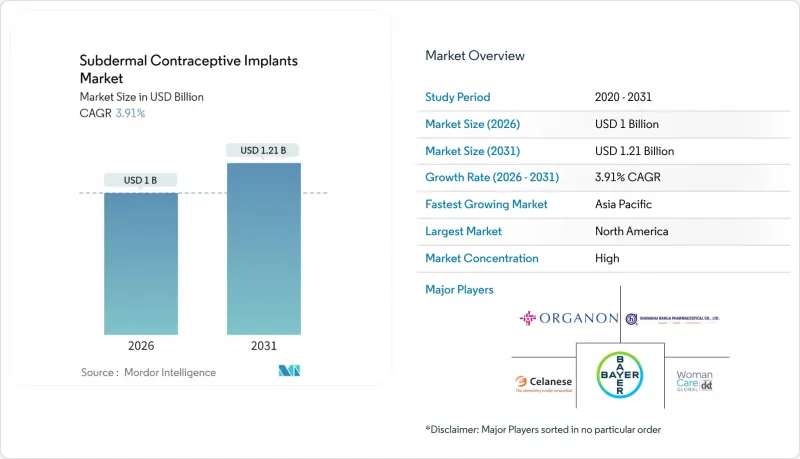

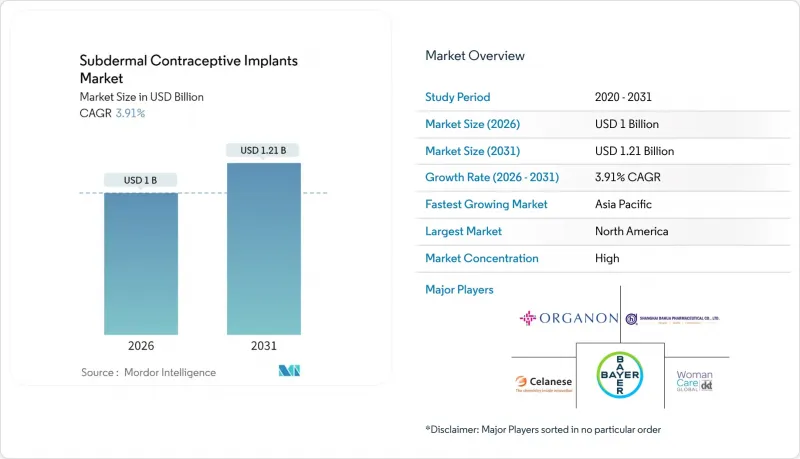

피하 피임 임플란트 시장 규모는 2026년에는 10억 달러로 추정되고 있으며, 2025년 9억 6,000만 달러에서 성장하며, 2031년에는 12억 1,000만 달러에 달할 것으로 예측됩니다.

2026-2031년 연평균 성장률(CAGR)은 3.91%를 보일 것으로 예측됩니다.

이러한 점진적인 확대는 공공구매자, 보험사, 기부자의 임플란트 예산이 증가함에 따라 장기 지속형 가역 피임법이 틈새 대안에서 주류 가족계획 수단으로 전환되고 있음을 반영합니다. 미국 국제개발처(USAID)가 2024년 6억 7,500만 달러의 가족계획 예산을 책정하는 등 정부 지원(임플란트 피임약 가치의 34%를 차지)은 예측 가능한 수요 파이프라인을 구축하여 제조업체가 생산량과 가격 책정을 최적화할 수 있도록 돕고 있습니다. 할 수 있게 해줍니다. 이러한 도입 가속화는 의도파관 않은 임신의 지속적인 증가, 정책 주도로 인한 보험급여 확대, 소비자에 대한 접근성을 확대하는 원격의료 지원 프로바이더 네트워크의 확대와 함께 진행되고 있습니다. 경쟁 전략은 순수한 제품 차별화에서 기기 공급과 교육, 상담, 디지털 사후관리를 결합한 생태계 구축으로 전환되고 있으며, 보건부 및 NGO와의 다층적 파트너십을 구축할 수 있는 기업에게 유리하게 작용하고 있습니다. 동시에, 새로운 생분해성 폴리머 설계는 임플란트 제거에 따른 비용과 불안감을 없애고, 저자원 클리닉의 추가 수용량을 확대하는 것을 목표로 하고 있습니다.

