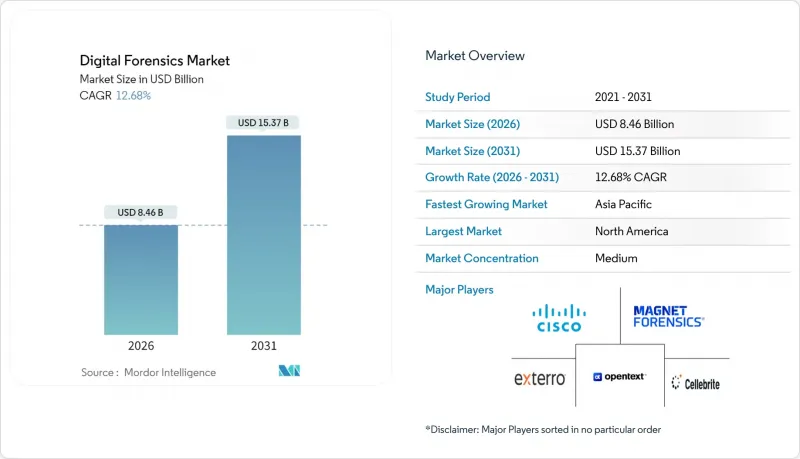

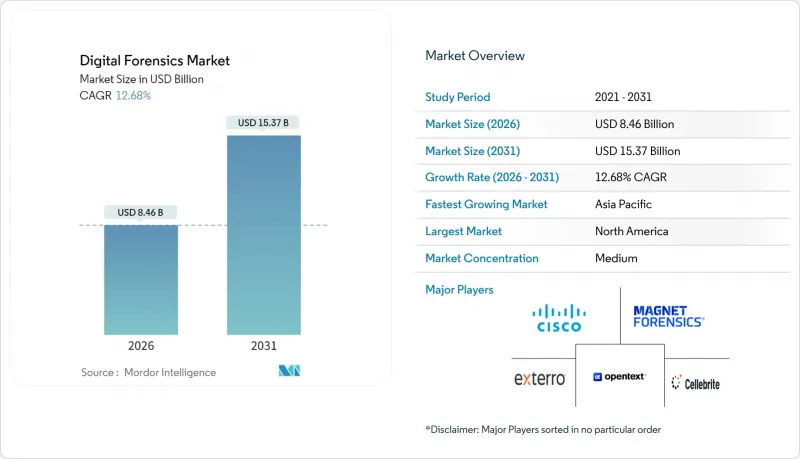

디지털 포렌식 시장 규모는 2025년 75억 1,000만 달러에서 2026년 84억 6,000만 달러로 성장할 전망입니다.

2031년까지 15억 3,700만 달러에 달할 것으로 예상되며, 2026년부터 2031년까지 연평균 12.68%의 성장률을 나타낼 것으로 전망됩니다.

클라우드 네이티브 SaaS형 조사, 딥페이크 대응, 확장된 감지 및 대응 플랫폼에 대한 디지털 포렌식 통합이 성장의 핵심입니다. 법적으로 의무화된 모바일 단말기의 증거 추출과 공공 부문의 꾸준한 투자가 수요를 더욱 뒷받침할 것입니다. 반면, 기본 암호화와 수사관 부족은 운영상의 마찰을 야기하며, 자동화된 클라우드 기반 증거보존 기술 혁신을 촉진하고 있습니다. 경쟁 환경은 기존 벤더들이 차별화를 위해 인공지능과 블록체인을 활용한 증거관리 기능을 도입하고 있어, 여전히 중간 정도의 분산 상태가 지속되고 있습니다.

클라우드 마이그레이션은 기존의 디스크 이미징을 대체하고 있으며, 분산된 멀티테넌트 환경에서 휘발성 데이터를 수집하면서 ISO/IEC 27035-4:2024의 증거 채택 기준을 충족하는 포렌식 플랫폼의 도입을 촉진하고 있습니다. 증거 격리 요구 사항과 자동화된 증거 관리 이력 추적으로 인해 하이퍼스케일러의 보안 서비스 및 사전 통합 솔루션에 대한 수요가 증가하고 있습니다. 그 결과, 클라우드 네이티브 획득 API를 제공하는 벤더들은 특히 복잡한 관할권 경계를 넘나드는 다국적 기업을 중심으로 기업들 사이에서 채택이 가속화되고 있습니다.

