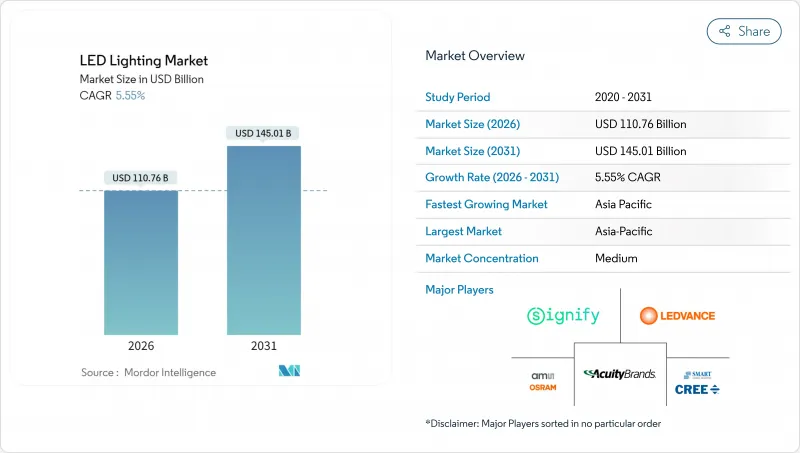

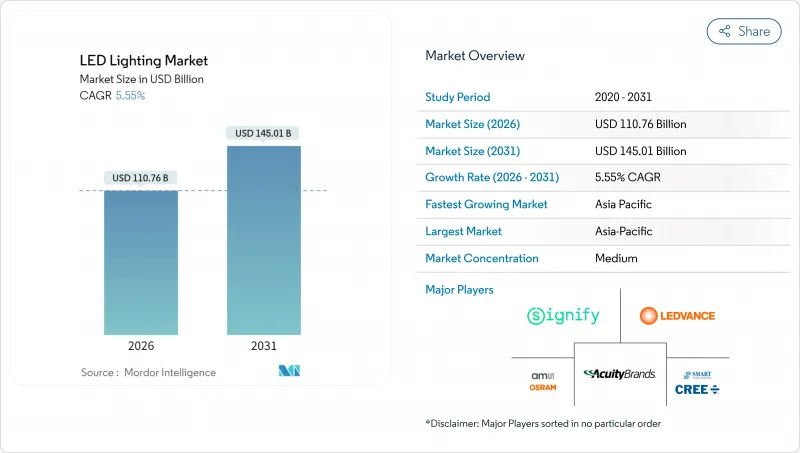

LED 조명 시장은 2025년의 1,049억 3,000만 달러에서 2026년에는 1,107억 6,000만 달러로 성장하고 2026년부터 2031년에 걸쳐 CAGR 5.55%를 나타낼 것으로 예상됩니다. 2031년까지 1,450억 1,000만 달러에 이를 것으로 전망됩니다.

이 추이는 업계가 급속한 초기 도입 단계에서 품질 차별화와 통합 제어가 경쟁 우위를 좌우하는 안정적인 대체 주도 단계로 이행하고 있음을 보여줍니다. 비효율적인 조명기구에 대한 정부의 단계적 폐지, 2014년부터 2016년에 설치된 설비의 2차적인 대체 수요, 스마트시티계획의 가속이 주요 수요의 견인역이 되고 있습니다. LED 하드웨어에 센서, 네트워크 인터페이스, 부가가치 서비스를 통합하는 제조업체는 대규모 계약과 장기적인 고객 관계 확보에 유리합니다. 한편 삼성의 철수계획에 상징되는 공급측의 통합이 진행되고 있는 가운데, 잔존 공급업체 간의 경쟁은 격화되고 있어 판매 채널 확보와 이익률 유지를 위한 경쟁이 가속화되고 있습니다.

정책 개입은 여전히 LED 조명 시장에서 가장 강한 추진력입니다. 호주 '온실가스·에너지 최저기준규제'(2026년 3월 시행)는 최저효율기준을 끌어올려 백열등의 금지를 2030년까지 연장함으로써 제조업체에 명확한 컴플라이언스 스케줄을 제공하여 체류재고 리스크를 경감합니다. 연방 기준이 주·지자체 조달을 이끄는 미국에서도 유사한 움직임을 볼 수 있어 예측 가능한 대량 구매 파이프라인이 형성되고 있습니다. 필라델피아시가 실시한 13만 1천기의 조명기구 갱신(에너지 소비량 50% 삭감, 연간 240만 달러의 절약 효과)와 같은 도시 규모의 전환 사례는 다른 지자체에 대해서도 경제적 합리성을 증명하고 있습니다. 이러한 정책에 따라 적합성이 높고 고품질의 램프나 조명기구만이 시장에서 살아남아 평균 판매 가격이 상승. 강력한 인증 포트폴리오를 가진 브랜드가 혜택을 받는 구조로 되어 있습니다.

