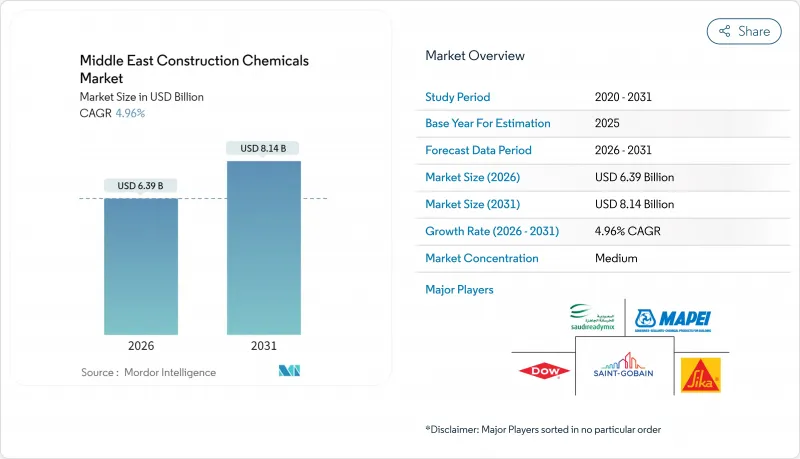

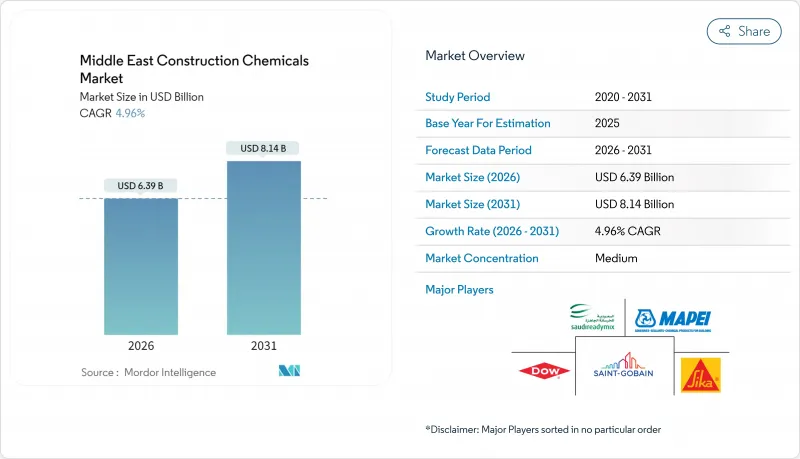

중동의 건설 화학 시장 규모는 2026년 63억 9,000만 달러로 추정됩니다. 2025년 60억 9,000만 달러에서 성장했으며, 2031년에는 81억 4,000만 달러에 이를 것으로 예측됩니다. 2026-2031년에 걸쳐 CAGR 4.96%로 성장할 전망입니다.

이러한 확장은 국가 비전 프로그램과 연계된 국부펀드 지출, 석유 의존도 탈피, 고성능·저배출 제형을 장려하는 기술 규제로 인해 발생합니다. 사우디아라비아의 기가 프로젝트, UAE의 공항 및 데이터센터 급증, 카타르의 LNG 인프라가 함께 콘크리트 혼합제, 방수 시스템, 내식성 코팅에 유리한 수요 기반을 형성합니다. 장기 프레임워크 계약 체결, 다단계 성능 보장, 저휘발성 유기화합물(VOC) 배출량 입증 능력을 갖춘 공급업체들은 가격 프리미엄을 확보할 수 있으며, 세계의 선도 기업들의 통합은 규모의 경제 효과를 증폭시킵니다. 프로젝트 개발사들이 전 주기 공급 안정성, 현지 콘텐츠 확보, 친환경 건축 규정 준수 입증을 요구함에 따라 진입 장벽도 높아지고 있습니다.

