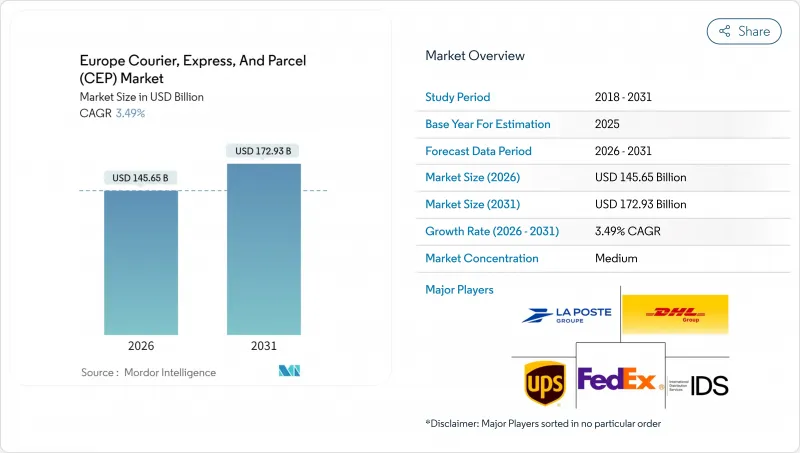

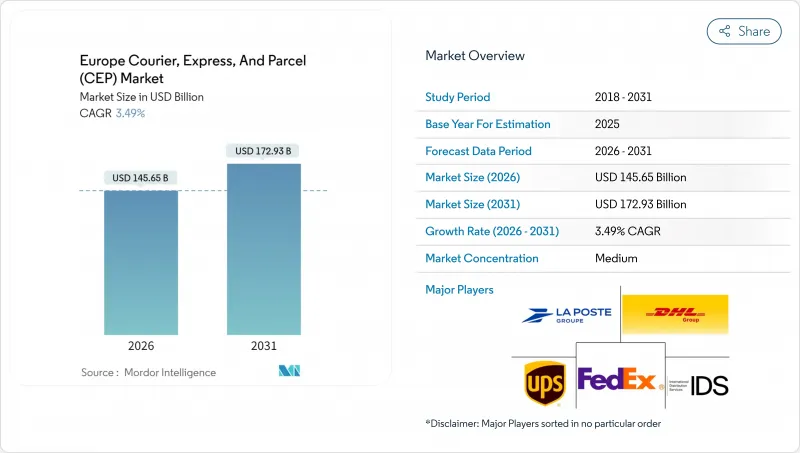

유럽 택배, 특송 및 소포(CEP) 시장 규모는 2026년 1,456억 5,000만 달러로 추정됩니다. 이는 2025년 1,407억 4,000만 달러에서 증가한 수치입니다. 2031년에는 1,729억 3,000만 달러에 이르고, 2026-2031년 동안 CAGR은 3.49%를 나타낼 전망입니다.

이 완만한 성장 곡선은 전자상거래 확대, 규제 조화, 기술 도입이 대륙 전체의 마지막 마일 네트워크를 재구성하는 동안 더 깊은 구조적 변화를 가리고 있습니다. 소매업체는 배송 경험의 차별화를 선호합니다. 유럽 구매자의 81%가 원하는 배송 옵션을 사용할 수 없는 경우 구매를 포기하기 때문에 경쟁의 초점은 가격에서 서비스 품질로 전환하고 있습니다. 2035년까지 단계적으로 실시되는 EU 수준의 디지털 시대의 부가가치세(VAT) 개혁(ViDA)은 국경 간 데이터 흐름을 표준화하고 첨단 컴플라이언스 시스템을 보유한 대규모 사업자를 선호합니다. 한편, 50만명이 넘는 운전자 부족이 자동화 투자를 가속화하고 있으며, 사업자는 노동력 부족에 직면하고 있습니다. 특히 네덜란드에서 지속가능성 요건을 강화하고 도시 중심부의 제로 배출구역 도입은 전기자동차 플릿과 택배 로커의 밀도 확대를 시급히 하고 있으며, 녹색자산 투자가 가능한 운송사업자 간의 통합을 촉진하고 있습니다.

소셜 커머스의 기세로 인해 소포 유통은 전통적인 계절성이 아니라 예측 불가능한 동향 주도의 피크로 향하고 있으며, 유럽의 택배, 특송 및 소포(CEP) 시장 전체에서 유연한 용량 계획이 요구되고 있습니다. 독일의 전자상거래용 포장자재 지출은 2025년에 39억 9,000만 달러에 이르렀으며, 2034년까지의 연평균 성장률(CAGR) 14.03%(2025-2030년)로 성장할 것으로 전망되고 있으며, 이 성장에 있어서의 포장 자재의 중요성을 뒷받침하고 있습니다. 반품이 어렵게 느껴지면 구매자의 79%가 구매를 취소하므로 역 물류의 고도화가 추가 기능에서 핵심 능력으로 전환되고 있습니다. 헬스케어 부문의 소포 배송도 이 옴니 채널의 파도를 타고 있습니다. DHL이 20억 유로(22억 달러)를 들여 전개하는 헬스케어 물류 사업은 전자 약국의 보급 확대에 대응한 전문적인 콜드체인 서비스를 자금면에서 지원하고 있습니다. 인플루언서 프로모션과 관련된 배송량의 집중화로 인해 운송 회사는 서비스 수준을 유지하면서 급증하는 트래픽을 흡수하기 위해 동적 라우팅 알고리즘의 설계를 강요하고 있습니다.

