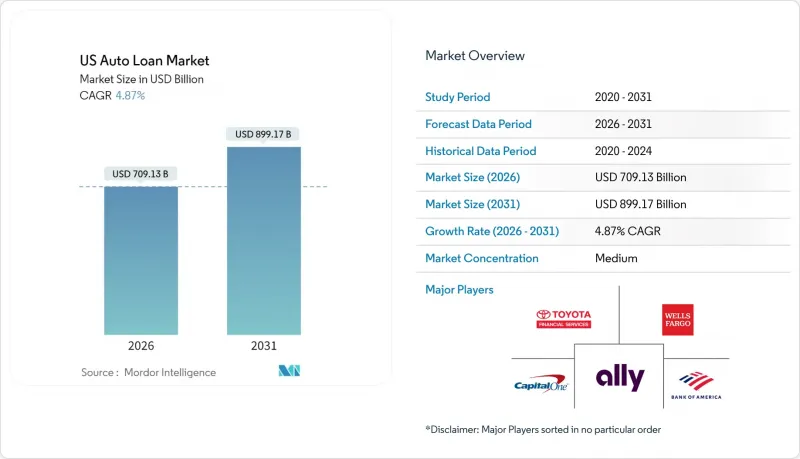

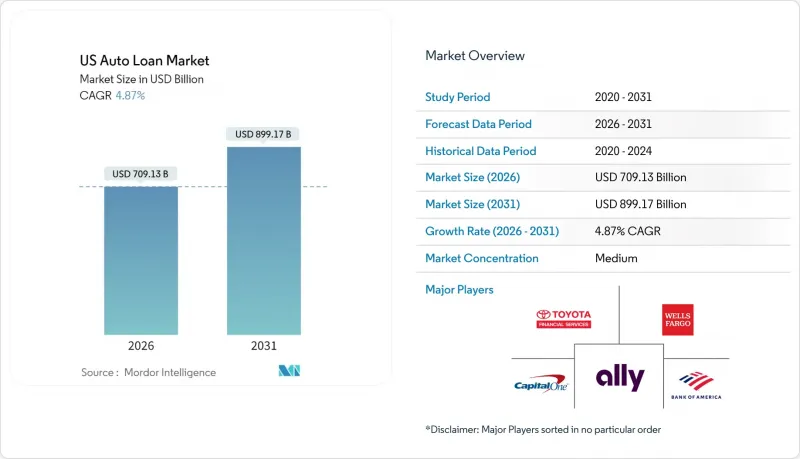

미국의 자동차 대출 시장은 2025년 6,762억 달러에서 2026년에는 7,091억 3,000만 달러로 성장하며, 2026-2031년에 CAGR 4.87%로 추이하며, 2031년까지 8,991억 7,000만 달러에 달할 것으로 예측되고 있습니다.

차량 가격 상승, 연방기금 금리 하락, 디지털화의 급속한 발전으로 신용 기준이 강화되는 가운데 자동차 금융에 대한 수요는 안정적으로 유지되고 있습니다. 신차 평균 가격이 많은 중산층 가구가 감당할 수 없는 수준으로 상승함에 따라 중고차 금융이 뚜렷한 주도권을 유지하고 있습니다. 얼터너티브 데이터를 활용한 신용평가로 준우량 및 서브프라임 계층의 대출자에게도 대출 기회가 확대되고, 핀테크 신규 진출기업은 빠르게 성장하고 있습니다. 라스트 마일 배송을 담당하는 차량 사업자들의 상용차에 대한 관심이 높아짐과 동시에 경트럭의 인기로 인해 평균 융자금액이 상승하고 있습니다. 총 이자 부담이 늘어나는 상황에서도월상환액을 관리 가능한 범위로 유지하려는 대출자들이 늘어나면서 5년 이상의 장기 대출이 확산되고 있습니다.

