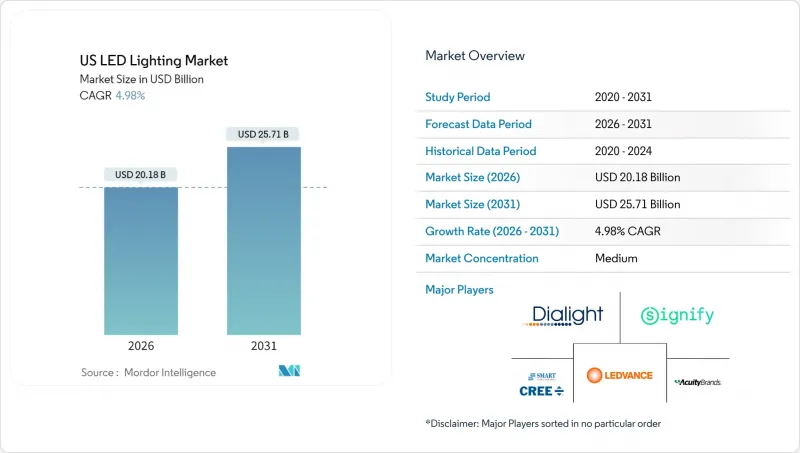

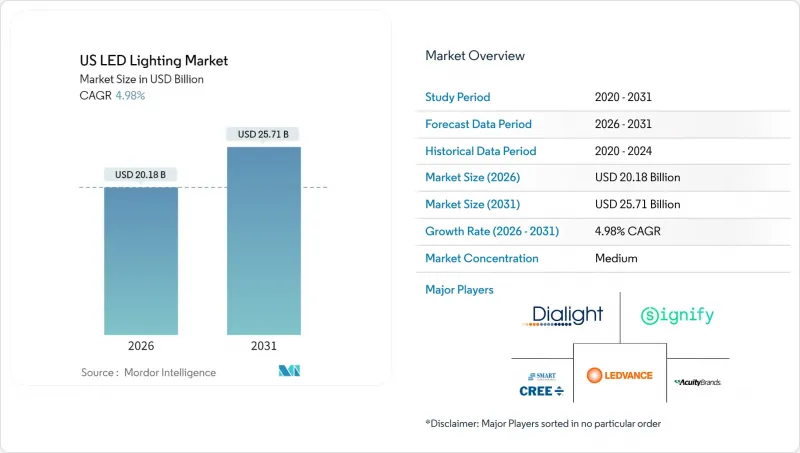

2026년 미국의 LED 조명 시장 규모는 201억 8,000만 달러로 추정되며, 2025년 192억 2,000만 달러에서 성장하며, 2031년에는 257억 1,000만 달러에 달할 것으로 예측됩니다. 2026-2031년에 CAGR 4.98%로 확대할 전망입니다.

2023년 백열등과 할로겐 램프를 폐지하는 연방 규제와 캘리포니아, 버몬트, 워싱턴 주에서 대부분의 형광등을 금지하는 조치가 이어지면서 대체 수요를 창출하고 판매량을 계속 늘리고 있습니다. 현재 지자체 건축 기준에서는 단순한 효율 향상보다 제어 가능한 조명기구에 더 많은 점수를 부여하고 있으며, 건축가들이 센서와 네트워크 지원 드라이버가 장착된 조명기구를 지정하도록 권장하고 있습니다. 포춘지 선정 500대 기업은 투자 회수 계산이 불리한 경우에도 탄소 배출 목표 달성을 위해 기존 조명의 교체를 가속화하고 있으며, 조달 우선순위를 입증된 배출 감소 효과로 전환하고 있습니다. 동시에 캐나다-멕시코 수입품에 대한 25%의 관세와 중국산 하위 부품에 대한 10%의 추가 과징금 부과로 인해 제조업체들은 공급업체 다변화와 하위 조립품의 국내 회귀를 통해 경쟁 구도를 재편하고 있습니다.

와트당 45루멘 미만의 램프를 금지하는 연방 규정으로 인해 소비자와 기업은 와트당 80-100루멘의 LED로 전환하고 있습니다. 2024년 시행되는 캘리포니아주의 형광등 튜브 금지령은 사무실과 소매점의 조기 교체를 촉진하여 미국 LED 조명 시장에서 리노베이션 수요의 우위를 강화했습니다. 이 규정은 장비의 연식에 관계없이 준수해야 하므로 업그레이드 시기를 감가상각 일정과 분리하여 규정합니다. 관세로 인해 수입 램프의 가격이 상승함에 따라 공급선이 짧은 국내 제조업체는 가격 우위를 점하게 되었습니다.