스마트 시티에 대한 투자는 조명을 도시 관리를 위한 데이터 기반으로 전환하여 각 조명기구의 전략적 가치를 높입니다. 밀턴 킨스에서는 2만기의 센서 탑재 LED 가로등을 도입하여 에너지 사용량을 40% 삭감함과 동시에 교통량과 공기질 모니터링 기능을 추가했습니다. 파라마타는 65%의 에너지 절약을 달성하여 조명 노드를 도시 전체의 IoT 네트워크에 통합. 조명 기능을 넘어 수익 창출 서비스를 지원합니다. 이러한 사례는 LED 조명 시장이 상품 제품 판매에서 장기 서비스 계약 및 데이터 플랫폼 수익원을 포함한 다 분야의 인프라 프로젝트로 전환하고 있음을 보여줍니다.

엔트리 모델과 프리미엄 연결형 조명기구의 가격 차이는 여전히 커서 비용 중심 지역에서의 도입을 막고 있습니다. 부품 비용은 해마다 저하되고 있는 것, 가변 스펙트럼, 통합 센서, 견고한 열 관리 등의 첨단 기능은 부품 원가의 압박 요인이 됩니다. 그 결과 LED 조명 시장은 양극화되고 있으며, 기본 모델은 순수한 가격 경쟁에, 프리미엄 제품은 라이프 사이클 비용 절감을 촉구하고 일부 구매자는 여전히 그 가치를 과소 평가했습니다. 신흥 시장, 중소기업, 제한된 자본을 가진 지자체 예산은 가장 엄격한 제약에 직면하고 있으며, 이익률이 높은 스마트 제품과 인간 중심 설계 제품의 보급이 늦어지고 있습니다.

2025년 매출의 61.45%를 조명기구가 차지해 광학계·방열기·제어 기능을 통합한 일체형 설계가 구매자로부터 지지된 것으로 나타났습니다. 이 우위성으로 특정 건축·산업 사양에 맞는 제품 개발이 가능한 풀픽스 차벤더의 LED 조명 시장 점유율이 확대되고 있습니다. 조명기구 카테고리는 평균 판매 가격이 높고 교체 사이클도 길기 때문에 제조업체의 현금 흐름을 안정시킵니다. 한편, 램프 부문은 주택용 및 경상용 소켓에 있어서 2차 교환 수요의 파도에 견인되어, 8.29%의 연평균 복합 성장률(CAGR)로 확대가 전망됩니다. Cree LED의 XLamp XFL은 소형 인클로저에서 최대 2만 루멘을 구현하고 휴대용 조명을 위한 특정 성능 향상을 제공하는 램프 기술 혁신의 좋은 예입니다.

2차적인 교환 동향의 높아짐에 따라, 배선 공사나 천장 공사를 필요로 하지 않고, 신속한 성능 향상을 요구하는 소유자층에 있어서 램프의 중요성이 증가하고 있습니다. 그러나 LED 조명 시장에서는 네트워크 제어 기능을 통합하고 전력 회사의 보조금 신청 절차를 지원하는 조명기구 제조업체가 고객의 봉쇄를 강화하고 계속 우위를 유지하고 있습니다. 기업이 리노베이션 램프와 새로운 연결 기구를 함께 제공하는 하이브리드 전략은 예산 중시층과 기능 중시층 모두에 대응하는데 효과적입니다.

도매·소매 채널은 2025년에 53.55%의 점유율을 차지했습니다. 이는 계약자 및 시설 관리자가 제품의 즉각적인 입수성, 기술 지도, 애프터 지원을 중시하고 있기 때문입니다. 이 채널은 프로젝트의 스케줄 확보와 지역 규제, 사양에의 준거를 보증하는 것으로, LED 조명 시장의 기반을 지지하고 있습니다. 그러나 주택 소비자와 중소기업에 의한 직접 배송 채용이 증가하고 있기 때문에 전자상거래는 2031년까지 6.62%의 연평균 복합 성장률(CAGR)로 가장 빠른 성장이 전망되고 있습니다. Havells 등의 제조업체는 사우스 캐롤라이나주 앤더슨에 재고를 완비한 창고를 개설하는 동시에 독립된 조명 대행사와의 관계를 유지함으로써 듀얼 채널 모델을 활용하고 있습니다.

디지털 구매 과정에서는 카탈로그 표준화와 제품 선택 프로세스를 명확하게 설명하는 리치 미디어 컨텐츠를 활용합니다. 그러나 복잡한 상업시설 개조 공사에서는 측광 레이아웃, 리베이트 조정 및 현장 문제 해결을 제공하는 도매업체가 여전히 유리합니다. 결과적으로 온라인 컨피규레이터와 현지 수령 또는 신속한 배송을 결합한 옴니채널 전략은 가장 광범위한 고객층을 지원합니다.

