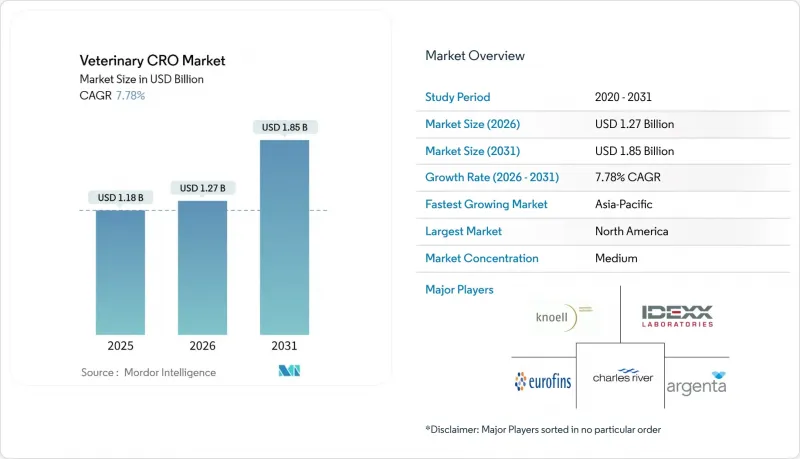

2026년 수의 계약 연구기관(CRO) 시장 규모는 12억 7,000만 달러로 추정되며, 2025년 11억 8,000만 달러에서 성장하여 2031년에는 18억 5,000만 달러에 달할 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 7.78%에 달할 것으로 예상됩니다.

동물용 의약품 기업이 직면한 규제 강화, 연구개발비 증가, 신약의 시장 출시 기간 단축의 필요성으로 인해 수요가 증가하고 있습니다. 2024-2025년 H5N1 조류독감 사태와 같은 인수공통전염병 비상사태는 신속한 백신 개발 서비스의 필요성을 더욱 높이고 있으며, 미국 및 유럽의 규제 신속화 제도는 신청 서류를 가속화된 경로로 안내할 수 있는 CRO를 평가하고 있습니다. 특히 AI를 활용한 진단기술과 정밀 축산 데이터 도입으로 외부 위탁조사 범위가 확대되고 있습니다. 또한, 벤처 투자자들의 반려동물 바이오테크 스타트업에 대한 자금 유입으로 수의 CRO(Contract Research Organization) 시장의 고객 기반이 확대되고 있습니다.

미국 반려동물 소유자의 수의학 지출은 2024년 400억 달러에 달했으며, 이는 외부 연구 역량이 필요한 혁신적 치료법에 대한 강력한 수요를 견인하고 있습니다. 반려동물의 인간화가 진행됨에 따라, 스폰서 기업들은 인체용 의약품 프로토콜을 모방한 종양학, 신경학, 장수 시험을 추진하고 있으며, 이로 인해 연구의 복잡성이 증가하고 있습니다. 대규모 진료 네트워크를 통한 다군 비교 및 위약 대조 임상시험을 수행할 수 있는 CRO가 우위를 점하고 있습니다. 반려견의 수명을 늘리기 위한 Loyal의 LOY-002 프로그램은 현재 1,000마리의 반려견을 대상으로 한 중요한 시험 단계에 있으며, 2,200만 달러의 새로운 자금 조달을 달성했습니다. 이는 수의 CRO 시장이 어떻게 반려동물 중심의 연구개발 프로그램을 가능하게 하는지를 보여주는 좋은 예입니다. 중국에서는 1억 가구 이상이 반려동물을 키우고 있으며, 아시아태평양의 현지 CRO 역량에 대한 수요 기반이 확대되고 있습니다. 진료소의 비용 압박은 간접비를 최소화하는 외부 관리형 연구 프로토콜의 채택을 촉진하고, 아웃소싱 모델을 더욱 강화시키고 있습니다.

FDA의 '동물 및 수의학 혁신 계획'은 2024년 4개의 혁신 센터를 설립하고, 신속 승인 과학을 촉진하기 위해 300만 달러를 배정하여 미충족 수요에 대한 단기 승인 경로를 개설했습니다. 마이너유즈마이너스페이스(MUMS) 법의 확대 규정에 따라 기존 치료제가 제한되어 있는 주요 적응증에 대한 조건부 허가 경로가 허용되었습니다. 2025년 2월에 이 경로로 승인된 트리븀베츠의 고양이 비대성 심근증 치료제 후보물질이 좋은 예입니다. VICH(국제수의약품 규제조화회의)의 병행 조화로 EU, 미국, 일본의 CMC(화학-제조-품질 관리) 서류가 통일되어 다지역 신청이 간소화되었습니다. 그러나 관할권 간의 미묘한 차이를 잘 알고 있는 컨설턴트에 대한 수요가 증가하고 있습니다. FDA의 사용자 수수료 인상(2025년 신청당 58만 1,735달러)으로 인해 중소 스폰서 기업들은 외부 규제 파트너에 대한 의존도가 높아지고 있습니다. 이러한 조치들이 결합되어 파이프라인의 처리 속도가 빨라지고, 수의 CRO(임상시험수탁기관) 시장의 잠재적 고객 기반이 확대되고 있습니다.

