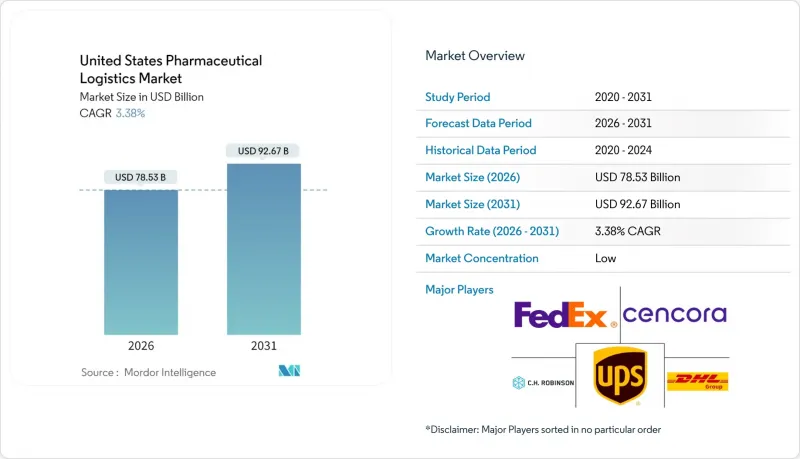

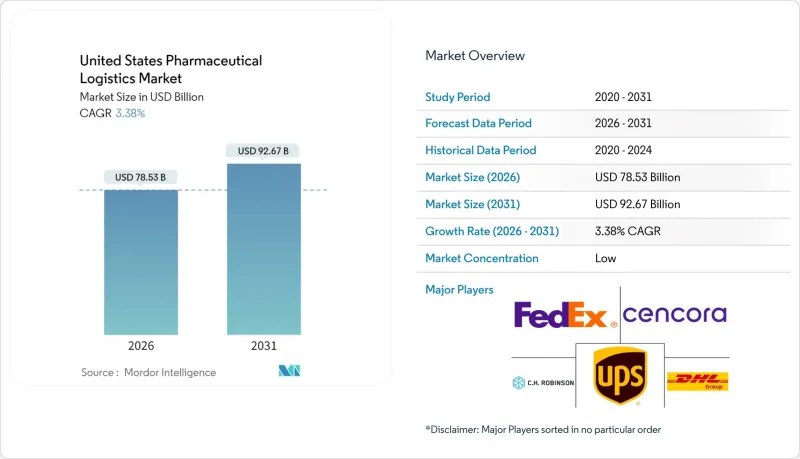

미국 의약품 물류 시장은 2025년에 759억 6,000만 달러로 평가되며, 2026년 785억 3,000만 달러에서 2031년까지 926억 7,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 3.38%로 예상됩니다.

미국 의약품 물류 시장 규모 예측은 규정 준수 기한과 생물제제 수요가 비용 구조와 서비스 설계를 재구성하고 있는 현실을 강조하고 있습니다. 2025년 8월에 만료되는 의약품 공급망 보안법(DSCSA)의 강화된 일정은 자본력이 있는 사업자만이 실행 가능한 직렬화 투자를 강제하고, 그들에게 프리미엄 가격 책정 재량권을 부여하고 있습니다. 급증하는 GLP-1 계열 체중조절요법, 꾸준히 증가하는 세포-유전자치료제, 환자 직접 배송(DTP)의 확대는 미국 의약품 물류 시장을 더욱 확대시키고 있으며, 사업자에게는 신속한 온도 관리 능력의 확대가 요구되고 있습니다. 한편, 제조업체들은 운송비 상승을 억제하기 위해 기존 의약품의 상온 안정화 버전을 개발 중입니다. 이로 인해 비냉장 유통의 상대적 성장은 둔화되지만, 부가가치 서비스(VAS) 프로바이더에게는 새로운 포장 및 표시 업무가 생겨나고 있습니다. 지역 네트워크의 재구축이 진행되어 중서부 지역이 전국 허브의 점유율을 확대하는 한편, 남부 지역의 용량 증설로 해안 회랑의 혼잡을 완화하고 있습니다.

