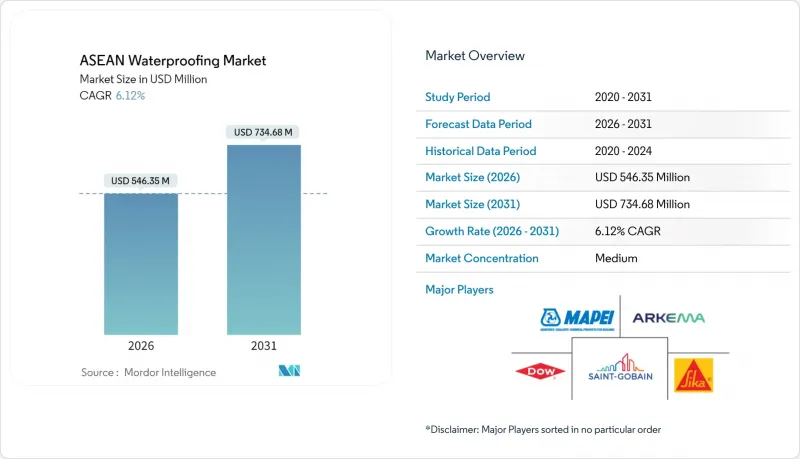

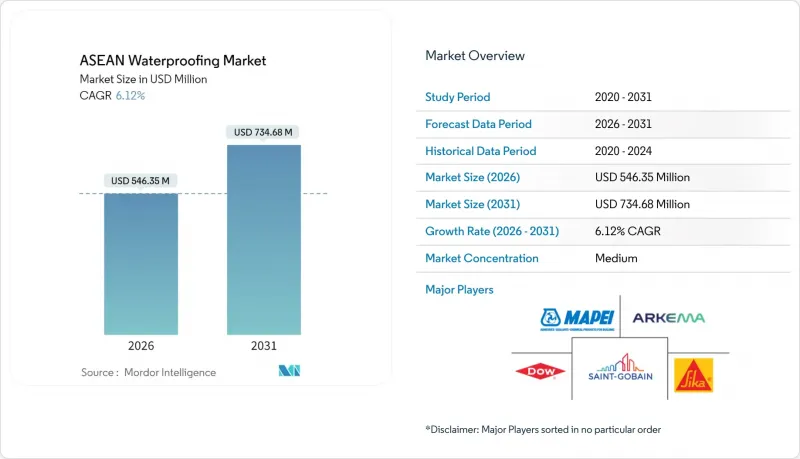

아세안의 방수 시장은 2025년 5억 1,486만 달러에서 2026년에는 5억 4,635만 달러로 성장하고, 2026-2031년 CAGR 6.12%로 성장을 지속하여, 2031년까지 7억 3,468만 달러에 이를 것으로 예측되고 있습니다.

견고한 정부 자본 지출 계획, 주택 건설의 꾸준한 회복세, 기후 변화 적응 조치의 우선 순위가 결합되어 아세안의 방수 시장은 지속적인 성장 궤도를 유지하고 있습니다. 인도네시아, 말레이시아, 태국, 베트남의 인프라 대형 프로젝트는 습하고 강우량이 많은 환경에서 철근콘크리트 구조물을 보호하는 고성능 방수시트, 액상방수시스템, 시멘트계 코팅제 조달과 직결되어 있습니다. 동시에 싱가포르와 태국의 녹색건축 규제와 도시 차원의 녹색 지붕 도입 인센티브가 결합되어 방습층, 단열층, 뿌리 저항층이 통합된 프리미엄 방수 어셈블리의 채택이 가속화되고 있습니다. 경쟁 환경은 균형을 유지하고 있습니다. 다국적 업체들은 운송비 관리를 위해 생산의 현지화를 추진하는 반면, 지역 전문업체들은 비용 측면의 유연성과 프로젝트 실적을 바탕으로 중규모 프로젝트를 수주하고 있습니다. 원자재 가격 변동과 공인 시공자 부족은 단기적인 수익률을 억제하는 한편, 단순화 및 노동력 절감 제품을 향한 기술 혁신을 촉진하는 요인으로 작용하고 있습니다.

재정 부양책이 교통 회랑, 공항, 상수도 공급 계획, 홍수 대책 프로젝트에 투입되면서 콘크리트용 결정성 혼화제, 터널용 방수포, 교량 상판용 코팅제 등의 수주가 급증하고 있습니다. 베트남은 2025년 공공투자 지출 한도를 743조 3,300억 동으로 상향 조정했습니다. 이는 공공투자법 개정에 따른 조달기간 단축과 고속도로-항만-지하철 프로젝트에서 첨단 방수기술 도입 촉진을 위한 조치입니다. 자본 프로젝트 소유자는 일반적으로 건설 비용의 70%를 자재에 할당하며, 그 중 방수는 열대 환경에서의 서비스 수명 목표를 달성하는 데 필수적인 작은 규모이지만 매우 중요한 요소입니다. 아시아개발은행은 2016년부터 2030년까지 아세안 인프라 격차를 2.8조-3조 1,000억 달러로 추산하고 있으며, 고성능 방습 시스템을 포함한 건설용 화학제품의 장기적인 수요가 보장되고 있습니다.