2024년에는 평균 거래가격이 4만 8,000달러를 넘어섰고, 대출자들은 상환능력을 확보하기 위해 72개월 이상의 상환기간을 확보해야 합니다. 대출자 입장에서는 원금 잔액 증가로 평생 이자매출을 기대할 수 있으며, 환영하는 한편, 채무불이동 발생시 손실액이 커지기 때문에 충당금도 쌓아두고 있습니다. 가격 상승으로 인해 소비자들은 동등한 실용성을 대폭 할인된 가격으로 얻을 수 있는 중고차로 전환이 가속화되고 있습니다. 반도체 등 핵심 부품공급 부족은 2025년까지 신차 생산을 계속 억제하고 가격 상승 압력을 높이고 있습니다. 현재 대출기관들은 리스크를 제한하기 위해 소득 대비 가격 비율이 15%를 초과할 경우 경고를 발령하는 소득 확인 알고리즘에 대한 의존도를 높이고 있습니다.

머신러닝 엔진은 2분 이내에 신용 판단을 수행하여 수동 심사 비용을 30% 절감합니다. 인적 심사 대비 대출 수익성을 10.2% 향상시키는 동시에 연체율을 6.8% 감소시킵니다. 대출기관, 판매점, EC 포털 간의 API 연계를 통해 한 화면에서 '구매 및 대출' 프로세스를 실현하여 이탈률을 크게 낮출 수 있습니다. 디지털 워크플로는 지역적 범위 확대에도 기여하며, 지역 은행이 지점망을 구축하지 않고도 여러 주에 걸쳐 멀리 떨어진 고객을 확보할 수 있게 해줍니다. 경기 침체기에는 클라우드 네이티브의 대출 개시 프로세스의 비용 우위가 대출기관의 경쟁적 할인에 대한 순금리 마진 보호에 기여합니다. 이러한 플랫폼내 컴플라이언스 모듈은 연방 정부의 지침이 변경될 때 자동으로 업데이트되어 법적 위험과 감사 지적을 줄입니다.

연이은 금리 인상으로 2024년 말까지 자동차 대출의 평균 연이율(APR)은 7%를 넘어섰고, 적격 대출자 층은 약 5분의 1로 줄어들었습니다. 서브프라임 계층의 신청자들은 현재 두 자릿수 금리에 직면하고 있으며, 많은 사람들이 현지 구매-현지 지불 방식의 매장이나 차량 공유 서비스로 유입되고 있습니다. 이에 대해 대부업체는 상환기간을 84개월로 연장하는 대응을 취하고 있는데, 이는 자산가치 축적을 저해하고 대출 실행시 대출가치비율(LTV)을 110% 이상으로 끌어올리는 결과를 초래합니다. 신협은 저비용의 예금자금을 활용하여 시중은행보다 낮은 금리를 유지함으로써 지역내 재융자 수요 증가에 힘을 보태고 있습니다. 딜러 측은 제조업체의 현금 인센티브 확대로 대응하고, 비용 부담을 다시 OEM의 전속 금융 자회사에 전가하려는 움직임을 보이고 있습니다.

2025년 기준 미국 자동차 대출 시장의 86.25%를 승용차 대출이 차지하고 있습니다. 이는 가정이 여전히 개인 이동 수단에 크게 의존하고 있기 때문입니다. 그러나 E-Commerce 확대에 따른 택배 물량 증가와 긱 이코노미형 배차 플랫폼의 보급으로 상용차 분야는 2031년까지 연평균 복합 성장률(CAGR) 6.08%로 확대될 것으로 전망됩니다. 수요는 라스트마일 배송, 택배 서비스, 이동식 작업장에 사용되는 3-5등급 트럭과 화물 밴에 집중되어 있습니다. 전문 금융기관은 텔레매틱스를 대출 계약에 통합하여 가동 주기를 추적하고 담보 가치를 유지하는 예방적 유지보수를 촉진하고 있습니다. 디젤 연료비 상승과 배기가스 규제 강화로 인해 차량의 전동화가 촉진되고 있으며, 배터리 리스 부대서비스라는 새로운 틈새 시장을 개발하고 있습니다.

