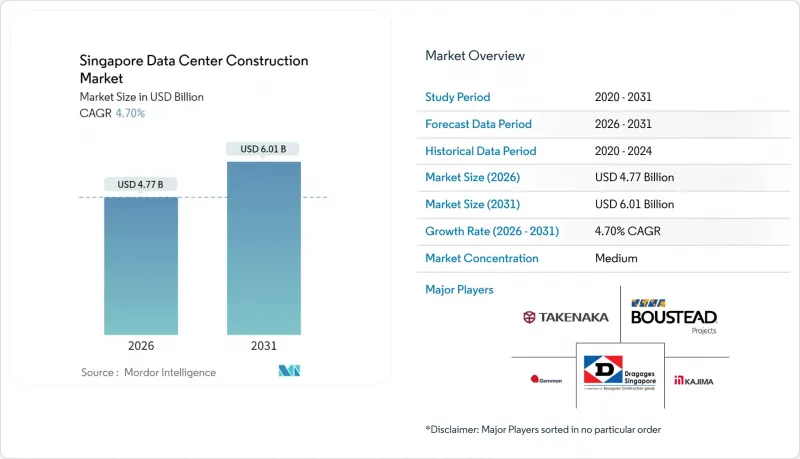

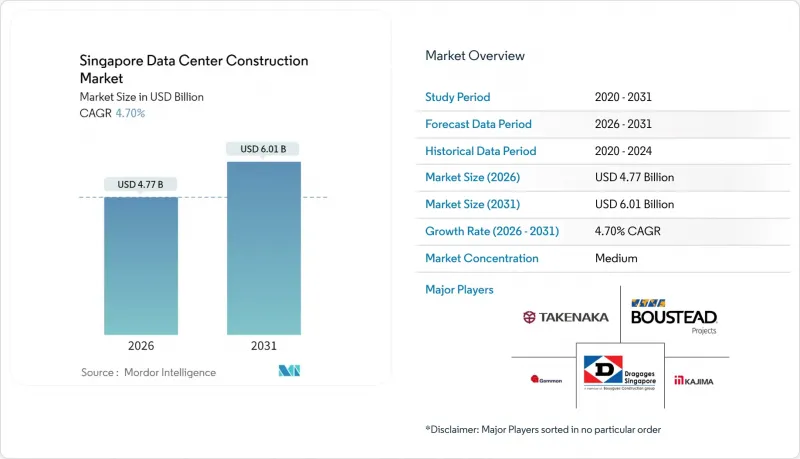

싱가포르의 데이터센터 건설 시장은 2025년 45억 6,000만 달러에서 2026년에는 47억 7,000만 달러로 성장하며, 2026-2031년에 CAGR 4.70%로 추이하며, 2031년까지 60억 1,000만 달러에 달할 것으로 예측됩니다.

싱가포르는 엄격하게 관리되는 전력 배분 정책, 견고한 해저 케이블 연결, 금융 허브로서의 지위가 지속적인 투자를 지원하고 있습니다. 한편, 사업자들은 토지 부족과 높은 건설 비용에 직면해 있습니다. 그린 데이터센터 로드맵에 따른 규제 강화로 전력사용효율(PUE) 1.3 이상을 달성하는 설계가 촉진되고, 입찰 사양 및 장비 선택 방식이 변화하고 있습니다. 하이퍼스케일러 기업은 GPU 고밀도 인프라를 지속적으로 도입하고 있으며, 랙 평균 전력 소비량이 50kW를 초과하고, 첨단 개폐기, 액체 냉각, 모듈식 조립식화에 대한 수요를 가속화하고 있습니다. 한편, 싱가포르와 조호르를 연결하는 트윈 허브 전략은 핵심 워크로드에 대한 5밀리초 미만의 지연을 유지하면서 용량 잉여를 허용함으로써 현지의 제약을 완화하고 있습니다. 데이터센터 REIT에 대한 투자자들의 관심은 건전한 프로젝트 파이낸싱 파이프라인을 지원하고, 개발업체들이 도시 국가의 높은 토지 및 인건비를 상쇄할 수 있도록 돕고 있습니다.

