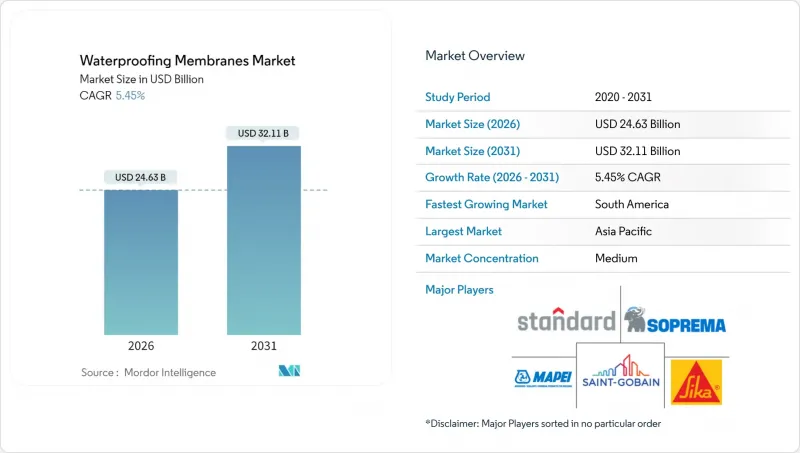

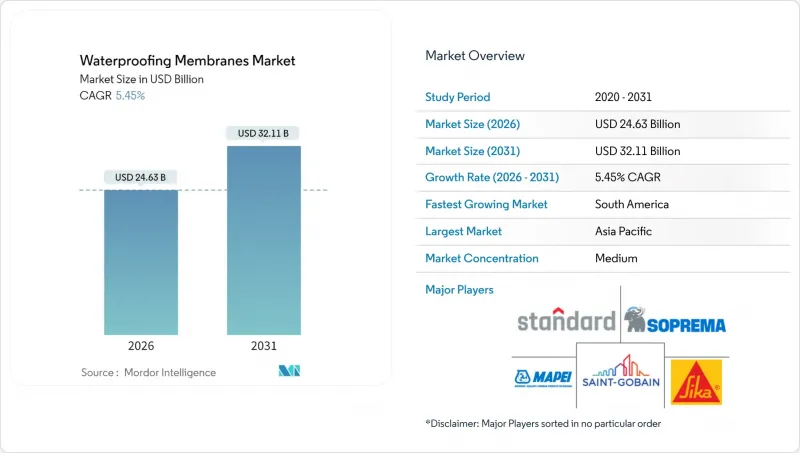

방수막 시장 규모는 2026년에는 246억 3,000만 달러로 추정되며, 2025년 233억 6,000만 달러에서 성장이 전망됩니다. 2031년의 예측에서는 321억 1,000만 달러에 달하며, 2026-2031년에 CAGR 5.45%로 성장할 것으로 전망되고 있습니다.

이러한 성장은 가속화되는 도시화, 엄격한 건물 외피 에너지 기준 및 인프라 현대화 프로그램에 힘입어 주거, 상업 및 인프라 시설 전반에 걸쳐 잠재적 수요를 안정적인 프로젝트 기반 주문으로 전환하고 있습니다. 방수는 구조적 자산을 물의 침투로부터 보호하는 것이며, 경제 사이클을 통해 불변의 기본 요구 사항이기 때문에 제품 대체는 제한적입니다. 모듈식 건축, 급속한 지하철 개발, 녹색 지붕 장려 정책은 용도 구성을 변화시키고 있으며, 시산업체는 설치 주기를 단축하고 숙련공 부족을 완화하기 위해 스프레이 액체 시스템을 점점 더 선호하는 경향이 있습니다. 수익성은 원자재의 적시 헤지, 민첩한 유통, 새로운 화재 안전 및 에너지 성능 규제를 충족하는 제품 포트폴리오에 달려 있습니다.

