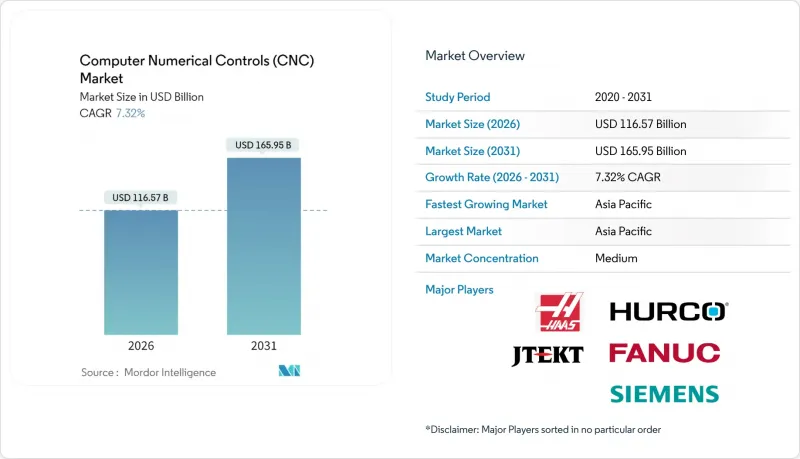

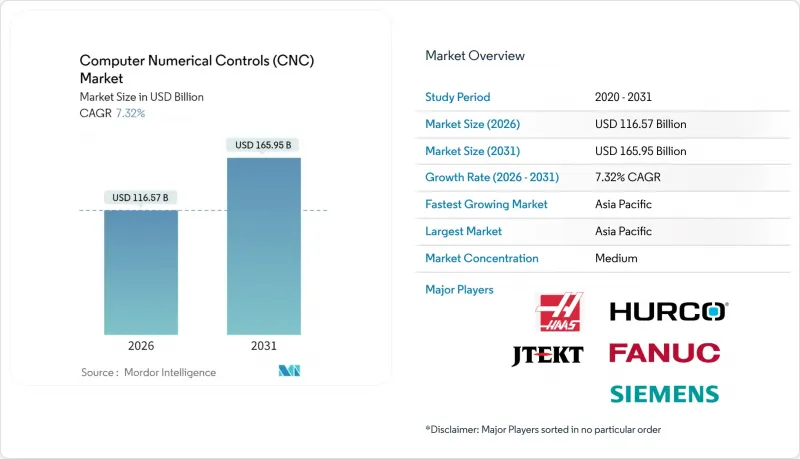

2026년 컴퓨터 수치제어(CNC) 시장 규모는 1,165억 7,000만 달러로 추정되며, 2025년 1,086억 3,000만 달러에서 성장하여 2031년에는 1,659억 5,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR)은 7.32%를 나타낼 것으로 예측됩니다.

지속적인 노동력 부족, 생산의 니어쇼어링, 그리고 인더스트리 4.0의 자동화 추진과 함께 제조업체들은 다축 가공 및 디지털 연결 장비에 대한 투자를 가속화하고 있습니다. 미국이나 유럽의 리쇼어링 관련 법은 자본을 저비용 지역으로부터 생산의 단납기를 실현할 수 있는 유연한 가공설비로 이동시키고 있습니다. 연결성이 향상됨에 따라 사이버 보안 위험도 증가하고 있으며, 벤더들은 새로운 컨트롤러에 보안 바이 디자인(Security by Design) 기능을 통합하도록 동기를 부여하고 있습니다. 동시에 철강 및 알루미늄 가격의 고공행진은 스크랩을 최소화하는 정밀 가공 공정에 대한 수요를 견인하고 있습니다. 이러한 요인들이 결합되어 부품 부족으로 인한 단기적인 공급 마찰에도 불구하고 컴퓨터 수치 제어(CNC) 시장은 견고한 성장 궤도를 유지하고 있습니다.