온도관리 운송비용은 상온화물 운송의 3-5배에 달하며, 선진국 시장에서 유통되는 치료제의 80%가 현재 2-8℃의 보관이 필요하므로 콜드체인의 복잡성이 증가하고 있습니다. UPS는 2025년 4월 Andlauer Healthcare Group을 16억 달러에 인수하여 GDP 인증 창고 170만 평방피트를 추가하고, -80℃ 냉동고 네트워크를 확장하는 등 발빠르게 움직이고 있습니다. 생물제제는 주문에서 배송까지의 주기를 단축하므로 대량 운송보다 고빈도 보충 경로에 대한 수요가 증가하고 있습니다. 중소 운송업체는 FDA가 일탈 기록에 대한 감사 대상인 연속 모니터링 시스템 자금 조달에 어려움을 겪고 있으며, 업계 구조조정이 가속화되고 있습니다. 2차 시장에서 콜드체인 거점이 증가함에 따라 사업자는 지역적 유연성을 확보하는 한편, 추가 인수인계 지점에서의 재고 조정이 필요하며, AI를 통한 경로 가시성의 중요성이 더욱 커지고 있습니다.

FDA는 2025년 8월까지 처방약의 완전한 단위 단위 추적성을 의무화하고 있으며, 이로 인해 미국 의약품 물류 시장은 시리얼라이제이션 지원 프로바이더와 접근이 제한되는 사업자로 양분되고 있습니다. TraceLink의 B2B 네트워크에서 90일 동안 6천만 건의 EPCIS 이벤트를 처리한 결과, 30%의 데이터 오류율을 기록했으며, 이는 매일 제품 격리를 유발할 수 있다는 점에서 도입의 복잡성을 알 수 있습니다. 판매 가능 단위당 0.06달러로 추정되는 초기 시스템 비용은 제3자 물류 전문 업체들의 풀 솔루션 도입을 촉진하고 있습니다. DSCSA 준수를 부가가치 서비스(VAS) 패키지에 통합하는 공급자는 고정 보상을 확보할 수 있을 뿐만 아니라, 리콜 관리, 품절 대책, 위탁 생산 모니터링 등 디지털 생태계에 대한 구매자의 의존도를 더욱 심화시킬 수 있습니다.

2024-2025년 WTI 현물 가격은 23% 변동했고, 의약품 운송업체들은 비용 급등으로 인해 몇 주 늦어지는 불합리한 유류할증료 산정방식에 직면했습니다. 온도관리 트럭은 냉동장치 가동으로 인해 12% 더 많은 디젤을 소비하고, 위험을 확대시키고 있습니다. LNG와 전기 트랙터의 시험운행은 유망하지만, 항속거리의 제한과 충전 네트워크의 부족으로 인해 동서횡단 노선에서의 도입이 억제되고 있습니다. 경로 최적화 소프트웨어와 다중 거점 순회 모델은 공회전 거리를 줄일 수 있지만, 제품 무결성 규정으로 인해 화물 통합에는 여전히 한계가 있습니다.

운송은 여전히 매출의 기반이지만, 미국 의약품 물류 시장에서는 통합 솔루션으로의 전환이 뚜렷하게 나타나고 있습니다. 2025년에는 운송이 매출의 70.45%를 차지했으나, 2026-2031년 연평균 4.75%의 연평균 복합 성장률(CAGR)로 2026-2031년 화물 운송 외에도 시리얼라이제이션, 재라벨링, 키트화에 대한 고객 수요로 인해 부가가치 서비스가 매출의 70.45%를 차지할 것으로 예측됩니다. 도로화물 운송의 점유율은 라스트마일 배송과 지방 진료소 배송으로 견고한 성장세를 유지하고 있으며, 센서와 이중구획 트레일러의 도입이 컴플라이언스 강화에 기여하고 있습니다. 항공화물 운송은 고비용, 세포치료 및 지연이 허용되지 않는 특수 목적의 운송에서 틈새 시장을 유지하고 있습니다. 해상운송은 안정성이 높은 제제용 원료를 아시아에서 미국으로 향하는 항로에서 온도관리형 냉동 컨테이너로 전환하는 화주가 증가함에 따라 확대되고 있으며, ESG 목표와의 정합성 및 항공 운송 용량 부족시 수송력 확보에 기여하고 있습니다.

철도 운송은 GDP 인증 중계기지 부족으로 인해 여전히 제한적입니다. DSCSA(의약품유통안전법)에 의한 추적성 강화에 따라 창고 및 보관 수요가 급증하고 있습니다. 디포는 출하 전 2D 데이터 매트릭스 코드 검증을 위한 디지털 직렬화 허브로 변모하고 있으며, 이를 통해 자동화 프로젝트(비전 시스템 스캐너 및 자율 팔레트 운반기)를 통해 컴플라이언스 검사 지연을 줄이고 있습니다. 가장 빠르게 성장하는 분야는 부가가치 서비스(VAS) 분야로, 팔레트 재구성, 최종 단계 커스터마이징, 수출입 차액 서류 작성 등이 포함됩니다.