아시아태평양은 중국의 대규모 제조 및 인도 인프라 개발에 견인되어 2025년에는 LED 조명 시장에서 42.10%의 수익 점유율을 차지하고 시장을 선도했습니다. 인도의 UJALA 전구 배포와 광범위한 스마트 시티 프로그램 등 정부 계획이 지속적인 수요를 추진하는 한편, 국내 제조업체는 비용 우위성을 활용해 해외 프로젝트에 공급하고 있습니다. 이 지역은 2031년까지 연평균 복합 성장률(CAGR) 7.58%로 가장 높은 성장률을 보일 것으로 예측되고 있으며, 가속화하는 도시화, 경기 자극책에 의한 건설 수요, 접속형 조명 에코시스템에 대한 선호의 고조가 이를 지원하고 있습니다. 한국과 일본의 부품 제조업체가 고효율 칩을 공급함으로써, 지역 조명기구 브랜드는 성능과 가격의 양면에서 세계 경쟁력을 획득하고 있습니다.

북미는 엄격한 에너지 절약 기준, ESCO 계약 및 LED 전환을 선호하는 연방 인프라 지출로 견조한 지위를 유지하고 있습니다. 주 수준의 우대조치와 지자체의 지속가능성 목표가 함께 가로등과 공공시설에서의 높은 보급률을 견인하고 있습니다. 상업용 신축 프로젝트에서는 거주자 웰니스 기준을 충족시키기 위해 네트워크 대응 조명기구가 도입되어, 창고 및 물류 시설에서는 운용 코스트 삭감을 위해 하이베이 LED로의 이행이 진행되고 있습니다. 그러나 공급망의 혼란으로 인해 프로젝트 지연이 발생하는 경우도 있으며, 많은 구매자가 드라이버와 칩 패키지의 이중 조달을 진행하고 있습니다.

유럽에서는 '건축물의 에너지 성능 지령'과 '개수파'가 회원국 전체에서 대규모 개수를 의무화하고 혜택을 가져오고 있습니다. 공공 요금과 탄소세가 LED 갱신의 경제적 합리성을 강화하고 공공 조달의 현지 조달 규칙이 유럽 브랜드를 우월합니다. 스칸디나비아의 도시에서는 인간 중심 조명의 파일럿 사업이 선행해, 조광 가능한 백색 조명기구의 보급을 추진중입니다. 한편, 중동 및 아프리카에서는 발전에 편차가 보입니다. 석유 자원이 풍부한 걸프 국가들은 스마트 시티의 모델 사업에 투자하는 반면, 많은 아프리카 국가들은 기본적인 전기 사업에 주력하고 기증자 자금에 의한 LED 도입에 의존하고 있습니다. 라틴아메리카에서는 에너지 보조금의 감소와 공공 조명 사업의 컨세션 방식이 성과 연동형 계약의 도입을 촉진하고 점진적인 진전을 볼 수 있습니다.

The LED lighting market is expected to grow from USD 104.93 billion in 2025 to USD 110.76 billion in 2026 and is forecast to reach USD 145.01 billion by 2031 at 5.55% CAGR over 2026-2031.

This trajectory illustrates the sector's transition from rapid early adoption to a stable, replacement-driven phase, where quality differentiation and integrated controls drive competitive success. Government phase-outs of inefficient lamps, a secondary replacement wave for installations completed between 2014 and 2016, and the acceleration of smart-city programs form the primary demand engines. Manufacturers that integrate LED hardware with sensors, network interfaces, and value-added services tend to secure larger contracts and longer customer relationships. Meanwhile, supply-side consolidation, illustrated by Samsung's planned exit, intensifies rivalry among remaining suppliers as they race to secure channel loyalty and defend margins.

Policy intervention remains the strongest accelerator for the LED lighting market. Australia's Greenhouse and Energy Minimum Standards regulation, effective March 2026, raises minimum efficacy thresholds and extends the incandescent ban through 2030, providing manufacturers with clear compliance schedules and mitigating the risk of stranded inventory. Similar dynamics in the United States, where federal standards guide state and municipal procurement, create predictable bulk-purchase pipelines. Citywide conversions such as Philadelphia's 131,000-fixture program, which delivered 50% energy savings and USD 2.4 million annual savings, prove the financial logic to other municipalities. These policies narrow the viable product spectrum to compliant, higher-quality lamps and luminaires, raising the average selling price and rewarding brands with strong certification portfolios.

