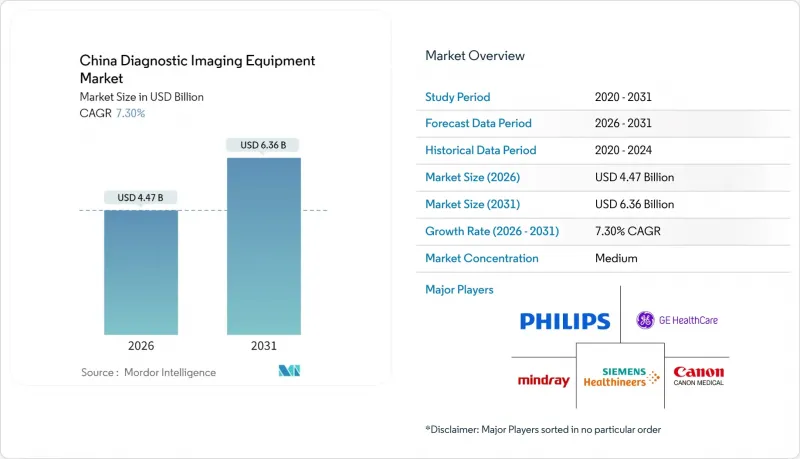

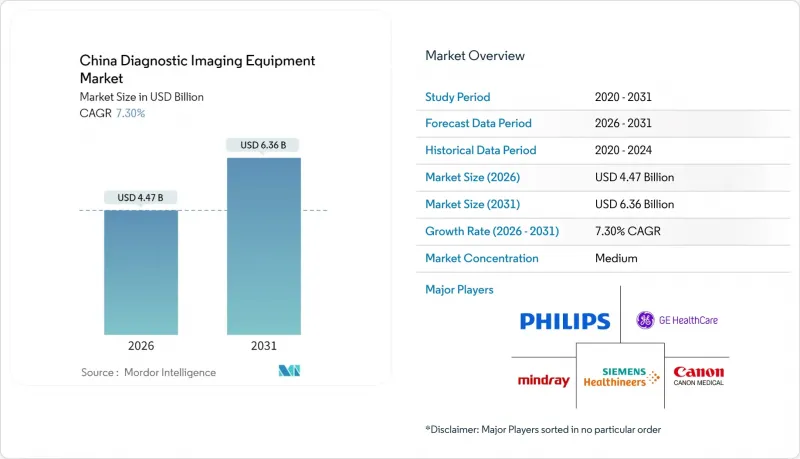

2026년 중국의 진단용 영상 장비 시장 규모는 44억 7,000만 달러로 추정되며며, 2025년 41억 7,000만 달러에서 성장을 이루어 2031년에는 63억 6,000만 달러에 이를 것으로 예측됩니다. 2026-2031년에는 CAGR 7.3%로 성장할 전망입니다.

국내 제조에 대한 정부의 강력한 지원, 인공지능(AI)의 급속한 통합, 정책 주도의 가격 인하가 경쟁 환경을 재정의하고, 도시와 농촌 모두에서 첨단 기술에 대한 접근성을 확대하고 있습니다. 유나이티드이미징, 뉴소프트메디컬과 같은 국내 혁신 기업들은 비용 경쟁력 있는 하드웨어와 AI 기반 워크플로우 툴을 결합하여 다국적 벤더의 역사적 우위를 점차 잠식하고 있습니다. 수량 기준 조달(VBP)은 가격 압축과 수요 증가를 동시에 촉진하고 있으며, 특히 2024년까지 보급률이 낮았던 지방에서 두드러지게 나타나고 있습니다. AI 도입은 워크플로우 효율을 가속화하고 있으며, 3차 의료기관에서는 인간과 AI의 협업으로 평균 판독 시간이 27.2% 단축되고, 진단 민감도가 12% 향상되었습니다. 이러한 요인들이 결합되어 종양학, 심장병학, 만성질환 모니터링 분야의 지속적인 수요를 뒷받침하고 있습니다.

