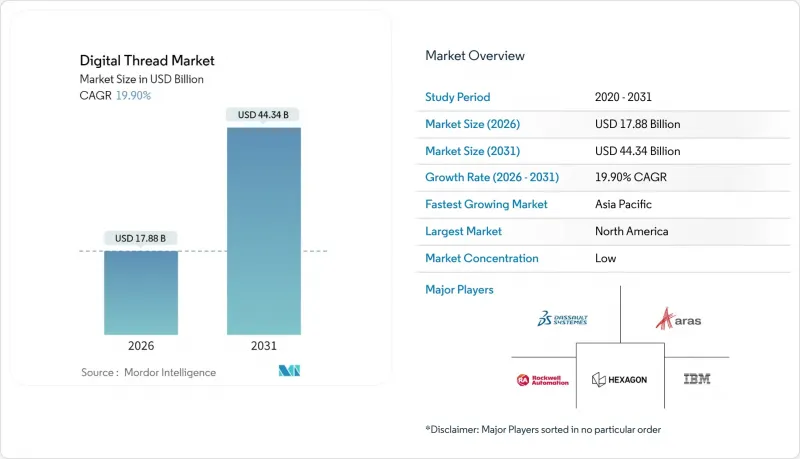

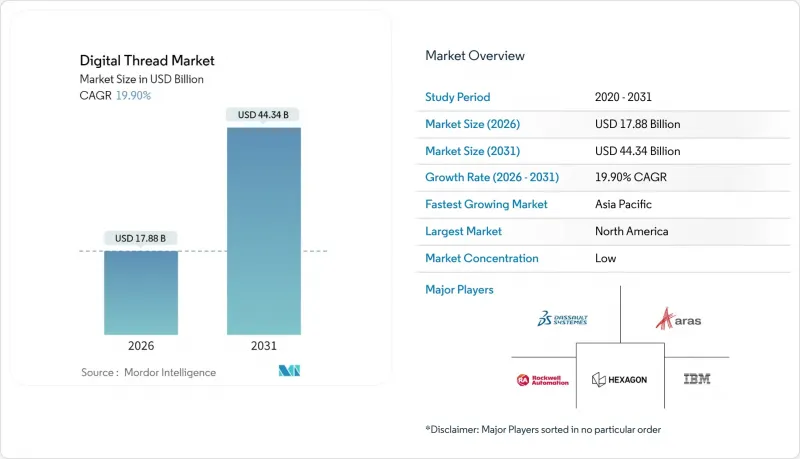

디지털 스레드 시장 규모는 2026년에는 178억 8,000만 달러로 추정되고 있으며, 2025년 149억 1,000만 달러에서 성장이 전망됩니다.

2031년까지의 예측에서는 443억 4,000만 달러에 달하며, 2026-2031년에 CAGR 19.9%로 성장할 것으로 전망되고 있습니다.

설계, 생산, 서비스 전반에 걸친 단일하고 지속적인 데이터 흐름을 통해 제조업체가 설계 의도와 실시간 운영을 연계할 수 있도록 하는 수요가 증가하고 있습니다. 클라우드 네이티브 제품수명주기관리 플랫폼은 IT 비용을 절감하면서 상시 가동되는 협업 환경을 구축합니다. 저비용 IIoT 센서가 시뮬레이션 모델에 상세한 현장 데이터를 제공함으로써 엔지니어는 가상 자산과 물리적 자산의 연계를 강화할 수 있습니다. 생성형 AI는 CAD 모델 자동 주석을 통해 설계 주기를 더욱 단축하고, 지속가능성 규제로 인해 전과정 탄소 추적의 필요성이 증가하고 있습니다. 사이버 공격 위험은 연결된 생산 라인을 보호하는 보안 아키텍처에 대한 병행 추진 요인이 되고 있습니다.

