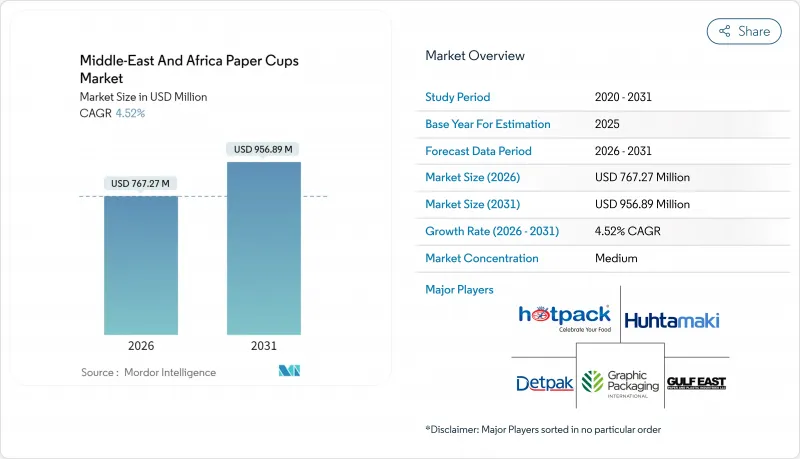

중동 및 아프리카의 종이컵 시장은 2025년에 7억 3,409만 달러로 평가되었으며, 2026년 7억 6,727만 달러에서 2031년까지 9억 5,689만 달러에 이를 것으로 예측됩니다.

예측기간(2026-2031년)의 CAGR은 4.52%로 전망되고 있습니다.

관광업의 강력한 회복이 성장을 뒷받침하며 푸드 딜리버리 플랫폼의 보급과 배리어 코팅의 혁신에 대한 지역 컨버터의 지속적인 투자가 이루어지고 있습니다. 걸프협력회의(GCC) 국가의 규제 기한은 소재 대체를 가속화하고 있습니다. 한편, 공장의 효율성 향상과 기업의 넷 제로 로드맵은 인증을 취득한 퇴비화 코팅재에 대한 수요를 강화하고 있습니다. 경쟁은 중간 정도이며 다국적 기업은 비용 절감을 위해 지역사업 기반을 통합하고, 지역 유력 기업은 태양광 발전 플랜트 및 생분해성 기술에 자본을 투입하여 접객 및 퀵서비스 레스토랑(QSR) 채널 전반에 걸쳐 브랜드 계정을 확보하고 있습니다. 수입에 의존하는 사하라 이남의 일부 시장에서는 원료의 가격 변동과 전력 부족이 여전히 계속되고 있지만, 전문 카페, 기관 급식, 편의점 등 다양한 최종 사용자 기반이 종이컵 시장의 수익 확대에 유리한 기반을 유지하고 있습니다.

스페셜티 커피 체인, 직장용 케이터링, 교통 거점에서의 귀가 중 소비가 GCC 도시권에서 정착하고 있어, 종이컵 시장에서 프리미엄 핫컵 수요의 구조적인 상승을 가져오고 있습니다. GCC 지역의 접객 산업 매출은 2028년까지 481억 달러에 이를 것으로 예측되며, 2022년부터의 CAGR은 7.5%로 나타났습니다. 또한 국제관광객수는 연간 8.1%의 속도로 증가하여 1억 1,620만 명에 이를 전망입니다. 호텔과 카페에서는 특히 두바이가 목표로 하는 400회의 국제 이벤트와 카타르의 연간 80회 이상의 전시회에서 차별화된 컵 디자인을 활용하여 브랜드 ID의 강화를 도모하고 있습니다. 2030년까지 커피 체인 매장 수는 CAGR 5.25%로 확대될 전망이며 이는 서양의 카페 문화와 기존 아라비아 커피의 의식을 양립시키는 젊은 층의 기호 변화를 반영하고 있습니다. 신규 출점마다 사업자는 지속 가능한 핫컵 사양을 표준화하여 종이컵 시장의 침투를 촉진하고 있습니다.

COP28 이후 규제 체제가 가속화되어 플라스틱에서 종이로 즉각적인 조달 전환이 촉구되었습니다. 아랍에미리트(UAE)에서는 2006년에 경질 폴리스티렌 컵의 사용을 금지하고, 아부다비 환경청 주도의 단계적 시책에 의해 2022년에는 뚜껑, 젓개, 식기로 규제를 확대했습니다. 두바이 공항에서는 2020년에 일회용 플라스틱을 배제하였고, 사우디아라비아에서는 2017-2019년에 걸쳐 3단계의 단계적 플라스틱 폐지를 실시했습니다. 이러한 프레임워크는 QSR 체인, 호텔 및 소매업체가 재활용 가능성과 미래 생산자 책임 재활용(EPR) 의무에 부합하는 섬유 기반 형태를 우선시하도록 하여 규제가 종이컵 시장에 미치는 견인력을 강조합니다.

