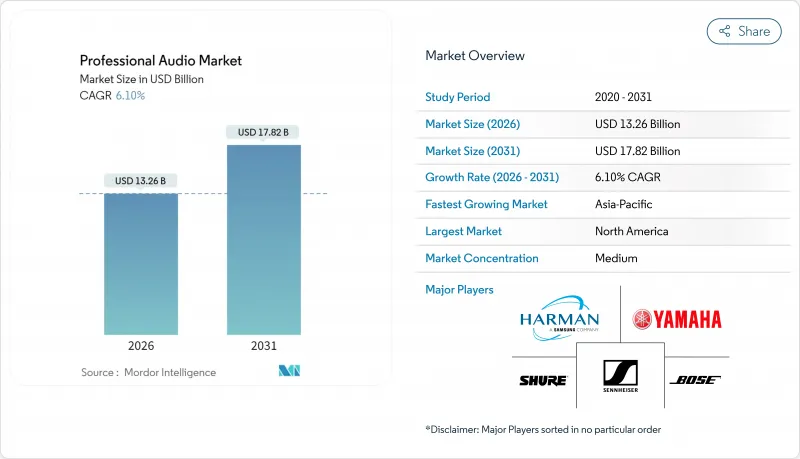

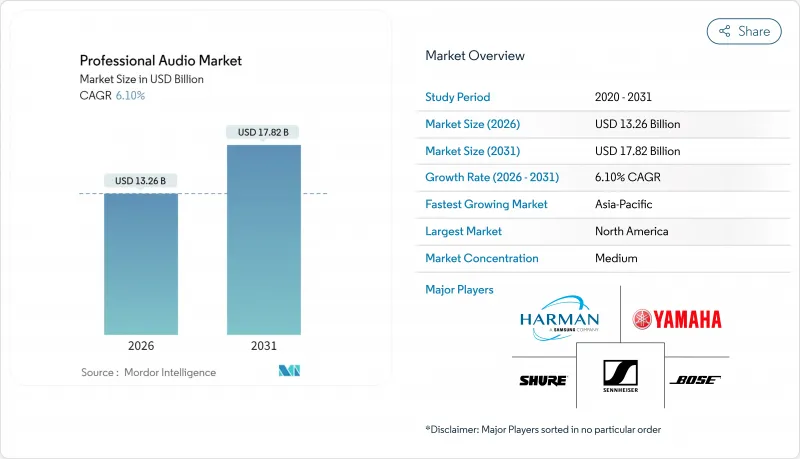

프로페셔널 오디오 시장은 2025년 125억 달러로 평가되었고, 2026년 132억 6,000만 달러에서 2031년까지 178억 2,000만 달러에 이를 것으로 보입니다. 예측기간(2026-2031년)의 CAGR은 6.1%로 전망됩니다.

장비 소유에서 경험 중심 솔루션으로의 수요 전환, 라이브 이벤트 부활, 기업 하이브리드 근무 환경 업그레이드가 핵심 성장 동력을 형성합니다. AES67 및 Dante와 같은 네트워크 프로토콜은 상호운용성 장벽을 낮춰 시설의 레거시 인프라 교체를 촉진합니다.

반도체 의존도를 최소화하는 공급망 재설계와 소프트웨어 정의 기능으로의 전환은 반복 수익 흐름을 강화합니다. 한편, Acuity Brands의 QSC 인수로 입증된 건물 시스템과 오디오의 융합은 조명, HVAC, 음향 플랫폼이 상호 연결되는 새로운 경쟁 구도를 예고합니다.

2024년 주요 콘서트 티켓 판매량은 전년 대비 26% 증가했으며, 이로 인해 렌탈 업체와 공연장은 노후화된 어레이를 더 엄격한 소음 규제 기준을 충족하면서도 강력한 음향을 유지하는 카디오이드 서브 어레이 시스템으로 교체하고 있습니다. 페스티벌 운영사들은 2025 울트라 뮤직 페스티벌에서 볼 수 있듯이, 체험형 마케팅을 스폰서십 수익과 연계하는 프리미엄 사운드 존을 통해 수익을 창출하고 있습니다. 하이브리드 기업 쇼는 현장 관객과 가상 관객 간 저지연 브리징이 필요해 확장형 디지털 콘솔 판매를 촉진합니다. 스피어 엔터테인먼트의 167,000개 스피커 설치 사례는 몰입형 건축이 브랜드 참여도를 어떻게 높이는지 보여줍니다. 따라서 프로페셔널 오디오 시장은 유연한 라우드스피커 구성과 신속한 쇼 전환을 가능케 하는 고밀도 무선 채널에 대한 수요가 증가하고 있습니다.

