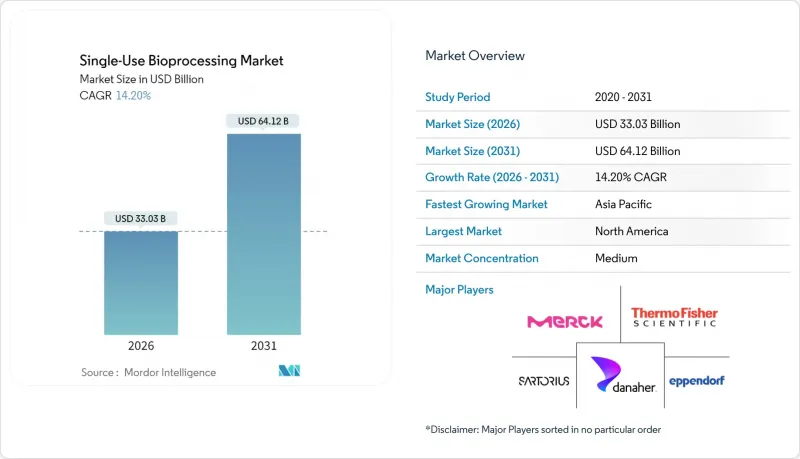

2026년 일회용 바이오 프로세싱 시장 규모는 330억 3,000만 달러로 추정되며, 2025년 289억 2,000만 달러에서 성장이 전망됩니다.

2031년까지 예측은 641억 2,000만 달러에 달할 것으로 예상되며, 2026-2031년 연평균 복합 성장률(CAGR) 14.2%로 확대될 것으로 전망됩니다.

유연한 mRNA 백신 생산 능력, 맞춤형 치료제 생산, 자본 집약도가 낮은 시설 모델에 대한 지속적인 수요가 일회용 기술에 대한 투자를 지속적으로 견인하고 있습니다. 북미와 유럽의 제조업체들은 고정식 스테인리스강 설비를 모듈식 일회용 라인으로 교체함으로써 가동 기간을 최대 24개월까지 단축하고 있습니다. 한편, 아시아태평양의 그린필드 프로젝트에서는 기존 플랜트의 높은 유틸리티 요구 사항을 피하기 위해 일회용 시스템을 채택하고 있습니다. 비용 절감, 빠른 전환, 오염 위험 감소가 여전히 주요 구매 기준이며, 기업이 물 절약 솔루션을 찾는 가운데 지속가능성 요구사항이 공급업체 선정에 영향을 미치고 있습니다. 경쟁의 초점은 대형 바이오리액터, 폴리머의 안정적인 공급, 연속 처리 및 하이브리드 처리 흐름을 지원할 수 있는 통합 센서 패키지에 집중되어 있습니다.

일회용 시스템은 스테인리스강 시설에 일반적으로 필요한 5,000만-1억 달러의 자본을 절감하여 기업이 배관, 청정 증기, 주입수 네트워크가 아닌 연구개발에 자금을 할당할 수 있도록 합니다. GSK가 1억 2,000만 달러를 투자한 펜실베니아 공장은 2,000리터 일회용 바이오리액터를 채택하여 시운전 기간을 최대 2년 단축하고 세척 검증 작업을 없앴다. 소규모 바이오텍 기업이나 CDMO(위탁개발생산기관)는 규모의 제약 없이 지역 분산 생산 전략을 가능하게 하는 일회용 라인의 이점을 가장 많이 누릴 수 있습니다. 지속적인 비용 절감은 물 사용량의 80% 감소와 오토클레이브 에너지 감소를 통해 이루어지며, 제품수명주기 전반에 걸쳐 시설의 영업 이익률을 향상시킵니다.

