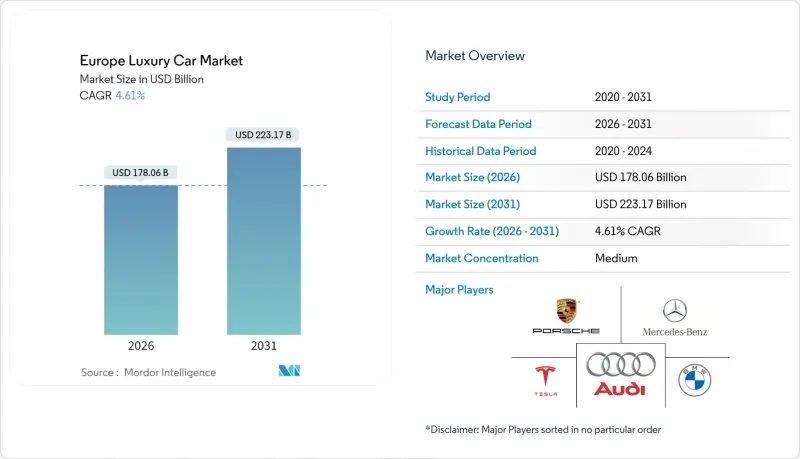

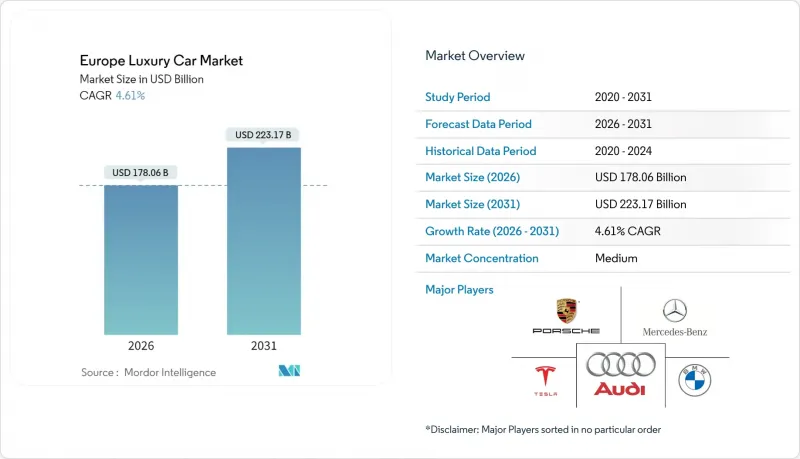

유럽의 고급차 시장은 2025년에 1,702억 1,000만 달러로 평가되었고, 2026년 1,780억 6,000만 달러에서 2031년까지 2,231억 7,000만 달러에 이를 것으로 예측됩니다. 예측 기간(2026-2031년) CAGR은 4.61%로 전망됩니다.

수요 회복력은 부유층 가구의 지속적인 자산 형성, 전통 제조업체가 구축한 탄탄한 브랜드 가치, 전동화 모델 투입을 가속화하는 지원적 정책 프레임워크에 기인합니다. 스포츠유틸리티차량(SUV)이 여전히 가장 큰 고객층을 확보하고 있지만, 쿠페와 컨버터블 차체 스타일에 대한 관심이 높아지면서 체험형 드라이빙에 대한 새로운 수요를 보여주고 있습니다. 배터리 전기 파워트레인으로의 전환이 가속화되고 있지만, 내연기관 차량이 여전히 판매량을 차지하고 있으며, 제조업체들은 규모의 경제와 규제 준수 사이에서 균형을 맞추어야 하는 상황에 처해 있습니다. 구독 및 기타 유연한 액세스 모델이 가장 빠르게 성장하고 있으며, 서비스 기반 모빌리티로의 세대적 전환을 반영하고 차량 내 디지털 기능과 연계된 새로운 수익원을 창출하고 있습니다.

부유한 유럽인들의 금융자산 축적은 계속되고 있으며, 잠재적인 고급차 구매층의 기반을 뒷받침하고 있습니다. 거시경제의 불확실성이 높아지는 가운데, 자산조사에 따르면 특히 스위스와 독일에서 초고액자산가(UHNWI)의 꾸준한 증가가 확인되고 있습니다. 이러한 소비자들은 독점적인 개인화, 최첨단 기술, 브랜드의 역사적 가치를 추구하며, 대중 시장 부문의 연화에도 불구하고 수요를 지탱하고 있습니다. 제조업체는 이 고객층이 선호하는 맞춤형 트림을 통해 높은 매출 총이익률을 얻고 있습니다. 경제력이 상위 소득층에 더욱 집중되는 가운데, 높은 구매력이 프리미엄 자동차 제조업체를 경기 침체로부터 보호하고 가격 결정력을 지탱하고 있습니다.

