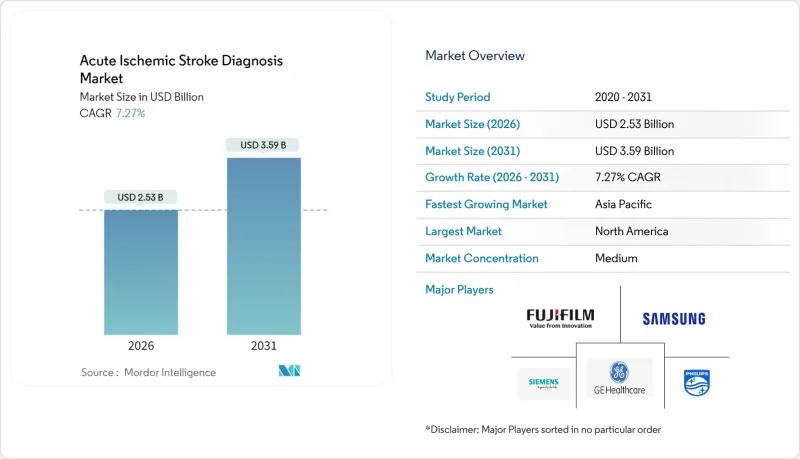

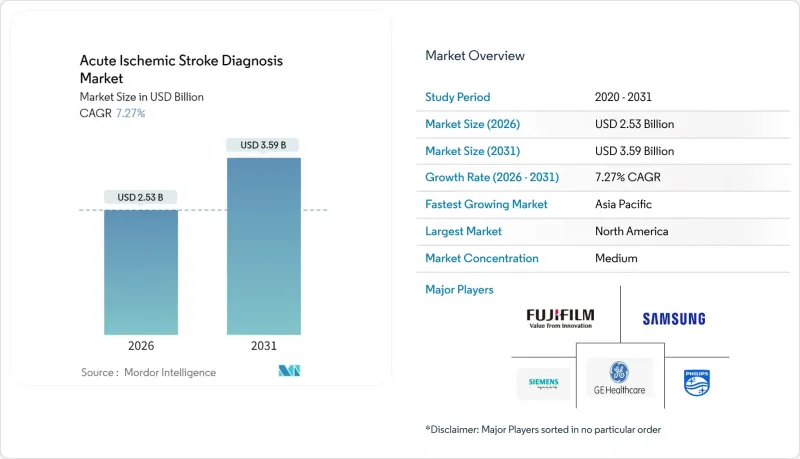

급성허혈성 뇌졸중 진단 시장 규모는 2026년에 25억 3,000만 달러로 추정되며, 이는 2025년 23억 6,000만 달러에서 성장한 것입니다.

2031년에는 35억 9,000만 달러에 달할 것으로 예상되며, 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 7.27%로 성장할 것으로 전망됩니다.

급성 허혈성 뇌졸중 진단 시장은 인구 고령화, 첨단 영상진단 프로토콜의 보급 확대, 임상적 판단을 빠르게 하는 인공지능(AI) 분류 시스템을 배경으로 확대되고 있습니다. AI를 활용한 대혈관 폐색 감지 기술은 진단의 해석 격차를 줄이고 민감도를 향상시키며, 이동형 뇌졸중 유닛은 미국 및 EU의 여러 연구에서 치료 지연 시간을 25-40분 단축시켰습니다. 기계적 혈전제거술 시간이 24시간까지 연장됨에 따라 관류 영상 진단 및 자동 ASPECTS 스코어링에 대한 수요가 증가하고 있습니다. 또한, 북미와 유럽에서는 가이드라인 준수와 보험급여를 연계하는 국가 차원의 품질향상 시책이 추진되고 있습니다. 스캐너 장비 투자 비용, 영상의학과 전문의 부족, 지방의 접근성 격차 등의 문제는 여전히 존재하지만, 각 벤더들은 구독형 AI 번들, 휴대용 CT 시스템, 원격 뇌졸중 네트워크와 같은 솔루션으로 이러한 장벽을 해결하고 있습니다.