세계에서 바이오의약품이 확대됨에 따라 제조업체들은 교차 오염 위험을 최소화하고 여러 분자를 빠르게 연속 생산할 수 있는 장비 세트로 전환해야 하는 상황에 직면해 있습니다. 특히 바이오시밀러 제조업체들은 일회용 전환을 통해 규제상의 복잡성을 증가시키는 장기간의 세척 검증이 필요하지 않기 때문에 이점을 얻게 되었습니다. 인도의 바이오의약품 CDMO 매출은 2023년 135억 8,000만 달러에서 2028년까지 247억 7,000만 달러로 증가할 것으로 예상되며, 단일 사용 플랫폼의 도입으로 과거 국내 생산 능력 확대를 제한했던 막대한 침몰 비용이 해소될 것으로 예측됩니다. 해소할 수 있습니다. ATMP 개발 기업도 마찬가지로 세포 및 유전자 치료의 밀폐 및 무균 처리를 위해 일회용 라인을 선호하고 있으며, 향후 10년간 안정적인 수요를 지원하고 있습니다.

규제 당국은 고분자 용출물로부터 환자를 보호하기 위해 2026년 5월까지 기존 USP(88) 클래스 VI 시험 대신 USP(665) 및 USP(87)에 의한 감시를 강화하고 있습니다. 시스템 공급업체는 현재 각 필름, 커넥터 및 개스킷의 광범위한 화학적 특성 평가에 자금을 투입하고 있으며, 이로 인해 적격성 평가 예산이 증가하고 프로젝트 일정이 길어지고 있습니다. 제약기업의 허가 신청시 다각적인 분석 데이터 제출이 의무화되어 첨단 실험 설비를 갖춘 기존 기업에 유리하게 작용하는 한편, 중소 벤더의 진입을 지연시킬 가능성이 있습니다.

배양액 백 및 용기는 2025년 98억 4,000만 달러의 매출을 창출하여 일회용 바이오프로세싱 시장 점유율 34.02%를 차지할 것으로 예측됩니다. 원료 처리, 종자 배양 저장, 수확물 수집 등 범용적인 역할로 인해 모든 규모에서 높은 수요를 유지하고 있습니다. 3층 필름 기술의 발전으로 가스 투과성 및 용매 호환성이 향상되어 포유류 및 미생물 응용 분야에서 우위를 점하고 있습니다. 3,000L-5,000L 포맷의 상업적 타당성이 입증됨에 따라 일회용 바이오리액터 카테고리는 2031년까지 연평균 복합 성장률(CAGR) 14.75%로 확대될 것으로 예측됩니다. 자기 교반, 프로브 이중화, 통합 광학 센서로 도입을 방해하던 전단력 및 스케일업에 대한 우려를 줄였습니다. 바이오리액터용 일회용 바이오프로세싱 시장 규모는 아시아태평양의 파일럿 플랜트의 상업적 도입 프로그램에 힘입어 2031년까지 2배 이상 확대될 것으로 예측됩니다.

고밀도 퍼퓨전 배양이 정제 라인에 공급되면서 다운스트림 공정의 병목현상이 심화되는 가운데, 여과 어셈블리는 수익성 측면에서 2위를 차지합니다. 하이브리드형 심층여과막 설계는 현재 2,000리터 이상의 생산용 바이오리액터에 대응할 수 있는 처리 용량을 달성하여 일회용 제품의 보급을 확대하고 있습니다. 튜브, 무균 커넥터, 샘플링 밸브는 꾸준한 성장세를 보이고 있습니다. 이는 대용량 연속 라인이 반복적인 압력 사이클을 견딜 수 있는 고신뢰성 유체 경로가 필요하기 때문입니다. 공정 분석 기술(PAT)에 대한 기대가 높아지면서 일회용 분석 프로브도 빠르게 보급되고 있으며, 스테인리스강 하우징 내부의 오염에 대한 걱정 없이 작업자에게 실시간 제어를 제공합니다.