국가 및 기부자 프로그램에 의한 다년 구매 계약이 확대됨에 따라 공공 예산 증가로 피임 임플란트 시장이 지속적으로 재편되고 있습니다. 미국 국제개발처(USAID)는 2024년 세계 가족계획에 6억 7,500만 달러의 예산 배정을 유지했으며, 임플란트는 그 공급량의 34%를 차지하여 안정적인 공급 기반을 구축했습니다. 캐나다의 법안 C-64는 임플란트를 포함한 피임 수단에 대한 보편적 보장을 도입하고, 기부자 자금과 국내 자금 모델의 수렴을 시사하고 있습니다. 이미 세계 최대 기부 피임기구인 유엔인구기금(UNFPA)은 이미 구축된 공급 네트워크를 통해 이러한 공적 예산을 활용하여 충분한 서비스를 받지 못하는 여성들에게 임플란트 공급을 우선순위에 두고 있습니다. 재정적 약속이 장기화됨에 따라 공급업체는 생산 라인 확장, 단가 인하, 장기 프레임 워크 계약 협상에 대한 명확성을 얻었습니다. 이러한 진화로 인해 정부 조달에서의 주도권 장악이 순수 제조 능력보다 결정적인 경쟁 우위로 자리매김하고 있습니다.

의도파관 않은 임신의 지속적인 증가는 거시경제 사이클이나 지역 소득 동향과 관계없이 기초적인 수요를 지탱하고 있습니다. 개트마커 연구소의 추정에 따르면 피임 자금 확충으로 연간 1,710만 건의 의도치 않은 임신을 예방할 수 있으며, 1달러의 지출에 대해 최대 6달러의 의료비 절감 효과를 기대할 수 있다고 합니다. 인도에서는 연간 4,800만 건의 임신 중 약 절반이 의도파관 않은 임신으로 기록되고 있으며, 이는 이 지역에서 지속형 피임법에 대한 미개발된 잠재적 수요를 지원하고 있습니다. 나이지리아의 의약품 접근성 구상(AMI) 시범사업에서 임플란트 도입률이 90% 증가했으며, 이는 의도파관 않은 임신의 측정 가능한 감소와 연계된 결과를 보여 직접적인 영향 경로를 입증했습니다. 이러한 지표는 임플란트를 공중보건 예산의 임의적 개입 수단에서 비용 효율적인 필수품으로 격상시켜 피임 임플란트 시장을 구조적으로 방어적인 시장으로 자리매김하고 있습니다.

부작용에 대한 잘못된 정보가 디지털 채널을 통해 빠르게 확산되어 좋은 임상적 근거가 있음에도 불구하고 수요를 억제하고 있습니다. 가나 조사에서는 부작용에 대한 우려가 주요 억제요인으로 18%에서 26%로 상승하는 것으로 나타났습니다. 국제가족계획연맹은 불임과 삽입시 통증에 대한 오해를 불식시키기 위해 노력하고 있지만, 소셜미디어를 통한 체험담이 확산되는 속도에는 미치지 못하고 있습니다. 호주의 질적 조사에 따르면 임플란트 효과를 인정하는 여성들 사이에서도 부정적인 친구나 지인의 경험담이 의사의 조언보다 더 큰 영향력을 발휘하는 것으로 나타났습니다. 생분해성 유형은 제거시 불안감을 해소하지만, 용해 시점에 대한 새로운 교육 부담이 발생합니다. 이러한 인식의 역풍을 극복하기 위해서는 다각적인 이해관계자들의 지속적인 소통이 필수적입니다.

