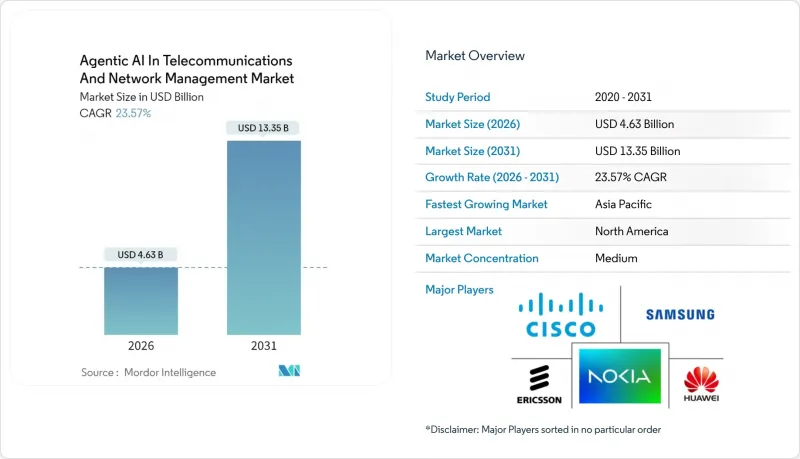

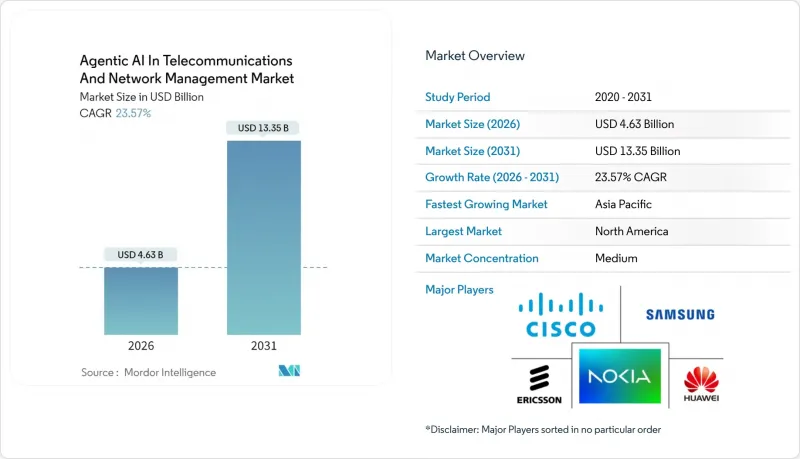

통신 및 네트워크 관리용 에이전트형 AI 시장은 2025년 37억 5,000만 달러에서 2026년에는 46억 3,000만 달러로 성장하여 2026년부터 2031년까지 CAGR 23.57%를 기록하며 2031년까지 133억 5,000만 달러에 달할 것으로 예측됩니다.

통신사들은 자율적인 오케스트레이션을 우선시하고 있습니다. 5G와 새롭게 부상하는 6G 네트워크는 기존의 규칙 기반 시스템으로는 관리할 수 없는 수백만 개의 변수에 대한 실시간 최적화가 필요하기 때문입니다. 클라우드 네이티브 플랫폼이 초기 도입의 기반이 되었지만, 추론 지연을 줄이기 위해 엣지 및 멀티 액세스 엣지 컴퓨팅(MEC)으로의 빠른 전환이 진행되고 있습니다. 공격자들이 AI를 도입하면서 부정행위와 보안 관리가 특히 주목받고 있으며, 통신사들은 각 계층에 지능형 이상 징후 탐지 기능을 통합해야 할 필요성이 대두되고 있습니다. 네트워크 장비 업체, 하이퍼스케일러, AI 전문 업체들이 오픈 인터페이스와 빠른 혁신 주기를 약속하는 멀티 벤더 연합을 형성하면서 경쟁이 치열해지고 있습니다. 광섬유와 사이버 보안 분야의 전략적 합병은 통합된 연결성과 AI 보안이 시장 지위를 지키기 위한 필수 조건이 될 미래를 암시합니다.