비전 전략 하의 전례 없는 공공 부문 자금 지원으로 공항, 철도 회랑, 산업 단지, 신도시 프로젝트에 대한 다년간의 파이프라인이 확정되었습니다. 사우디아라비아만 해도 NEOM 및 레드 시 세계의(Red Sea Global)과 같은 계획에 1조 1,000억 달러 이상을 투입하고 있으며, 이 자본 유입은 역사적 건설 화학 소비 기준선을 사실상 두 배로 늘렸습니다. 개발사들은 단계 중복 위험을 줄이기 위해 최대 5년간의 공급 계약을 체결하며, 실제 콘크리트 타설 전에 벌크 혼합제 수요가 급증합니다. 350억 달러 규모의 알 막툼 국제공항 확장 사업을 포함한 UAE의 병행 추진 계획은 GCC 국가 간 경쟁을 심화시키고 단가를 견고하게 유지합니다. 이러한 복합적 효과로 지역 내 주문량이 증가하고 공장 가동률이 안정화되며, 공급업체의 현지 생산 투자 기반이 공고해집니다.

아부다비의 '에스티다마 펄'과 카타르의 'GSAS' 와 같은 규제는 프로젝트 승인에 저휘발성유기화합물(VOC) 및 저탄소 함유량 기준을 포함시켜, 친환경 규격 제품이 틈새 프리미엄이 아닌 필수 요건이 되도록 합니다. 2024년 UAE 기후법은 기업에 온실가스 배출량 공개를 의무화하여 건설사들이 화학 공급업체에 환경 제품 선언서(EPD) 제출을 요구하도록 합니다. 이에 대응해 다국적 기업들은 경화 시간 및 압축 강도 기준을 유지하면서 용제 함량을 100g/L 미만으로 낮춘 수성 기술을 도입합니다. 선행 도입 기업들은 우선 공급업체 지위를 확보하고 전체 마스터 플랜 커뮤니티에 걸친 사양 고정 혜택을 누립니다.

지역 당국은 미국 환경보호청(EPA)의 에어로졸 코팅 개정안을 기준으로 채택하여, VOC 함량이 100g/L를 초과하는 기존 재료의 제조업체들에게 재제형화 또는 철수를 의무화합니다. 연구개발 역량이 부족한 중소 공급업체들은 매몰비용 상각을 감수하고 마진이 낮은 일반 상품 라인으로 후퇴합니다. 대형 업체들은 수성 분산 및 분말 기반 시스템을 활용해 기계적 성능을 유지하며, 규제 변화를 통해 매장 진열 공간을 확보합니다. 시공업체들은 도포량 조정과 기후 경화 문제에 직면하지만, 규정 미준수 시 발생하는 사양 불이익이 적응 비용을 상회합니다.

2025년 중동의 건설 화학 시장에서 콘크리트 혼합제가 35.07%를 차지했으며, 이는 기가 프로젝트가 기존 혼합물을 뛰어넘는 성능 요구 사항을 제시했기 때문입니다. 50°C 고온에서도 작업성을 유지하면서 80MPa 압축 강도를 충족하는 독점 배합제가 여전히 조달 기준입니다. 1차 공급업체들은 시멘트 공장에 대한 잠재적 탄소세 규제를 대비해 나노 실리카 주입 및 CO2 경화 촉진제 시험을 진행 중입니다.

HDPE 지오멤브레인부터 폴리우레탄 액상 도포형 막에 이르는 방수 시스템은 2031년까지 5.32%의 가장 빠른 연평균 복합 성장률(CAGR)을 기록할 전망입니다. 여기서는 0.1 퍼름-인(perm-in) 미만의 습기 이동 등급과 밀폐된 건물 외피를 촉진하는 친환경 건축 규정이 사양을 주도합니다. 또한 지하수 염분으로 인해 열화가 가속화되는 밀집된 도시 중심부의 지하 구조물 증가로 수요가 발생합니다. 이러한 추세를 활용하는 공급업체들은 현재 30년 설계 수명에 부합하는 보증을 패키지로 제공하여 개발사와의 수명주기 비용 논의에서 우위를 점하고 있습니다.

중동의 건설 화학 보고서는 제품 유형(콘크리트 혼합제, 표면 처리제, 수리 및 재생제, 보호 코팅, 산업용 바닥재, 방수재, 접착제, 실란트 등), 최종 사용자 생산 업별(인프라 및 공공 공간, 상업시설, 산업시설, 주택), 지역별(사우디아라비아, 아랍에미리트(UAE), 카타르, 쿠웨이트, 이집트, 기타 중동 국가)로 분류됩니다.

