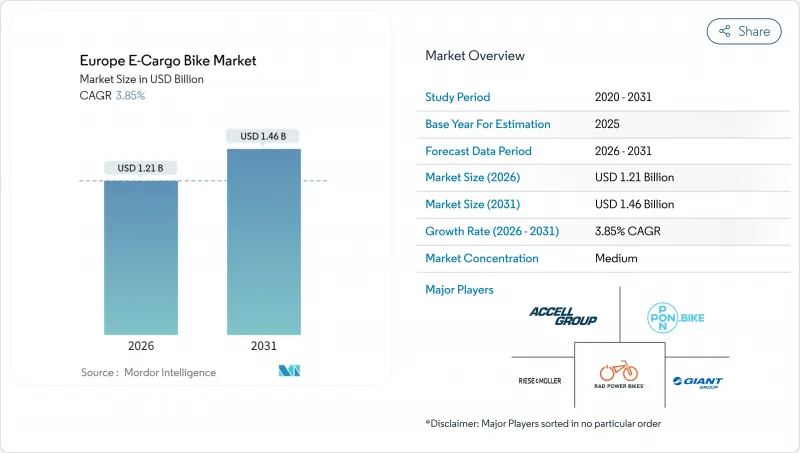

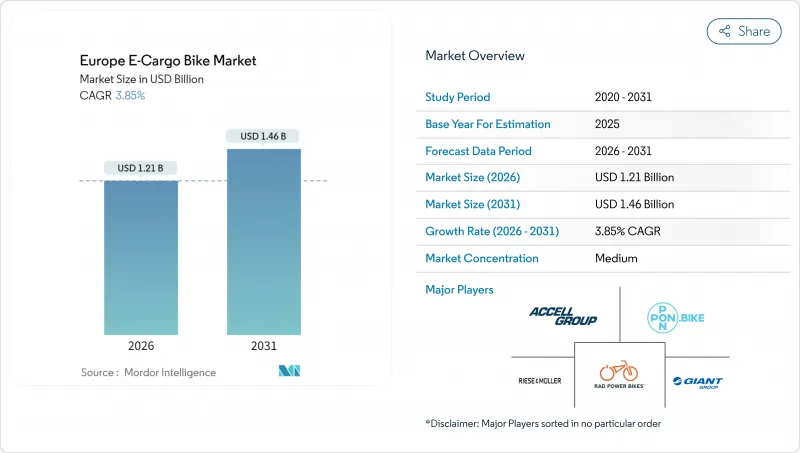

유럽의 전기 화물 자전거 시장 규모는 2026년에 12억 1,000만 달러로 추정되고 있습니다. 이는 2025년 11억 6,000만 달러에서 성장한 수치이며, 2031년에는 14억 6,000만 달러에 이를 것으로 예측되고 있습니다. 2026-2031년에 걸쳐 CAGR 3.85%로 성장이 전망되고 있습니다.

이 전망은 성숙기에 접어든 수요 곡선을 반영합니다. 지원적 규제, 리튬이온 배터리 비용 하락, 도시 물류 구조 재편이 계속해서 채택을 촉진하지만, 초기 몇 년간 보였던 폭발적인 증가세는 보이지 않는다. 도시 차원의 무공해 배송 구역, 상업용 차량에 대한 관대한 보조금, 고밀도 마이크로 풀필먼트 네트워크가 종합적으로 사업 타당성을 강화하는 한편, 배터리 USD/kWh의 급격한 하락은 주요 비용 장벽을 제거했습니다. 경쟁 강도는 여전히 중간 수준이다 : 기존 자전거 브랜드들은 수직 통합과 서비스 네트워크를 활용하지만, 디지털 중심 신규 진입자들이 조달이 온라인으로 전환되면서 가격 압박을 가하고 있습니다. 한편, 부문 동향을 살펴보면 페달 보조 구동계, 리튬이온 배터리, 미드드라이브 모터, 중상위 가격대가 서유럽 허브 지역 전반에 걸친 주류 상업용 사양을 정의하고 있습니다.