업스트림 공정은 포유류 세포배양에서 일회용 바이오리액터에 대한 신뢰가 확산되면서 2025년 매출의 46.60%를 차지할 것으로 예측됩니다. 고강도 퍼퓨전을 통한 생산성 향상은 상업용 항체 생산에 있으며, 일회용 반응기를 매력적인 선택으로 만들고 있습니다. 그러나 수지 프리크로마토그래피, 멤브레인 흡착 장치, 단일 패스턴셜 플로우 필터가 기존의 성능 한계를 극복하면서 다운스트림 공정 시스템은 15.05%의 연평균 복합 성장률(CAGR)로 성장하며 격차를 좁혀가고 있습니다. 바이러스 벡터 및 차세대 백신을 위한 완전 일회용 처리 라인이 도입됨에 따라 다운스트림 공정용 일회용 바이오프로세싱 시장 규모는 2031년까지 220억 달러 이상에 달할 것으로 예측됩니다.

연속 처리의 모멘텀이 이 다운스트림 공정으로의 전환을 가속화하고 있습니다. 통합형 관류 크로마토그래피 스키드는 시설 면적을 40% 이상 절감할 수 있으며, 설비 가동률이 생산량보다 더 중요한 고부가가치 제품에 매력적인 제안입니다. 성공사례가 축적됨에 따라 일회용 정제 시스템에 대한 규제 당국의 이해도가 높아지면서, 기존 일회용 업스트림 공정과 스테인리스강 하류 설비를 결합한 하이브리드 레이아웃을 폐지하려는 움직임이 가속화되고 있습니다. 그 결과, 민첩성을 높이고 교차 오염 위험을 줄이는 엔드 투 엔드 일회용 플랜트로의 전환이 진행되고 있습니다.

북미는 2025년 매출의 41.75%를 차지할 것으로 예상되며, 이는 젠텍과 암젠과 같은 선도 기업이 일회용 라인에 대한 규제 선례를 확립한 것이 기반이 되었습니다. 성숙한 CDMO 생태계와 명확한 FDA 지침은 도입 주기를 효율화하고, 주정부 보조금 제도는 팬데믹으로 인한 공급 부족에 따라 지역 백신 생산 능력을 강화하는 데 도움을 주고 있습니다. 보스턴 캠브리지 지역과 샌프란시스코 베이 지역의 지식 집적지에서는 일회용 설비를 높은 가동률로 운영할 수 있는 숙련된 운영자를 쉽게 확보할 수 있습니다.

아시아태평양은 2031년까지 15.25%의 연평균 복합 성장률(CAGR)을 보이고, 세계에서 가장 빠른 성장세를 보이고 있습니다. 중국의 산업 정책은 신규 바이오로지스 캠퍼스에 보조금을 지급하고, 현지 건설업체는 고순도 배관 비용과 장기 시운전 일정을 피하기 위해 일회용 시스템을 선호합니다. BioNTech가 10개의 2,000L 일회용 라인이 있는 시설을 인수한 것은 지역 규제 당국의 수용에 대한 확신을 보여줍니다. 인도 CDMO 시장은 전력 및 수자원 제약을 보완하기 위해 일회용에 의존하고 있으며, 한국에서는 정부 지원의 Cytiva 공장이 주요 고객사와 가까운 소모품 공급을 확보하고 있습니다.

유럽에서는 이미 많은 플랜트들이 미드스트림 공정의 핵심 공정을 이미 전환했으므로 꾸준하고 완만한 성장세를 보이고 있습니다. EU 기후법은 물과 에너지를 절약하는 일회용 원자로의 채택을 가속화하는 한편, 매립지 규제는 기업이 재활용 연합에 투자하도록 강요하고 있습니다. 사노피의 새로운 인슐린 생산기지는 초고처리량 제품에는 여전히 스테인리스강을 선호하고 있으며, 초대형 범용 바이오의약품은 비용 측면에서 금속 기반이 지속될 가능성을 보여주고 있습니다. 라틴아메리카, 중동 및 아프리카은 미숙하지만 인프라 부족으로 인해 스테인리스강이 비현실적인 그린필드 건설지로 매력적입니다. 다자간 백신 구상은 이들 지역에서의 1차 매출을 촉진하고, 일회용 바이오프로세싱 시장의 장기적인 생산량 확대를 지원할 수 있습니다.