안테나 수, 주파수 대역, 서비스 수준 요구사항이 급증함에 따라 수동 최적화가 현실적으로 불가능해짐에 따라, 통신사업자들은 네트워크의 의도를 학습하고 지속적으로 실행하는 자율 에이전트를 구축해야 합니다. Digital Nasional Berhad는 에릭슨 인텐션 기반 플랫폼 도입 후 6개월 만에 가동률 99.8%, 알람 500% 감소를 달성했습니다. 6G 관련 연구에 따르면, 비지상파 링크가 지상파 셀에 통합되면 오케스트레이션의 부담이 두 배로 증가하여 비즈니스 사례가 강화될 것으로 보입니다. 노키아의 모델링에 따르면, 자율 네트워크는 설비투자(CAPEX), 운영비용(OPEX), 수익 효과를 결합하여 통신사업자에게 연간 8억 달러의 이익을 가져다 줄 수 있다고 합니다. 이러한 경제성은 개념증명(PoC)을 대규모 실사용 배포로 전환하는 이사회 차원의 시급성을 높이고 있습니다.

실시간 동영상과 AI 워크로드로 인한 시간당 트래픽 폭증은 기존의 계획 주기를 압도하고 있습니다. 버라이즌이 도입한 무선 지능형 컨트롤러는 트래픽이 급증하기 전에 용량을 이동시켜 15%의 에너지 절감을 실현하고 있습니다. 통신사업자의 보고에 따르면, 예측형 에이전트를 통한 사전 리소스 할당은 사후 대응 방식에 비해 혼잡 이벤트를 30-50% 감소시키는 것으로 나타났습니다. 엣지 데이터센터에서는 추론 부하가 갑작스럽고 국지적으로 발생하기 때문에 이 문제는 더욱 심각해집니다. 결과적으로 사용자 경험과 기업의 SLA(서비스 수준 계약)를 보호하기 위해 예측 최적화는 더 이상 선택이 아닌 필수적인 조치로 자리 잡았습니다.

GDPR과 곧 시행될 EU AI 법규로 인해 통신사업자는 설명가능성 계층과 엄격한 데이터 현지화 관리를 추가해야 하며, 이는 프로젝트 타임라인을 연장할 수밖에 없습니다. 페더레이티드 러닝은 컴플라이언스를 실현하지만, 컴퓨팅 비용을 3배로 증가시킬 수 있습니다. 국경을 넘나드는 사업자는 규모의 경제를 해치는 서로 다른 프레임워크를 조정해야 합니다. 이러한 불확실성으로 인해 단계적 도입과 감사 대응을 보장하는 하이퍼스케일러의 프라이버시 보호 툴킷에 대한 의존도가 높아지고 있습니다.

2025년 지출의 59.65%는 솔루션과 플랫폼이 차지했습니다. 이는 통신사업자가 기존 OSS/BSS에 연결할 수 있는 턴키 기능을 요구했기 때문입니다. 서비스는 커스터마이징 작업 흐름으로 인해 통신 및 네트워크 관리 분야의 에이전트형 AI 시장 전체보다 26.99%의 CAGR로 확대될 것으로 예측됩니다. 기존 네트워크(브라운필드)는 영역 특화형 조정이 필요하기 때문에 통신-네트워크 관리에서 에이전트형 AI의 서비스 시장 규모는 빠르게 확대될 것으로 예상됩니다. 통합 전문가는 데이터 파이프라인 조정, 도메인 모델 개발, 라이프사이클 거버넌스를 담당하지만, 이러한 기능을 사내에 보유하고 있는 통신사는 많지 않습니다. 또한, 변화하는 비즈니스 KPI에 AI 에이전트를 지속적으로 적응시키는 관리형 최적화 서비스도 제공합니다. 따라서 전문 서비스 수익은 AI 성숙도 단계와 연동하여 증가하며, 통신 사업자의 운영에 프로바이더를 깊숙이 통합하고 지속적인 수익원을 창출하여 시장 전체에 대한 가시성을 높입니다.

