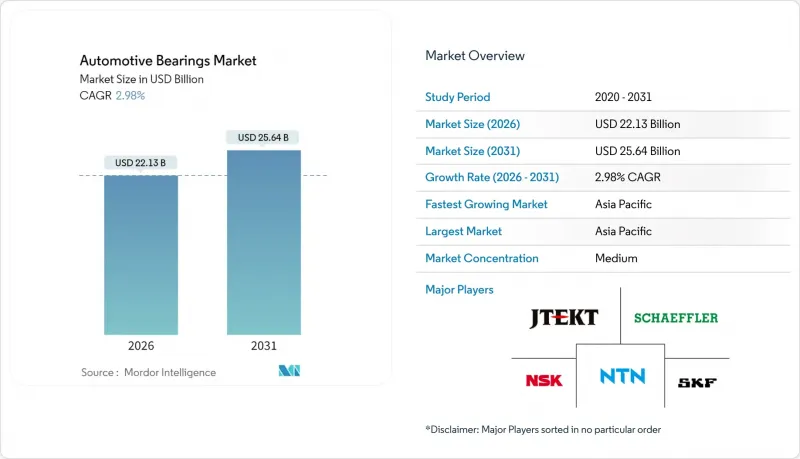

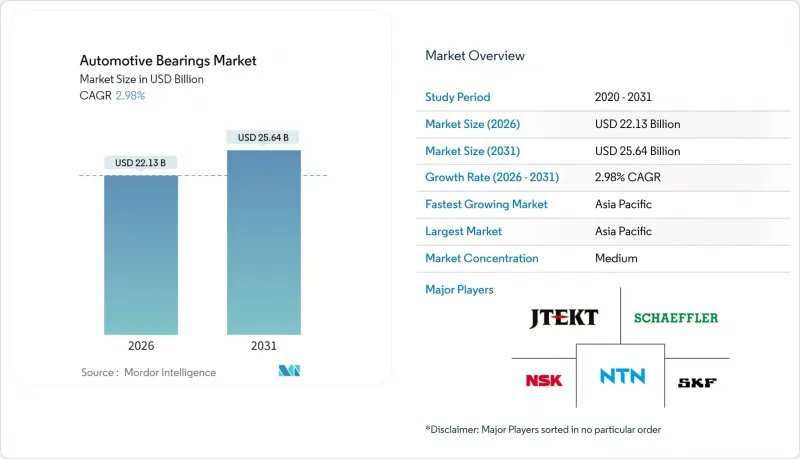

자동차 베어링 시장은 2025년 214억 9,000만 달러에서 2026년에는 221억 3,000만 달러로 성장하고, 2026-2031년 CAGR 2.98%로 성장을 지속하여, 2031년까지 256억 4,000만 달러에 이를 것으로 예측되고 있습니다.

이러한 확대는 내연기관 생산량이 안정화되는 동시에 전동화가 가속화되는 상황의 교차점에 위치하여 베어링 사양을 재구성하고 차량당 평균 베어링 수를 감소시키는 동시에 저마찰 및 고효율 솔루션에 대한 수요를 촉진하고 있습니다. 구름 베어링 설계는 휠 엔드, 변속기, 전동 파워트레인의 핵심 부품에서 여전히 주류입니다. 그러나 OEM 업체들이 에너지 절약과 컴팩트한 모듈형 레이아웃을 추구하면서 세라믹 하이브리드, 센서 통합 유닛, 적층 케이지가 프리미엄 점유율을 차지하고 있습니다. 아시아태평양은 경차 생산량 증가와 현지 전기차 보급으로 세계 성장을 견인하고 있습니다. 한편, 북미와 유럽에서는 지능형 베어링을 통한 애프터마켓용 업그레이드와 예지보전에 집중하고 있습니다. 철강재 가격 변동, 관세 부과, 위조품 유입으로 인해 수익률이 지속적으로 압박을 받고 있으며, 주요 공급업체들은 수직계열화, 첨단 소재, 순환형 성능 비즈니스 모델로 전환해야 하는 상황입니다.

전기자동차는 초저마찰과 높은 전기 절연성을 갖춘 베어링을 요구하고 있으며, 공급업체들은 에너지 손실 억제와 방전 방지를 위해 세라믹 볼, 특수 코팅, 새로운 디자인의 케이지 형태로의 전환을 추진하고 있습니다. SKF의 초저마찰 휠 베어링 시리즈는 토크 저항을 줄이고 EV 허브를 대상으로 하며, 쉐플러의 원심 디스크 볼 베어링은 마찰을 80% 감소시키고 수명을 10배 연장합니다. 전기 파워트레인 유닛에 요구되는 성능의 비약적인 발전을 구현하고 있습니다. 각 제조업체는 또한, 고속 모터 샤프트에 있어서 하이브리드 질화규소 솔루션이 전략적으로 필요한 고속 모터 샤프트에 있어서도 미행전류의 위협에 직면하고 있습니다. EV 전용 라인에 대한 투자가 유입되고, 차량당 수량 감소를 프리미엄 가격 책정으로 상쇄함으로써 부품 수 감소에도 불구하고 자동차 베어링 시장은 전동화로 인한 수익화를 지속하고 있습니다.