에토노게스트렐 제제는 다년간의 안전성 데이터, 안정적인 공급, 확립된 임상 프로토콜로 인해 2025년 피임 임플란트 시장에서 68.43%의 매출 점유율을 차지할 것으로 예측됩니다. 이러한 탄탄한 기반은 현금흐름을 보호하는 한편, 2027년 이후 예상되는 특허 만료에 영향을 받기 쉬운 측면이 있습니다. 생분해성 후보 제품은 2031년까지 연평균 복합 성장률(CAGR) 5.72%를 보일 것으로 예측되며, 체내 용해 특성은 환자와 의료진 모두에게 제거 부담을 덜어줄 수 있습니다. 현재 임상 1상 평가 중인 Casea S는 분해 가능한 폴리(ε-카프로락톤) 골격을 채택하여 18-24개월 후 예측 가능한 분해 순서를 시작하면서 치료제의 지속적 방출을 유지합니다.

방사선 불투과성 폴리(ε-카프로락톤) 첨가제 개발로 영상 진단시 가시성 부족을 해소하고 삽입 확인시 의료진의 확신도 향상에 기여하지만, 새로운 규제 문서 요구사항이 발생합니다. 상하이 다화(Shanghai Dahua)는 2년 동안 30개국에 600만개 이상의 WHO 인증 임플란트를 공급하며 비용 효율성이 뛰어난 레보노르게스트렐 제제의 확장 가능성을 보여주었습니다. 예측 기간 중 생분해성 화학 기술을 습득하고 사전 인증을 확보한 선행 기업이 신규 조달 물량의 대부분을 차지하여 현재 에토노제스트렐의 우위를 점진적으로 잠식해 나갈 것으로 보입니다.

북미는 2025년 전 세계 매출의 37.50%를 차지할 것으로 예상되며, 성숙한 상환 시스템, 고도로 훈련된 의료 서비스 프로바이더, 안정적인 공중 보건 자금에 힘입어 성장세를 보이고 있습니다. 시장 확대는 현재 지방 군에 여전히 존재하는 피임 수단 부족 지역에 대한 대응에 의존하고 있습니다. 캐나다에서는 곧 시행될 전국민 의료보험제도로 인해 본인부담금 격차가 해소되고, 조달량 증가가 예상됩니다. 미국에서는 수요가 많은 지역의 지속적인 접근성 격차에 대한 직접적인 대응책으로 오가논의 'Her Plan is Her Power' 프로그램에 따라 원격의료 및 모바일 아웃리치 보조금을 시범적으로 도입하고 있습니다. 멕시코가 북미 의약품 공급망에 통합됨에 따라 저비용의 위탁 생산 옵션이 생겨 지역적 가격 상승을 억제할 수 있습니다.

아시아태평양은 인구 압력과 정책 추진력을 배경으로 2031년까지 연평균 복합 성장률(CAGR) 6.55%로 가장 빠르게 성장하는 지역입니다. 중국에서는 상하이 Dahua가 주도하는 대규모 피임 임플란트 생산기지가 수백만 개를 수출하는 동시에 도시 지역 증가하는 국내 수요에 대응하고 있습니다. 인도에서는 높은 비의도적 임신율과 비용 효율성이 새로운 정부 입찰을 지원하고 있으며, 도시 지역을 넘어 피임 임플란트 보급이 확대될 것으로 예측됩니다. 호주와 일본은 임상 기준에서 서유럽와 거의 동등한 수준으로 운영되고 있으며, 생분해성 시제품의 초기 도입 시험장 역할을 하고 있습니다. 인도네시아, 베트남, 필리핀의 급속한 인프라 현대화는 다층적인 조달 수요를 창출하고 있으며, 공급의 민첩성이 중요해졌습니다.

유럽은 안정적 전망을 보이고 있으며, 유럽의약품청(EMA)의 조화(harmonization)로 인해 다국가 출시가 간소화되었습니다. EMA는 임플라논의 위험-편익 프로파일이 여전히 양호한 것으로 확인하여 안전성 우려를 완화하고 각국의 의약품 리스트에 계속 등재하는 것을 지지하고 있습니다. 독일은 법정 건강 보험을 활용하여 의료기기와 상담 모두에 대한 보험금 지급을 통해 의료 프로바이더의 매출 예측 가능성을 유지하고 있습니다. 영국에서는성 생식 의학 학회의 개정된 가이드라인을 통해 기술 및 사후관리가 표준화되었고, 제조업체의 교육 자원이 효율화되었습니다. 남유럽 국가에서는 비용 대비 효과가 높은 레보노르게스트렐 제제를 우선적으로 사용하는 지역 공중보건 캠페인을 통해 LARC 보급률 격차를 해소하고 있습니다.