통신 및 네트워크 관리 분야의 에이전트형 AI 시장은 플랫폼 벤더와 서비스 파트너 간의 공생 사이클의 혜택을 누리고 있습니다. 플랫폼이 성숙해짐에 따라 세분화된 API가 공개되고, 서드파티 모듈의 개발이 촉진될 것입니다. 이는 통합 및 데브옵스 인력에 대한 수요를 촉진하는 선순환 구조를 만들어냅니다. 이러한 선순환은 혁신의 속도를 가속화하는 동시에 사업자가 슬림한 내부 팀을 유지할 수 있게 해줍니다. 그 결과, 서비스는 솔루션과의 수익 격차를 줄이는 것이 아니라 2031년까지 전체 컴포넌트 스택에서 균형 잡힌 성장을 보장합니다.

2025년 기준 클라우드 구축이 57.62%의 점유율을 유지했습니다. 이는 하이퍼스케일러가 거대 모델 트레이닝을 위한 탄력적인 컴퓨팅 자원을 제공하기 때문입니다. 그러나 자율주행차, 산업 자동화 등 한 자릿수 밀리초 단위의 응답이 요구되는 사용 사례가 증가함에 따라 MEC(엣지 컴퓨팅) 인스턴스는 26.02%의 CAGR로 확대될 것으로 예상됩니다. 통신 및 네트워크 관리 분야에서 에이전트형 AI의 엣지 시장 점유율은 사업자들이 기지국 사이트 전체에 마이크로 데이터센터 설치 기준을 통일하는 시점에 급상승할 것으로 예상됩니다. 선행 도입 사업자들은 추론 처리를 로컬로 유지함으로써 15%의 에너지 절감 효과와 백홀 부하 감소를 보고하고 있습니다. 클라우드 상의 정책 엔진이 학습을 조정하는 한편, 에지 측에서 의사결정 루프를 축소하고 하이브리드 토폴로지를 강화합니다.

특히, 엄격한 주권 규제를 가진 사업자들은 국내에 설치된 온프레미스형 클라우드에 의존하여 컴플라이언스를 유지하면서 하이퍼스케일 수준의 운영을 실현하고 있습니다. 클라우드, 엣지, 온프레미스의 혼합된 형태는 라이프사이클 관리를 복잡하게 만들고, 모델의 일관성을 보장하는 오케스트레이션 벤더가 진입할 수 있는 여지를 만들어내고 있습니다. 우승자가 될 솔루션은 위치의 복잡성을 추상화하고, 지연 시간이나 보안을 손상시키지 않으면서도 전체 페더레이션 계층에 단일 제어 플레인을 제공하는 솔루션이 될 것입니다.

북미는 5G의 보급, 풍부한 벤처 캐피탈, 실험을 장려하는 명확한 규제 정책으로 인해 2025년에도 38.34%의 매출 점유율을 유지했습니다. Verizon과 T-Mobile은 Google 및 NVIDIA와 협력하여 최적화 엔진을 공동 개발하고 있으며, 이를 통해 이미 판매 전환율을 40% 향상시키고 에너지 비용도 절감하고 있습니다. 이 지역은 통신 분야 AI 특허 출원의 대부분을 차지하고 있으며, 현지 벤더는 지적재산권 측면에서 우위를 점하고 있어 해외 라이선싱 시에도 그 강점이 발휘됩니다. 지방의 엣지 클라우드에 대한 정부 지원 프로그램으로 대상 사이트가 더욱 확대되고, 구축 속도가 빨라지고 있습니다.