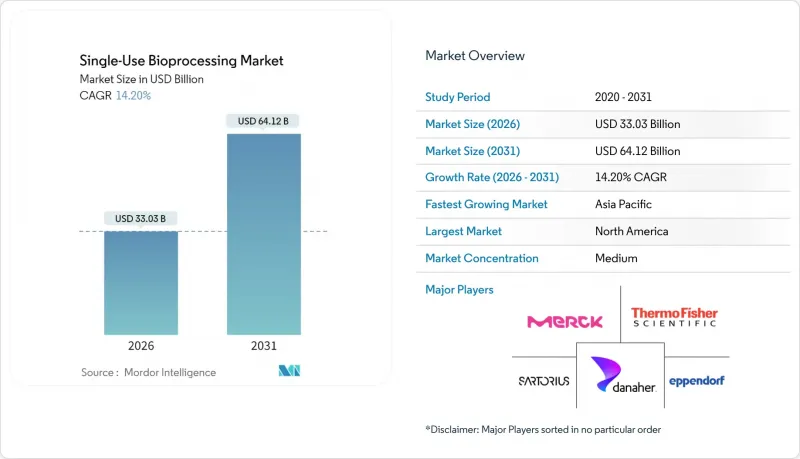

Single-use bioprocessing market size in 2026 is estimated at USD 33.03 billion, growing from 2025 value of USD 28.92 billion with 2031 projections showing USD 64.12 billion, growing at 14.2% CAGR over 2026-2031.

Consistent demand for flexible mRNA vaccine capacity, personalized therapy production, and capital-light facility models continues to pull investment toward disposable technologies. North American and European manufacturers replace fixed stainless-steel assets with modular single-use lines that reduce start-up timelines by up to 24 months, while Asia-Pacific greenfield projects use single-use systems to bypass the high utility requirements of conventional plants. Cost avoidance, faster changeovers, and lower contamination risk remain the dominant purchasing criteria, and sustainability mandates now influence vendor selection as firms seek water-saving solutions. Competitive activity centers on larger bioreactors, polymer security of supply, and integrated sensor packages that can support continuous and hybrid processing flows.

Single-use systems eliminate USD 50-100 million of capital that stainless-steel facilities typically require, enabling companies to allocate funds to R&D instead of piping, clean-steam, and water-for-injection networks. GSK's USD 120 million Pennsylvania plant uses 2,000 L disposable bioreactors and cut commissioning time by up to two years while removing cleaning-validation labor . Smaller biotech firms and CDMOs benefit most, as single-use lines allow distributed regional production strategies without scale penalties. Ongoing savings stem from 80% lower water consumption and reduced autoclave energy, which improve facility operating margins across product life cycles.

Global biologics expansion pushes manufacturers toward equipment sets that minimize cross-contamination risk and accommodate multiple molecules in rapid succession. Biosimilar producers gain particular advantage because single-use changeovers do not require prolonged cleaning verification that adds to regulatory complexity. India's biologics CDMO revenue is projected to climb from USD 13.58 billion in 2023 to USD 24.77 billion by 2028, with single-use platforms removing the large sunk costs that once limited domestic capacity growth. ATMP developers equally prefer disposable lines for enclosed, sterile handling of cell and gene therapies, reinforcing steady demand into the next decade.

Regulators escalate scrutiny through USP (665) and USP (87), replacing legacy USP (88) Class VI testing by May 2026 to protect patients from polymer leachates. System suppliers now fund extensive chemistry characterization for each film, connector, and gasket, raising qualification budgets and elongating project timelines. Pharma license applications must include multi-modal analytical data, which favors incumbents with sophisticated labs and may slow smaller vendors' entry.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Media bags and containers delivered USD 9.84 billion revenue in 2025, equal to 34.02% of the single-use bioprocessing market share. Their universal role in raw-material handling, seed-culture storage, and harvest collection keeps volume demand high across every scale. Technology advances in 3-layer films improve gas permeability and solvent compatibility, reinforcing their dominance in both mammalian and microbial applications. The single-use bioreactor category grows at a 14.75% CAGR through 2031 as 3,000 L-5,000 L formats prove commercially viable. Magnetic mixing, probe redundancy, and integrated optical sensors mitigate shear and scale-up worries that once limited adoption. The single-use bioprocessing market size for bioreactors is projected to more than double by 2031 on the back of commercial install programs in Asia-Pacific pilot plants.