세계적으로 평균 수명이 연장됨에 따라 뇌졸중 유병률이 급격히 증가하고 있습니다. 2021년판 '질병 세계 바덴' 모델에 따르면, 2050년까지 뇌졸중 발생 건수가 2,143만 건에 달할 것으로 예측했습니다. 고령 환자는 비전형적인 증상과 여러 동반 질환을 가지고 있는 경우가 많아 병원들은 신속한 영상 진단과 AI 지원 진단 플랫폼에 대한 투자를 진행하고 있습니다. 일본과 한국에서는 후생노동성이 연령별 검진 목표를 설정하여 조기 영상진단을 장려하고 있으며, 이는 급성 허혈성 뇌졸중 진단 시장 전체에서 검사기기 이용이 지속적으로 증가하는 요인으로 작용하고 있습니다.

현재 종합뇌졸중센터에서는 비조영 CT와 CT 조영술, CT 혈관조영술, CT 퍼퓨전, 확산강조 MRI를 조합하여 구제가 가능한 반영상을 확인하는 것이 표준화되어 있습니다. 이러한 멀티모달 프로토콜은 여러 시퀀싱 데이터를 몇 초 만에 통합하는 AI 엔진에 의해 강화되어 민감도를 높이고 위양성을 감소시킵니다. 각 벤더들은 관류지도, 혈관폐색 오버레이, 자동 ASPECTS를 단일 콘솔 디스플레이에 통합하여 워크플로우의 효율성을 높이고 있습니다. 독일, 미국, 호주 등에서는 멀티모달 영상진단에 대한 보상 정책을 시행하고 있으며, 이는 급성 허혈성 뇌졸중 진단 시장 전반에 걸쳐 도입을 촉진하고 하드웨어 업데이트 주기를 앞당기는 데 기여하고 있습니다.

뇌졸중 프로토콜을 지원하는 최고급 CT 및 MRI 플랫폼은 100만-300만 달러의 비용이 소요되며, 연간 유지보수 계약 비용은 구매 가격의 최대 12%를 차지합니다. 인도네시아, 나이지리아, 페루의 병원에서는 자본 배분이 기초 인프라에 집중되어 있어 조달 지연이 보고되고 있습니다. 미국에서는 2000년부터 2019년까지 메디케어의 주요 뇌졸중 시술에 대한 인플레이션 조정 후 상환액이 11.2% 감소하여 의료 서비스 제공업체의 수익률을 압박하고 있습니다. 현재 업체들은 임대 또는 스캔당 지불 옵션을 제공하고 있지만, 저렴한 가격 책정은 급성 허혈성 뇌졸중 진단 시장의 광범위한 보급에 가장 큰 장벽으로 작용하고 있습니다.

컴퓨터 단층촬영(CT)은 2025년 매출의 37.52%를 차지하며 급성 허혈성 뇌졸중 진단 시장의 선두주자로서의 입지를 확고히 하고 있습니다. 조영제를 사용하지 않는 CT는 3분 이내에 출혈을 신속하게 배제할 수 있으며, CT 혈관 조영술은 같은 세션에서 혈관 폐쇄 부위를 식별할 수 있습니다. 종합병원에서 CT 시퀀싱의 급성 허혈성 뇌졸중 진단 시장 규모는 검출 민감도 향상과 워크플로우 효율화를 가져오는 AI 라이선스 번들화로 인해 6.78%의 연평균 복합 성장률(CAGR)로 확대될 것으로 예측됩니다. 초음파 검사(특히 경동맥 및 경두개 도플러)는 이동식 뇌졸중 치료실과 저재원 병원이 휴대용 및 방사선 비조사 도구를 필요로 하기 때문에 7.98%의 가장 빠른 CAGR을 나타낼 것으로 예측됩니다.

자기공명영상(MRI)은 여전히 가장자리 영역 매핑에 필수적입니다. 확산강조영상 및 동맥 스핀 표지 시퀀싱는 CT에서 판단이 어려운 경우 경색 중심부와 치료 가능한 조직을 구분하여 치료 방침을 결정합니다. GFAP-D 다이머와 같은 혈액 기반 바이오마커 패널은 현재 93%의 특이도를 달성하여 병원 전 선별 패러다임 전환을 가져올 수 있지만, 아직 임상시험 단계에 있습니다. 디지털 감산 혈관조영술은 복잡한 혈관 내 치료 계획에 국한되어 있지만, AI 전용 의사결정 지원 소프트웨어는 급성 허혈성 뇌졸중 진단 시장에서 독립적인 수익원으로 부상하고 있으며, 여러 검사 데이터를 단일 임상 대시보드에 통합하는 플랫폼의 개발을 촉진하고 있습니다.