아시아태평양은 2031년까지 CAGR 25.78%를 기록하며 가장 빠르게 성장하는 시장이 될 것으로 예상됩니다. 중국에서는 국가 주도의 투자로 전국적인 5G망 구축이 보장되고, 통신사업자의 요구에 부합하는 첨단 AI 연구소가 설립되고 있습니다. 한국의 주요 통신사들은 2024년부터 2025년까지 신흥 알고리즘에 대한 독점적 접근권을 확보하기 위해 AI 스타트업에 2억 1,000만 달러 이상을 투자했습니다. 인도에서는 스마트폰 보급이 급증하는 가운데, 방대한 주파수 대역을 구매하지 않고도 밀집된 도시 지역에 대응하기 위해 AI 기반의 스펙트럼 효율성이 요구되고 있습니다. 세계 및 텔레콤 AI 얼라이언스 등 지역적 협력을 통해 검증된 프레임워크가 국경을 넘어 확산되고 도입 주기가 단축되고 있습니다.

유럽은 지출 규모에서 3위를 차지했지만, GDPR 준수로 인해 연합학습 채택이 촉진되면서 프라이버시 보호 혁신에서 1위를 차지했습니다. 통신사들은 설명 가능한 에이전트를 프로덕션 환경에서 운영하기 전에 시범운영을 하는 경우가 많으며, 타임라인은 길어지지만 신뢰를 쌓아가고 있습니다. 남미에서는 설비투자의 급증을 피하기 위해 매니지드 서비스를 통해 제공되는 비용 효율적인 AI를 선호합니다. 한편, 중동 및 아프리카에서는 치솟는 전력 비용을 상쇄하기 위해 AI를 활용한 에너지 최적화를 추구하고 있습니다. 이들 시장은 전반적으로 다양한 진입 경로를 보여 주며, 세계 공급업체들이 지역적 제약에 맞게 포트폴리오를 조정할 수 있도록 보장합니다.

The Agentic AI in Telecommunications and Network Management market is expected to grow from USD 3.75 billion in 2025 to USD 4.63 billion in 2026 and is forecast to reach USD 13.35 billion by 2031 at 23.57% CAGR over 2026-2031.

Operators are prioritizing autonomous orchestration because 5G and emerging 6G networks require real-time optimization across millions of variables that conventional rule-based systems cannot manage. Cloud-native platforms anchor early deployments, yet rapid migration toward edge and multi-access edge computing (MEC) is underway to shave inference latency. Fraud and security management is enjoying outsized attention as adversaries adopt AI, pushing operators to embed intelligent anomaly detection at every layer. Competitive intensity is rising as network equipment makers, hyperscalers, and AI specialists form multi-vendor coalitions that promise open interfaces and faster innovation cycles. Strategic mergers in fibre and cybersecurity hint at a future where integrated connectivity and AI security become table stakes for defending market positions.

Escalating antenna counts, spectrum bands, and service-level requirements make manual optimisation unworkable, prompting operators to embed autonomous agents that learn network intent and enforce it continuously. Digital Nasional Berhad achieved 99.8% uptime and a 500% alarm reduction within six months of adopting Ericsson's intent-based platform. Research for 6G suggests the orchestration burden will multiply as non-terrestrial links join terrestrial cells, reinforcing the business case. Nokia's modelling shows autonomous networks can unlock USD 800 million in annual operator benefits through combined CAPEX, OPEX, and revenue effects. Those economics drive board-level urgency to convert proof-of-concepts into production deployments at scale.

Hourly traffic spikes fuelled by live video and AI workloads now overwhelm conventional planning cycles. Verizon's deployment of radio-intelligent controllers delivers 15% energy savings by shifting capacity ahead of surges. Operators report 30-50% reductions in congestion events when predictive agents pre-allocate resources versus reactive steps. Edge data centres intensify the challenge because inference loads appear suddenly and locally. Consequently, predictive optimisation is no longer optional for safeguarding user experience and enterprise SLA commitments.

