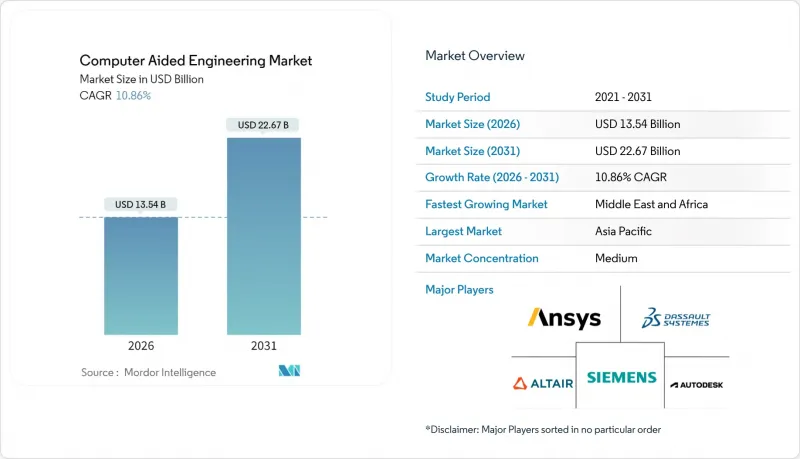

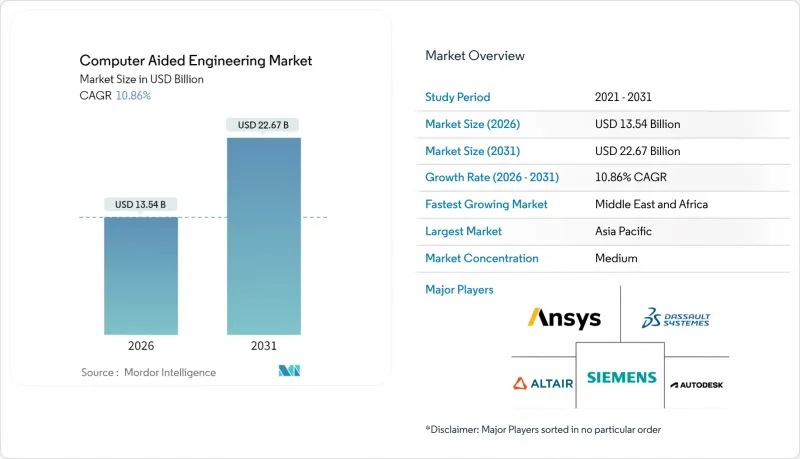

CAE(Computer aided Engineering) 시장은 2025년에 122억 1,000만 달러로 평가되며, 2026년 135억 4,000만 달러에서 2031년까지 226억 7,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 10.86%로 예상됩니다.

고성능 클라우드 인프라, AI 지원 솔버, 가상 프로토타이핑에 대한 규제 요건이 강화되면서 제품 개발 수명주기 전반에 걸쳐 도입이 가속화되고 있습니다. 기업은 보다 엄격한 출시 시기와 내장된 지속가능성 목표를 달성하기 위해 후기 단계의 물리 테스트를 초기 단계의 멀티피직스 시뮬레이션으로 대체하고 있습니다. 대규모 반도체 투자와 자동차 전동화 진전에 힘입은 아시아의 주도적 입지가 세계 시장을 주도하고 있습니다. 소프트웨어 라이선스가 여전히 주요 수입원이지만, 기업이 점점 더 복잡해지는 디지털 트윈 환경에 필요한 기술을 갖추기 위해 고군분투하는 가운데 컨설팅 및 통합 서비스가 급성장하고 있습니다.

자동차 제조업체들은 충돌 안전성을 유지하면서 차량 중량을 줄이기 위해 생성 알고리즘과 유한요소해석기를 결합하고 있습니다. MeshWorks는 배터리 모듈 개발 기간을 최대 70% 단축하고, 기존에는 비현실적이었던 토폴로지 검증을 가능하게 합니다. 연구에 따르면 10%의 질량 감소는 6-8%의 에너지 소비 개선으로 이어지며, 이는 적극적인 무공해 규제를 추진하는 시장에서 매우 중요한 의미를 지닙니다. 유럽과 중국에서는 보조금 제도와 차종별 평균 CO2 배출량 목표에 따라 경량화 구조가 경쟁에서 필수 요건이 되고 있으며, 그 영향은 더욱 확대되고 있습니다. AI 지원 시뮬레이션 템플릿을 도입하는 공급업체는 형식승인 주기의 단축과 다분야 팀의 효과적인 활용을 기대하고 있습니다.