클라우드 플랫폼은 설계, 실행, 서비스 데이터를 통합하는 API 퍼스트 환경으로 On-Premise의 사일로화를 해소합니다. Aras는 지역별 호스팅이 데이터 주권 규정을 준수하면서 전 세계 팀에게 안전한 공유 워크스페이스를 제공하는 사례를 보여주고 있습니다. PTC의 클라우드 배포으로 의료기기 시장 출시 기간을 40% 단축하여 구체적인 재무적 이익을 입증했습니다. 업그레이드 비용 절감으로 디지털 스레드의 가치를 확장하는 시뮬레이션 및 분석 모듈에 예산을 배분할 수 있습니다. 그러나 유럽 기업은 GDPR(EU 개인정보보호규정)의 엄격한 요구 사항에 직면하고 있으며, 벤더 종속성에 대한 우려로 인해 최종 구매 결정이 늦어지고 있습니다.

센서의 평균 가격은 0.38달러까지 떨어졌고, 대량 생산은 공장에서 모든 자산을 측정할 수 있는 중요한 0.30달러를 향해 빠르게 진행되고 있습니다. 아시아태평양 공장의 44%가 12개월 이내에 스마트 제조를 도입할 계획이며, 이는 미국의 계획보다 10% 포인트 더 높은 수치입니다. 저렴한 센서와 엣지 게이트웨이가 실시간 지표를 디지털 트윈에 공급함으로써 품질 개입에 대한 대응 시간을 단축하고 폐기율을 낮춥니다. 하드웨어 비용이 감소함에 따라 소프트웨어 구독 및 사이버 보안 툴이 프로젝트 총 예산에서 더 큰 비중을 차지하게 되었습니다.

2030년까지 200만 개의 제조업 일자리가 미충원될 가능성이 있으며, 현재 노동력의 3분의 1이 디지털 기술이 부족합니다. 중소기업은 대기업의 급여 수준을 따라잡지 못하고, 첨단 PLM 모듈 도입이 늦어지고 있습니다. 커뮤니티 칼리지에서는 MBSE(모델 기반 시스템 엔지니어링) 과정을 추가하고 있지만, 졸업생이 현장에 배치되기까지 4년이 걸립니다. AI를 통한 설계 보조는 도입이 용이하지만, 오너가 운영하는 공장에서는 여전히 문화 변화가 장벽으로 작용하고 있습니다.

2025년 기준 PLM은 디지털 스레드 시장의 27.80%를 차지하며 기업 디지털 전략의 근간을 이루고 있습니다. 기업이 설계 데이터와 실행 데이터를 연계함에 따라 PLM 중심 스택의 디지털 스레드 시장 규모는 꾸준히 확대될 것으로 예측됩니다. 그러나 ALM의 CAGR 21.7%는 코드와 하드웨어의 긴밀한 동기화를 필요로 하는 소프트웨어 정의 제품으로의 전환을 시사합니다. 생성형 AI는 텍스트 프롬프트를 파라메트릭 모델로 변환하여 추진력을 더하며, Triebwerk에 따르면 초기 설계 작업을 70%까지 줄일 수 있다고 합니다. CAD 및 CAM 부문은 AI 플러그인이 설계 오류를 조기에 감지하여 완만하지만 꾸준한 성장세를 보이고 있으며, SLM은 애프터세일즈 컴플라이언스가 까다로운 항공우주 및 의료 분야에서 성장세를 보이고 있습니다. ERP 및 MRP 제품군은 현재 운영 트랜잭션과 설계 변경 지시서를 연계하는 오픈 API를 공개하여 기존 PLM의 틀을 넘어 디지털 스레드 시장의 확장을 촉진하고 있습니다. 다른 시뮬레이션 및 분석 툴들도 이러한 통합의 물결에 편승하여 엔지니어에게 유한 요소 모델에서 현장 센서의 피드백까지 한 화면에서 관리할 수 있는 환경을 제공합니다.