북미는 2025년 매출의 42.60%를 차지할 것으로 예상되며, 이는 성숙한 뇌졸중 네트워크와 AI의 빠른 도입을 반영합니다. 미국에서는 1,700개 이상의 병원이 6만여 명의 의료진에게 Viz.ai를 도입해 생태계의 깊이를 보여주고 있습니다. 텍사스의 이동형 뇌졸중 치료 유닛은 치료까지 걸리는 시간을 40분 단축하여 지방 환자 치료에 의미 있는 효과를 가져왔습니다. 뇌졸중 치료의 급여액은 감소 추세, 성과 개선을 평가하는 가치 기반 구매 제도로 인해 설비 투자 예산은 견조하게 유지되고 있으며, 급성 허혈성 뇌졸중 진단 시장 전체에서 기기 업데이트의 모멘텀이 지속되고 있습니다.

아시아태평양은 2031년까지 8.11%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측되며, 세계에서 가장 빠른 성장률을 보일 것으로 예측됩니다. 이는 고령화 속도가 빨라지고 정부의 뇌졸중 치료 인프라가 확충된 것이 배경입니다. 중국의 뇌졸중 발생 건수는 1990년 76만 건에서 2021년 277만 건으로 증가하여 관류 평가가 가능한 CT 스캐너의 대량 조달을 촉진하고 있습니다. 일본의 국가 뇌졸중 등록제도에서는 현재 멀티모달 영상진단이 의무화되어 있습니다. 한편, 인도에서는 환자층이 젊어지고 있으며, 주요 연령층은 41-50세입니다. 인도네시아와 필리핀의 원격 뇌졸중 진료 시범사업은 전문의 부족과 지역적 제약을 기술로 보완할 수 있다는 정책적 인식을 보여주고 있습니다.

유럽에서는 AI 도구와 국경을 초월한 데이터 공유를 지원하는 2,690만 유로 규모의 'UMBRELLA 프로젝트' 등 협력적 연구에 힘입어 꾸준한 확장을 보이고 있습니다. 지멘스 헬스인어스, 세계뇌졸중기구와 협력하여 영상진단 프로토콜 표준화 추진. 이로 인해 중동부 유럽의 급성 허혈성 뇌졸중 진단 시장이 활성화되고 있습니다. 중동, 아프리카, 중남미은 인프라와 인력 부족으로 인해 뒤쳐져 있지만, 에티오피아의 공중보건 캠페인과 헝가리의 이동진료차량을 통한 노력은 자원이 부족한 환경에서도 표적화된 개입을 통해 진단 접근성을 향상시킬 수 있다는 것을 입증하고 있습니다.

acute ischemic stroke diagnosis market size in 2026 is estimated at USD 2.53 billion, growing from 2025 value of USD 2.36 billion with 2031 projections showing USD 3.59 billion, growing at 7.27% CAGR over 2026-2031.

The acute ischemic stroke diagnosis market is expanding on the back of population aging, widening adoption of advanced imaging protocols, and artificial-intelligence triage systems that speed clinical decision-making. AI-enabled large-vessel-occlusion detection has narrowed interpretation gaps and raised diagnostic sensitivity, while mobile stroke units have cut treatment delays by 25-40 minutes in several U.S. and EU studies. Extended mechanical-thrombectomy time windows out to 24 hours are driving demand for perfusion imaging and automated ASPECTS scoring, and national quality initiatives in North America and Europe are linking reimbursement to guideline adherence. Challenges persist around scanner capital costs, radiologist shortages, and uneven rural access, yet vendors are countering these hurdles with subscription AI bundles, portable CT systems, and tele-stroke networks.

Stroke prevalence is climbing sharply as global life expectancy rises. The Global Burden of Disease 2021 model projected stroke cases will reach 21.43 million by 2050. Elderly patients often present with atypical symptoms and multiple comorbidities, prompting hospitals to invest in rapid-sequence imaging and AI-assisted interpretation platforms. Health ministries in Japan and South Korea have set age-specific screening targets that encourage earlier imaging, supporting a durable uptick in modality utilization across the acute ischemic stroke diagnosis market.