인플레이션 억제법에 따라 주택 에너지 보조금에 88억 달러가 배정되어 있으며, 대상 LED 제품에 대해는 가구당 최대 200달러가 지급됩니다. 상업시설 소유주는 설치 시스템이 기준에서 요구하는 효율을 초과하는 경우, 섹션 179D에 따라 평방피트당 최대 5달러를 공제할 수 있습니다. 이 규정은 네트워크 지원 조명기구에 유리합니다. 캘리포니아주 'Title 24 2025'는 일광 수확(자연광 이용)과 첨단 제어를 의무화하고, 센서와 무선 드라이버가 내장된 조명기구의 도입을 가속화할 것입니다.

2025년 3월에 도입된 관세로 인해 캐나다와 멕시코 수입품에 대한 관세가 25%로 인상되어 국경을 넘어선 마킬라도라 경제의 기반이 훼손되었습니다. 동시에 중국산 LED 드라이버에 대한 추가 관세가 20%로 증가함에 따라 미국 조립업체의 부품 비용이 10-15% 상승했습니다. 각 업체들은 현재 베트남과 인도공급업체 인증을 서두르고 있지만, 보통 18개월이 소요되는 이전 일정으로 인해 가격 변동과 재고 부족의 영향을 받기 쉬운 상황입니다.

2025년 미국 LED 조명 시장에서 조명기구 카테고리가 62.95%의 압도적인 점유율을 차지했습니다. 이는 건축가와 기술자가 점유 감지 및 자연 채광 규제에 대응하는 센서가 내장된 설비를 지정했기 때문입니다. 통합 시스템이 시운전 및 보증을 간소화하므로 성장은 꾸준히 지속되고 있습니다. 반면, 백열전구와 형광등 금지에 따른 즉각적인 수요를 충족시키는 램프는 6.72%로 더 높은 CAGR을 보이고 있습니다. 미국 LED 조명 시장은 리노베이션 수요가 중심이기 때문에 평균 판매가격은 하락세를 보이고 있지만, 램프 판매량은 견고하게 유지되고 있습니다.

칩 온보드 어레이와 무선 제어 모듈의 혁신으로 건물 소유주가 상세한 에너지 데이터를 요구함에 따라 조명기구는 부가가치를 창출할 수 있는 위치에 있습니다. 램프 벤더는 학교와 의료시설을 타겟으로 범용 조광 호환성과 내충격 코팅으로 시장 점유율을 지키고 있습니다. 두 하위 부문을 통해 미국 LED 조명 시장 규모는 효율 개선의 여지가 점차 줄어들고, 재배용 조명 및 인간 중심 조명과 같은 특수 분야에서의 채택이 확대됨에 따라 확대될 것으로 예측됩니다.

2025년 기준 도매 및 소매가 매출의 54.85%를 차지할 것으로 예상되며, 계약업체들이 직송 모델을 채택하면서 E-Commerce는 CAGR 5.21%로 확대될 것으로 보입니다. 이러한 변화는 표준화된 SKU가 소량 배송망에 적합한 주거용 DIY 시장과 소규모 상업시설에서 두드러집니다. 광도계 설계나 보조금 신청 서류가 필요한 대규모 프로젝트에서는 여전히 직접 판매가 중요하지만, 유지보수용 재고의 정기 주문은 웹 포털을 통한 주문이 증가하는 추세입니다. 강력한 온라인 구성 툴와 실시간 재고 데이터를 갖춘 제조업체가 미국 LED 조명 시장에서 더 큰 점유율을 차지하고 있습니다.

이에 반해 기존 유통업체는 설계 지원, 보조금 신청 대행, 현지 런칭 서비스 등을 패키지화하여 대응하고 있습니다. 자산대장 관리, 예지보전 등을 다루는 소프트웨어 업체를 인수해 물리적 가치와 디지털 가치를 융합한 하이브리드형 제안을 구축하려는 움직임도 보입니다. 관세 비용이 변동하는 가운데, 온라인 플랫폼은 투명한 가격 제시를 통해 복잡한 시공에서 여전히 현지 서비스를 중시하는 시장에서 구매 행동에 영향을 미치고 있습니다.