중동 및 아프리카에서는 기부자 자금, NGO의 보급 활동, 신흥 정부 예산이 상호 작용하고 있습니다. 나이지리아의 의약품 접근성 구상(AMI) 시범사업에서 수요 창출과 연계된 배포를 통해 극적인 보급이 입증되었습니다. 남아공에서는 청소년층의 임플란트 선택권 확대를 위해 성과연동형 자금조달(RBF)에 대한 검토가 진행되고 있습니다. 프랑스어권 서아프리카에서는 유엔인구기금(UNFPA)과 마리스토프에 의한 상품 공급에 의존하면서도 경제 성장에 따른 재정 여력 확대에 따라 국내 조달에 대한 관심이 높아지고 있습니다.

남미는 여전히 2차적이지만 성장하는 시장이며, 브라질과 아르헨티나에서는 공공 의료 네트워크의 임플란트 보험 적용 범위가 확대되고 있습니다. 칠레의 디지털 헬스 정책은 원격 상담과 원격 후속 조치를 강조하고 있으며, 이웃 국가들이 모방할 수 있는 선례를 만들고 있습니다.

Subdermal Contraceptive Implants market size in 2026 is estimated at USD 1.0 billion, growing from 2025 value of USD 0.96 billion with 2031 projections showing USD 1.21 billion, growing at 3.91% CAGR over 2026-2031.

This moderate expansion reflects the transition of long-acting reversible contraception from a niche alternative to a mainstream family-planning staple as public purchasers, insurers, and donors raise implant budgets. Government allocations such as the USAID family-planning envelope of USD 607.5 million in 2024, with implants accounting for 34% of the contraceptive value delivered, have established predictable demand pipelines that enable manufacturers to optimize output and pricing. Accelerated adoption further aligns with a sustained uptick in unintended pregnancies, policy-driven reimbursement gains, and telehealth-enabled provider networks that widen consumer reach. Competitive strategies have shifted from pure product differentiation toward ecosystem building that couples device supply with training, counseling, and digital follow-up, favoring firms capable of forging multi-level partnerships with health ministries and NGOs. At the same time, emerging biodegradable polymer designs aim to remove the cost and anxiety associated with implant removal, opening incremental addressable volumes among low-resource clinics.

Escalating public budgets continue to reshape the subdermal contraceptive implants market as national and donor programs expand multi-year purchasing agreements. USAID sustained a USD 607.5 million allocation for global family planning in 2024 and implants represented 34% of the value delivered, cementing a stable volume foundation. Bill C-64 in Canada introduces universal contraceptive coverage that includes implants, signaling the convergence of donor and domestic funding models. UNFPA, already the largest global distributor of donated contraceptives, leverages these public budgets through established supply networks that prioritize implants for underserved women. As fiscal commitments lengthen, suppliers gain clarity to scale production lines, reduce per-unit costs, and negotiate long-term framework contracts. This evolution positions government procurement mastery as a decisive competitive edge over pure manufacturing prowess.

A persistent surge in unintended pregnancies sustains baseline demand irrespective of macro cycles and local income trends. The Guttmacher Institute estimates that expanded contraception funding can prevent 17.1 million unintended pregnancies every year while returning up to USD 6 in health savings for each dollar spent. India records nearly half of its 48 million annual pregnancies as unintended, reinforcing the region's untapped potential for long-acting solutions. Outcomes from Access to Medicines Initiative pilots in Nigeria showed a 90% rise in implant uptake that paralleled measurable drops in unintended pregnancies, underscoring direct impact pathways. These metrics elevate implants from optional interventions to cost-saving necessities in public health budgeting and frame the subdermal contraceptive implants market as structurally defensive.