단일 수의학 생물학적 제제의 총 연구개발비는 10억 달러가 넘는 경우도 있어 중소 혁신기업을 압박하고 실행 가능한 스폰서 수를 제한하고 있습니다. FDA 신청 비용의 상승은 또 다른 부담으로 작용하고, 인체용 의약품과 달리 동물용 의약품의 판매량은 비용 상각에 필요한 규모에 도달하는 경우가 드뭅니다. 신속 승인 루트가 존재하지만, 이는 시판 후 연구 의무를 부과하기 때문에 여전히 CRO의 참여와 자본이 필요합니다. 신흥국 규제 당국은 통일된 가이드라인이 없는 경우가 많으며, 국가별 시험이 추가되어 승인 절차가 길어지는 경우가 많습니다. 이러한 장벽은 절대적인 성장을 억제하는 한편, 아웃소싱을 촉진하는 요인으로 작용하여 수의 CRO 시장의 장기적인 성장 궤도를 유지하고 있습니다.

2025년 임상시험은 규제 당국이 요구하는 통제된 다기관 유효성 시험의 필요성을 반영하여 수의 CRO 시장 점유율의 33.12%를 차지했습니다. 복잡한 생물학적 제제가 개발 파이프라인을 통과함에 따라, 이 하위 부문은 안정적이고 높은 한 자릿수 성장을 유지할 것으로 예상됩니다. 한편, 규제 대응 및 컨설팅 업무는 스폰서들이 FDA의 혁신 아젠다 파일럿, VICH 조화, 농림수산식품부 가이드라인 대응을 위해 외부 전문가에게 의뢰하는 추세로 인해 8.52%의 CAGR로 가장 빠른 성장이 예상됩니다. 안전성 데이터 패키지가 모든 승인의 기반이 되는 독성학 서비스는 필수적이며, 바이오 분석 분석 개발 등 소규모 틈새 분야는 정밀농업 기술을 활용한 시료 추적 기술의 발전으로 혜택을 받고 있습니다.

연구의 복잡성에 따라 CRO는 서비스 일괄 제공을 추진하고 있습니다. 트리븀벳이 실시한 300마리의 고양이를 대상으로 한 다국적 HCM 연구는 임상 업무, 영상 핵심 실험실, 중앙 병리 서비스를 통합하여 풀서비스에 대한 수요를 실감할 수 있습니다. AI를 활용한 시험 설계 플랫폼은 샘플 크기 요구 사항을 줄이고 CRO가 차별화된 속도와 비용 지표를 제공할 수 있도록 지원합니다. 그 결과, 수의학 임상시험수탁기관(CRO) 시장은 종량제 모델에서 다년간의 수익원을 확보할 수 있는 통합형, 성과 기반 계약 모델로 전환하고 있습니다.

북미는 세계 최대 반려동물 헬스케어 지출, 임상시험 승인을 간소화하는 확립된 FDA 프레임워크, 미국의 고밀도 CRO 인프라로 인해 2025년 세계 매출의 41.75%를 차지할 것으로 예상됐습니다. 찰스 리버의 CRADL 확장 및 미스프로의 동물 사육 시설 네트워크 업데이트와 같은 자본 프로젝트가 이 지역의 생산능력을 강화하고 있습니다. 그러나 이노티브의 3,500만 달러에 달하는 동물복지 위반 벌금 등 컴플라이언스 위반 사례가 잇따르면서 규제 리스크가 고객의 지지기반을 재편할 가능성을 부각시키고 있습니다. 북미의 성장은 견조한 성장세를 유지하지만, 시장이 성숙기에 접어들면서 성장률은 둔화되는 추세입니다.