급증하는 도시 인구와 부족한 토지 공급으로 인해 고층 아파트와 교통 중심의 개발이 이루어지면서 견고한 외벽 보호가 요구되고 있습니다. 싱가포르에서는 '2040 육상교통 마스터플랜'에 따라 225억 스위스프랑이 철도망 정비에 투입되어 인접한 주택 건설을 촉진하고 있습니다. 지붕 데크용 타포린은 녹지율 규정을 충족해야합니다. 필리핀에서는 타운십 프로젝트에 대한 외국인 직접투자가 활발히 이루어지고 있으며, 10년 보증을 유지하면서 비용 최적화된 시멘트계 코팅에 대한 수요를 견인하고 있습니다. 지역 전체에서 개발업체들은 복잡한 형상을 따라갈 수 있는 액상 도포형 타포린으로 전환을 추진하고 있으며, 접합부 결함 감소와 공수 감소를 실현하고 있습니다. 촉박한 공사기간 속에서 매력적인 선택이 되고 있습니다. 또한, 300% 이상의 연신율과 2시간 이내의 내우성을 제공하는 하이브리드 아크릴-폴리우레탄 하이브리드 시스템으로 수요가 이동하고 있습니다. 이러한 특성은 긴 몬순 시즌에 특히 중요하게 여겨집니다. 이러한 주택시장 동향에 따라 아세안의 방수 시장에서는 각 아파트의 건설 단계 및 개보수 주기마다 새로운 보호층이 요구되기 때문에 지속적인 조달 주기가 확보되고 있습니다.

멤브레인 제조에서 생산 비용의 최대 70%는 나프타 유도체, 베이스 아스팔트, 고분자 수지가 차지합니다. Polymerupdate의 기록에 따르면, 2025년 4월 동남아시아의 스티렌 모노머 가격은 톤당 910-920달러로 전월 대비 30달러 하락하여 중국 수요 감소에 따른 가격의 급격한 변동이 두드러졌습니다. BitumenMag지에 따르면, 폴리머 개질 아스팔트 제조업체는 원유 연동 바인더 가격이 견조한 반면 SBS 및 APP 개질제 가격이 하락하고 스프레드 마진이 압축되면서 이익 압박을 받았습니다. 헤지 수단과 후방 통합이 부족한 아세안의 방수 산업 참여 중소기업의 경우, 원자재 가격 변동으로 인해 EBITDA가 침식되어 정기적인 가동 중단과 배합 개선에 대한 설비 투자 둔화를 초래하고 있습니다.

방수포는 2025년 아세안의 방수 시장에서 43.62%의 점유율을 차지할 것으로 예상되며, 2031년까지 연평균 복합 성장률(CAGR) 6.78%로 확대될 것으로 예상되며, 아세안의 방수 시장 규모의 증분 수익의 대부분을 견인할 것으로 예측됩니다. 이러한 성장은 15년 이상의 자외선 안정성, 화학적 불활성, 저온 용착성을 실현하는 열가소성 폴리올레핀(TPO) 및 에틸렌프로파일렌디엔모노머(EPDM)의 혁신에 기인합니다. 다이킨의 불소계 고분자 첨가제는 표면 반사율과 내열 노화 성능을 향상시켜 열대 지역 지붕의 수명 연장에 기여하고 있습니다.

향후 연구개발에서는 천공 시 활성화되는 마이크로 캡슐화 고분자를 통합한 자가복원형 멤브레인이 주목받고 있습니다. 이를 통해 오너의 라이프사이클 비용을 절감하고, 사양 중심의 입찰에서 공급업체를 차별화할 수 있습니다. 새로운 하이브리드 시트는 TPO 표면층과 부틸 고무 뒷면층을 결합한 듀얼 모드 접착(기계적, 화학적)을 실현하여 복잡한 관통부의 세부 설계를 단순화합니다. 이러한 복합재를 생산하는 지역 파일럿 플랜트에 투자하는 공급업체는 운송비 절감과 현지 조달 규정 적용 자격을 획득하고, 공공 자금 프로젝트에서 입찰 경쟁력을 강화할 수 있습니다.

아세안의 방수 보고서는 시스템 유형(시멘트계 시스템, 타포린, 방수시트, 방수재, 내화학성 방수 시스템), 용도(지붕/벽, 바닥/지하, 상하수도 관리, 터널 라이너 등), 지역(말레이시아, 인도네시아, 태국, 싱가포르, 필리핀, 베트남, 미얀마)별로 분류되어 있습니다. 별로 분류되어 있습니다. 시장 예측은 금액 기준(USD)으로 제공됩니다.