기업은 단품 솔루션 구매보다는 여러 모듈을 통합한 플랫폼 벤더를 선택하는 경향이 강해지고 있습니다. 지멘스, PTC, 다쏘시스템은 임베디드 시뮬레이션 엔진과 규제 대상 사용자에 가까운 클라우드 영역을 강점으로 내세우고 있지만, 종량제 클라우드 전용 스택을 제공하는 새로운 경쟁사들과 맞서야 하는 상황입니다. 고객사들이 자체 사양에 의한 락인(lock-in)에 저항하는 가운데, 개방형 표준 데이터 포맷이 더 많은 로드맵에 채택될 것으로 예측됩니다. 경쟁 환경의 동향은 PLM 매출은 안정화되는 반면, 노동 집약적인 작업을 자동화하는 AI 강화 모듈의 확대가 가속화되고 있으며, 디지털 스레드 시장내 지출의 재분배가 점차 진행되고 있음을 시사합니다.

클라우드는 수년간의 SaaS 보급 활동을 통해 2025년 53.85%의 점유율을 차지할 것으로 예상되며, 많은 중소기업이 완전 호스팅 환경에서 디지털 스레드를 도입하기 시작했습니다. 주요 프라임 기업은 기밀성이 높은 지적 재산을 사내에 보관하기 위해 하이브리드형과 타협하여 20.6%의 연평균 복합 성장률(CAGR)로 성장하고 있습니다. 하이브리드 도입과 관련된 디지털 스레드 시장 규모는 기업이 레거시 장비, 지연 요건, 수출 관리 규정을 모두 충족시키면서 2031년까지 거의 3배로 확대될 것으로 예측됩니다. 방산 관련 기업은 FedRAMP 고보장 지역을 협업 기반으로 삼으면서도 미국 국제무기거래규제(ITAR) 대응을 위해 코어 리포지토리를 방화벽 뒤에 미러링하고 있습니다. 유럽에서는 GDPR(EU 개인정보보호규정)의 엄격한 거주지 조항으로 인해 듀얼 스택 배포가 운영 표준이 되었습니다.

제조업체들이 단순한 파일 복제에서 마이크로서비스 오케스트레이션으로 전환함에 따라 하이브리드 도입 패턴이 성숙해지고 있습니다. 클라우드 계층은 시뮬레이션의 버스트 처리와 AI 추론을 담당하고, 생산 이력 시스템은 밀리초 단위의 피드백을 실현하기 위해 로컬 데이터센터에 배치됩니다. 각 벤더들은 두 환경에서 동일하게 동작하는 컨테이너화 서비스를 제공함으로써 업데이트 주기를 간소화했습니다. On-Premise 구축은 소프트웨어 변경 인증이 필수적인 원자력, 제약 및 중요 인프라 사업자에게 여전히 중요하며, 성장이 둔화되고 있지만 기능 로드맵에 계속 영향을 미치고 있으며, 에어갭 환경을 위한 기능이 주류 제품의 일부로 유지될 수 있도록 보장합니다.

북미의 현재 우위는 항공우주 분야 주요 기업, 국방 예산, 실리콘밸리의 소프트웨어 파트너십에 기인합니다. 디지털 엔지니어링의 요구에 따라 엔드투엔드 데이터 연속성 프로젝트에 대한 투자가 촉진되고 있으며, 클라우드 하이퍼스케일러는 엄격한 보안 요건을 충족하는 FedRAMP 지원 지역을 운영하고 있습니다. 캐나다에서는 미국 항공기 제조업체와의 공통 공급망으로 인해 유사한 관행이 북쪽으로 확산되고 있으며, 멕시코에서는 신흥 항공우주단지가 신규 계약 체결을 위해 디지털 스레드를 도입하고 있습니다. 노동력 부족이 현실적인 제약이 되는 한편, AI 강화 설계 툴이 생산성 저하를 완화하고 있습니다.

