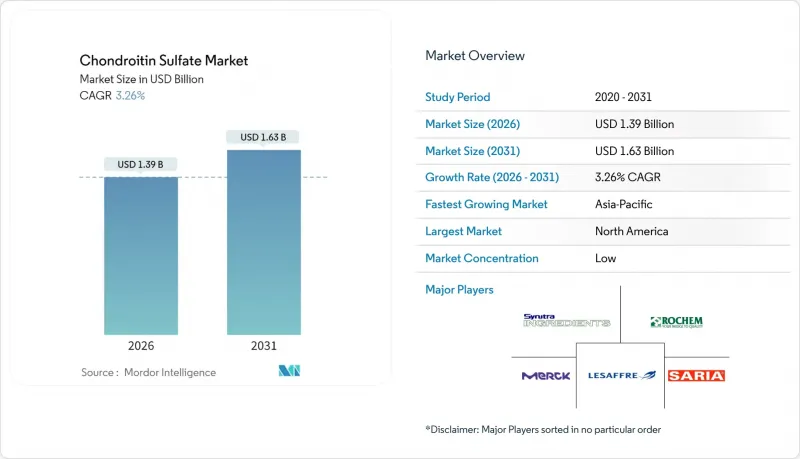

콘드로이틴 황산 시장은 2025년에 13억 5,000만 달러로 평가되었고, 2026년 13억 9,000만 달러에서 2031년까지 16억 3,000만 달러에 이를 것으로 예측됩니다. 예측 기간(2026-2031년) CAGR은 3.26%로 전망되고 있습니다.

이러한 꾸준한 성장 궤도는 45세 이상 성인의 골관절염 급증, 동물성 원료에 대한 압력 증가, 그리고 제약 등급 원료가 업계 표준으로 자리매김하는 임상적 효능의 확대로 인해 형성되고 있습니다. 합성 및 발효 기반 생산 기술 혁신의 가속화는 장기적인 공급 안정성을 뒷받침하고, 콜라겐, 히알루론산 또는 보스웰리아 세라타와의 복합 제제는 적용 범위를 확장하고 있습니다. 경쟁 전략에서는 원료의 품질 관리와 고급 제품에 유리한 규제 차별화를 활용하기 위해 수직적 통합이 점점 더 강조되고 있습니다. 이와 함께 성장 기회가 예상되는 것은 아시아태평양의 제조 능력으로, 수출 시장을 지원하고 주기적으로 세계 공급을 압박하는 원자재 가격 변동을 완화할 수 있습니다.

평균 수명 연장과 45세 이상 인구 증가로 인해 의약품용 콘드로이틴 황산에 대한 수요가 지속되고 있습니다. 미국에서는 3,250만 명의 성인이 골관절염을 앓고 있으며, MOVES 임상 등 대규모 임상시험에서 6개월 투여 시 셀레콕시브와 동등한 효과를 확인했습니다. 아시아태평양도 이와 유사한 인구통계학적 변화를 반영하여 건강기능식품에 대한 수요 증가가 가속화되고 있습니다. 최근 컬 선충을 이용한 연구에서 내인성 콘드로이틴이 2배 증가하면 수명이 30.6% 연장되는 것으로 나타나 예방의학으로서의 자리매김에 부합하는 기전 검증이 추가되었습니다. 근골격계 질환이 전 세계 장애 원인 순위에서 상승하는 가운데, 의료 시스템은 복합 치료 관리에 콘드로이틴 황산을 채택하고 있으며, 이 촉진요인은 장기적인 기반이 되고 있습니다.

예방적 셀프케어의 추세에 따라 제약 분야의 지식이 일반의약품으로 전환되면서 관절 건강 보조식품 세계 시장 규모는 1,000억 달러를 돌파했습니다. 아시아태평양의 중산층 소비자들은 콘드로이틴 황산 분말, 과립, 츄어블 정제를 일상적으로 섭취하고 있으며, 콜라겐 및 보스웰리아 세라타와 결합하여 최소 5일 만에 통증을 완화하는 복합 제품에 매력을 느끼고 있습니다. 의약품 등급과 식품 등급의 표준화 격차는 여전히 존재하지만, 프리미엄 건강 보조 식품이 이 차이를 메우고 있으며, 브랜드는 USP 수준의 순도를 주장하며 높은 가격대를 정당화하고 있습니다.