유럽의 지자체들은 무공해 배송 구역을 꾸준히 확대하며 물류 운영사들로 하여금 차량 경제성을 재검토하도록 압박하고 있습니다. 암스테르담이 2025년부터 도심 내 화석연료 밴 운행을 금지함에 따라 전기 화물자전거 선행 구매가 이미 촉발되었습니다. 런던의 초저공해구역(ULEZ)은 디젤 밴에 일일 요금을 부과하는데, 이 요금이 총소유비용(TCO)을 전기 보조 화물자전거 쪽으로 결정적으로 기울게 하는 임계점을 초과할 수 있습니다. 독일, 프랑스, 네덜란드의 규제 수렴은 이러한 비용 신호를 강화하며, 아마존 물류와 같은 범유럽 차량 운영사들이 베를린, 파리, 밀라노에 마이크로모빌리티 물류 거점을 표준화하도록 촉구하고 있습니다. 더 많은 도시들이 내연기관 밴의 단계적 폐지 일정을 발표함에 따라, 운영사들은 유럽의 전기 화물 자전거 시장을 관할 구역 간 경로 유연성을 유지하는 규정 준수 헤지 수단으로 보고 있습니다.

현재 국가 및 지방자치단체의 인센티브 프로그램은 이제 소비자보다 기업 구매자를 대상으로 합니다. 독일의 BAFA 제도는 구매 비용의 최대 25%를 환급하며, 보조금 적용 범위를 확대하는 지역 보조금과 중복 적용이 가능합니다. 프랑스의 5,500만 유로(약 6,400만 달러) 규모 자전거 투자 기금은 상업용 전기 화물 차량 군에 보조금을 지원합니다. 네덜란드는 중소기업을 대상으로 상당한 화물 자전거 구매 지원금과 세금 공제를 추가로 제공합니다. 이러한 인센티브는 고이용률 서비스의 투자 회수 기간을 단축시켜, 서유럽에서 기업 구매자가 주문량을 주도하는 이유를 설명합니다.

대부분의 유럽 도시는 상업용 전기 화물 자전거 전용 노변 충전기를 갖추지 못하고 있습니다. 이에 운행 업체들은 운영을 차고지에 의존하게 되며, 800Wh 배터리가 4A 충전기에서 완전 충전까지 최대 6시간이 소요될 때 부동산 비용과 가동 중단 비용이 발생합니다. 개방형 표준 부재로 혼합 차량군은 다수 공급업체의 독점적 도크를 설치해야 하여 자본 예산을 압박합니다. 마드리드, 로마, 아테네 등 남유럽 허브 지역은 공유 마이크로모빌리티 정책이 상업용 화물 자전거보다 스쿠터에 집중되어 가장 큰 격차를 보입니다. 시의회가 적재 구역에 도로변 충전을 의무화하기 전까지는 유럽의 전기 화물 자전거 시장을 노리는 택배 스타트업의 시범 차량군 이상 확장은 여전히 어렵습니다.

페달 보조 구동계는 2025년 유럽의 전기 화물 자전거 시장 점유율의 92.58%를 차지했으며, 이는 EU 규정 168/2013에 따라 자전거로 분류되어 자동차 보험 및 면허 취득이 면제됨을 반영합니다. 규제 확실성의 안정성은 기업 구매자들이 평균 적재량이 약 120kg인 일반 택배 배송 부문에서 이 카테고리에 계속 머물게 합니다. 대형 택배사들이 교육 및 규정 준수 비용을 최소화하기 위해 차량을 표준화함에 따라 유럽 페달 보조 전기 화물 자전거 시장 규모는 꾸준히 성장할 전망입니다.