싱가포르의 개정된 그린 데이터센터 로드맵은 시설이 PUE 1.3 이하를 달성하는 조건으로 최소 300MW의 신규 IT 부하를 할당할 것을 약속하고 있으며, 싱가포르의 데이터센터 건설 시장은 고효율 설계로 전환하고 있습니다. 할당량의 3분의 2는 재생에너지와 대체 백업 연료를 통합하는 프로젝트에 할당되며, 개발자들은 수소 지원 발전기 및 열 회수식 냉각기 채택을 추진하고 있습니다. 선도 기업은 AI 기반 냉각 제어를 도입하여 에너지 사용량을 최대 30%까지 절감하고 있습니다. 한정된 메가와트를 둘러싼 경쟁 입찰이 치열해지면서 설계 컨설팅에 대한 수요가 증가하고, 지속가능성 측면에서 검증된 기업이 유리하게 작용할 것입니다. 중기적으로 이 정책은 시장의 액체 냉각 및 현장 태양광+에너지 저장 하이브리드로의 전환을 가속화할 것입니다. 이러한 요소들이 결합되어 싱가포르 데이터센터 건설 시장에서 전문 계약업체 및 장비 공급업체들의 잠재적인 비즈니스 기회를 확대할 수 있습니다.

생성형 AI의 물결로 인해 랙 밀도가 50kW를 넘어섰고, 싱가포르 데이터센터 건설 시장에서는 기계 및 전기 설비 패키지가 액침냉각 및 직접 칩 냉각으로 전환되고 있습니다. 주요 캠퍼스 개보수 프로젝트에서는 이러한 변화가 두드러져 설정 온도 27℃에 대응하는 냉수 순환 시스템과 액체 냉각 루프를 채택하고 있습니다. 고밀도 도입으로 케이블 배선 거리가 연장되고, 버스웨이의 대형화가 요구됩니다. 이로 인해 자재비는 증가하는 반면, 시운전 기간은 15-20% 연장됩니다. 이에 대해 개발업체들은 구리 사용량을 줄이기 위해 리어 도어 열교환기와 중전압(22kV) 배전 시스템 채택을 추진하고 있습니다. 금융, 의료, 공공 부문의 워크로드에서 AI 추론이 확산되는 가운데, 건설 프로젝트에서 GPU 포드 전용 화이트스페이스를 통합하는 사례가 증가하고 있으며, 국가 전력 상한선에도 불구하고 싱가포르의 데이터센터 건설 시장은 두 자릿수 프로젝트 수 성장을 유지하고 있습니다.

3년간의 유예기간을 거쳐 2024년에 재도입된 싱가포르의 전력 할당량 상한제는 지역 수요 성장률을 밑돌고 있으며, 많은 계획 중인 하이퍼스케일 건설을 정체시키고 있습니다. 개발업체들은 PUE(전력사용효율)와 탄소강도를 중시하는 채점방식의 신청공모 과정에서 경쟁할 수밖에 없고, 건설 전 컨설팅 비용이 부풀어 오르고 있습니다. 메가와트 부족으로 인해 일부 사업자들은 바탐섬이나 조호르주로 증설 용량을 옮기려는 움직임을 보이고 있으며, 이는 싱가포르 데이터센터 건설 시장의 매출 잠재력을 억제하고 있습니다. 장기적인 불확실성은 변압기 및 발전기의 주문 주기 또한 복잡하게 만들고 있으며, 세계 공급 제약으로 인해 리드타임은 이미 장기화되고 있습니다. 이러한 요인들이 복합적으로 작용하여 예측 CAGR을 약 1.4% 낮출 것으로 예측됩니다.

2025년 싱가포르 데이터센터 건설 시장 전체 지출 중 전기 설비 패키지가 37.38%를 차지할 것으로 예측됩니다. 이는 하이퍼스케일러가 22kV 전원 공급, 지능형 배전반, 50kW 이상의 GPU 랙을 위해 설계된 고용량 버스웨이를 선호하는 추세를 반영합니다. 액체냉각은 여전히 기계설비의 한 분야이지만, 가장 빠르게 성장하는 품목으로 2031년까지 싱가포르 데이터센터 건설 시장 규모에 6억 2,850만 달러의 기여를 할 것으로 예측됩니다. 침수 탱크와 리어 도어형 열교환기 채택으로 랙당 화이트 스페이스 면적을 줄여 코로케이션 사업자의 매출 밀도를 향상시킬 수 있습니다. 설계-시공 통합 및 시운전 등의 서비스는 소유주가 PUE 목표의 턴키 검증을 요구하므로 높은 단가로 청구할 수 있습니다. 예측 기간 중 AI 기반 최적화 플랫폼은 전력 및 냉각 루프 모두에 대한 실시간 텔레메트리를 필요로 하므로 전기 설비와 제어 시스템의 통합이 심화될 것입니다. 이를 통해 단일 계약으로 전기와 기계 분야를 모두 아우를 수 있는 기업의 전략적 가치가 높아져 싱가포르 데이터센터 건설 시장에서 경쟁 우위를 확고히 할 수 있게 되었습니다.