기계가 생성한 음성 및 동영상 사기가 실시간 대화까지 침투함에 따라, 연구소에서는 기존의 인증 기술을 저해상도 컨텐츠에서 91.82%의 정확도를 달성하는 신경망 감지 알고리즘으로 대체해야 할 필요성이 대두되고 있습니다. BFSI 기관은 고가 거래를 보호하기 위해 블록체인 출처 추적 체계를 통합하고, 법 집행 기관은 수사 인터뷰 중 증거 보존을 위해 실시간 스크리닝 도구에 투자하고 있습니다.

하드웨어 기반 암호화로 인해 최신 디바이스의 추출 성공률은 40% 미만으로 떨어지고, 고가의 복호화 유틸리티나 클라우드 기반 증거 대안에 의존할 수 밖에 없는 상황입니다. 소규모 기관은 예산상의 장벽에 직면하고, 수사 격차가 확대되는 가운데 합법적 접근 협력에 대한 정책적 논의가 촉진되고 있습니다.

2025년, 소프트웨어는 암호화 및 클라우드 증거를 위한 고급 분석을 기반으로 디지털 포렌식 시장 점유율 44.62% 유지. 물리적 획득에서는 하드웨어 활용이 제한적이지만, 복호화 가속기가 수사 처리 능력을 지원합니다. 관리형 서비스는 턴키 확장을 원하는 기업들을 끌어들이고, 인력 부족이 지속되는 가운데 전문 서비스는 14.43%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다.

서비스 제공업체는 중소기업의 서비스형 포렌식 채택을 활용하여 사고 대응과 전문가 증언을 패키지로 제공합니다. 벤더들은 블록체인 계보 추적과 AI를 통한 선별을 통합하여 분석 주기를 단축함으로써 소프트웨어의 우위를 강화하고 있습니다. 플랫폼 라이선싱과 지속적인 서비스의 전략적 상호 작용은 수익 예측 가능성을 높이고, 벤더가 인접한 보안 기능을 교차 판매할 수 있게 해줍니다.

컴퓨터 포렌식은 2025년 매출의 36.55%를 차지했지만, 멀티 클라우드 환경에서의 기업 워크로드 증가에 따라 클라우드 포렌식이 12.96%의 가장 빠른 CAGR을 나타낼 것으로 예측됩니다. 모바일 포렌식은 암호화의 역풍에도 불구하고 진화하는 바이패스 툴킷에 힘입어 성장세를 유지하고 있습니다. 네트워크, 데이터베이스, IoT 조사는 제로 트러스트 아키텍처와 커넥티드 디바이스 증가로 인해 다양한 증거 스트림이 생성됨에 따라 확대되고 있습니다.

BFSI 분야의 규제 감사는 지속적인 클라우드 증거 대응에 대한 수요를 증폭시키고 전문 클라우드 네이티브 벤더의 기회를 확대하고 있습니다. SaaS에 대한 의존도가 높아지면서 클라우드 조사를 위한 디지털 포렌식 시장 규모는 2031년까지 컴퓨터 포렌식과의 격차를 좁힐 것으로 예측됩니다. 따라서 벤더들은 API 기반 수집, 휘발성 데이터 저장, 관할권별 세분화를 우선순위에 두고 채택을 촉진하기 위해 노력하고 있습니다.

북미는 2025년 매출의 34.65%를 차지할 것으로 예상되며, 대통령령 14144호와 AI 기반 조사 도입을 가속화하는 강력한 연방 예산이 뒷받침하고 있습니다. 팔란티아의 12억 달러에 달하는 정부 수익으로 대표되는 공공 부문 플랫폼 조달은 보다 광범위한 생태계 현대화를 촉진하고 있습니다.

아시아태평양은 13.16%의 연평균 복합 성장률(CAGR)로 성장을 주도하고 있으며, 이는 전자상거래의 확대와 2025년까지 3조 3,000억 달러에 달할 것으로 예상되는 사이버 범죄 비용 증가를 반영하고 있습니다. 중국의 국경 간 이전 면제 완화 등 규제가 정교해지면서 다국적 포렌식 제공업체들의 조사 마찰이 점차 줄어들고 있습니다.

유럽에서는 EU AI 법과 데이터 프라이버시 규제가 프라이버시 보호형 포렌식 툴에 대한 수요를 견인하며 균형 잡힌 성장세를 유지하고 있습니다. 중동 및 아프리카에서는 에너지 및 금융 회랑 방어를 위한 사이버 보안 예산이 배정되고, 라틴아메리카에서는 인력 부족의 제약에도 불구하고 지역의 디지털화 정책에 힘입어 점진적인 진전을 보이고 있습니다.

