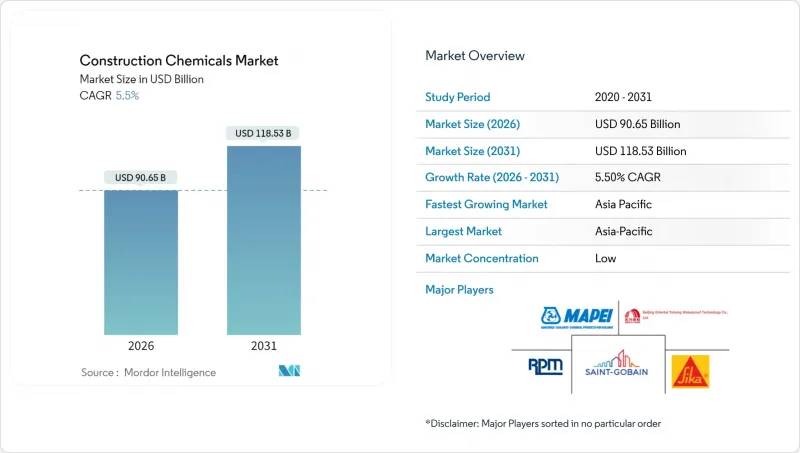

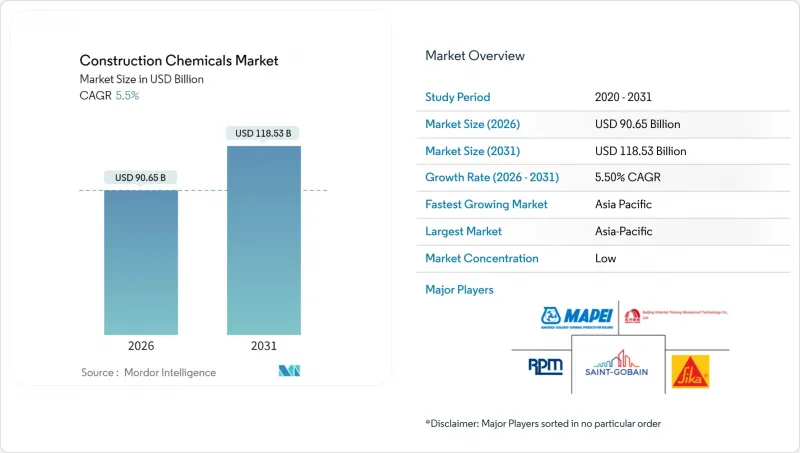

건설용 화학제품 시장 규모는 2026년에는 906억 5,000만 달러로 추정되고 있으며, 2025년 859억 2,000만 달러에서 성장이 전망됩니다. 2031년의 예측에서는 1,185억 3,000만 달러에 달하며, 2026-2031년에 CAGR 5.5%로 성장할 것으로 전망되고 있습니다.

탄탄한 도시 인프라 계획, 강화되는 그린 빌딩 규제, 안정적인 주택 수요와 함께 건설화학제품 시장의 성장 전망은 더욱 강화되고 있습니다. 방수 시스템은 보험사 및 건축 기준 당국이 습기 보호를 우선시하므로 제품 매출의 기반이 되고 있으며, 첨단 표면 처리 기술은 자동화 프리캐스트 공장에서 보급이 진행되고 있습니다. 지역적 성장세는 아시아태평양에 집중되어 있으며, 이 지역의 메가 프로젝트 계획은 특수화학제품의 채택을 가속화하고 있습니다. 성숙된 경제권에서는 신규 건설 활동이 둔화되는 가운데, 자산 재생 프로그램이 수요를 지원할 것입니다. 경쟁 환경은 배합 기술과 현장 기술 서비스를 통합하고 계약자가 더 엄격한 성능 사양을 충족하도록 지원하는 공급업체에게 유리합니다.