미국 내 차량 노후화에 따라 특히 허브 베어링과 드라이브 트레인 베어링의 부품 교체 주기가 길어지고 있습니다. 표면 처리 기술의 발전은 이러한 부품의 수명을 연장하고, 소유자는 안전성을 유지하면서 서비스 빈도를 줄일 수 있습니다. 차량 운영자들은 데이터 분석을 통해 기계적인 문제를 예측하는 경향이 증가하고 있으며, 애프터마켓은 사후 대응형 수리에서 상태 모니터링에 기반한 예방적 구매로 전환하고 있습니다. 유통 경로의 효율화와 소비자 직접 판매 모델을 통해 고성능 베어링 제품은 초기 설치 후에도 그 가치를 유지할 수 있습니다. 이러한 진화하는 구조는 신차 판매의 변동성에도 불구하고 자동차 베어링 분야의 전체 수요를 안정화시키는 데 일조하고 있습니다.

JTEKT의 시험에서 위조 허브 유닛은 정품의 10분의 1의 수명으로 피로 시험에 불합격하는 것으로 나타났습니다. SKF는 압수한 모조품 15톤을 폐기했지만, 홀로그램 라벨의 개선과 블록체인을 통한 추적성 도입에도 불구하고 위조품의 유입을 완전히 막지 못하고 있습니다. 신흥 시장에서는 법적 처벌이 약하기 때문에 재범이 만연하고, 정식 공급업체는 교육 캠페인과 포렌식 감사 비용을 부담해야 합니다. 이러한 평판 위험과 보증 비용은 자동차 베어링 시장의 OEM 및 애프터마켓 부문에 큰 영향을 미치고 있습니다.

롤링 베어링 제품은 2025년 매출의 53.10%를 차지할 것으로 예상되며, 2031년까지 연평균 5.08% 성장할 것으로 예측됩니다. 그 우위는 휠 허브, 변속기, e-axle에 적합한 비용, 부하, 속도 성능의 균형에 기인합니다. 원통형 롤러와 테이퍼 롤러는 고부하 구동계에, 깊은 홈 볼 베어링은 저마찰과 정숙성이 최우선인 고속 EV 모터에 각각 우수합니다. EV의 장기 보증은 영구 밀폐형 유닛에 유리하며, 통합 윤활 및 센서 패키지에 대한 수요를 촉진하고 있습니다.

평활 베어링의 틈새 시장은 진동 운동이 지배적인 소형 패키지 연소 엔진과 HVAC 주변기기에서 살아남고 있지만, 그 점유율은 계속 감소하고 있습니다. 한편, 크로스 롤러와 니들 베어링의 혁신은 소형 스티어링 칼럼과 전동식 주차 브레이크를 겨냥하여 가치 밀도를 단계적으로 높이고 있습니다. 허브 모듈 설계가 ABS 인코더가 장착된 3세대 더블 롤러 형태로 전환됨에 따라 프리미엄 부문의 구름 베어링에 대한 수요가 증가하여 자동차 베어링 시장에서의 중심성을 강화할 것입니다.

2025년 전 세계 출하량의 76.10%를 차지할 것으로 예상되며, 이는 성숙한 용해 공정, 입증된 피로 수명, 비용 우위를 반영합니다. 그러나 OEM 제조업체가 전기화 플랫폼을 추구함에 따라 누설 전류 절연이 중요하기 때문에 이 부문의 성장은 완만할 것입니다. 세라믹 및 하이브리드 유닛은 CAGR 6.02%로 발전하고 있습니다.

폴리머 및 코팅된 강철 베어링은 부식성 환경과 소음에 민감한 틈새 시장을 채우고 있습니다. 한편, 표면처리 기술의 혁신(다이아몬드 라이크 카본, 플라즈마 질화처리 등)을 통해 재료를 교체하지 않고도 서비스 주기를 연장할 수 있습니다. 가마 가동률 향상에 따라 세라믹의 원가 하락 가능성이 있으며, 가격 프리미엄이 축소되면서 중급 EV 모델로의 채택이 촉진될 것으로 예측됩니다. 그러나 저렴한 가격의 양산형 내연기관차(ICE) 및 하이브리드 자동차 수요에 힘입어 2031년까지 자동차 베어링 시장에서 철강재의 점유율은 3분의 2에 육박할 것으로 예측됩니다.