아시아태평양은 다른 지역을 능가하는 속도로 발전하고 있습니다. 중국 정부는 IIoT, AI, 첨단 로봇을 통합한 파일럿 라인에 자금을 지원하여 현지 OEM(Original Equipment Manufacturer)에 비용과 속도면에서 우위를 제공합니다. 일본의 전자제품 제조업체들도 비슷한 원칙을 적용하여 세계 품질 리더십을 유지하고 있습니다. 국내 조선소는 디지털 트윈을 활용하여 선체 응력 예측 및 유지보수 계획을 수립하고 있습니다. 인도는 저비용 센서와 클라우드 데이터센터를 결합하여 중소기업이 기존 MES 아키텍처를 뛰어넘을 수 있도록 지원하고 있습니다. 아세안 지역내에서는 전자기기 및 의료기기 수출기업이 디지털 스레드 플랫폼을 도입하여 유럽 및 미국 고객공급업체 감사를 통과하고 있습니다.

유럽에서는 탄소 보고 의무를 이동하기 위해 디지털 스레드를 활용하고 있습니다. 독일 기계 제조업체는 모든 자산 기록에 에너지 소비 지표를 통합하고 있습니다. 프랑스 항공우주 공급업체는 복합재료 데이터와 부품 여권을 상호 연계하여 규정 준수를 실현하고 있습니다. 이탈리아의 자동차 부품 클러스터는 1등급 공급업체로서의 지위를 유지하기 위해 추적 가능성에 초점을 맞추었습니다. GDPR(EU 개인정보보호규정)(일반 데이터 보호 규정)은 멀티 인스턴스 클라우드 설계를 촉진하고, 하이브리드 구축에 대한 수요를 증가시키고 있습니다. 동시에, EU의 탄소 국경 조정 조치로 인해 검증된 수명주기 데이터가 부족한 수입품은 곧 과징금 부과 대상이 될 것이며, 전 세계 파트너를 호환 가능한 플랫폼으로 전환할 것으로 예측됩니다.

digital thread market size in 2026 is estimated at USD 17.88 billion, growing from 2025 value of USD 14.91 billion with 2031 projections showing USD 44.34 billion, growing at 19.9% CAGR over 2026-2031.

Demand rises as manufacturers link engineering intent with real-time operations through a single, persistent data flow that spans design, production, and service. Cloud-native product lifecycle management platforms cut IT overhead while creating always-on collaboration environments. Cheaper IIoT sensors feed granular shop-floor data into simulation models, letting engineers close the loop between virtual and physical assets. Generative AI further trims design cycles by auto-annotating computer-aided models, and sustainability regulations intensify the need for lifecycle carbon tracking. Cyber-attack risks add a parallel push toward secure architectures that guard connected production lines.

Cloud platforms replace on-premises silos with API-first environments that unite design, execution, and service data. Aras shows how regional hosting satisfies data-sovereignty rules while giving global teams a secure shared workspace. PTC's cloud deployment cuts medical-device time to market by 40%, proving tangible financial benefit. Lower upgrade costs free budgets for simulation and analytics modules that extend digital thread value. Yet European firms face tougher GDPR hurdles, and the fear of vendor lock-in slows final purchase decisions.

Average sensor pricing has dropped to USD 0.38, with volume production racing toward the pivotal USD 0.30 mark that lets factories instrument every asset. Forty-four percent of Asia-Pacific plants plan smart-manufacturing rollouts within 12 months, eclipsing U.S. intent by 10 percentage points. Cheap sensors plus edge gateways feed real-time metrics into digital twins, cutting response times for quality interventions and shrinking scrap rates. As hardware costs fall, software subscriptions and cybersecurity tools become the larger share of total project budgets.

Two million manufacturing positions may stay vacant by 2030, and one-third of today's workforce lacks digital skills. Small firms cannot match enterprise salaries, so they lag in adopting advanced PLM modules. Community colleges add MBSE courses, but four years must pass before graduates fill shop floors. AI-guided design assistants ease onboarding, yet culture change remains a stumbling block for many owner-managed plants.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