그러나 스로틀 보조 방식은 4.35%의 연평균 성장률을 기록할 전망입니다. 무거운 식료품, 가구, 도시 폐기물 운송에는 라이더 체력에 영향을 받지 않는 지속적인 동력이 필요하기 때문입니다. 독일, 프랑스, 이탈리아가 시속 25km 이하의 동력 등급 정의를 통일함에 따라, 차량 관리자는 책임 보험 범위를 확대하지 않고도 스로틀 보조 장치를 도입할 수 있게 되었습니다. 이에 따라 제조사들은 운영자가 규정 준수 등급을 전환할 수 있는 듀얼 모드 컨트롤러를 출시하여 변화하는 도시 규정에 대비한 자산의 미래 대비를 가능하게 합니다.

리튬 이온 기술은 2025년 유럽의 전기 화물 자전거 시장 규모에서 89.65%의 점유율을 차지했으며, 킬로와트시 비용이 급락함에 따라 4.02%의 CAGR로 계속 상승하고 있습니다. 배터리 팩 수명은 이제 상당한 완전 충전 사이클에 도달하여 기업 차량 교체 주기와 일치합니다. LFP(리튬 인산철) 화학은 고유한 열 안정성과 주목할 만한 사이클 내구성 덕분에 대부분의 시장 점유율을 차지하며, 이는 고회전 택배 업무에 필수적인 특성입니다.

납축전지는 구매 가격이 총소유비용보다 중요한 초급 소비자용 화물 자전거에만 잔존합니다. 고체 배터리 프로토타입은 주목받지만 상용화 비용 경쟁력 확보까지는 4년이 더 소요될 전망입니다. 그 사이 OEM 업체들은 셀 단위 모니터링, 블루투스 진단, 지오펜싱 기반 차량 잠금 기능 등 잔존 가치를 높여 차량 재판매 시 이점을 제공하는 스마트 배터리 관리 시스템으로 초점을 전환하고 있습니다.

허브 모터는 여전히 55.72%의 점유율을 유지하고 있지만, 미드 드라이브 유닛은 2031년까지 연평균 복합 성장률(CAGR)5.05%로 시장 평균을 웃도는 성장이 예상됩니다. 자전거 기어와의 통합에 의한 토크 증폭 효과는 리스본과 리옹에 많은 경사로에서 매우 유용합니다. 보쉬의 「Performance Line CX Cargo」모터는 85Nm을 발생해, 라이더에 부담을 주지 않고 200kg의 적재물을 경사지에서 발진시킬 수 있습니다.

높은 유지보수 복잡성은 과거 구매를 주저하게 했으나, 서비스 네트워크 확대와 예측 진단 앱으로 가동 중단 시간이 줄어들었습니다. 일부 플릿 운영사는 현재 허브와 미드드라이브의 총소유비용(TCO)을 2년차 이후 거의 동등한 수준으로 평가하며, 유틸리티 집약적 노선에서는 후자로 사양 구성을 전환하고 있습니다.

The Europe e-cargo bike market size in 2026 is estimated at USD 1.21 billion, growing from 2025 value of USD 1.16 billion with 2031 projections showing USD 1.46 billion, growing at 3.85% CAGR over 2026-2031.

This outlook captures a maturing demand curve in which supportive regulation, falling lithium-ion battery costs, and urban logistics restructuring continue to nudge adoption forward without the explosive jumps seen in earlier years. City-level zero-emission delivery zones, generous commercial fleet subsidies, and dense micro-fulfillment networks collectively reinforce the business case, while the rapid drop in battery USD/kWh has erased a key cost barrier. Competitive intensity remains moderate: established bicycle brands leverage vertical integration and service networks, yet digital-first entrants add pricing pressure as procurement shifts online. Meanwhile, segment dynamics reveal that pedal-assisted drivetrains, lithium-ion batteries, mid-drive motors, and mid-premium price points define the mainstream commercial specification across Western European hubs.

European municipalities are steadily enlarging zero-emission delivery zones, forcing logistics operators to reassess vehicle economics. Amsterdam's ban on fossil-fuel vans inside the city core from 2025 has already triggered forward purchases of e-cargo bikes. London's Ultra Low Emission Zone exposes diesel vans to daily fees that can surpass a threshold that tilts total cost of ownership decisively toward electrically assisted cargo cycles. Regulatory convergence across Germany, France, and the Netherlands compounds these cost signals, prompting pan-European fleets such as Amazon Logistics to standardize on micromobility depots in Berlin, Paris, and Milan. As more cities publish phase-out timelines for internal-combustion vans, operators view the Europe e-cargo bike market as a compliance hedge that preserves route flexibility across jurisdictions.