2023년 미국의 중국산 완제품 수입은 13% 감소한 반면, 인프라 및 반도체 산업에 대한 특혜 조치로 인해 국내 공장 투자가 급증했습니다. 수주 상황은 변동이 심하기 때문에 구매자는 다양한 부품군에 대응할 수 있는 적응성이 높은 5축 가공기나 모듈형 로봇 셀을 선호합니다. 시장과 가까운 생산 기지는 운송 위험 감소와 납기 단축을 통해 높은 자본 지출을 정당화합니다. 신속한 재공구화 및 디지털 설정 기능을 제공하는 업체는 경쟁 우위를 확보할 수 있습니다. 이러한 리쇼어링의 움직임은 수십 년에 걸친 외주 생산량을 현지 생산 능력의 확대로 전환함으로써 컴퓨터 수치제어(CNC) 시장을 직접적으로 확대할 수 있습니다.

디지털 트윈을 통해 프로그래머는 공구 경로를 가상으로 검증할 수 있으며, 지멘스 Sinumerik 828D 하드웨어를 통해 물리적 설정 시간을 20% 단축할 수 있습니다. 연구에 따르면, 기계가 가상 대조군과 폐루프 연동으로 작동할 경우 생산성이 14.53% 향상되고 에너지 사용량이 13.9% 감소하는 것으로 나타났습니다. 열 드리프트와 공구 마모에 대한 실시간 보정이 필요한 항공우주 및 자동차 분야에 가장 많이 도입되고 있습니다. 제어장치 공급업체들은 클라우드 연결성과 AI 분석 기능을 통합하여 CNC 시장을 소프트웨어 중심의 영역으로 변화시키고 있습니다. 라이선스 수익이 증가함에 따라 기계 제조업체들은 일시적인 하드웨어 수익률보다 지속적인 수익원을 중요시하는 경향이 있습니다.

정밀 서보 드라이브는 특수 ASIC에 의존하고 있지만, 공급 부족이 계속되고 있으며, 고급 기계의 리드 타임은 9개월 이상 연장되고 있습니다. 일부 제조업체는 사용 가능한 칩으로 설계 변경을 하고 있지만, 이를 위해서는 고가의 재인증이 필요합니다. 할당량을 확보한 OEM은 점유율을 확보하는 반면, 후발주자들은 수주잔량을 잃어가고 있습니다. 이 병목현상으로 인해 견조한 수주잔고가 있음에도 불구하고 단기적으로 CNC 시장 규모는 억제되고 있습니다.

CNC 선반은 2025년 기준 CNC 시장 점유율의 22.95%를 차지하며, 샤프트, 허브 등 원형 부품 가공에 필수적인 존재입니다. 전기자동차(EV) 파워트레인 개발의 발전에 따라 공차 요구사항이 엄격해짐에 따라 많은 공장에서 기존 선반 가공 센터에 라이브 툴링 및 Y축 기능을 추가하고 있습니다. 밀링머신은 CNC 공작기계 시장에서 두 번째로 큰 점유율을 차지하고 있으며, 항공우주 부품 및 의료용 임플란트용 복잡한 금형 캐비티 가공을 담당하고 있습니다. 배터리 인클로저의 판금 설계가 증가함에 따라 레이저 절단기 및 플라즈마 절단기에 대한 수요가 증가하고 있으며, 방전 가공기(EDM)는 경화 공구강 가공에서 여전히 중요한 역할을하고 있습니다. 5축 플랫폼 CNC 공작기계 시장 규모는 10.35%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 이는 단일 셋업 기능으로 지그 시간을 크게 단축하고 재설치 오류를 제거할 수 있기 때문입니다. 연삭기와 용접기는 틈새 분야의 깊이를 더합니다. 마찰 교반 용접은 충전물 없이 배터리 외피를 접합하고, 연삭 가공은 터빈 디스크에 경면 마무리를 제공합니다.