Filtration assemblies rank second in revenue as downstream bottlenecks become acute when high-density perfusion cultures feed purification trains. Hybrid depth-filter and membrane designs now reach throughputs that support production bioreactors larger than 2,000 L, expanding disposable penetration. Tubing, aseptic connectors, and sampling valves register steady growth because larger-volume continuous lines require high-integrity fluid paths that withstand repeated pressure cycles. Single-use analytical probes also post brisk uptake as Process Analytical Technology expectations rise, giving operators real-time control without fouling concerns inside stainless-steel housings.

Upstream processing held 46.60% of 2025 revenue owing to widespread confidence in single-use bioreactors for mammalian cell culture. Productivity boosts from high-intensity perfusion make disposable reactors attractive for commercial antibody manufacturing. However, downstream systems advance at 15.05% CAGR, narrowing the gap as resin-free chromatography, membrane adsorbers, and single-pass tangential-flow filters overcome earlier performance limits. The single-use bioprocessing market size allocated to downstream operations is expected to exceed USD 22 billion by 2031 as fully disposable trains roll out for viral vectors and next-generation vaccines.

Continuous processing momentum accelerates this downstream shift. Integrated perfusion-chromatography skids can reduce facility footprints by more than 40%, an enticing proposition for high-value products where equipment utilization matters more than volumetric output. Regulatory familiarity with disposable purification systems grows as successful dossiers accumulate, encouraging adopters to eliminate hybrid layouts that once paired single-use upstream with stainless downstream gear. The result is a move toward end-to-end disposable plants that advance agility and reduce cross-contamination risk.

The Single-Use Bioprocessing Market Report is Segmented by Product (Single-Use Bioreactors, Filtration Assemblies, and More), Workflow Stage (Upstream Processing, Downstream Processing, Other Operations), End User (Biopharmaceutical Companies, and More), Scale (Clinical Scale, Commercial Scale), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America accounted for 41.75% of 2025 revenue, anchored by early-mover companies such as Genentech and Amgen that set regulatory precedent for disposable lines. A mature CDMO ecosystem and clear FDA guidance streamline adoption cycles, while state capital grants encourage local vaccine capacity after pandemic supply shortages. Knowledge clusters in Boston-Cambridge and the San Francisco Bay Area ensure ready access to experienced operators who can run single-use facilities at high utilization.

Asia-Pacific records a 15.25% CAGR through 2031, the fastest worldwide trajectory. China's industrial policy subsidizes new biologics campuses, and local builders prefer disposable systems to avoid high-purity piping costs and long commissioning schedules. BioNTech's acquisition of a facility with ten 2,000 L single-use lines highlights confidence in regional regulatory acceptance. India's CDMO market leans on single-use to bridge power and water constraints, and South Korea's government-backed Cytiva factory secures consumable supply closer to key customers.

Europe shows steady but slower growth as many plants have already transitioned core upstream steps. EU climate law accelerates further adoption because disposable reactors save water and energy, yet landfill regulations force companies to invest in recycling alliances. Sanofi's new insulin site still favors stainless for ultrahigh-throughput products, demonstrating that very large commodity biologics may remain metal-based for cost reasons. Latin America, the Middle East, and Africa remain nascent but attractive for greenfield builds where infrastructure gaps make stainless less practical. Multilateral vaccine initiatives could catalyze first-wave sales in those regions, supporting long-term volume upside for the single-use bioprocessing market.