아시아태평양은 2025년 매출의 43.40%를 차지할 것으로 예상되며, 중국의 규모, 인도의 두 자릿수 조립 증가, 아세안의 급성장하는 공급업체 네트워크에 힘입어 연평균 6.55%의 성장률을 나타낼 것으로 전망됩니다. 중국 OEM 제조업체는 EV 보증 요구 사항을 충족시키기 위해 현지 생산 하이브리드 세라믹 허브를 통합하고 있습니다. 한편, 인도의 '메이크 인 인디아' 정책에 따라 2020년 중반까지 수입 의존도는 40%에서 25%로 낮아질 것으로 예측됩니다. 배터리 전기 이륜차에 대한 정부 보조금은 소형 깊은 홈 볼 베어링 제품에 대한 수요를 확대하여 이 지역이 자동차 베어링 시장에서 차지하는 기여도를 강화하고 있습니다.

북미는 픽업트럭과 SUV의 높은 생산량과 성숙한 교체 주기로 인해 여전히 큰 점유율을 유지하고 있습니다. 바이든 행정부의 관세 환경은 연간 80억 달러의 부품 비용 증가를 가져왔고, 쉐플러와 같은 공급업체가 오하이오 주에 2억 3,000만 달러 규모의 e-axle 공장을 설립하는 데 일조했습니다. 이를 통해 공급망을 단축하고 OEM의 승인을 확보할 수 있습니다. 멕시코의 비용 효율성이 뛰어난 가공 클러스터는 링 단조 투자를 유치하여 미국의 부족한 부분을 보완. 캐나다는 철강 원료 공급력을 활용하고 있습니다. 평균 차량 사용 연한이 12.8년을 넘어서면서 이 지역의 애프터마켓은 견조한 성장세를 유지하고 있습니다. 신차 판매의 변동에도 불구하고, 자동차 베어링 시장 내 수익이 유지되고 있습니다.

유럽은 경차 생산 둔화에 직면한 반면, 전기차 의무화가 가속화되면서 센서 통합형 하이브리드 세라믹 솔루션에 대한 수요가 증가하고 있습니다. 독일이 연구개발비를 주도하고 스웨덴에 본사를 둔 SKF는 EU 그린딜 목표에 부합하는 순환형 성능 재피복 프로그램을 시범 도입했습니다. 쉐플러는 오스트리아 베른도르프 공장을 폐쇄하고 슬로바키아 키체 공장을 업그레이드하는 사업 구조조정을 통해 지속적인 비용 재검토를 추진하고 있습니다. 영국, 프랑스, 이탈리아에서는 지역 밀착형 e-axle 생산을 추진하고 있으며, 이를 통해 지역 조달을 중시하는 베어링 공급 체제를 구축하여, 자동차 베어링 시장에서의 점유율이 소폭 축소되는 상황에서도 유럽 대륙이 전략적 영향력을 유지할 수 있도록 보장하고 있습니다.

The automotive bearings market is expected to grow from USD 21.49 billion in 2025 to USD 22.13 billion in 2026 and is forecast to reach USD 25.64 billion by 2031 at 2.98% CAGR over 2026-2031.

The expansion sits at the intersection of stabilizing internal-combustion volumes and accelerating electrification, reshaping bearing specifications and reducing the average bearing count per vehicle while driving demand for low-friction, high-efficiency solutions. Rolling-element designs continue to dominate core wheel-end, transmission, and e-powertrain positions. Yet, ceramic hybrids, sensor-integrated units, and additive-manufactured cages carve a premium share as OEMs chase energy savings and compact modular layouts. Asia-Pacific anchors global growth on rising light-vehicle builds and local EV adoption. At the same time, North America and Europe focus on aftermarket upgrades and predictive maintenance enabled by intelligent bearings. Margins remain under pressure from steel volatility, tariff levies, and counterfeit inflows, pushing leading suppliers toward vertical integration, advanced materials, and circular-performance business models.