2026년 11월부터 시행되는 유로7 배기가스 규제에 따라 제조업체들은 고배기량 엔진을 단계적으로 폐지하고 배터리 전기차(BEV) 투입을 가속화할 수밖에 없습니다. 고급차 고객들은 첨단 기술을 일찍 채택하는 경우가 많으며, 성능 표준이 유지되는 한 전기차 운전에 대해 점점 더 긍정적으로 생각하고 있습니다. 자동차 제조업체들은 전용 EV 플랫폼, 고체 배터리 연구, 유럽 전역의 충전 인프라 연계에 많은 투자를 하고 있습니다. 규제 측면의 순풍과 지자체의 무공해 지역 정책이 맞물리면서 전시장 내 전기차의 비중이 높아지고 있습니다. 장기적으로 전기화는 배터리 공급망과 소프트웨어 정의 아키텍처를 장악하는 기업을 우대하는 방식으로 경쟁 구도를 재편할 것으로 예측됩니다.

지속적인 인플레이션은 실질 구매력을 약화시키고, 지정학적 긴장과 공급망 혼란은 소비자 심리를 불안정하게 만듭니다. 경기침체 위험이나 주식시장의 혼란을 알리는 뉴스가 나오면 고소득 가구도 임의지출을 늦추게 됩니다. 제조업체는 또한 배터리용 광물에서 반도체에 이르기까지 투입 비용의 상승에 직면하고 있으며, 이는 이익률을 압박하거나 판매 가격의 조정이 필요합니다. 통화정책이 안정되고인플레이션 기대감이 정착될 때까지 고급차 수요는 분기별로 변동이 있을 수 있습니다.

2025년 유럽의 고급차 시장에서 SUV의 점유율은 52.05%를 차지했습니다. 이는 높은 좌석 위치, 유연한 적재 용량, 모든 날씨에 대한 신뢰성 등의 특징이 부유한 가족이나 사업가들의 지속적인 지지를 받고 있다는 것을 반영합니다. 쿠페와 컨버터블 모델은 판매량이 적지만, 레저 여행의 회복과 소비자의 감성적인 운전 경험에 대한 수요 증가로 2031년까지 연평균 복합 성장률(CAGR) 6.09%로 확대될 것으로 예측됩니다. 이러한 표현력이 풍부한 부문의 성장은 최상위 계층 수요가 실용성과 라이프스타일의 정체성을 포괄하고 있음을 보여줍니다. 제조업체들은 포트폴리오의 폭을 넓히고, 플래그십 SUV와 한정 생산 스포츠 모델을 결합하여 브랜드의 매력을 강화하기 위해 노력하고 있습니다. 하이로쿠페에서 처음 선보인 디자인 요소와 기술은 판매량이 높은 크로스오버 차량에 자주 적용되어 전체 라인업의 통일감을 높이고 가격 책정력을 유지하고 있습니다.

세단의 전형적인 고급차로서의 지위는 지속되고 있지만, 구매자들이 스포츠 유틸리티의 실용성으로 이동함에 따라 점유율은 점차 압박을 받고 있습니다. 자동차 제조업체들은 첨단 운전 보조 시스템과 몰입형 인포테인먼트를 세단에 도입함으로써 그 존재 의미를 유지하고 있습니다. 다목적 차량(MPV)은 여전히 틈새 시장으로, 주로 대도시 지역의 운전자 동반 이용에 국한되어 있으며, 외관보다는 실내 공간을 중시하는 경향이 있습니다. 해치백은 동급에서 보기 드문 존재이지만, 주차공간이 제한된 혼잡한 도심지역에서 수요의 틈새를 찾아내고 있습니다. 차종 다양화로 유럽의 고급차 시장은 다양한 라이프스타일 니즈에 대응하면서 차별화된 차체 스타일로 수익성을 확보하고 있습니다.

내연기관차는 현재 75.62%의 출하 점유율을 차지하고 있으며, 기존 생산능력의 관성과 소비자의 익숙함이 그대로 드러나고 있습니다. 그러나 인프라 확충과 규제 기한이 다가옴에 따라 배터리 전기차는 2031년까지 연평균 복합 성장률(CAGR) 9.87%의 성장세를 이어갈 것으로 전망됩니다. 플러그인 하이브리드 자동차는 특히 지방의 장거리 통근자에게는 특히 귀중한 주행거리 걱정 없는 전기 주행 모드를 구매자에게 제공하는 가교 기술 역할을 합니다. 자동차 제조업체들은 가솔린, 하이브리드, 순수 전기차 등 다양한 차종에 연구개발비용을 분산하는 멀티 에너지 플랫폼을 개발하여 투자 위험을 헤지하고 있습니다.

유럽의 고급차 시장에서 BEV가 차지하는 비중은 고출력 충전 네트워크의 보급과 600km의 실주행거리를 자랑하는 그란투리스모 EV의 고급 브랜드 진출로 인해 매년 확대되고 있습니다. 소프트웨어로 조정 가능한 섀시 설정을 통해 전기차의 플래그십 모델은 기존에는 전용 V8 엔진이 담당했던 역동적인 특성을 재현할 수 있게 되었습니다. 그러나 일부 애호가층은 여전히 고성능 내연기관 파워트레인의 음향적, 촉각적 피드백을 중시하고 있어 배출가스 규제가 완전히 시행될 때까지 장기적인 공존이 보장됩니다. 이 두 가지 전략을 통해 제조업체는 내연기관 관련 자산의 상각 기간을 확보하는 동시에 차세대 배터리 프로그램에 자금을 투입할 수 있습니다.

