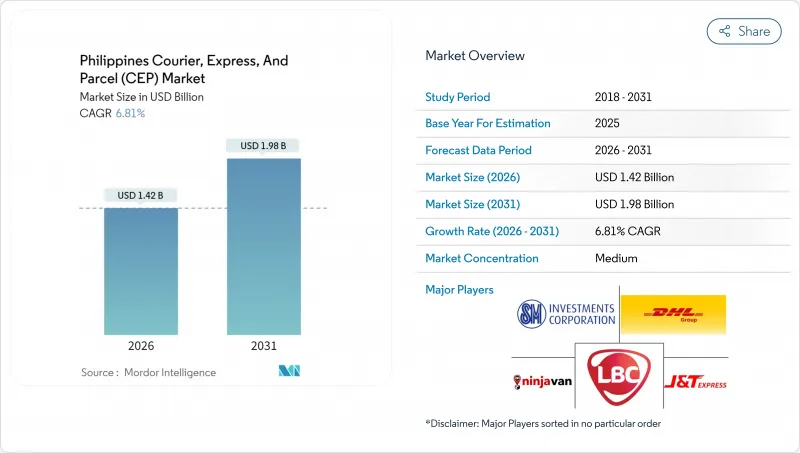

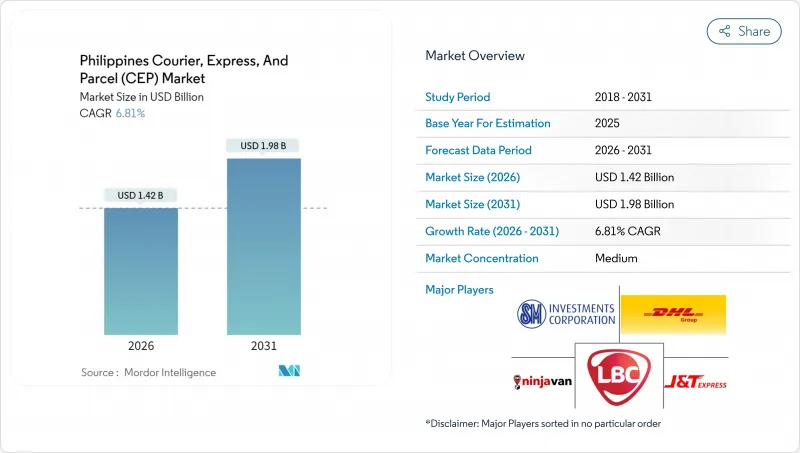

필리핀의 택배, 특송 및 소포(CEP) 시장은 2025년의 13억 3,000만 달러에서 2026년에는 14억 2,000만 달러로 성장하고 2026-2031년에 걸쳐 CAGR 6.81%로 성장을 지속하여, 2031년까지 19억 8,000만 달러에 달할 전망입니다.

이 성장은 급증하는 전자상거래량, 지속적인 인프라 투자, 섬나라라는 지역 특성에 의해 추진되고 있으며, 이들이 함께 섬간 배송 솔루션의 큰 잠재 시장을 형성하고 있습니다. 경쟁 격화, 규제 현대화, 실시간 가시성에 대한 소비자의 기대 고조에 따라 운영자에게 기술 기반 업그레이드 및 허브 앤 스포크 모델의 재설계를 촉구하고 있습니다. 연료 가격의 변동과 자산 집약적인 네트워크 요건이 소규모 사업자에게 부담을 가하고 있는 가운데, 규모가 큰 사업자는 자동화를 활용해 이익률을 보호하여 산업 재편의 압력이 높아지고 있습니다. 그 결과, 필리핀의 택배, 특송 및 소포 시장은 양을 중시하는 모델에서 속도, 신뢰성, 지리적 도달범위를 중시하는 기술 주도의 서비스 차별화형 시장으로 진화하고 있습니다.