아시아태평양의 지속가능한 도시 건설 프로그램은 혼잡한 현장에서 내구성을 향상시키는 혼화제, 방수제, 양생제의 대량 소비를 주도하고 있습니다. 인도의 1조 4,000억 달러 규모의 국가 인프라 계획도 비슷한 촉매제가 되어 대규모 고속도로 및 지하철 프로젝트에서 슬래브의 연속성을 보장하기 위해 저수축 콘크리트 혼화제를 지정하고 있습니다. 유엔인간정주계획(UN-Habitat)은 2050년까지 25억 명의 도시 거주자가 증가할 것으로 예측하고 있으며, 교통, 유틸리티, 고층 주택과 관련된 화학제품 수요는 장기적으로 성장할 여지가 있음을 시사하고 있습니다. 또한 건설업체는 메가 프로젝트 일정을 준수하기 위해 빠른 경화 그라우트에 의존하고 있습니다. 이러한 요인들을 종합해 볼 때, 건설화학 시장에는 단기적인 변동을 넘어선 구조적인 수요가 내재되어 있다고 할 수 있습니다.

에너지 성능 지침에 따라 설계자는 탄소 배출량 상한선을 설정해야 하고, 콘크리트 제조업체는 고감수제 및 시멘트계 보조재 채택을 추진하고 있습니다. 유럽연합(EU)은 '건축물 에너지 성능 지침'에 따라 2030년까지 모든 신축 건물의 순배출량 제로를 달성하도록 의무화하고 있습니다. 미국의 LEED v4.1과 BREEAM 기준도 마찬가지로 저 VOC 실란트나 바이오 페인트를 평가 대상으로 삼고 있으며, 대두 폴리올계 폴리우레탄 타포린과 같은 프리미엄 틈새 시장을 활성화하고 있습니다. EPA 세이퍼초이스와 같은 제품 등록 제도는 시산업체의 사양 선택을 수성 시스템으로 더욱 유도합니다. 규제 시한에 앞서 제품을 개선하는 공급업체는 사양 선정에 대한 신뢰를 얻고, 건설화학 시장에서 가격 결정력을 강화할 수 있습니다.

원유 및 그 파생원료 가격의 변동은 공급업체의 이익률을 압박하고, 계약업체의 예산편성을 복잡하게 만들고 있습니다. 2024년까지 브렌트유는 배럴당 70-90달러에 거래될 것으로 예상되며, 프로파일렌과 에폭시 수지 가격도 비슷한 추세를 보일 것으로 보입니다. 제조업체들은 비용 급등을 흡수하거나 추가 요금을 부과하는 방식에 대응하고 있으며, 이로 인해 현장에서 고부가가치 제품 도입이 지연되는 경우도 볼 수 있습니다. 지정학적 리스크 증가는 공급망을 더욱 혼란스럽게 만들고 있으며, 배합 제조업체들은 바이오 폴리올과 재생 폴리머로 다각화를 추진하고 있습니다. 따라서 원자재 가격 추세가 안정화되기 전까지는 단기적인 불확실성이 건설화학 시장 예측 성장률을 억제할 것으로 예측됩니다.

방수 솔루션은 2025년 건설화학 시장 점유율의 35.10%를 차지할 것으로 예상되며, 콘크리트 및 석조 구조물을 습기 침투로부터 보호하는 핵심적인 역할을 할 것으로 보입니다. 이 하위 부문은 지하실 전체 방수 처리, 녹색 지붕용 타포린, 저수 구조물의 음압 측 코팅을 규정하는 강화된 건축 기준의 혜택을 누리고 있습니다. 홍수 다발 지역의 인프라 기관은 2mm 폭의 균열을 메울 수 있는 엘라스토머 시트를 요구하고 있으며, 범용 폴리머 가격 변동에도 불구하고 높은 가격을 유지하고 있습니다. 제조업체는 폴리머 사슬에 나노 클레이 장벽을 내장하여 투과성을 40% 감소시킴으로써 브랜드 차별화를 꾀하고 있습니다.