수백개의 회사에 이르는 소규모 컨버터는 주로 단가 경쟁에 주력하고 있으며, 규모의 경제가 제한되어 고성능 코팅에 대한 투자 의욕도 둔화되고 있습니다. 후타마키사가 아랍에미리트(UAE) 생산을 통합하고, 핫팩 글로벌사가 두바이의 멀티라인 공장을 가동하는 가운데, 대기업이 호텔이나 다국적 QSR 체인과의 계약을 획득하는 한편, 소규모 기업은 상품 부문에 머무르는 양극화 구조가 현재화하고 있습니다. 이익률의 압박에 의해 소규모 시설의 연구개발 예산이 제약되어 종이컵 시장에서의 광범위한 기술 보급이 둔화되고 있습니다.

2025년 종이컵 시장에서는 점유율의 62.40%를 핫컵이 차지한 반면, 콜드컵은 4.74%의 연평균 복합 성장률(CAGR)이 예상되면서 가장 빠른 성장 부문이 되었습니다. Smart Planet의 EarthCoating-Bio(플라스틱 함량을 최대 51% 감량) 등 기술 혁신으로 냉음료 형태의 결로 및 차단성 과제가 해결되고 있습니다. QSR 체인과 편의점은 스무디와 단백질 쉐이크 등 음료 메뉴를 확충하고 있으며, 걸프 지역에서 일반적인 40°C 환경에서도 제품 품질을 유지할 수 있는 내구성 있는 콜드컵에 대한 수요가 높아지고 있습니다. 핫컵은 여전히 기관용 케이터링과 오피스 커피 서비스에서는 주류이지만, 이중벽 구조의 혁신으로 호스피탈리티 사업자는 슬리브 재고를 줄이고 고객의 만족도를 향상시켜 종이컵 시장에서 지속적인 수요량을 확보하고 있습니다.

온난기에는 아이스 음료의 수요가 급증하고 소매업체는 브랜드 프로모션용 커스텀 프린트를 인쇄한 계절 한정 콜드컵 SKU를 주문합니다. 이 계절 변동은 인바운드 관광의 피크와 연동하여 하계 분기의 수익 집중을 강화합니다. 한편, 마이크로 로스터리 카페나 부티크 찻집에서는 촉각적인 차별화를 도모하기 위해 텍스처 가공된 핫컵 마감을 선호합니다. 두 부문에 대한 지속적인 투자는 종이컵 시장 전체의 균형 잡힌 성장을 보장합니다.

폴리에틸렌 라이닝은 안정적인 성능과 비용 경쟁력으로 2025년 종이컵 시장 전체의 70.80%를 차지했습니다. 그러나 폴리유산(PLA) 및 기타 퇴비화 코팅은 기업 구매자가 플라스틱 제로 조달 지침을 채택하면서 4.83%의 연평균 복합 성장률(CAGR)로 우위를 확대하고 있습니다. 수성 분산 기술은 유지 및 습기 차단 성능을 유지하면서 표준지 재활용 프로세스에서의 재생 가능성을 지원하여 지자체의 폐기물 분별 처리를 용이하게 합니다. GCC 지역의 호텔 체인은 이미 조달 문서에 퇴비화 인증을 명시하고 있으며, 이는 에코 코팅으로의 구조적 전환을 시사하고 있습니다.

PE 라이닝 컵은 탁월한 열 보존성으로 인해 고온 충전 용도로 여전히 정착하고 있지만, 플라스틱 함량을 3분의 1로 줄이는 하이브리드 소재에 대한 규제 승인이 신속하게 진행되고 있습니다. 수성 또는 광물계 차단 기술에 조기 투자한 컨버터는 다국적 푸드서비스 브랜드에서 선행 우위를 획득하여 종이컵 시장의 프리미엄 층을 확고히 하고 있습니다.

The Middle-East and Africa paper cups market was valued at USD 734.09 million in 2025 and estimated to grow from USD 767.27 million in 2026 to reach USD 956.89 million by 2031, at a CAGR of 4.52% during the forecast period (2026-2031).