가축의 질병 주기, 도축장 가동 중단, 상어 연골에 대한 CITES 규제로 인해 원재료 공급이 주기적으로 제한되어 비용이 상승하고 있습니다. 제조업체는 여러 유형의 원료 조달과 재고 증가로 리스크 헤지를 위해 노력하고 있지만, 이로 인해 운전자금 수요가 증가하고, 최종 사용자의 가격 부담도 증가하고 있습니다. 합성 경로와 발효 기술은 이러한 위험을 줄이기 위해 통제된 바이오프로세스에 대한 전략적 설비 투자를 촉진하고 있습니다.

2025년 매출에서 돼지 연골은 성숙한 공급망과 경쟁력 있는 가격 설정에 힘입어 25.12%를 차지할 것으로 예측됩니다. 한편, 합성 제품의 점유율은 여전히 10% 미만이지만, 5.81%의 연평균 복합 성장률(CAGR)로 급성장하고 있습니다. 유전자 재조합 대장균을 이용한 발효 시스템에서는 48시간 만에 99%의 순도를 달성했습니다. 이 공정은 약전 테스트를 충족하는 균일한 황산화 패턴을 생성하여 내독소 위험을 크게 줄입니다. 이러한 전환은 에코라벨, 코셔/할랄 수요, 비건 대응과 일치하며, 선도 기업에게 평판 측면에서 우위를 가져다 줄 수 있습니다. 소 연골은 여전히 중요하지만, BSE(소해면상뇌증)에 대한 우려를 인증 조달로 관리할 필요가 있습니다. 상어 연골은 CITES(멸종위기에 처한 야생 동식물 종의 국제거래에 관한 협약)의 규제 확대에 따라 지속적으로 감소하고 있으며, 조류 연골은 종교적 요건을 충족하는 제제를 위한 틈새 시장을 유지하고 있습니다.

가격 동향은 트레이드오프를 보여줍니다. 합성 제품의 Kg당 비용은 현재 소에서 유래한 기준치보다 높지만, 정제 손실 감소와 환경 프리미엄이 그 차이를 좁히고 있습니다. 발효기 용량 확대에 따른 규모의 경제가 추진되어 2031년까지 합성품의 점유율은 15.3%에 육박할 것으로 예상되며, 역사적으로 수익률을 압박했던 원재료 가격 급등도 완화될 것으로 보입니다.

의약품 등급 제품은 2025년 시장 가치의 49.62%를 차지할 것으로 예상되며, 임상적 근거가 강화되고 보험 적용이 확대됨에 따라 프리미엄 가격이 확대되고 있습니다. MOVES 시험 결과, 셀록록시브와 동등한 효과를 확인했으며, 위장장애 부작용이 없는 것으로 나타났습니다. 식품 등급 제제에 기인한 콘드로이틴 황산 시장 규모는 예방적 관절 관리에 대한 소비자의 지불 의향을 반영하여 CAGR 5.18%로 확대되고 있습니다. 화장품 등급은 여전히 소규모 부문이며, 보습 효과를 목적으로 하는 안티에이징 세럼에 배합되어 있습니다.

제약 제조업체는 ICH를 완전히 준수하는 품질 관리 시스템, 배치 릴리스 분석, 추적 가능한 공급망을 갖추고 있으며, 소규모 식품 등급 공급업체는 종종 부족한 요소를 갖추고 있습니다. 그러나 USP 인증 제품 라인으로 이 차이를 메우는 건강기능식품 브랜드는 특히 투명성을 중시하는 EC 채널을 통해 제품의 매력을 높이고, 높은 가격대의 정당성을 확립하고 있습니다. 따라서 규제의 단계적 적용은 불침투성 장벽이라기보다는 유능한 식품 등급 기업이 처방 시장으로 진출할 수 있는 통로 역할을 할 것입니다. 단, 검증에 리소스를 할당하는 것을 전제로 합니다.