FAA의 2024년 동력 승강기 규정에서는 시뮬레이션 데이터를 인증 증거로 인정하여 고비용의 실기 시험을 줄일 수 있습니다. EASA의 병행 노력은 추진 시스템 및 구조물 승인을 가속화하기 위해 디지털 엔지니어링을 권장하고 있습니다. 밀레니엄 M1 CFD 슈퍼컴퓨터와 같은 하드웨어-소프트웨어 통합 플랫폼은 몇 주 걸리던 항공 열역학 해석을 몇 시간으로 단축하고, 엔지니어링의 처리 능력을 더 까다로운 프로그램 일정에 맞출 수 있게 해줍니다. 그 결과, 민간 및 국방 분야 모두에서 비반복적 지출을 줄이고 서비스 투입을 가속화할 수 있습니다.

가변 요금제는 OEM 프로그램 주기 후반에 시뮬레이션 수요가 최고조에 달하는 부품 제조업체에게 계획 리스크를 발생시킵니다. 학술적 검토에 따르면 중소기업은 자원의 제약과 비용의 불투명성으로 인해 예측 분석 도입에 있으며, 대기업에 비해 뒤쳐져 있다고 합니다. 벤더가 구독 계층을 표준화하거나 소비 상한을 도입하기 전까지는 중소기업은 완전한 전환을 지연시킬 수 있으며, 이는 전체 CAE(Computer aided Engineering) 시장의 확장을 억제할 수 있습니다.

소프트웨어 부문은 2025년 매출의 72.85%를 차지할 것으로 예상되며, 이는 CAE 시장을 지원하는 솔버 혁신과 인터페이스 업그레이드의 핵심적인 역할을 반영합니다. Ansys의 2024 R1 릴리즈는 모듈형 워크스페이스와 AI 지원 데이터 파이프라인을 도입하여 워크플로우 생산성에 대한 지속적인 투자를 보여주었습니다. 물리 라이브러리 확장과 GPU 가속은 신규 시장 진출기업이 전문 분야에서 점유율을 깎아먹는 와중에도 기존 라이선스의 갱신을 확실하게 유지하고 있습니다. 서비스 분야는 규모가 작지만, 멀티피직스, 클라우드 오케스트레이션, AI 모델 트레이닝의 지식 격차에 직면한 기업이 12.46%의 연평균 복합 성장률(CAGR)로 더욱 빠르게 성장하고 있습니다.

복잡성이 증가함에 따라 표준적인 즉시 사용 가능한 도입과 베스트 프랙티스를 채택하는 것 사이에는 점점 더 큰 격차가 발생하고 있습니다. 컨설팅 기업은 현재 배터리 열 폭주 분석 등 도메인 특화형 템플릿을 번들로 묶어 프로젝트 시작을 효율화하고 있습니다. 이 컨설팅 계층은 기존 유한요소해석 툴에서 통합 디지털 트윈 플랫폼으로 전환하는 조직에 특히 유용합니다. 그 결과, 서비스 매출은 전체 CAE(Computer aided Engineering) 시장에서 더 큰 비중을 차지하고 있으며, 특히 내부 전문 지식이 부족한 신흥 경제국에서 두드러지게 나타나고 있습니다.

유한요소해석은 구조, 열, 전자기 문제에 대한 광범위한 적용성으로 인해 2025년 CAE 시장 점유율의 35.22%를 차지했습니다. 메쉬 자동화와 재료 모델의 지속적인 개선으로 고정밀 어셈블리의 수렴 속도가 향상되고 있습니다. 제너레이티브 디자인 오버레이는 토폴로지 최적화 격자를 활용하여 항공기 브래킷의 금속 부피를 줄여 두 자릿수 중량 감소를 실현했습니다.