The Middle East Construction Chemicals Market market size in 2026 is estimated at USD 6.39 billion, growing from 2025 value of USD 6.09 billion with 2031 projections showing USD 8.14 billion, growing at 4.96% CAGR over 2026-2031.

The expansion stems from sovereign wealth fund spending tied to national Vision programs, a pivot away from oil dependence, and technical regulations that reward high-performance, low-emission formulations. Saudi Arabia's giga-projects, the UAE's airport and data-center surge, and Qatar's LNG infrastructure together form a demand backbone that favors concrete admixtures, waterproofing systems, and corrosion-resistant coatings. Suppliers that can align with long-term framework agreements, guarantee multi-phase performance, and document low-VOC footprints capture price premiums, while consolidation among global leaders amplifies scale advantages. Competitive barriers also rise as project developers insist on full-cycle supply security, local content, and proven compliance with green-building mandates.

Unprecedented public-sector funding under Vision strategies has locked in multi-year pipelines for airports, rail corridors, industrial zones, and new-city projects. Saudi Arabia alone channels more than USD 1.1 trillion into schemes such as NEOM and Red Sea Global, a capital flow that effectively doubles historical construction-chemicals consumption baselines. Developers negotiate supply commitments of up to five years to de-risk phase-overlap, causing bulk admixture demand to spike in advance of actual concrete pours. Parallel ambitions in the UAE, including the USD 35 billion Al Maktoum International Airport expansion, sharpen inter-GCC competition and keep unit prices firm. The combined effect lengthens regional order books, stabilizes plant-utilization rates, and anchors supplier investment in local production.

Regulations such as Abu Dhabi's Estidama Pearl and Qatar's GSAS embed low-VOC, low-embodied-carbon thresholds into project approvals, making eco-compliant formulations a ticket-to-play rather than a niche premium. The UAE climate law of 2024 forces enterprises to disclose greenhouse-gas metrics, compelling contractors to request environmental product declarations from chemical vendors. In response, multinationals deploy water-borne technologies that maintain set-time and compressive-strength thresholds while cutting solvent levels below 100 g/L. Early adopters secure preferred-supplier status and enjoy specification lock-ins that span entire master-planned communities.

Regional authorities adopt U.S. EPA aerosol-coating amendments as reference, obliging manufacturers to reformulate or withdraw legacy materials above 100 g/L VOC. Smaller suppliers lacking research and development depth face sunk-cost write-offs and retreat to commodity lines with lower margins. Large players leverage aqueous dispersion and powder-based systems to retain mechanical performance, using the regulatory shift to gain shelf space. Contractors grapple with application-rate adjustments and climate-cure challenges, but specification penalties for non-compliance outweigh adaptation costs.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Concrete admixtures commanded 35.07% of the Middle East construction chemicals market share in 2025 as giga-projects elevated performance requirements beyond conventional mixes. Proprietary blends that lengthen workability in 50 °C heat while meeting 80 MPa compressive strengths remain the procurement benchmark. Tier-one vendors trial nano-silica infusions and CO2-curing accelerators, hedging against potential carbon-levy regulations on cement plants.

Waterproofing systems, ranging from HDPE geomembranes to polyurethane liquid-applied membranes, chart the fastest 5.32% CAGR through 2031. Here, green-building mandates that promote tight building envelopes and moisture-migration ratings under 0.1 perm-in. drive specification. Demand also flows from rising below-grade structures in dense urban cores, where groundwater salinity accelerates deterioration. Suppliers capitalizing on this trajectory now bundle warranties that match 30-year design lives, giving them leverage in lifecycle-cost discussions with developers.

The Middle East Construction Chemicals Report is Segmented by Product Type (Concrete Admixtures, Surface Treatments, Repair and Rehabilitation, Protective Coatings, Industrial Flooring, Waterproofing, Adhesives, Sealants, and More), End-User Industry (Infrastructure and Public Spaces, Commercial, Industrial, and Residential), and Geography (Saudi Arabia, United Arab Emirates, Qatar, Kuwait, Egypt, and Rest of Middle East).