The United States LED lighting market size in 2026 is estimated at USD 20.18 billion, growing from 2025 value of USD 19.22 billion with 2031 projections showing USD 25.71 billion, growing at 4.98% CAGR over 2026-2031.

Federal rules that eliminated incandescent and halogen lamps in 2023, followed by bans on most fluorescent tubes in California, Vermont, and Washington, created replacement demand that continues to lift unit volumes. Municipal building codes now give more credit for controllable fixtures than for bare efficacy gains, pushing architects to specify luminaires that include sensors and networked drivers. Fortune 500 companies are increasingly replacing legacy lighting to meet their carbon targets, even when payback calculations are unfavorable, redirecting procurement priorities toward verified emission reductions. At the same time, tariffs of 25% on Canadian and Mexican imports, along with an additional 10% surcharge on Chinese sub-components, are nudging manufacturers to diversify their suppliers or reshore sub-assembly, reshaping the competitive landscape.

Federal rules that prohibit lamps delivering fewer than 45 lumens per watt have prompted consumers and businesses to shift toward LEDs that deliver 80-100 lumens per watt. California's fluorescent tube ban, effective in 2024, triggered early replacements in offices and retail spaces, reinforcing the dominance of retrofitting in the United States' LED lighting market. Because compliance is mandatory regardless of fixture age, the rule decouples upgrade timing from depreciation schedules. Domestic producers with shorter supply lines gained price leverage as tariffs inflated the costs of imported lamps.

The Inflation Reduction Act allocates USD 8.8 billion for Home Energy Rebates, which include up to USD 200 per household for qualified LED products. Commercial property owners can deduct up to USD 5.00 per square foot under Section 179D when installed systems surpass code-mandated efficiency, a provision that favors networked luminaires. Title 24 2025 in California will require daylight harvesting and advanced controls, accelerating the uptake of fixtures that ship with embedded sensors and wireless drivers.

Tariffs introduced in March 2025 raised duties on Canadian and Mexican imports to 25%, undermining cross-border maquiladora economics. Simultaneously, the surcharge on Chinese LED drivers increased to 20%, raising component costs by 10-15% for U.S. assemblers. Firms now rush to qualify suppliers in Vietnam and India, but the typical 18-month relocation timeline leaves them vulnerable to price fluctuations and inventory shortages.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The luminaires category accounted for a dominant 62.95% share of the United States' LED lighting market in 2025, as architects and engineers specified fixtures with onboard sensors that meet occupancy and daylighting mandates. Growth continues steadily because integrated systems simplify commissioning and warranty. By contrast, lamps post a faster 6.72% CAGR, as they satisfy the immediate needs arising from the bans on incandescent and fluorescent bulbs. The retrofit-heavy nature of the United States LED lighting market keeps lamp volumes buoyant even though average selling prices trend downward.

Innovation in chip-on-board arrays and wireless control modules positions luminaires to capture incremental value as building owners seek granular energy data. Lamp vendors defend their market share through universal dimming compatibility and shatter-resistant coatings, targeting schools and healthcare facilities. Across both sub-segments, the United States LED lighting market size will expand as efficacy gains become increasingly thin, but adoption widens in specialty niches such as grow lights and human-centric lighting.

Wholesale retail retained 54.85% of sales in 2025, yet e-commerce is advancing at a 5.21% CAGR as contractors embrace direct-ship models. The shift is most evident in the residential DIY and small commercial space, where standardized SKUs fit parcel networks. Direct sales remain critical for large projects that require photometric design and rebate paperwork, but web portals are increasingly handling repeat orders for maintenance stock. Manufacturers with robust online configurators and live inventory data are capturing a larger share of the United States' LED lighting market.

Traditional distributors respond by bundling design-assist, rebate administration, and on-site startup services. Some have acquired software firms that manage asset registers and predictive maintenance, creating hybrid physical-digital value propositions. As tariff costs fluctuate, online platforms provide transparent pricing, influencing buyer behavior in a market that still values local service for complex builds.

The United States LED Lighting Market Report is Segmented by Product Type (Lamps, and Luminaires/Fixtures), Distribution Channel (Direct Sales, Wholesale/Retail, and E-Commerce), Installation Type (New Installation, and Retrofit Installation), Application (Commercial Offices, Retail Stores, and More), and End User (Indoor, Outdoor, and Automotive). The Market Forecasts are Provided in Terms of Value (USD).