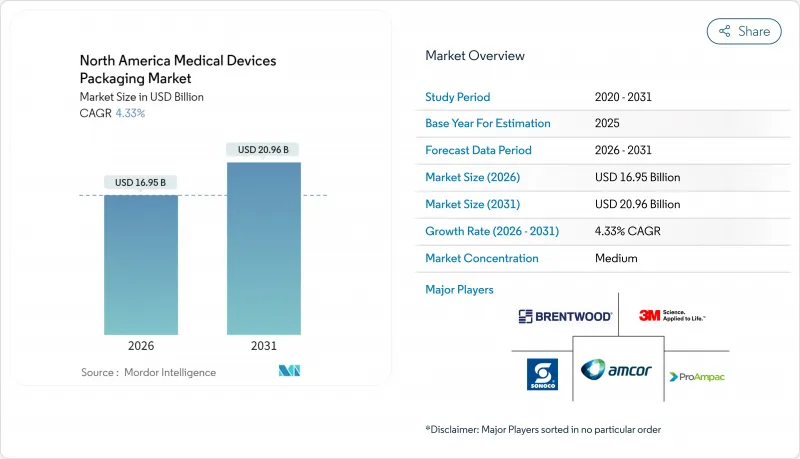

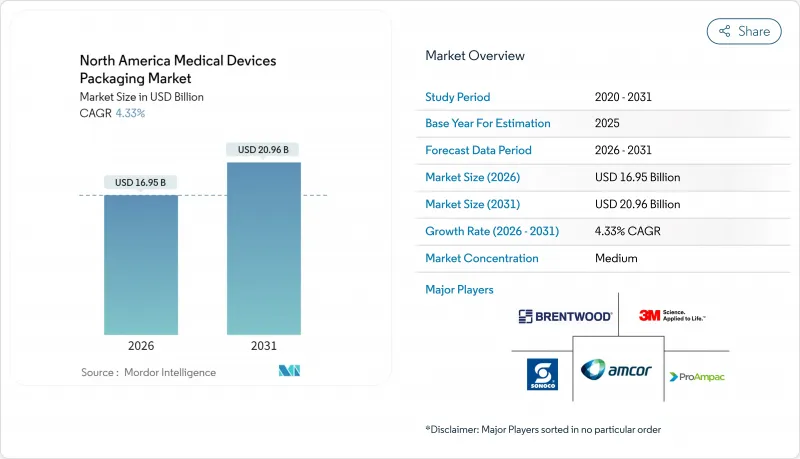

북미의 의료기기 포장 시장은 2025년 162억 5,000만 달러로 평가되었고, 2026년 169억 5,000만 달러에서 2031년까지 209억 6,000만 달러에 이를 것으로 예측됩니다. 예측 기간(2026-2031년) CAGR은 4.33%로 성장이 예상됩니다.

현재의 확장은 기존의 멸균 장벽 개념에서 복잡한 FDA의 추적 가능성 요구 사항을 충족하고 공급망의 탄력성을 향상시키는 지능형 저탄소 포장으로의 전환을 반영합니다. 선택적 수술 급증, UDI(제품 식별) 표시 규칙의 엄격화, 그리고 멸균성과 동등하게 지속가능성을 중시하는 병원의 구매 정책이 수요를 밀어 올리고 있습니다. 의료 제공업체가 재고를 재구성하는 동안 검증된 ISO 11607 시스템과 데이터 풍부한 콜드체인 모니터링을 결합한 생산자가 우선합니다. 한편, 복수의 멸균 방법을 견디면서 라이프 사이클 배출량을 삭감하는 바이오 베이스 폴리머 및 센서 탑재 포맷에 대한 자본 유입이 진행되고 있습니다.

수술의 백로그 해소에 수반해, 순환기 및 정형외과 분야에 있어서 고스루풋 멸균 팩 수요가 재연하고 있습니다. 병원에서는 현재, 보존 기간을 유지하면서 신속한 회전율을 실현할 수 있는 엔드 투 엔드로 검증이 끝난 배리어 시스템을 중시하고 있습니다. 실시간 재고 데이터에서 지원되는 ISO 11607 호환 형식을 제공하는 공급업체는 장기 계약을 받았습니다. 수지 코스트가 상승하는 가운데도, 대량 발주에 의해 단가당 이익률은 안정화하고 있습니다. 서비스 수준 보증을 충족하기 위해 자동 포장 라인에 대한 투자가 확대되고 있습니다.