A robust tourism rebound reinforces growth, the proliferation of food-delivery platforms, and sustained investments by regional converters in barrier-coating innovation. Regulatory deadlines in the Gulf Cooperation Council (GCC) nations are accelerating material substitution, while improving mill efficiency and corporate net-zero roadmaps strengthen demand for certified compostable coatings. Competitive intensity is moderate: multinational incumbents consolidate regional footprints to reduce costs, and local champions deploy capital toward solar-powered plants and biodegradable technologies to secure brand accounts across hospitality and quick-service restaurant (QSR) channels. Although raw-material volatility and electricity shortages persist in several import-dependent and Sub-Saharan markets, a diversified end-user base-spanning specialty cafes, institutional catering, and convenience retail-maintains a favorable baseline for revenue expansion in the paper cups market.

Specialty coffee chains, workplace catering, and transit hubs are normalizing grab-and-go consumption across GCC cities, causing a structural uplift in premium hot-cup demand in the paper cups market. GCC hospitality revenue is projected to reach USD 48.1 billion by 2028, marking a 7.5% CAGR from 2022, and international arrivals are on an 8.1% annual trajectory to 116.2 million visitors. Hotels and cafes leverage differentiated cup graphics to reinforce brand identity, particularly during Dubai's targeted 400 global events and Qatar's 80-plus annual exhibitions. A 5.25% CAGR in coffee-chain volume through 2030 mirrors shifting consumer preferences among younger demographics who balance Western cafe culture with traditional Arabic coffee rituals. With every incremental store opening, operators standardize sustainable hot-cup specifications, thereby deepening penetration of the paper cups market.

Regulatory regimes gained momentum after COP28, prompting immediate procurement switches from plastic to paper. The UAE banned rigid polystyrene cups as early as 2006 and, through staged policies led by the Environment Agency - Abu Dhabi, extended restrictions to lids, stirrers, and cutlery in 2022. Dubai airports eliminated single-use plastics in 2020, while Saudi Arabia executed a three-stage plastic phase-out between 2017 and 2019. These frameworks force QSR chains, hotels, and retailers to favor fiber-based formats compliant with recyclability and future extended producer responsibility (EPR) mandates, underscoring the regulatory pull on the paper cups market.

Hundreds of small converters compete primarily on unit price, limiting scale economies and dampening investments in high-performance coatings. As Huhtamaki consolidates UAE production and Hotpack Global ramps a multi-line Dubai plant, a two-tier structure emerges where large players secure hotel and multinational QSR contracts, while small firms remain trapped in commodity niches. Margin pressures restrict R and D budgets among smaller facilities, slowing broad-based technology diffusion in the paper cups market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Cold variants represented the fastest-moving segment with a 4.74% CAGR projection, even as hot cups accounted for a dominant 62.40% share of the paper cups market size in 2025. Technical advances such as Smart Planet's EarthCoating-Bio, which trims plastic content by up to 51%, address condensation and barrier limitations in chilled-drink formats. QSR chains and convenience retailers extend beverage menus to smoothies and protein shakes, elevating demand for durable cold cups that uphold product quality in 40 °C ambient conditions common across the Gulf. Hot cups retain primacy in institutional catering and office coffee service, but double-wall innovations help hospitality operators reduce sleeve inventory and elevate guest comfort, ensuring sustained volume within the paper cups market.

In warmer months, iced beverage volumes surge, prompting retailers to order seasonal cold-cup SKUs with custom prints for brand promotion. This seasonal swing aligns with inbound tourism peaks, reinforcing revenue concentration in the summer quarters. Meanwhile, micro-roaster cafes and boutique tea houses favor textured hot-cup finishes for tactile differentiation. Continuous investments in both segments assure balanced growth across the paper cups market.

Polyethylene linings captured 70.80% of the overall paper cups market share in 2025, thanks to predictable performance and cost competitiveness. Yet polylactic acid and other compostable coatings are gaining a 4.83% CAGR edge as corporate buyers adopt zero-plastic procurement guidelines. Water-based dispersion technology demonstrates recyclability in standard paper streams while matching grease and moisture barriers, easing municipal waste-sorting processes. GCC hotel chains already stipulate compostable credentials in tender documents, signaling a structural pivot toward eco-coatings.

PE-lined cups remain entrenched for high-temperature fill operations because of thermal-sealing robustness, but hybrid substrates that cut plastic content by one-third enjoy faster regulatory clearances. Converters investing early in aqueous or mineral-blend barriers gain first-mover advantages among multinational foodservice brands, consolidating premium tiers of the paper cups market.

The Middle-East and Africa Paper Cups Market is Segmented by Cup Type (Hot Paper Cups, Cold Paper Cups), Material Lining (Polyethylene Coated, Polylactic-Acid Compostable, and More), Application (Quick-Service Restaurants, Institutional Catering, Coffee Chains and Cafes, Retail and Convenience Stores), Capacity (Up To 7 Oz, 8-12 Oz, 13-16 Oz, Above 16 Oz), and Country. The Market Forecasts are Provided in Terms of Value (USD).