PLM commanded 27.80% of the digital thread market in 2025 and remains the backbone of enterprise digital strategies. The digital thread market size for PLM-centric stacks is projected to climb steadily as companies connect design vaults with execution data. However, ALM's 21.7% CAGR signals a pivot toward software-defined products that demand tighter code-hardware synchronization. Generative AI adds fuel by turning text prompts into parametric models, slashing initial design work by 70% according to Triebwerk. CAD and CAM segments show modest but consistent growth as AI plug-ins surface design errors early, while SLM picks up momentum in aerospace and healthcare, where after-sales compliance is strict. ERP and MRP suites now publish open APIs that join operational transactions with engineering change orders, expanding the addressable digital thread market beyond traditional PLM boundaries. Other simulation and analytics tools ride this integration wave, giving engineers a single pane of glass that stretches from finite-element models to field sensor feedback.

Enterprises increasingly choose platform vendors that fuse multiple modules rather than buying point solutions. Siemens, PTC, and Dassault lean on embedded simulation engines and cloud regions near regulated users, yet face new rivals who launch cloud-only stacks with consumption billing. Open-standard data formats appear on more roadmaps as customers push back against proprietary lock-ins. The competitive narrative suggests steady PLM revenue but faster expansion for AI-augmented modules that automate labor-intensive tasks, indicating a gradual redistribution of spending within the digital thread market.

Cloud held a 53.85% share in 2025 after years of software-as-a-service evangelism, and many SMEs began their digital thread journey in fully hosted environments. Large primes keep sensitive IP on site, driving hybrid's 20.6% CAGR as the preferred compromise. The digital thread market size associated with hybrid rollouts will nearly triple by 2031 as firms juggle legacy gear, latency demands, and export-control rules. Defense contractors rely on FedRAMP high-assurance regions for collaboration, yet mirror core repositories behind firewalls to meet U.S. International Traffic in Arms Regulations. In Europe, GDPR's strict residency clauses make dual-stack deployments an operational norm.

Hybrid adoption patterns mature as manufacturers shift from simple file replication to microservice orchestration. Cloud tiers now handle simulation bursts and AI inference, while production historians reside in local data centers for millisecond feedback. Vendors have responded with containerized services that run identically in both locations, simplifying update cycles. On-premises deployments remain relevant for nuclear, pharmaceutical, and critical-infrastructure operators who must certify every software change. Although their growth lags, they continue to influence feature roadmaps, ensuring that air-gapped functionality remains part of mainstream offerings.

The Digital Thread Market Report is Segmented by Technology (PLM, CAD, CAM, SLM, ALM, and More), Deployment Mode (Cloud, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium-Sized Enterprises), Industry Vertical (Aerospace and Defense, Automotive and Transportation, Industrial Machinery, Healthcare and Medical Devices, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America's current dominance stems from entrenched aerospace primes, defense budgets, and Silicon Valley software partnerships. Digital engineering mandates funnel investment into end-to-end data continuity projects, and cloud hyperscalers operate FedRAMP regions that satisfy strict security needs. Canada's shared supply chain with U.S. airframe builders spreads similar practices northward, while Mexico's rising aerospace parks embrace digital threads to win new contracts. Labor shortages pose a real constraint, yet AI-augmented design tools moderate the productivity hit.

Asia-Pacific advances faster than any other bloc. China's government funds pilot lines that integrate IIoT, AI, and advanced robotics, giving local OEMs cost and speed advantages. Japanese electronics makers apply the same principles to keep global quality leadership. South Korea's shipyards use digital twins to predict hull stress and schedule maintenance. India combines low sensor costs with cloud datacenters to let SMEs leapfrog older MES architectures. Across ASEAN, electronics and medical-device exporters adopt digital thread platforms to pass supplier audits from Western customers.

Europe relies on digital threads to meet carbon-reporting duties. German machine builders embed energy-consumption metrics in every asset record. French aerospace suppliers interlink composite material data with component passports for regulatory compliance. Italy's automotive parts clusters focus on traceability to maintain Tier-1 status. GDPR forces multi-instance cloud designs, boosting demand for hybrid deployments. In parallel, EU carbon border adjustments will soon penalize imports lacking verified lifecycle data, nudging global partners onto compatible platforms.