Misinformation about side effects spreads rapidly through digital channels and suppresses demand despite favorable clinical evidence. A Ghana survey found fear of side effects rising from 18% to 26% as the leading deterrent. The International Planned Parenthood Federation counters myths around fertility loss and insertion pain yet struggles to match the viral traction of anecdotal social posts. Qualitative studies in Australia show negative peer narratives can overrule clinician advice, even among women who acknowledge implant efficacy. Biodegradable formats address removal fears but add new educational burdens about dissolution timelines. Sustained multi-stakeholder communication remains essential to reverse perception headwinds.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Etonogestrel devices dominated the subdermal contraceptive implants market with 68.43% revenue share in 2025, thanks to long-standing safety data, consistent supply and embedded clinical protocols. This entrenched base protects cash flows but also heightens vulnerability to patent cliffs anticipated after 2027. Biodegradable candidates are accelerating at a 5.72% CAGR to 2031, and their ability to dissolve in situ directly addresses removal fatigue among both patients and providers. Casea S, currently in Phase I evaluation, applies a degradable poly(ε-caprolactone) backbone that triggers a predictable breakdown sequence after 18-24 months while sustaining therapeutic release .

Development of radiopaque poly(ε-caprolactone) additives solves imaging visibility gaps and supports clinician confidence during insertion verification, though it introduces new regulatory documentation requirements. Shanghai Dahua showcased the scaling potential of cost-efficient levonorgestrel variants by distributing over 6 million WHO-qualified implants to 30 nations in two years. Over the forecast horizon, first movers that master biodegradable chemistry and secure prequalification are likely to capture a disproportionate share of incremental procurement lots, gradually eroding the current etonogestrel advantage.

The Subdermal Contraceptive Implants Market Report is Segmented by Product Type (Etonogestrel Implants, Levonorgestrel Implants, Biodegradable Next-Gen Implants), End User (Hospitals, Specialty & Family-Planning Clinics, Community Health Centers, NGO & Government Programs), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America commanded 37.50% of global revenue in 2025, anchored by mature reimbursement systems, well-trained providers and steady public health funding. Market expansion now relies on addressing contraceptive deserts that persist in rural counties. Canada's impending universal coverage law is expected to rebalance pay-out-of-pocket disparities and stimulate higher volume procurement. The United States continues to pilot telehealth and mobile outreach grants under Organon's "Her Plan is Her Power" program, a direct response to persistent access gaps in high-need communities. Mexico's integration into North American pharmaceutical supply chains creates lower-cost contract manufacturing options that can dampen regional price inflation.

Asia-Pacific is the fastest-growing territory at 6.55% CAGR to 2031, powered by demographic pressure and policy momentum. China hosts large-scale implant fabrication hubs led by Shanghai Dahua, exporting millions of units while meeting rising urban domestic demand. India's high unintended pregnancy incidence and favorable cost-utility findings underpin new government tenders that are poised to expand implant coverage beyond urban centers. Australia and Japan operate at near-parity with Western Europe in clinical standards and thus serve as early adopter test beds for biodegradable prototypes. Rapid infrastructure modernisation in Indonesia, Vietnam, and the Philippines will add layered procurement demand, making supply agility critical.

Europe presents a stable outlook, underpinned by European Medicines Agency harmonization that simplifies multi-country rollout. The EMA confirmed that Implanon's benefit-risk profile remains positive, tempering safety concerns and sustaining inclusion in national formularies. Germany leverages statutory health insurance to reimburse both device and counseling, sustaining predictable provider revenue. The United Kingdom's refreshed Faculty of Sexual and Reproductive Healthcare guidelines standardize technique and follow-up, streamlining training resources for manufacturers. Southern European nations continue to close LARC penetration gaps through regional public health drives that favor cost-efficient levonorgestrel products.

The Middle East and Africa region intertwines donor funds, NGO outreach, and emerging government budgets. Nigeria's Access to Medicines Initiative pilot showcases dramatic adoption once distribution is coupled with demand generation. South Africa explores results-based financing to widen implant choice among adolescents. Francophone West Africa leans on UNFPA and Marie Stopes for commodity supply, yet exhibits rising domestic procurement interest as economic growth improves fiscal space.

South America remains a secondary yet rising market, with Brazil and Argentina expanding insurance coverage for implants in public health networks. Chile's digital health agenda highlights tele-counseling and remote follow-up, creating precedents that neighboring countries may replicate.