전산유체역학(CFD)은 전자기기의 열적 병목현상과 공기역학 최적화의 융합으로 11.74%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장하고 있는 분야입니다. 케이던스사의 GPU 기반 슈퍼컴퓨터 '밀레니엄 M1'은 비정상 유동 시뮬레이션에서 비약적인 고속화를 실현하여 설계 사이클 기간 내에 고해상도 해석을 가능하게 합니다. AI 프레임워크가 스파르타 CFD 트레이닝 세트로 유동장을 예측하는 가운데, 각 벤더들은 공정 산업 및 재생에너지 설계 분야에서 보급 확대를 예상하고 있습니다.

아시아는 2025년 매출의 38.12%를 차지하며 반도체 확대와 국가 지원 제조업의 디지털화에 힘입어 1위를 차지했습니다. 중국의 자급자족 추진으로 LICOMK++ 해양 모델링과 같은 기술 혁신이 생겨나면서 국내 HPC 역량의 성장이 강조되고 있다(scmp.com). 인도의 국가 슈퍼컴퓨팅 계획과 한국의 팹 투자가 이 지역의 두 자릿수 CAGR을 더욱 지원하고 있습니다. 이 지역의 거대한 전자부품 공급망으로 인해 멀티피직스 CFD 라이선스에 대한 수요가 지속적으로 증가하고 있습니다.

북미는 2위를 차지했으며, 미국의 국방 현대화 및 항공우주 디지털 트윈 분야 활동이 주도했습니다. 청정 에너지 인프라에 대한 연방 정부의 인센티브 정책으로 인해 풍력 터빈 및 그리드 스토리지 프로젝트에서 구조 및 열 시뮬레이션에 대한 수요가 증가하고 있습니다. 클라우드 하이퍼스케일러의 근접성은 사용자에게 탄력적인 컴퓨팅 리소스를 제공하고, 일상 업무 흐름내 AI 통합을 가속화합니다.

유럽은 자동차 및 민간 항공 시뮬레이션 분야에서 탄탄한 기반을 유지하고 있습니다. 수소 추진 시스템 및 초 고효율 기체 구조에 대한 청정 항공 자금이 차세대 CFD 및 복합재료 모델 솔버에 대한 예산 배분을 촉진하고 있습니다. 수명주기 탄소회계 의무화 규정에 따라 예지보전 및 연료소비 최적화를 위한 디지털 트윈 도입이 진행되고 있습니다. 한편, 중동은 12.17%의 지역 최고 CAGR을 기록했으며, 정유업체가 도입한 에너지 최적화 트윈으로 인해 계획되지 않은 다운타임이 35% 감소했습니다.

The computer aided engineering market was valued at USD 12.21 billion in 2025 and estimated to grow from USD 13.54 billion in 2026 to reach USD 22.67 billion by 2031, at a CAGR of 10.86% during the forecast period (2026-2031).

High-performance cloud infrastructure, AI-assisted solvers, and stricter regulatory expectations for virtual prototyping are accelerating adoption across product-development lifecycles. Companies are replacing late-stage physical testing with early-stage multiphysics simulation to meet tighter launch windows and embedded sustainability targets. Asia's leadership, sustained by large-scale semiconductor investments and rising automotive electrification, underpins global momentum. Software licences remain the principal revenue generator, yet advisory and integration services are surging as enterprises struggle to keep pace with the skills required for increasingly complex digital-twin environments.

Automakers are coupling generative algorithms with finite-element solvers to reduce curb weight without sacrificing crashworthiness. MeshWorks shows development-time cuts of up to 70% for battery modules, letting engineers test previously impractical topologies.Studies demonstrate 10% mass reductions translating into 6-8% energy-consumption improvements-vital in markets pushing aggressive zero-emission mandates. The impact is magnified in Europe and China, where subsidy structures and fleet-average CO2 targets make lightweight architectures a competitive requirement. Suppliers integrating AI-ready simulation templates expect shorter homologation cycles and better utilisation of multi-disciplinary teams.