The ASEAN Waterproofing Market is expected to grow from USD 514.86 million in 2025 to USD 546.35 million in 2026 and is forecast to reach USD 734.68 million by 2031 at 6.12% CAGR over 2026-2031.

Robust government capital-expenditure pipelines, a steady residential construction up-cycle, and climate-adaptation priorities converge to keep the ASEAN waterproofing market on a durable growth path. Infrastructure megaprojects in Indonesia, Malaysia, Thailand, and Vietnam are translating directly into procurement of high-performance membranes, liquid-applied systems, and cementitious coatings that secure reinforced-concrete assets in humid, high-rainfall conditions. At the same time, green-building mandates in Singapore and Thailand, together with city-level incentives for vegetated roofs, are accelerating the specification of premium waterproofing assemblies that combine moisture barriers, insulation, and root-resistance layers. Competitive dynamics remain balanced: multinational manufacturers are localizing production to manage freight costs, while regional specialists leverage cost agility and project relationships to win mid-scale work. Raw-material price swings and the shortage of certified applicators cap short-term margins but also catalyze innovation toward simplified, labor-saving products.

Fiscal stimulus is funneling into transport corridors, airports, water-supply schemes, and flood-control projects, creating immediate order books for concrete-integral crystalline admixtures, tunnel-grade membranes, and bridge-deck coatings. Vietnam has lifted its 2025 public-investment disbursement ceiling to VND 743,330 billion, a move supported by a revised Public Investment Law that speeds procurement timelines and opens doors for advanced waterproofing formulas in expressway, port, and metro packages. Capital-project owners typically allocate 70% of construction outlays to materials, of which waterproofing constitutes a small yet mission-critical fraction to secure service-life targets under tropical conditions. The Asian Development Bank pegs the 2016-2030 ASEAN infrastructure gap at USD 2.8-3.1 trillion, assuring long-run demand for construction chemicals, including high-performance moisture-barrier systems.

Surging urban populations and tightening land supplies are spawning high-rise condominiums and transit-oriented developments that require robust envelope protection. In Singapore, the Land Transport Master Plan 2040 commits CHF 22.5 billion to rail connections that stimulate adjacent residential construction, where roof-deck membranes must satisfy green-plot ratio rules. The Philippines is experiencing intensified foreign-direct-investment inflows into township projects, driving volume for cost-optimized cementitious coatings that still deliver 10-year warranties. Across the region, developers are upgrading to liquid-applied membranes that contour complex geometries, reducing joint failures and cutting labor hours-an attractive proposition amid tight construction schedules. Demand is also shifting toward hybrid acrylic-polyurethane systems offering elongation above 300% and rain-resistance in under two hours, features prized during the long monsoon season. These residential dynamics ensure recurring procurement cycles for the ASEAN waterproofing market as each condominium phase and refurbishment cycle specifies fresh layers of protection.

Naphtha derivatives, base bitumen, and polymer resins account for up to 70% of production cost in membrane manufacturing. Polymerupdate recorded Southeast Asian styrene monomer prices at USD 910-920 per metric ton in April 2025, down USD 30 month-on-month, underscoring price whiplash tied to Chinese demand weakness. BitumenMag notes that polymer-modified bitumen producers saw profit squeezes when crude-linked binder prices held firm while SBS and APP modifiers fell, compressing spread margins. Volatile feedstock costs erode EBITDA for smaller ASEAN waterproofing industry participants lacking hedging tools or backward integration, leading to periodic shutdowns and slowed capex on formulation upgrades.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Membranes claimed a 43.62% ASEAN waterproofing market share in 2025, and the segment is forecast to grow at a 6.78% CAGR through 2031, driving the lion's share of incremental revenue within the ASEAN waterproofing market size. Growth stems from thermoplastic polyolefin (TPO) and ethylene propylene diene monomer (EPDM) innovations that deliver UV stability beyond 15 years, chemical inertia, and weldability at lower temperatures. Daikin's fluoro-polymer additives boost surface reflectance and heat-aging performance, giving tropical rooftops an extended life cycle.

Looking ahead, research and development pipelines feature self-healing membranes integrating microencapsulated polymers that activate upon puncture, thus lowering life-cycle costs for owners and differentiating suppliers in specification-heavy tenders. Emerging hybrid sheets combine TPO topsides with butyl-rubber undersides for dual-mode adhesion, mechanical, and chemical, simplifying detailing at complicated penetrations. Suppliers investing in regional pilot plants to produce such composites gain freight savings and qualify under local-content rules, enhancing bid competitiveness across publicly financed projects.

The ASEAN Waterproofing Report is Segmented by System Type (Cementitious Systems, Membranes, Water Stops, and Chemical Resisting Water Proofing System), Application (Roofing and Walls, Floor and Basement, Water and Waste Management, Tunnel Liner, and More), and Geography (Malaysia, Indonesia, Thailand, Singapore, Philippines, Vietnam, and Myanmar). The Market Forecasts are Provided in Terms of Value (USD).