대도시 지역의 지하 네트워크, 교통 회랑, 복합용도 타워의 확장과 함께 도시 인구 증가는 조달 패턴을 변화시키고 있습니다. 중국의 도시화율은 2024년 66.2%에 달하며, 2030년까지 75%를 목표로 하고 있습니다. 또한 인도의 스마트 시티 구상은 도시 인프라 구축에 280억 달러를 투입하고 있습니다. 이 계획에서는 터널, 지하, 지하층, 연단 데크에 공공의 안전과 경제 활동의 연속성을 위협하는 연쇄 고장을 방지하기 위해 고품질의 장수명 타포린을 지정하고 있습니다. 지하 구조물에는 여러 보호 층이 필요하므로 방수포 시장은 프로젝트 당 사용량 증가의 혜택을 누리고 있습니다. 민관 협력의 장기 양허 계약은 유지보수 의무를 고정하고 소유주가 수명주기 비용을 최소화하는 내구성 높은 솔루션을 선택하도록 유도함으로써 수요를 더욱 강화하고 있습니다.

에너지 성능 규정에서는 방수포가 단열 외피 내의 기능층으로 취급되어 기밀층, 방습층, 방수층의 경계가 모호해졌습니다. 유럽연합의 '건축물 에너지 성능 지침'은 신축 건물에 순 제로 에너지를 의무화하고, 설계자에게 습기와 열 흐름을 동시에 제어하는 통합 방수 시스템을 채택할 것을 촉구하고 있습니다. 북미에서는 ASHRAE 90.1-2022에서 연속 기밀층을 규정 요건으로 명시함에 따라 기판 전체에 매끄러운 전환을 실현하는 액체 방수막에 대한 수요가 증가하고 있습니다. 규제가 진화함에 따라 공급업체들은 기존 방수층을 다기능 층으로 전환하는 고단열 첨가제 및 반사 안료의 부가가치를 수익화하여 리노베이션 시장과 신축 시장 모두에서 프리미엄 가격 책정을 지원하고 있습니다.

정유소 가동 축소와 지정학적 충격으로 인해 2024년 역청 가격은 23% 상승했고, 세 차례의 연속적인 가격 인상은 전체 프로젝트 예산에 영향을 미쳤습니다. 개질 아스팔트 시트는 세계 소비량의 약 40%를 차지하며, 원자재 가격 변동을 직접적으로 흡수합니다. 비용에 민감한 주택 지붕개량 공사 시공사들은 추가 비용을 주택 소유주에게 전가할 수 없어 공사 연기나 열가소성 수지로의 사양 변경이 선택적으로 발생하고 있습니다. 제조업체들은 장기 공급계약과 바이오 개질제를 통한 헤지를 진행하고 있지만, 리스크에 대한 노출은 구조적인 문제로 남아 단기적으로 방수막 시장의 성장을 억제하는 요인으로 작용할 것입니다.

2025년 기준 방수막 시장에서 가장 큰 점유율(33.92%)을 차지한 것은 냉액상 도포막입니다. 이는 모서리, 관통부, 복잡한 파사드 요소 주변에 피팅 없는 장벽을 형성할 수 있는 특성 때문입니다. 완전 접착 시트 시스템은 점유율은 낮지만, 건축가들이 치수 안정성과 우수한 A급 방화 성능을 높이 평가하고 있으며, 2031년까지 연평균 복합 성장률(CAGR) 7.38%를 나타낼 것으로 예측됩니다. 고온 액체 시스템은 공정 온도에 따른 내열성이 요구되는 산업 환경에서 지속적으로 채택되고 있습니다. 한편, 깔아놓은 시트는 수량은 감소하는 추세이지만, 비용 중심의 지붕 개보수 수요에 계속 대응하고 있습니다.

콜드 액상 타포린 시장 규모 확대는 속도와 균일한 품질을 중시하는 모듈식 제조 라인의 급속한 채택에 의해 주도되고 있습니다. 공급업체는 폴리우레탄 또는 PMMA 매트릭스에 자기복원성 나노복합체를 통합하여 유지보수 재작업을 줄이고 장기 보증을 실현하고 있습니다. 한편, 완전 접착식 PVC 및 TPO 시트는 미션 크리티컬한 설비를 위해 저할로겐 및 난연성 어셈블리를 필요로 하는 데이터센터 건설업체들의 주목을 받고 있습니다. 제품 구성의 동향은 스프레이 시공의 베이스층과 조립식 캡시트를 결합한 하이브리드 제품으로 전환되고 있으며, 각 기술의 특징을 살린 설계가 주류를 이루고 있습니다.