GDPR and impending EU AI Act rules force operators to add explainability layers and strict data-localisation controls that stretch project timelines. Federated learning offers compliance but can triple compute costs. Cross-border operators must juggle divergent frameworks that undercut scale economies. The uncertainty prompts phased deployments and higher dependence on privacy-preserving toolkits from hyperscalers that guarantee audit readiness.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Solutions and platforms accounted for 59.65% of 2025 spending as operators sought turnkey functionality that plugs into existing OSS/BSS. Services are projected to expand at a 26.99% CAGR, outpacing the overall Agentic AI in Telecommunications and Network Management market due to customisation workstreams. The Agentic AI in Telecommunications and Network Management market size for services is forecast to widen quickly as brownfield networks require domain-specific tuning. Integration specialists orchestrate data pipelines, develop domain models, and handle lifecycle governance, functions that many operators lack in-house. They also deliver managed optimisation that continuously aligns AI agents with shifting business KPIs. Professional services revenue, therefore, rises in tandem with AI maturity phases, embedding providers deep within operator operations and creating annuity streams that lift overall market visibility.

The Agentic AI in Telecommunications and Network Management market benefits from a symbiotic cycle between platform vendors and service partners. As platforms mature, they expose granular APIs that foster third-party modules, which in turn spur demand for integration and DevOps talent. This virtuous loop accelerates innovation velocity while allowing operators to maintain lean internal teams. Consequently, services will narrow but not erase the revenue gap with solutions, ensuring balanced growth across the component stack through 2031.

Cloud deployments retained a 57.62% share in 2025 because hyperscalers supply elastic compute for training massive models. However, MEC instances are set to post a 26.02% CAGR as use cases, such as autonomous vehicles and industrial automation, demand single-digit millisecond responses. The Agentic AI in Telecommunications and Network Management market share for edge is expected to rise sharply once operators standardise micro-data-centre footprints across base-station sites. Early adopters cite 15% energy savings and reduced backhaul when inference stays local. Policy engines in the cloud still coordinate learning, yet decision loops shrink at the edge, reinforcing a hybrid topography.

Notably, operators with stringent sovereignty rules rely on on-premises clouds inside national borders, preserving compliance while retaining hyperscale-like operations. This blend of cloud, edge, and on-premises outposts complicates lifecycle management, creating room for orchestration vendors that guarantee model consistency. Winning solutions will abstract location complexity, providing a single control plane across federation layers without compromising latency or security.

Agentic AI in Telecommunications and Network Management Market Report is Segmented by Component (Solutions/Platforms and Services), Deployment Mode (Cloud and More), Application (Customer Analytics and More), Network Domain (Core Network, Radio Access Network, and More), AI Technology (Machine Learning, Natural Language Processing, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America retained 38.34% revenue share in 2025 owing to pervasive 5G, deep venture capital, and clear regulatory signals that reward experimentation. Verizon and T-Mobile partner with Google and NVIDIA to co-create optimisation engines that have already lifted sales conversions by 40% and trimmed energy bills. The region also commands the lion's share of AI patent filings in telecoms, giving local vendors an intellectual-property edge that travels well when licensing abroad. Government funding programmes that subsidise rural edge clouds further expand addressable sites, accelerating rollout velocity.

Asia-Pacific is projected to post a 25.78% CAGR to 2031, making it the fastest-expanding theatre. China's state-backed investments guarantee nationwide 5G coverage and seed advanced AI research labs that dovetail with operator needs. South Korea's leading telcos invested over USD 210 million in AI start-ups during 2024-2025 to secure exclusive access to emerging algorithms. India, propelled by surging smartphone adoption, demands AI-based spectral efficiency to serve dense urban clusters without exhaustive spectrum purchases. Regional collaborations, such as the Global Telco AI Alliance, spread proven frameworks across borders, compressing deployment cycles.

Europe ranks third in spending but first in privacy-preserving innovation as GDPR compliance drives adoption of federated learning. Operators often pilot explainable agents before turning them loose in production, lengthening timelines yet fostering trust. South America favours cost-efficient AI delivered via managed services to sidestep capex spikes, while the Middle East and Africa pursue AI-enabled energy optimisation to offset high power costs. Collectively, these markets demonstrate diverse entry paths, ensuring global suppliers tailor portfolios to local constraints.