상업용 대출 심사는 개인 신용과 사업체 신용을 모두 대상으로 하며, FICO 점수와 더불어 현금흐름 분석이 요구됩니다. 은행은 중소기업과의 자금관리 관계를 활용하여 설비대출과 기업 당좌예금 계좌의 교차판매를 통해 고정성 높은 예금을 확보합니다. 핀테크 기업은 실시간 POS 데이터의 현금 흐름 스크래핑을 활용하여 기존 재무제표가 없는 개인사업자의 심사를 평가합니다. 가동 중단시 보상을 보장하는 보험 부수 서비스가 보급되어 트럭이 가동 중단 상태에서도 지불 능력을 안정적으로 유지합니다. 교외 및 지방 우편번호 지역에서의 물류 수요 증가에 따라 미국의 상업용 자산용 자동차 대출 시장 규모는 승용차 대출 잔액보다 빠른 속도로 확대될 것으로 예측됩니다.

2025년 기준 세단, 해치백, 크로스오버를 포함한 승용차가 미국 자동차 대출 시장의 87.35%를 차지할 것이며, 픽업트럭과 소형 밴은 2031년까지 연평균 복합 성장률(CAGR) 7.05%로 확대될 것으로 예측됩니다. 반도체 부족으로 인한 수요 지연으로 딜러들의 예약 리스트는 2025년 인도분까지 이어지고 있으며, 판매 파이프라인 전망은 유지되고 있습니다. 라이프스타일 마케팅을 통해 픽업트럭을 가족용 교통수단 및 주말 모험용 장비로 포지셔닝하여 고객층 확대를 도모하고 있습니다. 이에 대해 제조업체 계열 금융사들은 등급별 잔존가치표를 도입해 재판매 가치가 높은 옵션 패키지를 선택한 구매자에게 우대혜택을 제공합니다.

연비 규제로 인해 OEM 업체들은 픽업트럭에 소형 터보 엔진과 하이브리드 파워트레인을 탑재하도록 장려하고 있으며, 이는 운영 비용을 약간 개선하고 더 높은 MSRP(제조업체 희망소비자가격)를 더 쉽게 받아들일 수 있도록 하고 있습니다. 중고시장 분석에 따르면 3년이 지난 크루캡 트럭은 신차 가격의 65-70%를 유지하고 있으며, 대형 세단의 50-55%보다 높기 때문에 대출자의 손실 위험을 줄일 수 있습니다. 따라서 위험 대비 이익률 지표가 매력적으로 유지되는 가운데 미국 자동차 대출 시장에서 픽업트럭의 점유율은 자연스럽게 증가하고 있습니다. 반면, 오토바이와 세발자전거 금융은 계절적 사용 제한과 보험사의 제약으로 인해 여전히 틈새 시장에 머물러 있습니다.

The US Auto Loan Market is expected to grow from USD 676.20 billion in 2025 to USD 709.13 billion in 2026 and is forecast to reach USD 899.17 billion by 2031 at 4.87% CAGR over 2026-2031.

Rising vehicle prices, lower federal funds rates, and rapid digitalization keep demand for vehicle financing steady, even as credit standards tighten. Used-vehicle financing maintains clear leadership because average new-vehicle prices have climbed beyond the reach of many middle-income households. Fintech entrants grow briskly on the back of alternative data underwriting that opens credit access to near-prime and sub-prime borrowers. Commercial vehicles attract heightened interest from fleets serving last-mile delivery, while light-truck popularity pushes average ticket size up. Longer loan tenures above five years are gaining traction as borrowers try to keep monthly instalments manageable despite higher total interest outlays.

Average transaction prices climbed above USD 48,000 in 2024, forcing borrowers to stretch repayment horizons beyond 72 months for affordability[. Lenders welcome the higher principal balances because lifetime interest income rises, yet they also raise reserves as loss severity grows when defaults occur. Higher pricing accelerates the consumer pivot toward used vehicles, where comparable utility is available at sizeable discounts. Supply shortages of critical components such as semiconductors continue to constrain new-vehicle output through 2025, keeping price pressure elevated. Lenders now rely more heavily on income-verification algorithms that flag price-to-income ratios breaching 15% to limit exposure.