아시아태평양은 가장 빠르게 성장하는 시장으로 2031년까지 CAGR 9.34%에 달할 것으로 예상됩니다. 중국 내 1억 가구가 넘는 반려동물 사육 가구와 MARA(동물 관리 및 연구 관리국) 체제의 급속한 규제 강화로 인해 현지 GLP(우수실험실관리기준) 및 GCP(우수임상시험관리기준) 전문 지식에 대한 수요가 꾸준히 증가하고 있습니다. 이러한 요구사항에 대응하기 위해 랩코프는 상하이 캠퍼스의 대형 동물 대응 능력을 두 배로 늘리고, 면역독성학 연구소를 개설했습니다. 인도의 CPCSEA 감독부터 일본의 농림수산성 규제에 이르기까지 다양한 국가별 규정은 복잡성을 야기하는 한편, 아시아태평양의 시험 거버넌스를 포괄적으로 제공하는 CRO에게 프리미엄 요금의 기회를 창출하고 있습니다. 중국과 호주에서 정밀농업의 도입이 확대되면서 수의학 계약연구기관 시장을 뒷받침하는 야외 시험의 양이 증가하고 있습니다. 유럽은 VICH의 일관성과 2024년 12월에 여러 어류 및 가금류 백신을 승인한 EMA CVMP의 활발한 파이프라인을 바탕으로 견조한 점유율을 유지하고 있습니다. 경기 침체로 인해 반려동물에 대한 임의적 지출은 억제될 수 있지만, 공공 부문의 보조금과 강력한 학술 네트워크는 연구 수요를 유지하고 있습니다. 남미, 중동 및 아프리카는 아직 발전 초기 단계에 있지만, 전략적 전망으로 볼 때 주목할 만한 시장입니다. 브라질은 조화로운 서류작업을 위해 움직이고 있으며, 걸프협력회의(GCC) 회원국들은 수입 등록 규칙을 정식으로 제정하려고 하고 있습니다. 이러한 변화로 인해 신흥시장 컴플라이언스에 대응할 수 있는 CRO에 점차 새로운 비즈니스가 유입될 것입니다. 이러한 움직임을 종합하면, 수의 CRO 시장은 지리적으로 분산된 성장 프로파일을 강조하고 있다고 할 수 있습니다.

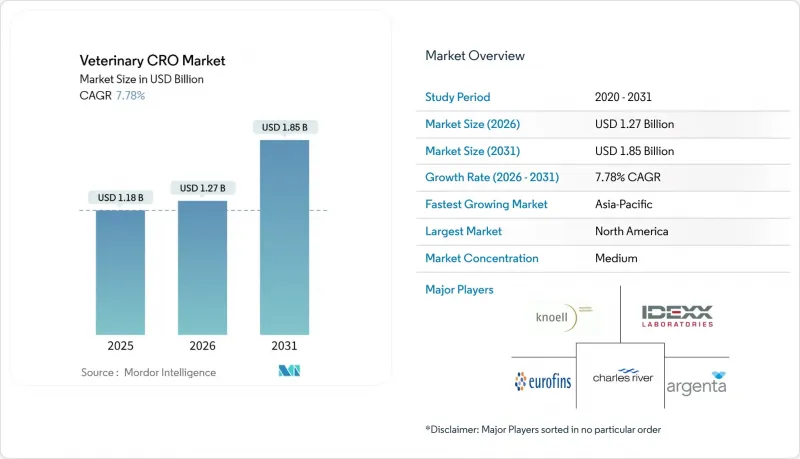

The veterinary contract research organization market size in 2026 is estimated at USD 1.27 billion, growing from 2025 value of USD 1.18 billion with 2031 projections showing USD 1.85 billion, growing at 7.78% CAGR over 2026-2031.

Demand is escalating because animal-health companies face tougher regulatory rules, rising R&D costs, and the need to speed time-to-market for novel therapeutics. Zoonotic disease emergencies such as the 2024-2025 H5N1 avian-influenza crisis have heightened the urgency for rapid vaccine development services, while regulatory fast-track schemes in the United States and Europe reward CROs that can shepherd dossiers through accelerated pathways. Technology adoption, notably AI-enabled diagnostics and precision livestock farming data, is widening the scope of outsourced studies, and capital flows from venture investors into pet-biotech start-ups are enlarging the client base for the veterinary contract research organization market.

Pet owners in the United States spent USD 40 billion on veterinary care in 2024, driving strong demand for innovative therapies that require outsourced research capabilities. Humanization of pets pushes sponsors to pursue oncology, neurology, and longevity trials that mirror human drug protocols, elevating complexity and favouring CROs able to run multi-arm, placebo-controlled studies across large clinic networks. Loyal's LOY-002 program for canine lifespan extension, now in a 1,000-dog pivotal study backed by USD 22 million in new capital, exemplifies how the veterinary contract research organization market enables high-profile, pet-centric R&D programs. In China, more than 100 million households keep companion animals, broadening the Asia-Pacific demand base for local CRO capacity. Cost pressures on clinics create incentive to adopt externally managed research protocols that minimise overhead, further reinforcing the outsourcing model.