표면처리 화학제품 분야가 가장 빠르게 성장하고 있으며, 6.65%의 연평균 복합 성장률(CAGR)을 기록하고 있습니다. 이는 배치의 균일성을 높이기 위해 로봇에 의한 양생제 도포를 하는 자동화 프리캐스트 공장 수요 증가가 견인하고 있습니다. 물류창고에서 분진 발생을 억제하는 규산리튬 경화제에 대한 수요도 증가하고 있습니다. 혼화제 포트폴리오는 24시간 내에 25MPa의 강도를 발휘하는 폴리카복실산 에테르계 고성능 감수제를 통해 모듈식 건설에 필수적인 거푸집 재사용 사이클을 실현하는 등 지속적으로 진화하고 있습니다.

건설용 화학제품 보고서는 제품별(접착제, 앵커 및 그라우트, 콘크리트 혼화제, 콘크리트 보호 코팅, 바닥용 수지, 보수 및 재생 화학제품, 실란트 등), 최종 용도별(상업/산업/공공시설, 인프라, 주거용), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류되어 있습니다.

아시아태평양은 2025년 건설용 화학제품 시장의 41.10%를 차지하며 2031년까지 연평균 6.12%의 연평균 복합 성장률(CAGR)로 가장 높은 수준을 유지할 것으로 예측됩니다. 중국에서는 '일대일로' 철도망과 연안 항만 개보수 사업이 수요를 지원하고 있으며, 해양환경에 대응하는 저염화물 혼화제가 지정되어 있습니다. 인도의 스마트 시티 구상은 100개 이상의 지자체에서 옥상 방수재와 포장용 실란트 구매를 촉진하고 있습니다. 한편, 동남아시아에서는 산업단지 건설이 가속화되면서 탄산가스 방지 코팅에 대한 수요가 증가하고 있습니다. 가격에 민감한 건설사들은 현지 배합을 선호하지만, 복잡한 교량 데크는 다국적 공급업체와 협의하여 지역 침투를 강화하는 협력 생산 계약이 체결되고 있습니다.

북미에서는 공공 부문의 현대화를 배경으로 안정적인 매출이 지속될 것입니다. 5,500억 달러 규모의 연방 인프라법에 따라 섬유 강화 보수 모르타르가 필요한 15,000개 차선 마일의 도로 포장재 교체 사업에 자금이 투입될 예정입니다. 국제주택기준 등 건축법에서 지하 방습층이 의무화되어 있으며, 소매용 타포린 판매에 도움을 주고 있습니다. 따라서 미국과 캐나다의 성장은 민간 상업용 건설 착공의 주기적 둔화를 상쇄하고 건설 화학 시장을 견고한 성장 궤도에 올려놓았습니다.

유럽에서는 성숙하면서도 혁신을 추구하는 움직임을 볼 수 있습니다. 유럽 그린딜의 탄소중립 목표는 클링커 저감 시멘트를 요구하고 있으며, 고감수제 및 탄산가스 발생을 억제하는 실란계 실러에 대한 수요를 촉진하고 있습니다. 독일과 이탈리아의 노후화된 교량 스톡은 음극 부식 방지 그라우트 사용을 촉진하고, 스칸디나비아에서는 지하 단열재용 바이오 폴리우레탄 폼의 개발이 진행되고 있습니다.

Construction Chemicals Market size in 2026 is estimated at USD 90.65 billion, growing from 2025 value of USD 85.92 billion with 2031 projections showing USD 118.53 billion, growing at 5.5% CAGR over 2026-2031.

Robust urban infrastructure pipelines, tighter green-building mandates, and steady residential demand together strengthen the construction chemicals market growth outlook. Waterproofing systems anchor product revenues because insurers and code officials prioritize moisture protection, while advanced surface treatments gain traction in automated precast yards. Regional momentum remains centered in Asia-Pacific, where megaproject pipelines accelerate specialty chemical adoption. Across mature economies, asset rehabilitation programs sustain volume when new-build activity plateaus. Competitive dynamics favor suppliers that marry formulation science with on-site technical service, helping contractors meet stricter performance specifications.

Sustained city building programs in Asia-Pacific drive bulk consumption of admixtures, waterproofers, and curing compounds that improve durability in congested job sites. India's USD 1.4 trillion National Infrastructure Pipeline offers a similar catalyst, with large highway and metro packages specifying low-shrinkage concrete admixtures for slab continuity. UN-Habitat forecasts 2.5 billion additional urban residents by 2050, implying a long runway for chemical demand tied to transit, utilities, and high-rise housing. Contractors also lean on fast-setting grouts to keep megaproject schedules on track. Taken together, these factors embed a structural pull for the construction chemicals market that transcends short-cycle fluctuations.