일회용 기기는 고비용 재처리가 필요 없고 교차 오염 위험을 줄이기 위해 에톡실렌(EtO), 감마선, 전자선(e-beam) 내성 라미네이트 구조의 채용이 진행되고 있습니다. 포장 제조업체는 섬세한 내시경을 보호하면서 수술실에서 개봉의 편리성을 실현하는 멀티 캐비티 인서트 부착 열성형 트레이를 투입하고 있습니다. 저침습 키트에서 부품의 소형화로 통기성 및 입자 제어의 균형을 유지하는 정전기 방지 필름과 마이크로 퍼포레이션 뚜껑 수요가 높아지고 있습니다. 이러한 컴팩트한 포맷 내에 기계 판독가능한 UDI 코드를 통합하는 것이 조달의 전제조건이 되고 있습니다.

크래커의 작동 중지 및 물류 병목 현상으로 인해 공급이 제한되는 가운데 의료용 PP, HDPE 및 PETG의 가격은 높아지고 있습니다. 일부 컨버터는 다층 공압출 성형품을 얇은 단층 대체품으로 대체하고 있지만, 검증 타임라인은 채용을 늦추고 있습니다. 전가 조항이 포함된 계약 조건에 따라 대량 구매자의 이익률 감소가 완화되었습니다. 중소 컨버터는 복수 조달처에 의한 헤지를 실시하고 있지만, 운전 자금의 압박에 직면하고 있습니다. 수지 제조업체는 재생재 함유 제품의 확충을 진행하고 있습니다만, 의료 등급의 원료 공급원이 한정되어 있기 때문에 생산량은 제약을 받고 있습니다.

2025년 시점에서 무균 포장 형태가 북미 의료기기 포장 시장 규모의 87.98%를 차지하였고, 2031년까지 연평균 복합 성장률(CAGR) 5.48%로 확대하고 있습니다. 병원에서는 일회용 정책이 재확인되어 장기 유통 사이클을 견디는 엄격한 장벽 성능이 요구되고 있습니다. HDPE, EVOH, 타이벡을 조합한 다층 라미네이트는 산소 투과율을 낮게 억제하면서 수술실에서의 깨끗한 박리를 가능하게 합니다. 신흥의 일산화질소 멸균 기술은 이러한 라미네이트 구조 전체에서의 적합성 시험이 요구되고 있습니다.

혁신의 초점은 열 성형 가동 힌지를 갖춘 트레이에 있습니다. 이것은 섬세한 로봇 지원 수술 암을 보호하고 무균 상태를 유지합니다. 얇은 디자인은 ASTM F88 Seal 시험에서 입증된 것처럼 내천자성을 손상시키지 않고 플라스틱 소비를 줄입니다. 통합 RFID는 최종 단계 추적성을 허용하고 인라인 검사 카메라는 감사 추적을 위한 씰 균일성을 기록합니다. 소규모 공급업체는 검증 비용의 높이에 직면하고 있으며, 이로써 자사 시험소를 보유한 세계 컨버터에 집약이 진행되고 있습니다.

플라스틱은 2025년에 64.05%의 수익 점유율을 유지했지만, 바이오 베이스 폴리머는 2031년까지 연평균 복합 성장률(CAGR) 6.85%로 가장 급속히 확대될 전망이며, 조달 스코어카드에서 환경 지표에 최대 20%의 비중이 할당되는 현상을 반영하고 있습니다. 폴리유산 경질 바이알은 제조 공정에서의 에너지 소비를 42% 절감하고 FDA 식품 접촉 규제에 준거하고 있어 진단 키트의 채용이 진행되고 있습니다. 폴리하이드록시알카노에이트 필름은 본질적인 멸균 내성을 나타내지만, 발효 라인에 대한 높은 설비 투자가 과제가 되고 있습니다.

컨버터는 기계적 재생 PETG 층과 버진 접촉 층을 결합하여 ISO 10993 생체 적합성을 충족하면서 탄소 발자국을 줄입니다. 발포 PET 구조 코어 시트는 운송 트레이의 재료 소비를 더욱 줄입니다. 캘리포니아 및 브리티시컬럼비아 병원에서는 자본 설비 팩에 대한 환경 제품 선언(EPD)을 의무화하고 전환 가속을 촉진하고 있습니다. 그러나 임상 폐기물의 재활용 경로가 제한되어 있기 때문에 완전한 순환 사회의 실현에는 과제가 남아 있습니다.