2030년 7월에 시행되는 ViDA의 전자 송장 의무화는 EU 역내 B2B 거래의 모든 형태가 EN16931 규격에 통일되어, 수작업에 의한 서류 처리가 삭감되어, 통관 수속이 신속화됩니다. 2028년 7월 원스톱 숍 시스템 확장은 회원국 간에 단일 VAT ID를 유지할 수 있게 해주며, 매일 수백만 건의 국경 간 소포를 취급하는 유럽 택배, 특송 및 소포(CEP) 시장에 큰 혜택을 제공합니다. 과세 사건 발생 후 10일 이내의 신고 의무화에 따라 고도의 IT 시스템 개수가 요구됩니다. 이로 인해 이미 통합 데이터 레이크를 운영하는 사업자가 이점을 얻을 수 있습니다. 동시에 수입관리시스템 2(ICS2)는 EU 국경을 통과하기 전에 상세한 수입 개요 제출을 의무화하고 보안 강화와 제품 수준의 상세 데이터 파이프라인을 가진 운송업체들에게 경쟁 우위를 제공합니다. 이러한 조치는 판매 확대 장벽을 줄이면서 디지털 컴플라이언스의 기준을 높이고 국제 통합을 향한 장기적인 변화를 촉진합니다.

유통 후 과잉 공급으로 인해 사업자가 점유율 방어를 위해 할인을 재개한 결과 유럽 택배, 특송 및 소포(CEP) 시장에서 취급량이 증가했음에도 불구하고 수익성이 떨어지고 있습니다. 체적 소비를 반영해야 하는 체중 중량 요금은 전략적 고객을 위해 면제되는 경우가 많으며 비용 효율성보다 빠른 속도로 마진을 압박합니다. 임포스트에 의한 요 Dell Inc와 센딩사의 인수는 고정비를 희석하기 위한 비유기적 밀도 확대로의 전환을 부각하고 있습니다. 운송회사는 피크시 요금이나 연료 서치를 추가하지만, 화주측은 멀티 캐리어 소프트웨어를 활용하여 요금 차익을 추구하고 이에 반발하고 있습니다. 이 줄다리기 상태는 단기적인 가격 회복을 제한하는 동시에 추가 산업 재편을 촉진합니다.

2025년의 EC부문의 점유율은 34.45%를 유지했지만, 2026-2031년에 걸쳐 의료품 소포가 CAGR 3.79%로 가장 급속히 확대될 전망입니다. 고령화와 온라인 약국의 확대로 온도관리된 라스트마일 배송이 우선 과제가 되고 있습니다.

DHL의 20억 유로(22억 달러) 규모의 프로그램은 GDP 준수 시설, 쿨 체인 포장 및 전용 관리 타워에 대한 투자를 추진합니다. 제조업체는 부품 전용 배송 경로가 필요하며 금융 서비스 문서는 보안 쿨리에의 틈새 시장을 지원합니다. 운송회사는 소매업의 한산기 동안 차량의 가동률 저하를 보완하기 위해 당일 집하의 바이오메디컬 항공편을 크로스셀하고 있습니다.

2025년 국제 소포 유통은 수익의 34.28%를 차지했으며, 국내 서비스는 유럽 택배, 특송 및 소포(CEP) 시장 점유율의 나머지를 유지했습니다. 국제화물은 2026-2031년에 걸쳐 CAGR 3.73%로 증가할 것으로 전망되며, VAT 결제의 간소화와 판매업체의 필필먼트 집중화로 국내 성장을 상회하는 속도로 확대됩니다.

유럽 소비자는 배송 시간이 국내 기준과 일치함에 따라 이웃 국가로부터의 구매를 증가시키고 있습니다. InPost가 2024년 11월에 EU8개국에서 전개한 네트워크는 수작업에 의한 분류나 통관 지연을 회피하는 로커간 배송 모델을 채택하고 있습니다. ICS2 데이터 요구사항은 역외 조달 품목의 리드타임을 초기에 연장하지만, EU 역내 루트에서는 마찰점이 감소합니다. 서비스의 예측가능성 향상으로 중소수출업체가 증가하고 기존 우편사업자는 추적시스템의 강화와 프리미엄 국경 간 서비스의 확충을 추진하고 있습니다.