2050년까지 비감염성 질환이 중국 전체 사망의 93%를 차지할 것으로 예측되는 가운데, 의료 계획 담당자들은 조기 발견과 장기적인 모니터링을 위한 영상 진단 역량을 강화해야 합니다. 고령층에서는 이미 만성질환 유병률이 66.3%에 달하고, CT와 MRI를 통한 경과관찰 검사에 대한 수요가 증가하고 있습니다. 검진 정책은 확대되고 있으며, 저선량 CT(LDCT) 프로그램은 사천성에서 1시간 이내에 이동 가능한 고위험군 주민의 96.95%를 커버하고 있지만, 농촌 지역의 검진율은 여전히 34.72%로 낮은 수준입니다. 당뇨병 간이검사는 현립병원에서 QALY당 185달러의 비용효과성을 보여주며, 휴대용 초음파 장비와 HbA1c 키트 세트 조달을 촉진하고 있습니다. 이러한 추세에 따라 투자는 순수하게 치료 목적의 인프라에서 확장 가능한 진단 기기군으로 옮겨가고 있습니다.

2050년까지 평균 수명이 82.1세, 75-84세 연령대의 복합질환 보유율이 33.7%로 정점에 도달할 것으로 예상에 따라 암, 심혈관질환, 신경퇴행성 질환의 모니터링에 대한 영상진단 수요가 증가할 것으로 예측됩니다. 2018년 이후 노인 돌봄 수요와 자원 공급의 조정이 개선되었지만, 특히 내륙 지방에서는 여전히 노인 인구 증가율을 따라잡지 못하고 있습니다. '건강 중국 2030' 계획은 예방적 영상진단을 노화 질병 관리의 기초로 삼고, 지역 병원의 심초음파 검사와 듀얼 에너지 CT에 대한 보조금 지원을 추진하고 있습니다. 원격지 이동형 CT 버스 파견이 증가하여 이동에 따른 의료 지연이 줄어들고 있습니다. 의사 밀도는 2024년 인구 1만 명당 30.4명으로 증가했고, 영상의학과 의사의 부족은 계속되고 있어 AI를 통한 선별진료 도구의 필요성이 부각되고 있습니다.

가치 기반 지불(VBP)에 의한 할인 후에도 고급 MRI는 200만 달러가 넘을 수 있어 3차 의료기관의 예산을 압박하고 있습니다. 고급 CT 부품에 대한 관세가 대당 20만 달러에 달하고, 일부 중국 기업들은 공급망을 아세안 시장으로 이전하려는 움직임을 보이고 있습니다. 2024년 주요 병원들이 발주를 연기함에 따라 지멘스 헬스인어스와 GE헬스케어는 한 자릿수 중반의 매출 감소를 보고해 조달 사이클의 변동성을 부각시켰습니다. 성(省) 단위의 효율성 조사에서 자본 배분 격차가 지속되고 있으며, 서부 지역의 평균 효율성 점수는 0.979인 반면, 연안 지역의 평균 효율성 점수는 거의 1에 가까운 것으로 나타났습니다.

2025년 기준 엑스레이 장비는 중국 진단영상기기 시장에서 27.21%로 가장 큰 점유율을 차지하고 있으며, 이는 저렴한 가격과 1차의료기관에서의 높은 보급률을 반영하고 있습니다. 컴퓨터 단층촬영(CT)은 반복재구성법과 광자 계수 기술의 업그레이드를 배경으로 부문 중 가장 높은 CAGR 8.75%를 나타낼 것으로 예측되며, 지방병원의 종양학 및 순환기 분야 수요를 흡수할 것으로 보입니다. 정부의 보조금 제도에 의한 구형 아날로그 장비의 단계적 폐지에 따라 디지털 엑스레이 촬영으로의 전환은 계속되고 있습니다. 한편, PCCT(고정밀 CT) 파일럿 사이트에서는 방사선 피폭량 40% 감소와 뼈 미세구조의 가시성이 크게 개선된 것으로 보고되고 있어, CT는 고주파 정형외과 검사에서 유력한 대안으로 자리매김하고 있습니다.