아시아태평양은 2025년 전 세계 매출의 36.08%를 차지할 것으로 예상되며, 중국의 일대일로 프로젝트와 인도의 도시철도의 급격한 확장이 견인차 역할을 할 것으로 보입니다. 중국과 인도의 지하철 계획과 스마트 시티 계획이 멤브레인 공급망에 지속적인 수주를 가져오고 있습니다. 일본과 한국은 내진보강 및 건물 개보수 수요가 유지되고 있으며, 인도네시아, 베트남, 태국은 산업단지 및 물류거점 증가에 따라 두 자릿수 성장을 기록하고 있습니다.

북미와 유럽은 성숙한 시장인 동시에 기술적으로도 앞선 시장입니다. 미국에서는 개정된 ASHRAE 90.1-2022 표준으로 인해 차폐 기능이 있는 타포린에 대한 지출이 촉진될 것으로 예측됩니다. 캐나다의 인프라 개선 계획은 지방정부의 상하수도 시설에 우선순위를 두고 있으며, 내화학성 액체 도포 시스템 조달이 증가하고 있습니다. 유럽 수요는 녹색 지붕 의무화에 집중되어 있으며, 베를린과 비엔나에서는 광활한 평지붕에 식물을 설치하는 것이 의무화되어 있습니다. 방수막 시장은 이에 대응하여 신장성과 내천공성을 겸비한 내근성 배합을 도입하여 식생 구조물과의 적합성을 확보하고 있습니다.

남미 지역은 2031년까지 연평균 5.94%의 성장률을 보일 것으로 예측되며, 브라질의 150억 달러 규모의 배수 및 홍수 대책 프로그램과 아르헨티나 부에노스아이레스의 상업 재개발이 이를 견인할 것으로 전망됩니다. 환율 변동과 자금 조달 격차로 인해 일시적인 정체 현상이 발생하지만, 프로젝트 백로그는 건전한 상태를 유지하고 있습니다. 공급업체는 환리스크 헤지 및 운송비 절감을 위해 현지에 혼합공장을 건설하고 있습니다. 중동 및 아프리카은 경제 다변화 정책에 따른 공공주택, 관광, 유틸리티 메가 프로젝트 자금 조달을 배경으로 완만한 성장이 예상됩니다.

Waterproofing Membranes Market size in 2026 is estimated at USD 24.63 billion, growing from 2025 value of USD 23.36 billion with 2031 projections showing USD 32.11 billion, growing at 5.45% CAGR over 2026-2031.

This growth is anchored in accelerating urbanization, stringent building-envelope energy codes, and infrastructure modernization programs that convert pent-up demand into steady, project-backed orders across residential, commercial, and infrastructure sites. Product substitution is limited because waterproofing protects structural assets from water ingress, a fundamental requirement that remains constant throughout economic cycles. Modular construction, rapid metro development, and green-roof incentives are reshaping the application mix, while contractors increasingly favor spray-applied liquid systems that shorten installation cycles and mitigate skilled-installer shortages. Profitability hinges on timely raw material hedging, agile distribution, and product portfolios that meet emerging fire safety and energy performance mandates.

Urban population growth is reshaping procurement patterns as megacities extend their underground networks, transit corridors, and mixed-use towers. China's urbanization rate reached 66.2% in 2024, with a national target of 75% by 2030, and India's Smart Cities Mission has earmarked USD 28 billion for urban infrastructure upgrades. These programs specify premium, long-service-life membranes for tunnels, basements, and podium decks to prevent cascading failures that would otherwise threaten public safety and economic continuity. The waterproofing membranes market benefits from the fact that below-grade structures require multiple layers of protection, driving higher volumes per project. Long concession tenures in public-private partnerships further reinforce demand by locking in maintenance obligations and encouraging owners to choose durable solutions that minimize life-cycle cost.