The FDA's Animal and Veterinary Innovation Agenda launched four innovation centres in 2024 and earmarked USD 3 million to advance accelerated approval science, opening short-cycle pathways for unmet veterinary needs. Expanded provisions under the Minor Use Minor Species (MUMS) Act now allow conditional approval routes for major-species indications with limited existing treatments, exemplified by TriviumVet's feline HCM candidate admitted to the pathway in February 2025. Parallel harmonisation under VICH has aligned CMC dossiers across the EU, US, and Japan, simplifying multi-region submissions yet raising the premium on consultants who master cross-jurisdictional nuances. Rising FDA user-fee rates-USD 581,735 per 2025 application-drive smaller sponsors toward external regulatory partners. Collectively, these measures accelerate pipeline throughput and enlarge the addressable pool for the veterinary contract research organization market.

Total R&D outlays can top USD 1 billion for a single veterinary biologic, squeezing smaller innovators and limiting the pool of viable sponsors. Rising FDA application fees add further burden, and unlike human pharmaceuticals, veterinary sales volumes rarely match the scale needed to amortise costs. While accelerated approval routes exist, they impose substantial post-market study obligations, which still require CRO engagement and capital. Emerging-market regulators often lack harmonised guidelines, adding country-specific studies that lengthen timelines. Although these hurdles temper absolute growth, they simultaneously incentivise outsourcing, preserving the long-run trajectory of the veterinary contract research organization market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Clinical trials contributed 33.12% to veterinary contract research organization market share in 2025, reflecting the need for controlled, multi-site efficacy studies demanded by regulators. The sub-segment is forecast to post steady high-single-digit gains as complex biologics move through pipelines. Regulatory and consulting work, however, is projected to grow fastest at 8.52% CAGR as sponsors turn to external experts to navigate FDA innovation-agenda pilots, VICH harmonisation, and Japan's Ministry of Agriculture protocols. Toxicology services remain indispensable because safety packages underpin all approvals, while smaller niches such as bioanalytical assay development benefit from precision-farming-enabled sample-tracking advances.

Rising study complexity drives CROs to bundle services: TriviumVet manages a 300-cat, multi-country HCM study that integrates clinical operations, imaging core labs, and central pathology services, illustrating full-service demand. AI-aided trial-design platforms cut sample-size requirements, enabling CROs to offer differentiated speed and cost metrics. Consequently, the veterinary contract research organization market is witnessing a pivot from fee-for-service models toward integrated, outcome-based contracts that lock in multi-year revenue streams.

The Veterinary Contract Research Organization Market Report is Segmented by Service Type (Clinical Trials, Toxicology, Regulatory & Consulting, Other Specialized Services), Animal Type (Companion Animals, Livestock), End User (Animal-Health Pharma & Biotech Companies, Academic & Research Institutes, Other End Users), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America held 41.75% of global revenue in 2025 thanks to the world's largest companion-animal healthcare spend, an established FDA framework that streamlines clinical-trial approvals, and dense CRO infrastructure clusters in the United States. Capital projects such as Charles River's CRADL expansion and Mispro's vivarium network upgrades reinforce regional capacity. Nonetheless, compliance incidents-Inotiv's USD 35 million welfare fine chief among them-spotlight regulatory risk that can reshuffle client allegiances. Growth in North America remains healthy but is moderating as the market approaches maturity.

Asia-Pacific is the fastest-expanding arena, predicted to hit a 9.34% CAGR through 2031. China's 100 million-plus pet households, coupled with rapid regulatory evolution under the MARA framework, generate robust demand for local GLP and GCP expertise. Labcorp doubled large-animal capacity at its Shanghai campus and inaugurated an immunotoxicology lab to meet these requirements. Diverse national rules-from India's CPCSEA oversight to Japan's MAFF controls-create complexity but also premium fee opportunities for CROs offering end-to-end Asia-Pacific study governance. Precision farming roll-outs across China and Australia are adding field-study volume that supports the veterinary contract research organization market. Europe maintains a solid share on the back of VICH coherence and an active EMA CVMP pipeline, which cleared multiple fish and poultry vaccines in December 2024. Economic softness may temper discretionary pet spending, yet public-sector grants and strong academic networks sustain research demand. South America and the Middle East & Africa are nascent but visible on the strategic horizon: Brazil is moving toward harmonised dossiers, and Gulf Cooperation Council states are formalising import-registration rules-both shifts will slowly channel new business to CROs equipped to navigate emerging-market compliance. Taken together, these dynamics underscore a geographically diversified growth profile for the veterinary contract research organization market.