The Europe courier, express, and parcel (CEP) market size in 2026 is estimated at USD 145.65 billion, growing from 2025 value of USD 140.74 billion with 2031 projections showing USD 172.93 billion, growing at 3.49% CAGR over 2026-2031.

This moderate trajectory masks deeper structural shifts as e-commerce expansion, regulatory harmonization, and technology adoption reshape last-mile networks across the continent. Retailers are prioritizing delivery-experience differentiation because 81% of European shoppers abandon baskets when preferred options are unavailable, tilting competitive focus from price to service quality. EU-level VAT in the Digital Age (ViDA) reforms, phased through 2035, are standardizing cross-border data flows, favoring scale players with advanced compliance systems. Meanwhile, a driver shortfall exceeding 500,000 openings has accelerated automation investment as operators grapple with labor scarcity. Heightened sustainability mandates and city-center zero-emission zones, notably in the Netherlands, add urgency for electric fleets and parcel-locker density, reinforcing consolidation among carriers that can fund green assets.

Social-commerce momentum is steering parcel flows toward unpredictable, trend-driven peaks rather than traditional seasonality, requiring flexible capacity planning across the Europe courier, express, and parcel (CEP) market. German e-commerce packaging spend reached USD 3.99 billion in 2025, reflecting 14.03% CAGR (2025-2030) expectations through 2034, underlining the packaging intensity of this growth. Reverse-logistics sophistication is turning from add-on to core capability, as 79% of shoppers cancel purchases when returns appear difficult. Healthcare parcels are piggybacking on this omnichannel wave; DHL's EUR 2 billion (USD 2.20 billion) health-logistics rollout funds specialized cold-chain services aligned with rising e-pharmacy penetration. Volume concentration around influencer promotions compels carriers to design dynamic routing algorithms to absorb traffic surges without impairing service-level compliance.

ViDA's e-invoicing mandate arriving in July 2030 will standardize EN16931 formats for all intra-EU B2B trades, shrinking manual paperwork and accelerating customs clearances. The July 2028 expansion of the One-Stop Shop lets merchants maintain a single VAT ID across member states, a boon for the Europe courier, express, and parcel (CEP) market handling millions of cross-border parcels daily. Advanced IT retrofits are required because declarations must be filed within 10 days of chargeable events, favoring operators that already run integrated data lakes. Concurrently, Import Control System 2 obliges detailed entry summaries before crossing EU borders, tightening security and tilting the playing field to carriers with rich product-level data pipelines. Together, these measures reduce friction in sales expansion while raising digital-compliance thresholds, shaping a long-run shift toward international consolidation.

Post-pandemic overcapacity has resurrected discounting as operators defend share, eroding yields despite volume growth in the Europe courier, express, and parcel (CEP) market. Dimensional-weight pricing, meant to reflect cubic consumption, often gets waived for strategic accounts, compressing margins faster than cost-line efficiencies. InPost's acquisitions of Yodel and Sending highlight the pivot toward inorganic density to dilute fixed overhead. Carriers add peak or fuel surcharges but shippers push back, leveraging multicarrier software to arbitrage rates. The tug-of-war limits near-term price recovery while stoking further consolidation.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

E-commerce retained a 34.45% share in 2025, yet healthcare parcels are set to rise fastest at 3.79% CAGR between 2026-2031. Aging populations and e-pharmacy expansion make temperature-controlled last-mile a priority.

DHL's EUR 2 billion (USD 2.20 billion) program funds GDP-compliant facilities, cool-chain packaging, and dedicated control towers. Manufacturers require part-express lanes, and financial-services documents sustain secure-courier niches. Carriers cross-sell same-day biomedical pickup to monetize vehicle downtime during retail off-peak cycles.

Cross-border parcel flows accounted for 34.28% of revenues in 2025 as domestic services retained the remainder of Europe courier, express, and parcel (CEP) market share. International consignments are forecast to climb at a 3.73% CAGR between 2026-2031, outpacing domestic growth as ViDA simplifies VAT settlement and merchants centralize fulfillment.

European shoppers increasingly purchase from neighboring states once delivery times align with domestic benchmarks. InPost's November 2024 network activation across eight EU countries uses a locker-to-locker model that bypasses manual sorting and customs delays. ICS2 data prerequisites initially elongate lead-times for goods sourced outside the bloc, but EU-internal routes face fewer friction points. Improved service predictability attracts SME exporters, prompting postal incumbents to upgrade track-and-trace and push into premium cross-border offerings.

The Europe Courier, Express, and Parcel (CEP) Market Report is Segmented by End User Industry (E-Commerce and More), Destination (Domestic and International), Speed of Delivery (Express and Non-Express), Shipment Weight (Heavy Weight Shipments, and More), Mode of Transport (Air, Road, and Others), and Model (Business-To-Business, and More). The Market Forecasts are Provided in Terms of Value (USD).