National and municipal incentive programs now target business buyers rather than consumers. Germany's BAFA scheme reimburses up to 25% of acquisition cost and can be stacked with local grants that raise subsidy coverage. France's EUR 55 million (~USD 64 million) bicycle investment fund extends grants to commercial e-cargo fleets . The Netherlands adds significant cargo bike plus tax deductions for small enterprises. These incentives compress payback periods for high-utilization services, explaining why corporate buyers dominate order books in Western Europe.

Most European cities lack purpose-built curbside chargers for commercial e-cargo cycles. Fleet operators therefore tether operations to depots, incurring real-estate and downtime costs when 800 Wh batteries require up to six hours for a full cycle on 4 A chargers. The absence of open standards forces mixed fleets to install proprietary docks from multiple vendors, straining capital budgets. Southern European hubs-Madrid, Rome, Athens-show the largest gaps because shared micromobility policies focus on scooters rather than commercial cargo bikes. Until city councils mandate curbside charging in loading bays, scaling above pilot fleets remains arduous for courier start-ups eyeing the Europe e-cargo bike market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Pedal-assisted drivetrains held 92.58% of the Europe e-cargo bike market share in 2025, reflecting their classification as bicycles under EU Regulation 168/2013, which exempts them from motor-vehicle insurance and licensing. The comfort of regulatory certainty keeps corporate buyers entrenched in this category for mainstream parcel delivery, where average loads hover near 120 kg. The Europe e-cargo bike market size for pedal assist is set to grow steadily as large couriers standardize fleets to minimize training and compliance overhead.

Throttle-assisted alternatives will, however, clock a 4.35% CAGR because heavy grocery, furniture, and municipal waste applications require continuous power unaffected by rider stamina. As Germany, France, and Italy align power-class definitions up to 25 km/h, fleet managers can integrate throttle-assisted units without increasing liability insurance lines. Manufacturers accordingly release dual-mode controllers that let operators toggle between compliance classes, future-proofing assets against evolving city statutes.

Lithium-ion technology captured 89.65% share of the Europe e-cargo bike market size in 2025 and continues rising at a 4.02% CAGR as kilowatt-hour costs freefall. Pack lifespans now reach significant full cycles, aligning with corporate fleet replacement timelines. LFP chemistry absorbs most volume due to intrinsic thermal stability and a notable cycle durability, a critical trait for high-turnover courier missions.

Lead-acid persists only in entry-level consumer cargo bikes where purchase price trumps total cost of ownership. Solid-state prototypes attract headlines but remain four years from commercial costing parity. In the interim, OEM focus shifts to smart battery management systems with cell-level monitoring, Bluetooth diagnostics, and geofenced immobilization-capabilities that enhance residual value at fleet resale.

Hub motors still hold 55.72% share yet mid-drive units will grow above the market at 5.05% CAGR through 2031. The torque multiplication afforded by integrating with bicycle gearing proves invaluable on gradients common in Lisbon or Lyon. Bosch's Performance Line CX Cargo motor delivers 85 Nm, enabling 200 kg payload starts on inclines without rider strain .

Higher maintenance complexity once deterred buyers, but expanding service networks and predictive diagnostic apps reduce downtime. Some fleet operators now benchmark hub versus mid-drive total cost of ownership at near parity after year two, tipping the specification mix toward the latter for utility-intensive routes.

The Europe E-Cargo Bike Market Report is Segmented by Propulsion Type (Pedal Assisted, Throttle Assisted), Battery Type (Lead Acid Battery, Lithium-Ion Battery, and More), Motor Placement (Hub (Front/Rear), Mid-Drive), Drive Systems (Chain Drive, Belt Drive), Motor Power (Below 250W, 251-350W, and More), Price Band, Sales Channel, End Use, and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).