기계설비 분야에서는 기존 냉각기에서 칩 1개당 1,200W의 방열이 가능한 펌프식 냉매 시스템이나 유전체 침지 냉각시스템으로 전환이 진행되고 있습니다. 공동 프로그램을 통해 냉각 에너지를 29% 절감하여 랙당 연간 약 2만 5,000달러를 절약할 수 있습니다. 이는 다른 사업자들이 목표로 삼는 비용 절감의 벤치마킹 대상이 되고 있습니다. 일반 건축 분야는 싱가포르의 엄격한 건축기준에서 요구하는 다층구조의 쉘, 내진보강, 방폭 파사드 등으로 안정적인 기여도를 유지하고 있습니다. IT 인프라(랙, 네트워크 패브릭, 케이블 관리)는 고밀도 레이아웃이 더 두꺼운 광섬유 트렁크와 AI 최적화 토폴로지를 필요로 하므로 추가 지출이 발생하고 있습니다. 이러한 변화는 종합적으로 워크로드가 복잡해질수록 싱가포르 데이터센터 건설 시장에서 전문 하청업체들 시장 점유율이 확대되는 추세를 보여줍니다.

2025년 Tier III 시설은 비용과 신뢰성의 균형 잡힌 제안과 99.982%의 가동률 보장으로 싱가포르 데이터센터 건설 시장 점유율의 53.22%를 차지했습니다. 기업 및 클라우드 프로바이더들은 2N 시스템과 같은 이중 설비투자를 필요로 하지 않고, 가동 중에도 업그레이드가 가능한 동시 유지보수가 가능한 인프라를 중요시하고 있습니다. 그러나 핀테크, 트레이딩 데스크, 99.995%의 가용성을 요구하는 소버린 클라우드 워크로드에 힘입어 Tier IV 파이프라인은 CAGR 5.03%로 확대되고 있습니다. 이러한 내결함성 사이트에는 일반적으로 2N UPS, 듀얼 연료 농장, 독립적인 냉수 플랜트가 도입되며, Tier III에 비해 MEP(기계, 전기, 설비) 범위가 두 배로 증가하여 하이티어 건설을 위한 싱가포르 데이터센터 건설 시장 규모를 끌어올리고 있습니다.

아이언마운틴의 싱가포르 시설은 지역적으로 분산된 3개의 미팅룸과 생물학적 보호 접근 통로를 갖춘 Tier IV의 특성을 구현하고 있습니다. Tier I 및 II 프로젝트는 엣지 및 통신사 용도에서 계속되고 있지만, 매출에 대한 기여도는 여전히 제한적입니다. 향후 규제와 고객의 내결함성 요구가 높아짐에 따라 Tier III 사양은 Tier IV에 가까워져 양자의 경계가 모호해질 것으로 예측됩니다. 이에 따라 싱가포르 데이터센터 건설 시장 전체에서 메가와트당 기준 지출이 증가할 것으로 예측됩니다.

The Singapore data center construction market is expected to grow from USD 4.56 billion in 2025 to USD 4.77 billion in 2026 and is forecast to reach USD 6.01 billion by 2031 at 4.70% CAGR over 2026-2031.

Singapore's tightly managed power-allocation policy, robust subsea connectivity, and status as a financial hub anchor sustained investment even as operators confront land scarcity and high build costs. Regulatory momentum under the Green Data Centre Roadmap encourages designs that achieve Power Usage Effectiveness (PUE) of 1.3 or better, reshaping tender specifications and equipment choices. Hyperscalers continue to deploy GPU-dense infrastructure that pushes average rack power beyond 50 kW, accelerating demand for advanced switchgear, liquid cooling, and modular prefabrication. Meanwhile, the twin-hub strategy that links Singapore with Johor mitigates local constraints by allowing capacity spill-over while preserving sub-5 ms latency to core workloads. Investor appetite for data-center REITs supports a healthy project finance pipeline, helping developers offset the city-state's premium land and labor costs.

Singapore's revised Green Data Centre Roadmap commits at least 300 MW of new IT load on the condition that facilities demonstrate PUE of 1.3 or lower, pivoting the Singapore data center construction market toward highly efficient designs. Two-thirds of the quota rewards projects that integrate renewables or alternative backup fuels, prompting developers to specify hydrogen-ready generators and heat-recovery chillers. Early movers have implemented AI-driven cooling control to reduce energy use by up to 30%. Competitive bidding for scarce megawatts intensifies, raising design consultancy demand and favoring firms with a proven sustainability track record. Over the medium term, the policy accelerates the market's migration toward liquid cooling and on-site solar plus energy-storage hybrids. These elements together enlarge the addressable opportunity for specialist contractors and equipment vendors within the Singapore data center construction market.