Electric vehicles require bearings with ultra-low friction and high electrical insulation, pushing suppliers toward ceramic balls, specialized coatings and new cage geometries that curb energy loss and avert electrical discharge. SKF's ultra-low-friction wheel bearing series targets EV hubs by cutting torque drag, while Schaeffler's centrifugal-disc ball bearing lowers friction by 80% and multiplies service life tenfold, highlighting the performance leap now expected in e-powertrain units. Manufacturers also confront stray-current threats that cause pitting, which makes hybrid silicon-nitride solutions a strategic necessity in high-speed motor shafts . Investment flows into dedicated EV lines, with premium pricing offsetting reduced per-vehicle volume, ensuring the automotive bearings market continues to monetize electrification despite lower component counts

The aging vehicle fleet in the United States prompts longer intervals between component replacements, particularly for hub and drivetrain bearings. Advances in surface treatment technologies are helping extend the lifespan of these parts, allowing owners to maintain safety while reducing service frequency. Fleet operators increasingly use data analytics to anticipate mechanical issues, shifting the aftermarket landscape from reactive repairs to proactive, condition-based purchasing. Streamlined distribution channels and direct-to-consumer models enable high-performance bearing products to retain value beyond their initial installation. This evolving structure is helping stabilize demand across the automotive bearings sector, even as new vehicle sales fluctuate

JTEKT testing shows counterfeit hub units failing fatigue tests in one-tenth the life of genuine parts . SKF destroyed 15 tons of seized knock-offs, yet improved holographic labels and blockchain traceability only partially stem the tide. In emerging markets, weak legal penalties allow repeat offenders, forcing legitimate suppliers to finance education campaigns and forensic audits. The reputational and warranty costs weigh on the automotive bearings market's OEM and aftermarket segments.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Rolling-element products generated 53.10% of 2025 revenue, and are forecast to grow at 5.08% CAGR through 2031. Their dominance stems from balanced cost, load, and speed capabilities that suit wheel hubs, transmissions, and e-axles. Cylindrical and tapered rollers serve heavy-duty drivelines, while deep-groove ball bearings excel in high-speed EV motors where low friction and acoustic comfort are paramount. Longer EV warranty terms favor sealed-for-life units, stimulating demand for integrated lubrication and sensor packages.

The plain-bearing niche persists in tight-package combustion engines and HVAC ancillaries where oscillatory motion prevails, yet its share continues to erode. Meanwhile, cross-roller and needle innovations target compact steering columns and electric park brakes, incrementally lifting value density. As hub module designs migrate to third-generation double-row formats with ABS encoders, rolling-element volumes will rise within premium segments, reinforcing their centrality to the automotive bearings market.

Steel accounted for 76.10% of global shipments in 2025, reflecting mature melting routes, proven fatigue life, and favorable cost. The segment expands more slowly as OEMs pursue electrified platforms where stray-current insulation becomes critical. Ceramic and hybrid units advance at 6.02% CAGR.

Polymer and coated-steel variants fill corrosive or noise-sensitive niches, while surface-engineering breakthroughs-diamond-like carbon, plasma nitriding-prolong service intervals without material substitution. Ceramic costs could drop as kiln utilization rises, trimming the price premium and enticing mid-range EV models. Nonetheless, the automotive bearings market share of steel is expected to remain near two-thirds by 2031, sustained by affordable mass-market ICE and hybrid volumes

The Automotive Bearings Market Report is Segmented by Bearing Type (Plain Bearings and Rolling Element Bearings), Material (Steel, Ceramic and Hybrid, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Application/Position (Wheel End, Engine and Turbocharger, and More), Sales Channel (OEM and Aftermarket), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific owned 43.40% of 2025 revenue and is forecast to grow at a 6.55% CAGR, buoyed by China's scale, India's double-digit assembly additions, and ASEAN's fast-rising supplier networks. Chinese OEMs integrate locally produced hybrid-ceramic hubs to meet EV warranty demands, while India's Make-in-India drive cuts import dependence from 40% toward 25% by mid-decade. Government subsidies for battery electric two-wheelers broaden demand for compact deep-groove products, reinforcing the region's contribution to the automotive bearings market.

North America sustains a sizeable share anchored by high pickup and SUV output plus a mature replacement cycle. The Biden-era tariff landscape adds USD 8 billion in annual components costs, nudging suppliers like Schaeffler to open the USD 230 million Ohio e-axle plant that shortens supply chains and secures OEM approvals. Mexico's cost-effective machining clusters attract ring-forging investments that backfill U.S. shortages, while Canada leverages raw-steel availability. The region's aftermarket remains resilient as average vehicle age climbs past 12.8 years, propping revenue inside the automotive bearings market despite volatile new-car sales.

Europe wrestles with slower light-vehicle production yet accelerates EV mandates that lift demand for sensor-integrated and hybrid-ceramic solutions. Germany leads R&D spending; Sweden-based SKF pilots circular-performance reclad programs that align with EU Green Deal objectives. Schaeffler's consolidation-closing Austria's Berndorf plant while upgrading Slovakia's Kysuce site-highlights ongoing cost realignment. The U.K., France and Italy pursue localized e-axle builds that favor regional bearing sourcing, ensuring the continent holds strategic sway even as its share modestly contracts within the automotive bearings market.