휴대용 초음파 장비와 핸드헬드 엑스레이 장비는 고정형 양상을 보완하는 아웃리치 프로그램에서 두 가지 도입 모델을 강조하고 있습니다. 핵의학은 틈새 시장이지만 전략적 역할을 유지하고 있으며, 1,200개 병원이 게이트 제어 SPECT 또는 PET 검사를 실시하여 연간 390만 명의 환자를 대상으로 하고 있습니다. 국내 방사성 동위원소 공급은 점차 개선되는 추세입니다. MRI 업체는 지방 설치를 용이하게 하는 헬륨 프리 시스템을 추구하고, AI 탑재 투시 장비는 중재 시술 중 선량률 자동 조절을 실현합니다. 이러한 진화가 결합되어 중국 진단영상기기 시장에서 다양한 임상환경에 대응할 수 있는 폭넓은 모달리티 구성을 구축하고 있습니다.

고정형 장비 매출은 여전히 81.12%를 차지하고 있으며, 이는 고가의 고선량 CT와 3T MRI가 수요를 견인하는 3차 의료기관의 고착화된 조달 구조를 반영하고 있습니다. 그러나 모바일 및 휴대형 시스템은 지방 의료 정책과 가치 기반 지불(VBP)의 비용 효율성으로 인해 CAGR 8.79%로 확대될 것으로 예측됩니다. 저선량 엑스레이, 심전도, 초음파를 통합한 의료용 올인원 키오스크는 하이난성 시범사업에서 효과를 입증하여 환자 수가 두 자릿수 증가를 보이고 있습니다.

국내 혁신기업들은 현재 응급의료 및 구급차에서 사용할 수 있는 배터리 구동식 휴대용 CT를 제공하며 진료 현장의 경계를 넓혀가고 있습니다. 5G 및 엣지 컴퓨팅 플랫폼을 기반으로 한 원격 방사선 진단 시스템을 통해 마을 진료소에서 촬영한 영상이 60초 이내에 도시 지역의 영상의학과 전문의에게 전달되어 인력 부족을 보완하고 있습니다. 그 결과, 모바일 시스템은 고급형 고정형 장비 시장을 침식하지 않고 점진적인 수요를 확보할 수 있는 태세를 갖추고 있으며, 중국 진단 영상 장비 시장 규모를 확대하는 데 기여하고 있습니다.

China Diagnostic Imaging Equipment Market size in 2026 is estimated at USD 4.47 billion, growing from 2025 value of USD 4.17 billion with 2031 projections showing USD 6.36 billion, growing at 7.3% CAGR over 2026-2031.

Robust government support for domestic manufacturing, rapid artificial-intelligence (AI) integration, and policy-driven price reductions are redefining competitive dynamics and expanding access to advanced modalities across urban and rural settings. Domestic innovators such as United Imaging and Neusoft Medical continue to erode the historic dominance of multinational vendors by pairing cost-competitive hardware with AI-enabled workflow tools. Volume-based procurement (VBP) is simultaneously compressing prices and stimulating unit demand, especially in lower-tier counties where penetration remained low until 2024. AI adoption is accelerating workflow efficiency; human-AI collaboration has cut average image-reading time by 27.2% while lifting diagnostic sensitivity by 12% in tertiary hospitals. Together, these forces underpin sustained demand across oncology, cardiology and chronic-disease monitoring segments.

Non-communicable diseases are expected to cause 93% of all deaths in China by 2050, pushing health planners to expand imaging capacity for early detection and longitudinal monitoring. Older adults already show 66.3% chronic-disease prevalence, reinforcing demand for CT and MRI follow-up exams. Screening policies are broadening; low-dose CT (LDCT) programs now cover 96.95% of high-risk residents within one-hour travel in Sichuan, yet rural adherence still lags at 34.72%. Diabetes point-of-care testing demonstrates cost-effectiveness at USD 185 per QALY in county hospitals, encouraging bundled procurement of portable ultrasound and HbA1c kits. These patterns shift investment away from purely therapeutic infrastructure toward scalable diagnostic fleets.