The generative-AI wave lifts rack densities above 50 kW, forcing mechanical and electrical packages in the Singapore data center construction market to pivot toward immersion and direct-to-chip cooling. A major campus upgrade showcases this shift, featuring chilled-water and liquid-cooling loops designed for 27 °C set-points. High-density deployment elongates cable runs and upsizes busways, which increases bill-of-materials value yet lengthens commissioning time by 15-20%. Developers respond by adopting rear-door heat exchangers and medium-voltage (22 kV) power distribution to reduce copper usage. As AI inferencing proliferates across finance, healthcare, and public-sector workloads, construction pipelines increasingly bundle specialized white space for GPU pods, helping the Singapore data center construction market sustain double-digit project count growth despite the national power cap.

Singapore's power-allocation ceiling, reinstated in 2024 after a three-year moratorium, falls below regional demand growth, stalling many planned hyperscale builds. Developers must compete in a Call-for-Application process whose scoring heavily weights PUE and carbon intensity, inflating pre-construction consultancy fees. The scarcity of megawatts drove some operators to shift incremental capacity to Batam or Johor, dampening the full revenue potential of the Singapore data center construction market. Long-term uncertainty also complicates transformer and generator ordering cycles, with lead times already stretched by global supply constraints. Together, these factors shave an estimated 1.4 percentage points from forecast CAGR.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The electrical package accounted for 37.38% of overall spend within the Singapore data center construction market in 2025, reflecting hyperscaler preference for 22 kV feeds, intelligent switchgear, and high-capacity busways designed for GPU racks running at 50 kW and above. Liquid-based cooling, though still a subset of mechanical infrastructure, is the fastest-growing line item and will contribute USD 628.5 million to the Singapore data center construction market size by 2031. Adoption of immersion tanks and rear-door heat exchangers reduces white-space real estate per rack, enabling higher revenue density for colocation operators. Services such as design-build integration and commissioning enjoy premium billing rates because owners demand turnkey validation of PUE targets. Over the forecast window, integration between electrics and controls will deepen as AI-driven optimization platforms require real-time telemetry from both power and cooling loops. This convergence elevates the strategic value of firms that can span electrical and mechanical scopes in a single contract, cementing their competitive position within the Singapore data center construction market.

The mechanical segment is evolving from traditional chillers toward pumped refrigerant and dielectric immersion systems capable of dissipating 1,200 W per chip. A joint program cut cooling energy by 29%, saving roughly USD 25,000 per rack annually and setting a cost-avoidance benchmark other operators now target. General construction remains a steady contributor driven by multi-story shells, seismic reinforcement, and blast-resistant facades required under Singapore's stringent codes. IT infrastructure-racks, network fabric, and cable management-captures incremental spend as high-density layouts demand thicker fiber trunks and AI-optimized topologies. Collectively, these shifts underscore how rising workload complexity expands wallet share for specialized subcontractors in the Singapore data center construction market.

Tier III facilities delivered 53.22% of the Singapore data center construction market share in 2025 thanks to their balanced cost-reliability proposition and 99.982% uptime guarantee. Enterprises and cloud providers value concurrently maintainable infrastructure that supports live upgrades without the doubled capex of 2N systems. Nevertheless, Tier IV pipelines are expanding at 5.03% CAGR, fueled by fintech, trading desks, and sovereign-cloud workloads that demand 99.995% availability. These fault-tolerant sites typically deploy 2N UPS, dual fuel farms, and independent chilled-water plants, doubling MEP scope relative to Tier III and lifting the Singapore data center construction market size for high-tier builds.

Iron Mountain's Singapore facility typifies Tier IV attributes with three geographically diverse meet-me-rooms and bio-protected access corridors. Although Tier I and II projects persist in edge or telco applications, their contribution to revenue remains marginal. Over time, regulatory and customer pressure for resilience is expected to pull Tier III specifications closer to Tier IV, blurring distinctions and increasing the baseline spend per megawatt across the Singapore data center construction market.

The Singapore Data Center Construction Market is Segmented by Infrastructure (Electrical Infrastructure, Mechanical Infrastructure, and More), Tier Standard (Tier I and II, Tier III, and More), Data Center Type (Colocation, Hyperscale, and More), End User Industry (Banking, Financial Services, Insurance, IT and Telecommunications, and More). The Market Forecasts are Provided in Terms of Value (USD).