전자상거래 거래액은 2025년까지 국내총생산(GDP)의 5.5%를 차지한 것으로 나타났으며, 소비자 1인당 소포 배송 빈도는 평균 3배로 증가해 기존의 구분처리 능력을 압박하고 있습니다. 사업자들은 7,641개의 섬을 가로지르는 다수의 운송 모드를 조정형 고처리량 자동 시스템과 동적 라우팅 툴로 전환하고 있습니다. 모듈형 허브, 확장 가능한 소프트웨어, 데이터 구동 용량 계획을 통해 필리핀의 택배, 특송 및 소포(CEP) 시장은 비례적인 비용 증가 없이 소규모 및 고빈도 배송의 물결을 흡수할 수 있게 되었습니다. 가전제품과 패션을 필두로 하는 소매 카테고리는 평균 소포 수익을 압축하면서 총 취급량을 높여, 고밀도 경로를 달성한 운송업자에게 이익을 가져오고 있습니다. 전자상거래 플랫폼은 낙찰 조건으로 배달 시간 보장을 점점 더 중시하고 있으며 운송업체에게 예측 분석 및 실시간 시각화를 촉구하고 있습니다. 로봇 분류기 및 API(Application Programming Interface) 통합에 대한 투자는 필리핀의 택배, 특송 및 소포(CEP) 시장에서 경쟁을 유지하기 위한 필수 조건이 되고 있습니다.

마닐라 도심에는 1,300만 명의 주민이 밀집한 도로망이 있으며, 교통 정체가 역설적으로 밴보다 기동력이 있는 이륜차 배송을 유리하게 하고 있습니다. 당일 도착은 프리미엄 서비스에서 기본 요건으로 바뀌었고, 배송업체는 도시 지역 내에 마이크로풀필먼트 거점을 전개하고 있습니다. 이 사이트는 배송 거리를 줄이고 배송 실패 위험을 낮춰 2시간 이내라는 엄격한 배송 범위를 제공합니다. 실시간 추적, 자동 배송 인증, 사전 고객 알림은 주요 플랫폼의 표준 기능이 되었습니다. 가시성 기준을 충족하지 못하는 운송 회사는 투명한 GPS 지원 서비스로 점유율을 얻는 앱 기반 경쟁사에게 고객을 빼앗길 위험이 있습니다. 당일 배송 서비스의 자본 집약성에 대응하기 위해 대기업은 자산 경량형 프랜차이즈 모델을 실험 중입니다. 이는 자사 소유의 허브와 크라우드소싱에 의한 배달원 공급을 융합시켜 필리핀의 택배, 특송 및 소포(CEP) 시장에서 급성장을 지원하는 네트워크 밀도를 강화하는 것입니다.

마닐라항과 세부항은 성수기에 설계처리능력을 40-50% 초과하는 가동이 상시화되어 평균 2일간의 체류 초과가 발생하고 이는 다운스트림 배송 보장으로 파급됩니다. 제한된 접안 슬롯과 수작업으로 인한 컨테이너 취급은 선박의 턴어라운드를 연장하고, 날씨로 인한 RORO(롤온 롤오프)선의 결항은 재고 경량 모델에 중요한 운항 리듬을 방해합니다. 항만 자동화와 버스 확대 프로젝트가 완료되기 전에는 필리핀의 택배, 특송 및 소포(CEP) 시장에서 서비스 수준을 유지하기 위해 운송 회사는 비축 재고 유지, 여러 항만을 상정한 대체 경로의 확보, 고객과의 커뮤니케이션 프로토콜 정비가 요구됩니다.

2025년에는 전자상거래가 42.10%의 점유율을 차지했으며, 온라인 마켓플레이스, D2C 브랜드, 소셜 셀러가 함께 1차 출하량의 급증을 견인했습니다. 창고 보관, 반품 관리 및 옴니채널 통합 서비스를 결합하여 대규모 플랫폼 고객의 관리 능력이 강화되었습니다. 의료 물류는 원격 의료, 백신 배포, 우편 배송 프로그램이 온도 관리, 관리 체인 준수, 신속한 이행을 요구하면서 2026-2031년에 걸쳐 견조한 7.10%의 연평균 복합 성장률(CAGR)을 기록할 전망입니다. GDP 인증 창고, 검증된 포장, 규정 준수 서류는 필리핀의 택배, 특송 및 소포(CEP) 시장에서 중요한 차별화 요인이 됩니다.