Digital forensics market size in 2026 is estimated at USD 8.46 billion, growing from 2025 value of USD 7.51 billion with 2031 projections showing USD 15.37 billion, growing at 12.68% CAGR over 2026-2031.

Growth pivots on cloud-native Software-as-a-Service investigations, deepfake countermeasures, and the integration of digital forensics within Extended Detection and Response platforms. Legislated mobile device extraction mandates and steady public-sector investments further underpin demand. Conversely, encryption-by-default and examiner shortages introduce operational friction yet also spur innovation in automated, cloud-based evidence preservation. Competitive dynamics remain moderately fragmented as established vendors embed artificial intelligence and blockchain-enabled chain-of-custody features to secure differentiation.

Cloud migrations are displacing traditional disk imaging, prompting the deployment of forensic platforms that capture volatile data across distributed, multi-tenant environments while meeting ISO/IEC 27035-4:2024 admissibility standards. Evidence isolation requirements and automated chain-of-custody tracking elevate demand for solutions pre-integrated with hyperscaler security services. As a result, vendors offering cloud-native acquisition APIs experience accelerated adoption among enterprises, particularly multinational corporations that navigate complex jurisdictional boundaries.

Machine-generated audio and video fraud now penetrates live interactions, forcing laboratories to replace legacy authentication with neural detection algorithms that achieve 91.82% accuracy on low-resolution content. BFSI institutions integrate blockchain provenance schemes to secure high-value transactions, while law-enforcement agencies invest in real-time screening tools to preserve evidentiary integrity during investigative interviews.

Hardware-backed encryption reduces extraction success to below 40% on recent devices, forcing reliance on premium decryption utilities and cloud-based evidence substitutes. Small agencies face budgetary barriers, widening investigative disparity and prompting policy debate on lawful access collaboration.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Software retained 44.62% of the digital forensics market share in 2025, underpinned by advanced analytics for encrypted and cloud evidence. Hardware usage remains niche for physical acquisitions, yet decryption accelerators support investigative throughput. Managed offerings capture enterprises seeking turnkey scalability, while professional services climb 14.43% CAGR as talent shortages persist.

Service providers capitalize on forensic-as-a-service adoption among SMEs, bundling incident response and expert testimony. Vendors integrate blockchain lineage and AI triage to compress analysis cycles, reinforcing software primacy. The strategic interplay between platform licensing and recurring services broadens revenue predictability, positioning vendors for cross-sell of adjacent security capabilities.

Computer forensics controlled 36.55% of 2025 revenue; however, cloud forensics now logs the fastest 12.96% CAGR amid multi-cloud enterprise workloads. Mobile forensics sustains growth despite encryption headwinds, supported by evolving bypass toolkits. Network, database, and IoT investigations expand as zero-trust architectures and connected devices generate diversified evidence streams.

Regulatory audits in BFSI amplify demand for continuous cloud evidence readiness, widening opportunities for specialized cloud-native vendors. Digital forensics market size for cloud investigations is poised to narrow the gap with computer forensics by 2031 as SaaS reliance deepens. Tool vendors therefore prioritize API-based collection, volatility preservation, and jurisdictional segmentation to boost adoption.

The Digital Forensics Market Report is Segmented by Component (Hardware, Software, and More), Type (Computer Forensics, Mobile Device Forensics, and More), Tool (Data Acquisition and Preservation, Forensic Data Analysis, and More), Organization Size (Large Enterprises, and Small and Medium Enterprises), End-User Vertical (BFSI, IT and Telecom and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America held 34.65% of 2025 revenue, aided by Executive Order 14144 and robust federal budgets that accelerate AI-driven investigative adoption. Public-sector platform procurements, exemplified by Palantir's USD 1.20 billion government revenue, cascade into broader ecosystem modernization.

Asia Pacific leads in growth at 13.16% CAGR, reflecting e-commerce expansion and rising cybercrime costs forecast at USD 3.3 trillion by 2025. Regulatory refinements, such as China's eased cross-border transfer exemptions, gradually reduce investigative friction for multinational forensics providers.

Europe sustains balanced expansion through the EU AI Act and data-privacy mandates driving privacy-preserving forensic tool demand. Middle East and Africa allocate cybersecurity budgets to defend energy and financial corridors, while Latin America shows incremental progress constrained by skill shortages yet supported by regional digitalization policies.