북미는 2025년 매출의 38.62%를 차지할 것으로 예상되며, 처방용 콘드로이틴 황산의 보험 적용, 대규모 골관절염 환자층, 확립된 건강기능식품 소매 채널이 기반이 됩니다. 식품용 GRAS(일반적으로 인정된 안전성) 인증과 FDA의 순도 기준 지침이 소비자 신뢰를 강화했지만, 소송 위험으로 인해 제조업체는 고정밀 분석에 대한 투자를 계속하고 있습니다. 이 지역의 안정적이면서도 완만한 2.78%의 연평균 복합 성장률(CAGR)은 이 지역의 성숙도를 반영합니다.

아시아태평양은 6.54%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장하고 있으며, 중국과 인도의 생산능력 확대가 국내 수요와 수출 수요를 모두 뒷받침하고 있습니다. 인구 고령화와 전통의학에 대한 수용성이 맞물려 과립형 콘드로이틴 황산을 용해하는 소포장 스틱과 발포성 음료의 보급이 가속화되고 있습니다. 일본에서 요추 추간판탈출증 치료제 콘드리아제의 임상적 수용은 치료법의 다양화를 더욱 촉진하고 있습니다.

유럽에서는 13개국에서 의료용 의약품으로 승인되어 의사들이 심혈관 위험 감소를 위해 NSAIDs 대신 의약품 등급의 콘드로이틴 황산을 처방하고 있습니다. 남유럽의 건강보조식품 소비자들은 지중해 식물 성분을 함유한 복합제형을 선호합니다. 남미와 중동 및 아프리카은 뒤쳐져 있지만, 현지 유통업체가 유럽 원료의약품 공급업체와 라이선스 계약을 체결하고 민간 클리닉과 고급 약국에 대한 판매망을 확대하면서 중등도의 한 자릿수 CAGR을 기록하고 있습니다. 표시 규정과 할랄 인증의 지역적 차이로 인해 제품 출시 시기가 계속 영향을 받고 있습니다.

The chondroitin sulfate market was valued at USD 1.35 billion in 2025 and estimated to grow from USD 1.39 billion in 2026 to reach USD 1.63 billion by 2031, at a CAGR of 3.26% during the forecast period (2026-2031).

This steady trajectory is shaped by the rapid rise in osteoarthritis among adults over 45, mounting pressure on animal-derived sources, and growing clinical validation that positions pharmaceutical-grade material as the industry benchmark. Intensifying innovation around synthetic and fermentation-based production underpins long-term supply security, while combination formulations with collagen, hyaluronic acid or Boswellia serrata broaden application breadth. Competitive strategies increasingly emphasize vertical integration to control raw-material quality and leverage regulatory differentiation that rewards higher-grade offerings. Parallel growth opportunities lie in Asia-Pacific manufacturing capacity, which supports export markets and mitigates raw-material price swings that periodically tighten global supply.

Rising life expectancy and a larger cohort of adults over 45 sustain demand for pharmaceutical-grade chondroitin sulfate, with osteoarthritis affecting 32.5 million U.S. adults. Large-scale trials such as MOVES confirmed efficacy comparable to celecoxib over six-month regimens. Asia-Pacific mirrors this demographic wave, magnifying nutraceutical uptake. Recent C. elegans work showing 30.6% lifespan extension when endogenous chondroitin doubled adds mechanistic validation that resonates with preventive-care positioning. With musculoskeletal disorders climbing the global disability chart, healthcare systems adopt chondroitin sulfate in multi-modal management, embedding this driver as a long-term pillar.

Preventive self-care trends convert pharmaceutical insights into over-the-counter formats, propelling joint-health supplements past USD 100 billion globally. In Asia-Pacific, middle-class consumers integrate chondroitin sulfate powders, granules and chewables into daily routines, attracted by combination formats that cut pain in as few as five days when paired with collagen and Boswellia serrata. Standardization gaps still differentiate pharmaceutical-grade from food-grade, but premium nutraceuticals bridge this divide as brands tout USP-level purity to justify higher price points.