금융 서비스 부문(신용카드 명세서, 법적 문서 등)에서는 디지털 채널로의 전환이 꾸준히 진행되고 있지만, 특정 규제 워크플로에서는 여전히 안전한 물리적 인도가 필요합니다. 제조 및 도매업의 선적에는 중량 SKU와 정기적인 대량 주문 패턴이 포함되어 있습니다. 농업 및 광업을 포함한 1차 산업은 시간 엄수 샘플, 예비 부품 및 규정 준수 문서의 운송을 택배 네트워크에 의존하고 있으며, 이는 이 부문이 국가 경제의 현대화와 널리 관련되어 있음을 뒷받침합니다.

국내 물류는 2025년 매출의 64.40%를 차지하였으며, 이는 네트워크 밀도가 높기 때문에 소포 단가가 하락하는 마닐라-세부-다바오 삼각지대에서의 집중적인 거래를 반영하고 있습니다. 사업자는 고정 경로 트럭 운송과 모듈형 마이크로 창고를 활용하여 루손섬 내 70%의 발송지-도착지 쌍에서 48시간 이내의 배달을 실현하고 있습니다. 필리핀의 택배, 특송 및 소포 시장에서 국내 물류의 규모는 꾸준한 성장이 예상되지만, 앱 기반 경쟁사가 할인을 강화하는 가운데, 이익률의 저하에 직면할 전망입니다. 국제 소포는 절대량은 작지만, 크로스보더 EC 구입품, 발릭바얀 박스(해외 거주 필리핀인용 소포), 해외 바이어용 중소 영세 기업(MSME)의 수출화물에 견인되어 2026-2031년에 걸쳐 CAGR 7.05%를 기록할 전망입니다. 통관, 항공화물 공간, 규제 준수에 대한 프리미엄 가격 설정이 단위경제성의 향상을 뒷받침하고, 크로스보더 사업은 필리핀의 택배, 특송 및 소포(CEP) 시장 전체에서 이익 안정화 요인이 되고 있습니다.

양자간 무역협정의 확대와 전자통관 플랫폼의 도입으로 통관 시간이 최대 48시간 단축되면서 지역 내 경쟁사와의 서비스 품질 격차가 축소되고 있습니다. 클라크 공항과 세부 공항에 통합 화물 터미널이 추가됨으로써 남북 간의 화물 분산이 진행되어 마닐라 허브의 부담이 경감되었습니다. 이에 따라 신선품과 고가 전자기기의 수송이 가속화되고 있습니다. 시장의 선도기업은 현재 국제 배송과 현지 반품 준비를 결합한 서비스를 제공하고 있으며, 해외 거주자에 의한 송금 연동형 구매를 활용함과 동시에 필리핀의 택배, 특송 및 소포(CEP) 시장의 세계 연결성을 확대하고 있습니다.

The Philippines courier, express, and parcel market is expected to grow from USD 1.33 billion in 2025 to USD 1.42 billion in 2026 and is forecast to reach USD 1.98 billion by 2031 at 6.81% CAGR over 2026-2031.

This growth is propelled by surging e-commerce volumes, sustained infrastructure investment, and the country's archipelagic geography, which together create a large addressable base for island-to-island delivery solutions. Intensifying competition, regulatory modernization, and rising consumer expectations for real-time visibility are prompting operators to upgrade technology stacks and redesign hub-and-spoke models. Consolidation pressure is growing as fuel price volatility and asset-heavy network requirements strain smaller fleets, while scale players leverage automation to protect margins. As a result, the Philippines courier, express, and parcel market is evolving from a volume-oriented model toward a technology-enabled, service-differentiated landscape that prizes speed, reliability, and geographic reach.

Transaction values are expected to represent 5.5% of national GDP in 2025, tripling the average parcel frequency per consumer and stretching existing sortation capacity. Operators are pivoting to high-throughput automation and dynamic routing tools that can orchestrate multiple transport modes across 7,641 islands. Modular hubs, scalable software, and data-driven capacity planning are enabling the Philippines courier, express, and parcel market to absorb a wave of small, frequent shipments without proportionate cost increases. Retail categories led by consumer electronics and fashion are compressing average parcel revenue yet boosting overall volume, rewarding carriers that achieve densification at the route level. E-commerce platforms increasingly condition tender awards on guaranteed delivery windows, pushing carriers toward predictive analytics and real-time visibility. Investments in robotic sorters and application-programming-interface integrations are becoming table stakes for relevance in the Philippines courier, express, and parcel industry.