Comprehensive stroke centers now routinely pair non-contrast CT with CT angiography, CT perfusion, and diffusion-weighted MRI to pinpoint salvageable penumbra tissue. These multimodal protocols, reinforced by AI engines that synthesize multi-sequence data in seconds, improve sensitivity and trim false positives. Vendors are streamlining workflow by integrating perfusion maps, vessel-occlusion overlays, and automated ASPECTS into a single console display. Reimbursement policies in Germany, the United States, and Australia have begun rewarding multimodal imaging, accelerating uptake and fueling hardware refresh cycles across the acute ischemic stroke diagnosis market.

Top-tier CT and MRI platforms equipped for stroke protocols cost USD 1-3 million, with annual service contracts consuming up to 12% of purchase price. Hospitals in Indonesia, Nigeria, and Peru report procurement delays because capital allocations focus on basic infrastructure. In the United States, Medicare's inflation-adjusted reimbursement for key stroke procedures fell 11.2% from 2000 to 2019, straining provider margins. Vendors now offer leasing and pay-per-scan options, yet affordability remains the biggest drag on broader penetration of the acute ischemic stroke diagnosis market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Computed tomography represented 37.52% of 2025 revenue, cementing its role as the frontline modality within the acute ischemic stroke diagnosis market. Non-contrast CT expedites hemorrhage exclusion in under 3 minutes, and CT angiography offers vessel-occlusion localization in the same session. The acute ischemic stroke diagnosis market size for CT sequences in comprehensive centers is projected to expand at a 6.78% CAGR on account of bundled AI licenses that raise detection sensitivity and streamline workflow. Ultrasound, specifically carotid and transcranial Doppler, is forecast to notch the quickest 7.98% CAGR as mobile stroke units and low-resource hospitals demand portable, radiation-free tools.

Magnetic resonance imaging remains vital for penumbral mapping. Diffusion-weighted and arterial-spin-labeling sequences differentiate core infarct from salvageable tissue, steering therapy when CT is inconclusive. Blood-based biomarker panels such as GFAP-D-dimer, now achieving 93% specificity, could shift prehospital triage paradigms but remain in clinical trials. Digital-subtraction angiography is reserved for complex endovascular planning, while AI-only decision-support software is emerging as a separate revenue line within the acute ischemic stroke diagnosis market, spurring integrated platforms that fuse modality data into a single clinical dashboard.

The Acute Ischemic Stroke Diagnosis Market Report Segments the Industry Into Diagnostic Technology (Computed Tomography, Magnetic Resonance Imaging, and More), End User (Hospitals, Diagnostic Imaging Centers, and More), and Geography (North America, and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

North America captured 42.60% revenue in 2025, reflecting mature stroke networks and rapid AI adoption. Over 1,700 U.S. hospitals deploy Viz.ai across 60,000 providers, illustrating ecosystem depth. Texas mobile stroke units achieved meaningful rural-patient benefit by shaving 40 minutes off treatment lag. Despite declining reimbursement for stroke procedures, capital budgets stay robust because value-based purchasing rewards outcome improvements, sustaining equipment refresh momentum throughout the acute ischemic stroke diagnosis market.

Asia-Pacific is set to post an 8.11% CAGR to 2031, the fastest worldwide, as aging rates accelerate and governments expand stroke-care infrastructure. China's incidence rose from 0.76 million in 1990 to 2.77 million in 2021, driving mass procurement of perfusion-capable CT scanners. Japan's national stroke registry now mandates multimodal imaging, while India confronts a younger patient profile, with the modal age band at 41-50 years. Tele-stroke pilots across Indonesia and the Philippines signal policy recognition that technology can offset specialist shortages and geography constraints.

Europe shows steady expansion underpinned by coordinated research, such as the €26.9 million UMBRELLA project that funds AI tools and cross-border data sharing. Siemens Healthineers partners with the World Stroke Organization to standardize imaging protocols, giving the acute ischemic stroke diagnosis market a boost in Central and Eastern Europe . Middle East & Africa and South America trail due to infrastructure and workforce deficits, yet Ethiopia's public-health campaigns and Hungary's mobile truck clinics prove that targeted interventions can lift diagnostic access even in low-resource settings .