Livestock disease cycles, slaughterhouse shutdowns and CITES constraints on shark cartilage periodically curtail raw-material flows and elevate costs. Manufacturers hedge through multi-species sourcing and higher inventories, which lift working-capital requirements and price tags for end users. Synthetic pathways and fermentation reduce this exposure, encouraging strategic capex toward controlled bioprocessing.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

2025 revenue shows swine cartilage at 25.12%, supported by mature supply chains and competitive pricing. Yet synthetic output, still below 10% share, races ahead at a 5.81% CAGR. Fermentation systems using engineered E. coli achieve 99% purity in 48 hours. This process yields consistent sulfation patterns that satisfy pharmacopoeia tests and greatly reduce endotoxin risk. The pivot aligns with eco-labeling, kosher/halal demand and vegan positioning, granting first movers a reputational moat. Bovine cartilage remains relevant but must manage BSE perception through certified sourcing. Shark cartilage continues to fall as CITES listings expand, and avian cartilage holds niche status for religious-compliance formulations.

Pricing dynamics illustrate the trade-off: synthetic costs per kilogram currently exceed bovine benchmarks, yet lower purification losses and environmental premiums narrow the gap. As expanded fermenter capacity drives economies of scale, synthetic share is projected to approach 15.3% by 2031, moderating raw-material price spikes that historically pinched margins.

Pharmaceutical-grade products contributed 49.62% of 2025 value and command a widening premium amid stronger clinical evidence and reimbursement recognition. MOVES trial outcomes showed equivalence to celecoxib without gastrointestinal side effects. The chondroitin sulfate market size attributable to food-grade formulations climbs at 5.18% CAGR, reflecting consumer willingness to pay for proactive joint care. Cosmetics-grade remains a micro-segment, integrated in anti-aging serums for moisture retention.

Pharmaceutical manufacturers showcase full ICH-compliant quality systems, batch-release analytics and traceable supply chains that smaller food-grade suppliers often lack. However, nutraceutical brands closing this gap with USP-verified product lines improve shelf appeal and justify higher price points, especially through e-commerce channels emphasizing transparency. The regulatory gradient therefore acts less as an impermeable wall and more as a pathway for capable food-grade players to ascend into prescription markets, provided they allocate resources to validation.

The Chondroitin Sulfate Market Report is Segmented by Source (Bovine Cartilage, Porcine Cartilage, Shark Cartilage, Avian Cartilage, Synthetic, Other Sources), Grade (Pharmaceutical Grade, Food Grade, Cosmetics Grade), Form (Powder, Granules, and More), Application (Pharmaceuticals & OTC Drugs, Dietary Supplements, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America retains 38.62% of 2025 revenue, anchored by insurance coverage for prescription chondroitin sulfate, a large osteoarthritis patient pool and well-established nutraceutical retail channels. GRAS acceptance for food use and FDA guidance on purity thresholds reinforce consumer trust, though litigation risk keeps manufacturers invested in high-end analytics. The region's stable yet modest 2.78% CAGR reflects maturity.

Asia-Pacific rises fastest at 6.54% CAGR, propelled by capacity buildouts in China and India that feed both domestic and export demand. Aging demographics intersect with traditional medicine openness, accelerating uptake of sachet sticks and effervescent drinks that dissolve granulated chondroitin sulfate. Japanese clinical acceptance of condoliase for lumbar disc herniation further diversifies therapeutic landscapes.

Europe benefits from ethical-drug approvals across 13 countries, with physicians prescribing pharmaceutical-grade chondroitin sulfate in place of NSAIDs to mitigate cardiovascular risk. Southern European nutraceutical consumers favor combination formulas featuring Mediterranean botanicals. South America and Middle East & Africa trail but post mid-single-digit CAGR as local distributors negotiate licensing deals with European API suppliers, extending reach into private clinics and upscale pharmacies. Regional heterogeneity in labeling rules and halal certification continues to affect product-launch timelines.