5축 이상 카테고리는 단순한 주축 출력이 아닌 유연성으로 가치가 이동하고 있는 이유를 보여줍니다. 통합형 공구 교환장치로 알루미늄, 티타늄, 복합재를 한 사이클에 수백 가지의 커터를 관리할 수 있습니다. Probe Routine을 통한 현장 형상 검증으로 고가의 재료비에도 불구하고 폐기물을 줄일 수 있습니다. 초기 도입 기업에 따르면, 작업자가 동시축 제어를 익힌 후 18%의 생산성 향상이 확인되었습니다. 따라서 부품 공급업체들은 다축 가공을 노동 위험에 대한 전략적 헤지 수단으로 인식하고, 공장 규모에 관계없이 CNC 시장을 고도의 복잡성 수준으로 끌어올리고 있습니다.

3축 유닛은 여전히 설치 기반의 45.35%를 차지하고 있으며, 단순 가공을 위한 우수한 가성비로 기반을 다지고 있습니다. 그러나 언더컷이나 헬리컬 그루브 가공을 수반하는 부품 프로그램은 회전 테이블을 추가하거나 풀 5축 기계를 도입해야 합니다. 5축 이상 부문은 CAGR 10.35%를 기록했는데, 이는 밀링과 선반 가공을 통합하여 재고정 없이 모든 방향에서 가공이 가능하기 때문입니다. CAM 소프트웨어의 개선과 교육 보조금 확대로 중견 시장에서의 기술 도입이 용이해져 고축수 CNC 시장 규모 확대가 촉진되고 있습니다.

4축 시스템에 장착된 회전 틸팅 테이블은 위치 결정 가공에 저렴하게 도입할 수 있으며, 기술적 격차를 해소합니다. 그러나 항공우주 분야의 주요 제조업체에서는 진정한 5축 가공기만이 구현할 수 있는 동시 동작 능력에 대한 수요가 증가하고 있습니다. Fanuc의 500i-A 컨트롤러는 CPU 성능이 2.7배 향상되어 복잡한 공구 경로의 축간 보간을 최적화합니다. OEM 업체들이 사이클 타임 단축과 표면 조도 향상을 입증함에 따라, 보수적인 가공업체들도 장비 도입 계획을 재검토하고 있습니다. 이러한 움직임은 전통적인 형식을 넘어 CNC 시장의 꾸준한 확장을 보장합니다.

아시아태평양은 중국의 방대한 공급업체 생태계와 일본의 선구적인 다축 기술을 바탕으로 CNC 공작기계 시장에서 51.40%의 매출 점유율을 차지하며 선두를 달리고 있습니다. 중국의 '이중 순환' 정책은 국내 조달을 촉진하고 국내 스핀들 제조업체와 피드백 인코더에 대한 수요를 불러일으켰습니다. 도쿄는 우주 로켓용 마그네슘 합금 가공에 대한 투자로 경량 소재 분야에서 선도적 지위를 확대. 한국에서는 정부 주도의 구동 시스템 개발이 진행되어 수입 서보에 대한 의존도를 줄이고 지역 전체의 자급자족 전략을 추진하고 있습니다. 아세안 국가들은 공급망 다변화의 혜택을 누리고 있으며, 초보적인 수준이지만 업그레이드 가능한 설비를 필요로 하는 신규 공장을 유치하고 있습니다.

북미에서는 인프라투자고용법, CHIPS법에 근거한 리쇼어링이 증가하면서 리쇼어링이 활발하게 진행되고 있습니다. 지멘스는 전기화 하드웨어의 미국 생산 라인 확장에 미화 100억 달러 이상을 투자하고 900명의 숙련된 인력을 추가 채용할 예정입니다. 파낙의 미시간주 미시간주 1억 1,000만 달러 규모의 캠퍼스는 연간 수천 명의 기술자를 양성하여 인력 부족을 해소하고 있습니다. 캐나다 퀘벡주 항공우주 클러스터에서는 고회전 티타늄 커터를 도입하고, 멕시코 자동차 거점에서는 전기차 조립 수요에 대응하기 위한 유연한 가공기술에 대한 투자가 진행되고 있습니다. 이러한 정책과 민간투자의 연계로 CNC(컴퓨터 수치제어) 시장은 수혜를 입고 있습니다.