The FAA's 2024 powered-lift aircraft rule recognises simulation data for certification evidence, shrinking costly full-scale tests. Parallel initiatives at EASA encourage digital engineering to accelerate propulsion and structure approvals. Hardware-software platforms such as the Millennium M1 CFD Supercomputer compress multi-week aero-thermal studies into hours, aligning engineering throughput with tighter programme timetables. The result is lower non-recurring expenditure and faster entry into service across both commercial and defence segments.

Variable billing creates planning risk for parts makers whose simulation demand peaks late in OEM programme cycles. Academic reviews show SMEs lag larger peers in predictive-analytics uptake because of resource constraints and cost opacity. Until vendors standardise subscription tiers or introduce consumption caps, smaller firms may delay full migration, tempering overall computer aided engineering market expansion.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The software segment contributed 72.85% of 2025 revenue, reflecting its centrality to solver innovation and interface upgrades that underpin the computer-aided engineering market. Ansys' 2024 R1 release rolled out modular workspaces and AI-ready data pipelines, illustrating steady investment in workflow productivity. Expanded physics libraries and GPU acceleration lock in entrenched licence renewals, even as newer entrants chip away in specialist niches. Services, though smaller, are scaling faster at 12.46% CAGR as enterprises confront knowledge gaps in multiphysics, cloud orchestration, and AI model training.

Rising complexity is widening the divide between standard out-of-the-box deployment and best-practice adoption. Advisory firms now bundle domain-specific templates-such as battery thermal run-away analyses-streamlining project kick-offs. This consultative layer is particularly valuable to organisations transitioning from legacy finite-element tools to integrated digital-twin platforms. Consequently, services revenue is capturing a larger portion of total computer aided engineering market size, especially within emerging economies where in-house expertise remains scarce.

Finite element analysis accounted for 35.22% of the 2025 computer-aided engineering market share, sustained by broad applicability across structural, thermal, and electromagnetic problems. Continuous improvements in mesh automation and material models enable faster convergence for high-fidelity assemblies. Generative design overlays now exploit topology-optimised lattices to reduce metal volumes in aircraft brackets, achieving double-digit weight savings.

Computational fluid dynamics is the fastest-growing category at 11.74% CAGR as electronics thermal bottlenecks and aerodynamic optimisation converge. Cadence's GPU-based Millennium M1 supercomputer demonstrates order-of-magnitude speed-ups for unsteady flow simulations, unlocking high-resolution studies within design-cycle windows. As AI frameworks predict flowfields with sparse CFD training sets, vendors anticipate broader uptake in process industries and renewable-energy design.

The Computer Aided Engineering Market is Segmented by Component (Software, Services), Software Type (Finite Element Analysis, Computational Fluid Dynamics, and More), Deployment (On-Premise, Cloud Based), Organization Size (Large Enterprises, Small and Medium Enterprises), End-User Vertical (Automotive, Aerospace and Defense, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia led with 38.12% of 2025 revenue, buoyed by semiconductor expansion and state-backed manufacturing digitalisation. China's drive for self-reliance spurred breakthroughs such as LICOMK++ ocean modelling, underscoring domestic HPC capability growth scmp.com. India's National Supercomputing Mission and South Korea's fab investments further support a double-digit regional CAGR. The region's outsized electronics supply chain keeps multiphysics CFD licences in sustained demand.

North America ranked second, dominated by the United States' activity in defence modernisation and aerospace digital twins. Federal incentives for clean-energy infrastructure amplify demand for structural and thermal simulation in wind-turbine and grid-storage projects. Cloud-hyperscaler proximity affords users elastic compute headroom, accelerating AI integration within day-to-day workflows.

Europe retains strong footholds in automotive and commercial aviation simulation. Clean-Aviation funding for hydrogen propulsion and ultra-efficient airframes steers budgets toward next-generation CFD and composite-model solvers. Regulations mandating lifecycle carbon accounting motivate digital-twin rollouts for predictive maintenance and fuel-burn optimisation. Meanwhile, the Middle East posts the highest regional CAGR at 12.17% as refiners deploy energy-optimisation twins that cut unplanned downtime by 35%.