Energy-performance regulations now treat waterproofing membranes as functional layers within the thermal envelope, blurring the lines between air, vapor, and water barriers. The European Union's Energy Performance of Buildings Directive mandates near-zero-energy new construction, pushing designers to specify integrated membrane systems that control moisture and heat flow simultaneously. In North America, ASHRAE 90.1-2022 lists continuous air barriers as a prescriptive requirement, prompting demand for liquid membranes that create seamless transitions across substrates. As codes evolve, suppliers monetize higher R-value additives and reflective pigments that transform traditional waterproofing into multifunctional layers, supporting premium pricing in both retrofit and new-build markets.

Refinery curtailments and geopolitical shocks lifted bitumen prices by 23% in 2024, prompting three consecutive list-price increases that rippled across project budgets. Modified-bitumen sheets comprise roughly 40% of global consumption and absorb raw-material shocks directly. Contractors in cost-sensitive residential reroofing struggle to pass surcharges to homeowners, causing postponements and selective specification switches to thermoplastics. Manufacturers are hedging through long-term supply contracts and bio-based modifiers, but exposure remains a structural risk that dampens the waterproofing membranes market growth in the short term.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Cold-liquid-applied membranes held the largest share at 33.92% of the waterproofing membranes market in 2025, thanks to their ability to form seamless barriers around angles, penetrations, and complex facade elements. Fully adhered sheet systems trail but register a 7.38% CAGR through 2031 as architects value their dimensional stability and superior Class A fire performance. Hot liquid systems persist in industrial settings where process temperatures demand thermal resistance, whereas loose-laid sheets continue to cater to cost-sensitive reroofing despite eroding volumes.

The waterproofing membranes market size for cold liquid-applied products is driven by the rapid adoption in modular manufacturing lines that prioritize speed and uniform quality. Suppliers integrate self-healing nano-composites into polyurethane and PMMA matrices, reducing maintenance callbacks and supporting longer warranties. Meanwhile, fully adhered PVC and TPO sheets attract data center builders who require low-halogen, flame-retardant assemblies for mission-critical installations. The product mix is trending toward hybrids that combine spray-applied base layers with prefabricated cap sheets, capitalizing on the respective strengths of each technology.

The Global Waterproofing Membranes Market Report is Segmented by Product Type (Cold Liquid Applied, Hot Liquid Applied, Fully Adhered Sheet, and Loose-Laid Sheet), End-Use Sector (Commercial, Industrial and Institutional, Infrastructure, and Residential), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific recorded a 36.08% share of global revenue in 2025, propelled by China's Belt and Road projects and India's surge in urban rail. China and India's metro pipeline and Smart Cities Mission funnel continuous orders into membrane supply chains. Japan and South Korea sustain demand through seismic retrofitting and building rehabilitation, while Indonesia, Vietnam, and Thailand post double-digit growth as industrial parks and logistics hubs proliferate.

North America and Europe represent mature but technologically advanced markets. In the United States, the upgraded ASHRAE 90.1-2022 standards are expected to stimulate spending on membranes that integrate air-barrier functionality. Canada's infrastructure improvement plan prioritizes municipal water and wastewater facilities, increasing procurement of chemically resistant liquid-applied systems. European demand centers on green-roof mandates, with Berlin and Vienna mandating vegetation on expansive flat roofs. The waterproofing membranes market responds by introducing root-resistant formulations that combine elongation with puncture resistance, ensuring compatibility with vegetated assemblies.

South America leads regional growth with a 5.94% CAGR forecast through 2031, guided by Brazil's USD 15 billion drainage and flood-control program and Argentina's commercial redevelopment in Buenos Aires. Currency volatility and financing gaps create intermittent pauses, but project backlogs remain healthy. Suppliers build local blending plants to hedge currency risk and slash freight costs. The Middle East and Africa follow with gradual gains as economic diversification funds public housing, tourism, and utility megaprojects.