유럽에서는 지속가능성에 대한 요구와 전동화 추진 속에서 꾸준한 성장세를 보이고 있습니다. 프랑스의 항공우주 보조금은 하이브리드형 적층-절삭 복합가공기 시험 도입을 가속화하여 현지 OEM의 경쟁력을 높이고 있습니다. 독일 중견기업은 구형 밀링 머신을 폐쇄 루프 구동 장치로 개조하여 EU 그린딜의 목표에 따라 에너지 사용량을 절감하고 있습니다. 파낙의 이베리아 사무소 확장은 스페인과 포르투갈의 로봇화 가공 셀에 대한 수요 증가를 보여줍니다. 동유럽 국가들은 서유럽 공장의 잉여 생산량을 인수하여 중급 3축 가공센터 수주를 주도하고 있습니다. 거시 경제의 역풍에도 불구하고 유럽은 미래의 CNC 시장 사양을 형성하는 기술 시험장으로서의 지위를 유지하고 있습니다.

The computer numerical controls market size in 2026 is estimated at USD 116.57 billion, growing from 2025 value of USD 108.63 billion with 2031 projections showing USD 165.95 billion, growing at 7.32% CAGR over 2026-2031.

Persistently tight labor markets, near-shoring of production, and the push for Industry 4.0 automation are converging, prompting manufacturers to accelerate investments in multi-axis and digitally connected equipment. Reshoring legislation in the United States and Europe is shifting capital away from low-cost regions toward flexible machining assets that support short lead times in production. Cybersecurity risk is rising in parallel with connectivity, motivating vendors to embed security-by-design features in new controllers. At the same time, sustained high steel and aluminum prices are driving demand for precision processes that minimize scrap. Together, these forces keep the computer numerical controls (CNC) market on a solid growth trajectory even as component shortages create near-term supply friction.

U.S. imports of finished goods from China fell 13% in 2023 while domestic factory investment rose sharply after infrastructure and semiconductor incentives. Incoming work is highly variable, so buyers prefer adaptable 5-axis machines and modular robot cells that handle diverse part families. Near-market production justifies higher capital outlays because freight risks fall and delivery speed improves. Vendors that offer rapid re-tooling and digital setup features gain a competitive edge. This reshoring vector directly enlarges the computer numerical controls market by converting decades of outsourced volumes into local capacity growth.

Digital twins let programmers validate tool paths virtually, cutting physical setup time by 20% with Siemens Sinumerik 828D hardware. Studies show 14.53% productivity gains and 13.9% lower energy use when machines run in closed-loop coordination with their virtual counterparts. Adoption is strongest in aerospace and automotive sectors that need real-time compensation for thermal drift and tool wear. Controller suppliers embed cloud connectivity and AI analytics, turning the computer numerical controls market into a software-centric arena. As license revenues grow, machine builders look to recurring income rather than one-time hardware margin.

Precision servo drives rely on specialty ASICs that remain in short supply, stretching lead times for premium machines to more than nine months. Some builders redesign around available chips, but that demands costly re-qualification. OEMs with secured allocations win share while latecomers lose backlog. The bottleneck suppresses the near-term computer numerical controls market volume despite solid order books.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

CNC lathes held 22.95% of the computer numerical controls market share in 2025 and remain indispensable for round parts such as shafts and hubs. Continuing EV power-train development raises tolerance demands, so many shops retrofit live tooling and Y-axis capability to conventional turning centers. Milling machines form the next largest slice of the CNC machine market, serving complex mold cavities for aerospace and medical implants. Laser and plasma cutters grow as sheet-metal designs multiply in battery enclosures, and EDM stays relevant for hardened tool steels. The CNC machine market size for 5-axis platforms is poised to grow 10.35% CAGR because single-setup capability slashes fixture time and eliminates reposting errors. Grinding and welding machines add niche depth: friction-stir welding joins battery shells without filler metal, while grinding delivers mirror finishes on turbine discs.