Metro Manila houses 13 million residents within a dense road network where traffic congestion paradoxically favors nimble motorcycle fleets over vans. Same-day arrival has shifted from premium to baseline expectation, prompting couriers to roll out micro-fulfillment nodes inside the metropolis. These nodes shorten stem mileage, lower failed-delivery risk, and enable tighter two-hour delivery windows. Real-time tracking, automated proof-of-delivery, and proactive customer notifications are now standard features across leading platforms. Carriers that fail to meet visibility benchmarks risk customer churn as app-based challengers capture share with transparent, GPS-enabled service. To meet the capital intensity of same-day service, larger players are experimenting with asset-light franchise models that blend company-owned hubs with crowd-sourced rider supply, reinforcing the network density that underpins express profitability within the Philippines courier, express, and parcel market.

Manila and Cebu ports routinely operate at 40-50% above designed throughput during peak periods, creating two-day average dwell overruns that ripple into downstream delivery commitments. Limited berthing slots and manual container handling extend vessel turnaround, while weather-driven RORO cancellations disrupt the sailing cadence vital for inventory-light models. Until port automation and berth expansion projects reach completion, carriers must maintain buffer inventory, multi-port contingency routes, and customer communication protocols to protect service levels in the Philippines courier, express, and parcel market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

E-commerce commanded 42.10% share in 2025 as online marketplaces, direct-to-consumer brands, and social sellers collectively fueled daily shipment spikes. Bundled warehousing, returns management, and omnichannel integration services enhance retention of large platform accounts. Healthcare logistics posts a robust 7.10% CAGR between 2026-2031 as telemedicine, vaccine distribution, and prescription-by-mail programs demand temperature integrity, chain-of-custody compliance, and rapid fulfillment. GDP-certified warehouses, validated packaging, and regulatory-aligned documentation become critical differentiators in the Philippines courier, express, and parcel industry.

Financial-services parcels credit-card statements, legal documents-continue a measured migration to digital channels but still require secure physical handover in certain regulatory workflows. Manufacturing and wholesale shipments incorporate heavier SKUs and scheduled bulk-order patterns. Primary industries including agriculture and mining rely on courier networks for time-sensitive samples, spare parts, and compliance paperwork, underscoring the sector's broad-based relevance to national economic modernization.

Domestic flow anchored 64.40% of 2025 revenue, reflecting concentrated trade along the Manila-Cebu-Davao triangle where network density lowers per-parcel cost. Operators leverage fixed-route trucking and modular micro-depots to hit sub-48-hour delivery for 70% of intra-Luzon origin-destination pairs. The Philippines courier, express, and parcel market size for domestic services is projected to grow steadily yet face thinning margins as app-based competitors intensify discounting. International parcels, although smaller in absolute volume, register a 7.05% CAGR between 2026-2031, driven by cross-border e-commerce purchases, balikbayan boxes, and export shipments from MSMEs tapping overseas buyers. Premium pricing for customs clearance, airfreight space, and regulatory compliance underpins higher unit economics, making cross-border a profit stabilizer within the wider Philippines courier, express, and parcel market.

Expanding bilateral trade agreements and electronic customs platforms are shaving up to 48 hours off clearance times, narrowing service-quality gaps with regional peers. As Clark and Cebu airports add integrated cargo terminals, north-south diversion reduces Manila hub pressure, enabling faster transit for perishables and high-value electronics. Market leaders now bundle international shipping with localized returns orchestration, capitalizing on the diaspora's remittance-linked purchases and expanding the Philippines courier, express, and parcel industry's global connectivity.

The Philippines Courier, Express, and Parcel Market Report is Segmented by End User Industry (E-Commerce and More), Destination (Domestic and International), Speed of Delivery (Express and More), Shipment Weight (Heavy Weight Shipments and More), Mode of Transport (Air, Road, and Others), and Model (Business-To-Business, Business-To-Consumer, and Consumer-To-Consumer). The Market Forecasts are Provided in Terms of Value (USD).