The United States Pharmaceutical Logistics Market was valued at USD 75.96 billion in 2025 and estimated to grow from USD 78.53 billion in 2026 to reach USD 92.67 billion by 2031, at a CAGR of 3.38% during the forecast period (2026-2031).

The United States pharmaceutical logistics market size projection underscores how compliance deadlines and biologics demand are reshaping cost structures and service design. A tightening Drug Supply Chain Security Act (DSCSA) timetable, expiring in August 2025, forces serialization investments that only well-capitalized providers can execute, granting them premium pricing latitude. Surging GLP-1 weight-management therapies, the steady rise of cell and gene treatments, and direct-to-patient (DTP) fulfillment further enlarge the United States pharmaceutical logistics market, pressing operators to expand temperature-controlled capacity at speed. Manufacturers are simultaneously formulating ambient-stable versions of existing drugs to curb rising freight costs, tempering the relative growth of non-cold-chain flows yet creating new packaging and labeling work for value-added service (VAS) providers. Regional network redesign is underway, with the Midwest gaining share as a national hub while capacity additions in the South ease congestion on coastal corridors.

Temperature-controlled transport costs three to five times more than ambient freight, and 80% of therapies shipped in developed markets now need 2°-8 °C custody, elevating cold-chain complexity. UPS moved early by paying USD 1.6 billion for Andlauer Healthcare Group in April 2025, adding 1.7 million ft2 of GDP-certified storage and extending its -80 °C freezer network. Biologics also shorten order-to-delivery cycles, driving demand for high-frequency replenishment lanes rather than bulk shipments. Smaller carriers struggle to finance the continuous monitoring systems the FDA now audits for excursion logs, accelerating consolidation. As cold-chain nodes multiply in secondary markets, operators gain geographic flexibility but must coordinate inventory at added hand-off points, intensifying the need for AI-driven route visibility.

The FDA requires full unit-level traceability on prescription medicines by August 2025, splitting the United States pharmaceutical logistics market between serialization-ready providers and those facing restricted access. Implementation complexity is evident in TraceLink's B2N network, which processed 6 million EPCIS events in 90 days yet logged a 30% data-error rate that could trigger daily product quarantines. Up-front system costs, estimated at USD 0.06 per saleable unit, invite pooling solutions run by third-party logistics specialists. Providers that embed DSCSA compliance into VAS packages not only lock in retainer fees but also deepen buyer dependence on their digital ecosystems for recall management, shortage mitigation, and contract manufacturing oversight.

WTI spot prices swung 23% in 2024-2025, leaving pharma carriers with unmatched fuel-surcharge formulas that lag cost spikes by weeks. Temperature-controlled trucks burn 12% more diesel to power reefers, amplifying exposure. While LNG and electric tractor pilots show promise, range limits and sparse charging networks curtail adoption on coast-to-coast lanes. Route-optimization software and multi-stop milk-run models reduce empty miles, but product-integrity rules still cap load consolidation.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Transportation still anchors revenue, yet the United States pharmaceutical logistics market shows a clear migration toward bundled solutions. In 2025, transportation delivered 70.45% of turnover, but value-added services are expected to outpace at a 4.75% CAGR (2026-2031) as clients seek serialization, relabeling, and kitting alongside freight. Road freight's share remains resilient due to final-mile and rural clinic deliveries, with sensors and dual-compartment trailers adding compliance. Air freight, while costly, preserves its niche for cell therapy and compassionate-use shipments that tolerate no delay. Ocean carriage gains as shippers divert stable formulation APIs to controlled-atmosphere reefers on Asia-to-US lanes, aligning with ESG goals and securing uplift during air-capacity crunches.

Rail remains marginal, hindered by limited GDP-certified hand-off nodes. Warehouse & storage demand tightens as DSCSA elevates traceability, turning depots into digital serialization hubs where 2D data-matrix codes are verified before release. This pushes automation projects-vision-system scanners and autonomous pallet movers-to squeeze latency out of compliance checks. The fastest growth occurs in VAS, including pallet reconfiguration, late-stage customization, and documentation for import-export variance.

The United States Pharmaceutical Logistics Market Report is Segmented by Service Type (Transportation, Warehousing & Storage, and Value-Added Services & Others), Mode of Operation (Cold-Chain Logistics and Non-Cold-Chain Logistics), Product Type (Prescription Drugs, Biologics & Biosimilars, Veterinary Medicine, and More), Region (Northeast, Midwest, South, and West). The Market Forecasts are Provided in Terms of Value (USD).