The 5-axis and above category illustrates why value is shifting toward flexibility rather than raw spindle horsepower. Integrated tool changers allow several hundred cutters that handle aluminum, titanium, and composites in one cycle. Probing routines verify geometry in situ, reducing scrap despite high material costs. Early adopters report 18% throughput gains once operators master simultaneous axis commands. Component suppliers therefore treat multi-axis as a strategic hedge against labor risk, pushing the computer numerical controls market toward higher complexity tiers regardless of plant size.

Three-axis units still anchor the installed base with a 45.35% share and attractive price-performance ratios for simple work. Yet part programs with undercuts and helical flutes drive shops to add rotary tables or invest in full five-axis machines. The 5-axis and above segment posts a 10.35% CAGR because it merges milling and turning, enabling machining from all directions without reclamping. Improved CAM software plus training subsidies make the technology accessible to mid-market buyers, widening the computer numerical controls market size for advanced axis counts.

Rotary-tilt tables on 4-axis systems bridge the gap and allow affordable entry into positional machining. However, aerospace primes increasingly require simultaneous motion capability that only true 5-axis delivers. FANUC's 500i-A controller, with 2.7 times CPU power, optimizes axis interpolation for complex tool paths. As OEMs validate shorter cycle times and better surface finishes, even conservative job shops reconsider equipment roadmaps. This dynamic ensures a steady migration that enlarges the computer numerical controls market beyond conventional formats.

The Computer Numerical Controls Market Report is Segmented by Machine Type (CNC Lathe Machines, CNC Milling Machines, and More), Axis Type (3-Axis, and More), Component (CNC Controller, Servo Motor Drive, and More), Control System (Open-Loop, Closed-Loop), Deployment (Stand-Alone CNC Machines, and More), End User (Automotive, Aerospace and Defense, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific leads the CNC machine market with a 51.40% revenue share, anchored by China's vast supplier ecosystem and Japan's trail-blazing multi-axis technology. Beijing's dual-circulation policy encourages local content, spurring demand for domestic spindle makers and feedback encoders. Tokyo's investment in magnesium alloy machining for space launch widens its leadership in lightweight materials. South Korea's state-funded drive system advances cut reliance on imported servos, underlining a regional strategy toward self-sufficiency. ASEAN countries benefit from supply-chain diversification, attracting greenfield plants that require entry-level yet upgradeable equipment.

North America gains momentum as reshoring projects proliferate under the Infrastructure Investment and Jobs Act and the CHIPS Act. Siemens earmarked over USD 10 billion to expand U.S. production lines for electrification hardware, adding 900 skilled roles. FANUC's USD 110 million campus in Michigan trains thousands of technicians annually, alleviating talent shortages. Canadian aerospace clusters in Quebec adopt high rpm titanium cutters, while Mexican automotive hubs invest in flexible machining to service near-term EV assembly demand. The computer numerical controls market thus benefits from synchronized policy and private investment.

Europe shows steady growth amid sustainability mandates and push for electric mobility. French aerospace subsidies accelerate hybrid additive-subtractive machine trials, boosting local OEM competitiveness. Germany's Mittelstand firms retrofit legacy mills with closed-loop drives to cut energy use, aligning with EU Green Deal goals. FANUC's Iberia office expansion signals rising demand in Spain and Portugal for robotized machining cells. Eastern European countries capture overflow work from Western plants, driving orders for mid-range 3-axis centers. Despite macro headwinds, Europe remains a technology testbed that shapes future computer numerical controls market specifications.