Life expectancy is forecast to hit 82.1 years by 2050, with multimorbidity peaking at 33.7% in the 75-84 cohort, amplifying imaging requirements for cancer, cardiovascular and neurodegenerative surveillance. Coordination between elder-care demand and resource supply improved after 2018 but still trails the growth rate of the senior population, especially in interior provinces. The Healthy China 2030 plan identifies preventive imaging as a cornerstone for managing age-related disease, prompting subsidies for echocardiography and dual-energy CT in community hospitals. Mobile CT buses are increasingly dispatched to remote villages, reducing travel-related care delays. Physician density rose to 30.4 per 10,000 residents in 2024, yet radiologist shortfalls endure, underscoring the need for AI triage tools.

Even after VBP discounts, high-end MRI can exceed USD 2 million, straining budgets for tier-3 facilities. Tariffs on premium CT components add up to USD 200,000 per unit, prompting some Chinese firms to relocate supply chains to ASEAN markets. Order deferrals by major hospitals in 2024 led Siemens Healthineers and GE HealthCare to report mid-single-digit revenue declines, underscoring procurement cyclicality. Provincial efficiency studies reveal persistent capital-allocation disparities, with western regions averaging a 0.979 efficiency score versus near-unity in coastal areas.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

X-ray maintained the largest share of the China diagnostic imaging equipment market at 27.21% in 2025, reflecting its affordability and entrenched presence in primary-care clinics. Computed tomography, fueled by iterative reconstruction and photon-counting upgrades, is forecast to post the segment-leading 8.75% CAGR, capturing oncology and cardiovascular demand in county hospitals. Digital radiography migration continues as older analog units phase out under government subsidy schemes. Meanwhile, PCCT pilot sites report 40% radiation-dose savings and sharply improved bone-microstructure visualization, positioning CT as a credible challenger for high-volume orthopedic exams.

Portable ultrasound and handheld X-ray units complement fixed modalities in outreach programs, underscoring a dual-track deployment model. Nuclear medicine retains a niche but strategic role; 1,200 hospitals run gated SPECT or PET studies for 3.9 million patients annually, with domestic radio-isotope supply gradually improving. MRI vendors pursue helium-free systems to ease rural installs, while AI-enabled fluoroscopy automates dose-rate modulation during interventional procedures. Together, these upgrades solidify a broad modality mix to serve heterogeneous clinical settings across the China diagnostic imaging equipment market.

Fixed rooms still account for 81.12% revenue, reflecting entrenched procurement in tertiary hospitals where high-slice CT and 3 T MRI command premium prices. Yet mobile and handheld systems are forecast to expand at an 8.79% CAGR, propelled by rural-health mandates and VBP affordability. Health All-in-One kiosks integrating low-dose X-ray, ECG, and ultrasound have proven effective in Hainan pilot sites, driving double-digit patient-volume gains.

Domestic innovators now offer battery-powered handheld CT for emergency medicine and ambulance use, widening point-of-care boundaries. Tele-radiology frameworks built on 5G and edge-computing platforms ensure that images captured in township clinics reach city radiologists in under 60 seconds, offsetting workforce shortages. As a result, mobile systems are poised to capture incremental volumes without cannibalizing high-end fixed installations, adding breadth to the China diagnostic imaging equipment market size.

The China Diagnostic Imaging Equipment Market Report is Segmented by Modality (MRI, CT, Ultrasound, X-Ray, Nuclear Imaging, Fluoroscopy, Mammography), Portability (Fixed Systems, Mobile and Hand-Held Systems), Application (Cardiology, Oncology, Neurology, Orthopedics, Gastroenterology, and More), End User (Hospitals, Diagnostic Imaging Centres, and More). The Market Forecasts are Provided in Terms of Value (USD).