The European luxury car market was valued at USD 170.21 billion in 2025 and estimated to grow from USD 178.06 billion in 2026 to reach USD 223.17 billion by 2031, at a CAGR of 4.61% during the forecast period (2026-2031).

Demand resilience stems from sustained wealth creation among affluent households, robust brand equity built by long-established manufacturers, and supportive policy frameworks accelerating electrified model launches. Sport utility vehicles (SUVs) continue to draw the largest customer base, while rising interest in coupe and convertible body styles reveals a renewed appetite for experiential driving. The transition toward battery-electric powertrains is gaining momentum, yet internal-combustion vehicles still dominate volumes, forcing producers to balance scale economics with regulatory compliance. Subscription and other flexible access models are expanding fastest, reflecting a generational shift toward service-based mobility and creating fresh revenue avenues tied to in-car digital features.

Affluent Europeans continue to accumulate financial assets, underpinning the addressable pool of potential luxury-car buyers. Despite broader macroeconomic uncertainty, wealth surveys show steady growth in ultra-high-net-worth cohorts, especially in Switzerland and Germany. These consumers seek exclusive personalization, state-of-the-art technology, and branded heritage, reinforcing demand even when mass-market segments soften. Manufacturers benefit from higher gross margins on bespoke trims that this clientele favors. As economic power concentrates further in the top income brackets, the purchasing buffer shields premium automakers from cyclical downturns and supports pricing power.

Euro 7 emissions limits, effective in November 2026, compel producers to phase out high-emitting engines and accelerate battery-electric launches. Luxury customers, often early adopters of advanced technology, are increasingly open to driving electric vehicles, provided performance benchmarks remain intact. Carmakers invest heavily in dedicated EV platforms, solid-state battery research, and pan-European charging alliances. The regulatory tailwind combines with municipal zero-emission zones to elevate electric models within showroom mixes. Over time, electrification is expected to reshape the competitive hierarchy by rewarding firms that master battery supply chains and software-defined architectures.

Persistent inflation erodes real purchasing power, while geopolitical tensions and supply-chain disruptions unsettle consumer sentiment. Even high-income households delay discretionary outlays when headlines signal recession risk or stock-market turbulence. Manufacturers also contend with higher input costs-ranging from battery minerals to semiconductors-that squeeze margins or require sticker-price adjustments. Premium car demand may progress unevenly across quarters until monetary policy stabilizes and inflation expectations anchor.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

SUVs represented 52.05% of the European luxury car market share in 2025, reflecting an enduring appeal for elevated seating, flexible cargo capacity, and all-weather confidence that resonates with affluent families and executives. Coupe and convertible nameplates, although smaller in volume, are enrolling a 6.09% CAGR to 2031 as leisure travel rebounds and consumers seek more emotive driving experiences. Growth in these expressive segments underscores that demand at the top encompasses practicality and lifestyle identity. Manufacturers expand portfolio breadth, pairing flagship SUVs with limited-run sports models that reinforce brand desirability. Design cues and technology debuted on halo coupes frequently cascade to high-volume crossovers, strengthening coherence across lineups and sustaining pricing power.

The sedan's archetypal luxury status endures yet faces incremental share pressure as buyers migrate toward sport-utility practicality. Automakers respond by injecting sedans with advanced driver assistance and immersive infotainment to preserve relevance. Multi-purpose vehicles remain a niche, mostly confined to chauffeur-driven use in select metropolitan areas where interior space overrides exterior presence. Although uncommon in this echelon, Hatchbacks find pockets of demand in congested cities that restrict parking footprints. Vehicle-type diversification ensures that the European luxury car market meets heterogeneous lifestyle needs while safeguarding margins through differentiated body styles.

Internal-combustion engines account for 75.62% of deliveries today, illustrating the inertia of legacy production capacity and consumer familiarity. However, battery-electric vehicles are pacing at a 9.87% CAGR through 2031 as infrastructure expands and regulatory deadlines near. Plug-in hybrids serve as a bridge technology, giving buyers an electric driving mode without range anxiety-especially valuable for rural long-distance commuters. Automakers hedge investments by deriving multi-energy platforms that spread R&D costs across gasoline, hybrid, and full-electric variants.

The European luxury car market size attributable to BEVs grows each year as high-capacity charging corridors become ubiquitous and luxury marques introduce grand-touring EVs boasting 600 km real-world range. Software-adjustable chassis settings allow electric flagships to replicate the dynamic character traditionally delivered by bespoke V-8 engines. Nevertheless, some connoisseurs still cherish the aural and tactile feedback of performance combustion powertrains, ensuring a prolonged coexistence until emission bans fully materialize. This twin-track strategy affords manufacturers time to amortize ICE assets while funding next-generation battery programs.

The European Luxury Car Market Report is Segmented by Vehicle Type (Hatchback, Sedan, and More), Powertrain Type (ICE, and More), Price Range (USD 45, 000-100, 000, USD 100, 001-200, 000, and Above USD 200, 000), Ownership Model (Outright Purchase, Finance/Lease, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).