Machine-learning engines deliver credit decisions in under two minutes and cut manual underwriting costs by 30%, producing 10.2% higher loan profitability with 6.8% fewer defaults than human review. API links among lenders, dealerships, and e-commerce portals enable a single-screen "shop-and-finance" journey that slashes abandonment rates. Digital workflows also boost geographic reach, letting regional banks acquire customers several states away without branch infrastructure. During economic slowdowns, the cost advantage of cloud-native origination helps lenders protect net-interest margins against competitive discounting. Compliance modules within these platforms auto-update when federal guidance changes, reducing legal risk and audit findings.

Successive rate hikes pushed average auto-loan APRs beyond 7% by late 2024, shrinking the qualified borrower pool by roughly one-fifth. Sub-prime applicants now face double-digit pricing, driving many toward buy-here-pay-here outlets or ride-sharing alternatives. Lenders counter by lengthening terms to 84 months, though that undermines equity build-up and raises loan-to-value ratios above 110% at origination. Credit unions leverage cheaper deposit funding to hold rates lower than large banks, fuelling regional refinancing waves. Dealers respond with bigger manufacturer cash incentives that shift the cost burden back onto OEMs' captive finance subsidiaries.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Passenger-vehicle loans accounted for 86.25% of the US auto loan market size in 2025 because households still rely heavily on private mobility. Nonetheless, the commercial-vehicle slice is set to expand at a 6.08% CAGR through 2031 as e-commerce accelerates parcel volumes and gig-driving platforms proliferate. Demand concentrates on Class 3-5 trucks and cargo vans used for last-mile delivery, courier services, and mobile workshops. Specialized lenders integrate telematics into loan covenants, tracking duty cycles and encouraging preventive maintenance that preserves collateral value. Rising diesel expenses and emissions regulations encourage fleet electrification, opening an adjacent niche for battery-lease overlays.

Commercial underwriting straddles personal and business credit, requiring cash-flow analyses alongside FICO scores. Banks leverage treasury relationships with small firms to cross-sell equipment loans and business checking accounts, locking in sticky deposits. Fintechs deploy cash-flow scraping of real-time POS data to evaluate sole-proprietor applicants who lack traditional statements. Insurance add-ons that guarantee downtime coverage gain popularity, smoothing payment capacity if trucks sit idle. The US auto loan market size for commercial assets will therefore compound faster than passenger balances as logistics intensity rises across suburban and rural ZIP codes.

Cars-including sedans, hatchbacks, and crossovers-accounted for 87.35% of the US auto loan market size in 2025, yet pickup trucks and small vans will expand at 7.05% CAGR through 2031. Pent-up demand from semiconductor shortages means dealerships carry reservation lists that still roll into 2025 deliveries, sustaining pipeline visibility. Lifestyle marketing frames pickups as family haulers and weekend adventure gear, broadening their demographic appeal. Captive finance units respond with trim-level-specific residual-value tables that reward buyers choosing option packages with historically strong resale.

Fuel economy regulations push OEMs to fit smaller turbo engines and hybrid powertrains into pickups, slightly improving operating costs and making higher MSRPs more palatable. Secondary-market analytics show three-year-old crew-cab trucks retaining 65-70% of their original value, superior to large sedans at 50-55%, reducing lender loss severity. The US auto loan market share of pickups thus grows organically as risk-reward metrics stay attractive. Conversely, motorcycle and three-wheeler financing remains niche, limited by seasonal usage and insurer constraints.

The US Auto Loan Market Report is Segmented by Vehicle Type (Passenger Vehicle, Commercial Vehicle), Vehicle Model (Motorcycles/Scooters, Cars, and More), Ownership (New Vehicles, Used Vehicles), Provider Type (Banks, Non-Banking Financial Institutions, and More), and Tenure (Less Than 3 Years, 3-5 Years, and More). The Market Forecasts are Provided in Terms of Value (USD).