Smart-city investments convert lighting into a data backbone for urban management, raising the strategic value of each luminaire. Milton Keynes' deployment of 20,000 sensor-enabled LED streetlights cut energy use by 40% while adding traffic and air-quality monitoring functions.Parramatta achieved 65% energy savings and integrated lighting nodes into city-wide IoT networks that support revenue-generating services beyond illumination. These examples illustrate how the LED lighting market is shifting from commodity product sales to multidisciplinary infrastructure projects that command long-term service contracts and data platform revenue streams.

Price differentials between entry-level lamps and premium connected luminaires remain sizeable, deterring adoption in cost-sensitive regions. Although component costs decline annually, advanced features such as tunable spectra, integrated sensors, and robust thermal management add to the bill-of-materials pressure. The result is a bifurcated LED lighting market where basic models compete purely on price, while premium offerings rely on lifecycle savings narratives that some buyers still discount. Emerging markets, small businesses, and municipal budgets with limited capital face the sharpest constraints, resulting in slower penetration of high-margin smart and human-centric products.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Luminaires captured 61.45% of 2025 revenue, demonstrating how buyers prefer integrated form factors that combine optics, heat sinks, and controls. This dominance has increased the market share of full-fixture vendors in the LED lighting market, which can tailor products to meet specific architectural and industrial specifications. The luminaire category commands higher average selling prices and longer replacement intervals, stabilizing cash flows for manufacturers. Meanwhile, the lamp segment is expected to expand at an 8.29% CAGR, driven by the secondary replacement wave in residential and light-commercial sockets. Cree LED's XLamp XFL, delivering up to 20,000 lumens in compact footprints, exemplifies lamp innovation that supplies specific performance gains for portable lighting.

The secondary replacement trend elevates lamps as owners seek quick performance upgrades without the need for rewiring or ceiling work. Nonetheless, the LED lighting market continues to reward luminaire makers that integrate networked controls and support utility rebate paperwork, deepening customer lock-in. Hybrid strategies, in which firms offer retrofit lamps alongside new connected fixtures, help address both budget-driven and feature-seeking buyers.

Wholesale and retail outlets held a 53.55% share in 2025 because contractors and facility managers rely on immediate product availability, technical guidance, and after-sales support. This channel anchors the LED lighting market by safeguarding project timelines and ensuring compliance with local codes and specifications. E-commerce, however, is on track for the fastest 6.62% CAGR through 2031, as residential consumers and small businesses increasingly adopt direct-to-door fulfillment. Manufacturers such as Havells tapped a dual-channel model by opening a fully stocked warehouse in Anderson, South Carolina, while maintaining relationships with independent lighting agents.

Digital purchase journeys capitalize on catalog standardization and rich media content that demystify the product selection process. Yet complex commercial retrofits still favor wholesalers who provide photometric layouts, rebate coordination, and on-site troubleshooting. Consequently, omni-channel strategies that blend online configurators with local pickup or rapid delivery serve the broadest customer base.

The LED Lighting Market Report is Segmented by Product Type (Lamps, and Luminaires/Fixtures), Distribution Channel (Direct Sales, Wholesale/Retail, and More), Installation Type (New Installation, and Retrofit Installation), Application (Commercial Offices, Retail Stores, and More), End User (Indoor, Outdoor, and More), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

The Asia-Pacific region led the LED lighting market, accounting for a 42.10% revenue share in 2025, driven by China's large-scale manufacturing and India's infrastructure development. Government schemes such as India's UJALA bulb distribution and widespread smart-city programs propel continuous demand, while domestic producers leverage cost advantages to supply foreign projects. The region is also expected to exhibit the fastest growth, with a 7.58% CAGR to 2031, underpinned by accelerating urbanization, stimulus-backed construction, and a growing preference for connected lighting ecosystems. Korean and Japanese component firms contribute high-efficacy chips, allowing regional fixture brands to compete globally on both performance and price.

North America maintains a robust position through stringent energy codes, ESCO contracting, and federal infrastructure spending that prioritizes LED conversions. State-level incentives combined with municipal sustainability targets drive high penetration in streetlights and public facilities. Commercial new-build projects integrate networked luminaires to meet occupant-wellness standards, while warehousing and logistics facilities migrate to high-bay LEDs for operational savings. Supply-chain disruptions, however, cause occasional project delays, prompting many buyers to dual-source drivers and chip packages.

Europe benefits from the Energy Performance of Buildings Directive and the Renovation Wave that compel deep retrofits across member states. Utility tariffs and carbon taxes strengthen the economic case for LED upgrades, and local content rules favor European brands for public tenders. Scandinavian cities are spearheading human-centric lighting pilots, advancing the adoption of tunable white fixtures. Conversely, the Middle East and Africa exhibit heterogeneous development; oil-rich Gulf states invest in smart-city showcase projects, while many African nations focus on basic electrification and rely on donor-funded LED rollouts. Latin America is experiencing gradual progress as energy subsidies decline and public lighting concessions encourage the adoption of performance-based contracting.