The North America medical devices packaging market was valued at USD 16.25 billion in 2025 and estimated to grow from USD 16.95 billion in 2026 to reach USD 20.96 billion by 2031, at a CAGR of 4.33% during the forecast period (2026-2031).

Current expansion reflects a pivot from conventional sterile-barrier concepts toward intelligent, low-carbon packs that satisfy complex FDA traceability mandates and bolster supply-chain resilience. A surge in elective procedures, tighter UDI labeling rules, and hospital purchasing policies that rank sustainability alongside sterility continue to lift demand. Producers that pair validated ISO 11607 systems with data-rich cold-chain monitoring gain preference as providers rebuild inventories. Meanwhile, capital is flowing into bio-based polymers and sensor-enabled formats that tolerate multiple sterilization modalities while cutting lifecycle emissions.

Recovering surgical backlogs have reignited demand for high-throughput sterile packs across cardiovascular and orthopedic lines. Hospitals now emphasize end-to-end validated barrier systems that can handle faster turnover while preserving shelf life. Vendors offering ISO 11607-compliant formats supported by real-time inventory data are securing long-term contracts. Larger order quantities are stabilizing price-per-unit margins even as resin costs rise. Investment in automated packaging lines is gaining traction to meet service-level guarantees.

Single-use devices eliminate costly reprocessing and cut cross-contamination risk, driving uptake of EtO-, gamma-, and e-beam tolerant laminate structures. Packagers are launching thermoformed trays with multi-cavity inserts that protect delicate scopes yet enable peel-open convenience in the OR. Component miniaturization in minimally invasive kits has spurred demand for antistatic films and micro-perforated lids that balance breathability and particle control. Integration of machine-readable UDI codes within these compact formats is becoming a procurement prerequisite.

Medical-grade PP, HDPE, and PETG prices remain elevated as cracker outages and logistics bottlenecks constrain supply. Some converters substitute multi-layer coextrusions with thinner single-layer alternatives, but validation timelines slow adoption. Contract terms with pass-through clauses temper margin erosion for large-volume buyers. Smaller converters hedge via multi-sourcing but face working-capital strain. Resin producers are expanding recycled-content offerings, although limited medical-grade streams restrict volumes.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Sterile formats accounted for 87.98% of the North America medical devices packaging market size in 2025, advancing at a 5.48% CAGR toward 2031. Hospitals reaffirm single-use policies and demand rigorous barrier integrity that withstands extended distribution cycles. Multi-layer laminates integrating HDPE, EVOH, and Tyvek maintain low oxygen transmission rates while enabling clean peel in the OR. Emerging nitric-oxide sterilization technologies are prompting compatibility testing across these laminate structures.

Innovation centers on trays with thermoformed living hinges that cradle delicate robot-assisted surgical arms and preserve aseptic presentation. Thin-wall designs reduce plastic consumption without sacrificing puncture resistance, as validated by ASTM F88 seal tests. Integrated RFID enables last-mile traceability while in-line inspection cameras document seal uniformity for audit trails. Smaller suppliers face high validation costs that consolidate volume toward global converters with captive test labs.

Plastics retained 64.05% revenue share in 2025; however, bio-based polymers are scaling fastest with a 6.85% CAGR through 2031, reflecting procurement scorecards that now allocate up to 20% weighting to environmental metrics. Poly(lactic-acid) rigid vials cut cradle-to-gate energy by 42% and comply with FDA food-contact regulations, easing adoption in diagnostic kits. Poly(hydroxyalkanoate) films demonstrate intrinsic sterilization resilience yet contend with high capex for fermentation lines.

Converters combine mechanical-recycled PETG layers with virgin contact layers to lower carbon footprints while meeting ISO 10993 biocompatibility. Foamed PET structural core sheets further decrease material consumption in transport trays. Hospitals in California and British Columbia now mandate Environmental Product Declarations for capital equipment packs, encouraging faster transition. Yet, limited recycling streams for clinical waste hamper full-circularity visions.

The North America Medical Devices Packaging Market Report is Segmented by Product Type (Sterile Packaging, and Non-Sterile Packaging), Material Type (Plastics, Paper and Paperboard, and More), Application (Diagnostic Substances, Surgical and Medical Instruments, and More ), Packaging Type (Pouches and Bags, Trays and Clamshells, Boxes and Cartons, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).