Energy-performance directives now force designers to cap embodied carbon, pushing concrete producers to adopt high-range water reducers and supplementary cementitious materials. The European Union requires all new buildings to achieve net-zero emissions by 2030 under the Energy Performance of Buildings Directive. U.S. LEED v4.1 and BREEAM standards likewise reward low-VOC sealants and bio-based coatings, stimulating premium niches for soy-polyol polyurethane membranes. Product registries such as EPA Safer Choice further influence contractor specifications toward water-borne systems. Suppliers that reformulate ahead of code deadlines capture specification loyalty and reinforce pricing power within the construction chemicals market.

Fluctuating oil and derivative feedstock prices compress supplier margins and complicate contractor budgeting. Brent crude traded between USD 70 and USD 90 per barrel throughout 2024, pulling propylene and epoxy resin prices along the same path. Manufacturers absorb cost spikes or issue surcharges that sometimes delay jobsite adoption of premium products. Heightened geopolitical risks further disrupt supply chains, prompting formulators to diversify into bio-based polyols or recycled polymers. Short-term uncertainty therefore trims the forecast growth slope of the construction chemicals market until feedstock trends stabilize.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Waterproofing solutions captured 35.10% of construction chemicals market share in 2025, illustrating their central role in safeguarding concrete and masonry against moisture intrusion. The sub-segment benefits from stricter building codes that specify full-basement tanking, green-roof membranes, and negative-side coatings on water-retaining structures. Infrastructure agencies in flood-prone regions demand elastomeric sheets that can bridge 2 mm-wide cracks, supporting premium pricing even when commodity polymers fluctuate. Manufacturers integrate nanoclay barriers into polymer chains to cut permeance by 40%, strengthening brand differentiation.

The fastest-growing surface-treatment chemicals segment posts a 6.65% CAGR, fueled by automated precast factories that apply curing compounds by robot to enhance batch consistency. Demand also rises for lithium-silicate hardeners that cut dusting in logistics warehouses. Admixture portfolios continue to evolve with polycarboxylate ether superplasticizers that deliver 25 MPa in 24 hours, enabling form-reuse cycles critical to modular construction.

The Construction Chemicals Report is Segmented by Product (Adhesives, Anchors and Grouts, Concrete Admixtures, Concrete Protective Coatings, Flooring Resins, Repair and Rehabilitation Chemicals, Sealants, and More), End-Use Sector (Commercial, Industrial and Institutional, Infrastructure, and Residential), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Asia-Pacific held 41.10% construction chemicals market share in 2025 and maintains the highest 6.12% CAGR through 2031. China anchors demand with Belt and Road rail lines and coastal port upgrades that specify low-chloride admixtures for marine exposure. India's Smart Cities Mission triggers rooftop waterproofing and paving sealant purchases across 100 municipalities, while Southeast Asia accelerates industrial park builds that require anti-carbonation coatings. Price-sensitive contractors favor locally blended formulations yet consult multinational suppliers for complex bridge decks, enabling cooperative production agreements that deepen regional penetration.

North America contributes steady revenue on the back of public-sector modernization. The USD 550 billion federal infrastructure act channels funds into 15,000 highway-lane-mile resurfacing projects that need fiber-modified patching mortars. Building codes such as the International Residential Code mandate dampproof courses in basements, supporting retail membrane sales. Growth in the United States and Canada therefore offsets cyclic softness in private commercial starts, keeping the construction chemicals market on a positive slope.

Europe shows mature yet innovation-driven behavior. Carbon-neutrality goals in the European Green Deal demand clinker-reduced cements, advancing demand for high-range water reducers and silane sealers that restrict carbonation. Aging bridge stock in Germany and Italy spurs cathodic-protection grout usage, while Scandinavia pioneers bio-based polyurethane foams for below-grade insulation.