2024년 중국 온라인 오디오 이용자 수는 7억 4,700만 명을 기록하며 688억 6천만 달러 규모의 시장을 형성했는데, 이는 개인 콘텐츠 제작자가 전문 장비 구매 결정에 미치는 영향력을 보여줍니다. 같은 해 세계의 팟캐스트 수익은 300억 달러를 돌파하며 마이크 제조사들이 편의성과 확장성을 결합한 USB-XLR 하이브리드 제품을 출시하도록 촉진했습니다. 시각적 브랜드 미학이 중요해짐에 따라 대형 방송용 마이크는 화면 내 신뢰도를 높여 실시간 음성 처리 기능을 통합한 셔어(Shure)의 MV7i 같은 제품의 채택률을 높였습니다. 중견 제조사들은 하드웨어와 소프트웨어 플러그인을 번들로 제공해 초보 구매자를 구독 고객으로 전환하며 이점을 활용하고 있습니다. 이러한 촉진요인은 기존 스튜디오를 넘어 최종 사용자 기반을 확장함으로써 프로페셔널 오디오 시장의 잠재적 규모를 확대합니다.

DSP 코어와 RF 트랜시버의 리드 타임이 60주를 초과하면서 설계 팀은 대체 부품 인증을 진행하거나 고급 기능을 제거해야 하는 상황에 직면했습니다. 관세 인상으로 착륙 비용이 상승한 가운데 2024년 미국 반도체 수입액은 1,390억 달러에 달했습니다. 중소 오디오 브랜드들은 대형 기술 기업들과 웨이퍼 할당을 놓고 경쟁하며 종종 프리미엄을 지불하거나 생산량을 축소해야 했습니다. 부품 노후화가 가속화되면서 일부 공급업체는 칩 수가 적은 아날로그 라인을 선호해 디지털 SKU 생산을 중단하고 있습니다. 따라서 프로페셔널 오디오 시장은 팹 생산 능력이 수요와 맞물릴 때까지 마진 압박에 직면할 전망입니다.

2025년의 프로페셔널 오디오 시장 규모의 38.02%를 라우드스피커가 38.02%를 차지하며, 투어링, 고정 설치, 하이브리드 공연장 전반에 걸친 핵심 위치를 확인했습니다. 팬데믹 기간의 가동 중단 이후 교체 주기가 가속화되었으며, 많은 공연장이 저주파 방향성을 개선하면서도 지방자치단체 소음 규정을 준수하는 카디오이드 서브 어레이를 도입했습니다. 한편 무선 마이크 시장은 아날로그 UHF 장비 사용 중단을 강제하는 규제적 주파수 재할당에 힘입어 연평균 7.45% 성장률을 기록 중입니다. 제조사들은 축소되는 주파수 대역 내에서 작동하며 혼잡한 RF 환경에서도 성능을 보장하는 암호화 디지털 플랫폼으로 대응하고 있습니다.

스피커 부문에서는FIR 기반 빔 스티어링으로 시스템 성능을 향상시키는 증폭, 리깅, 제어 소프트웨어에 대한 부가가치 수요를 주도합니다. 공급업체들은 예측 모듈을 활성화하는 소프트웨어 구독 서비스를 도입해 일회성 하드웨어 판매를 반복 수익으로 전환합니다. 마이크 제조사들은 WMAS 기반 생태계를 탐구 중인데, 예를 들어 젠하이저의 스펙테라(Spectera)는 단일 6MHz 블록 내에서 64채널을 제공하며, 고급 변조 기술이 스펙트럼 부족 문제를 어떻게 해결하는지 보여줍니다. Dante 브레이크아웃 박스나 PoE 전원 공급 스테이지 박스 같은 액세서리는 통합 간극을 메우며, 프로페셔널 오디오 시장 내 공급업체들의 지갑 점유율을 완성합니다.

유선 솔루션은 정부 회의실 및 방송 스튜디오 등 RF 위험을 견디는 미션 크리티컬 애플리케이션 덕분에 2025년 프로페셔널 오디오 시장 규모에서 56.85% 점유율을 유지했습니다. Cat6a 케이블과 중복 링 토폴로지는 거의 제로에 가까운 지연 시간을 보장하며 PoE++를 통한 전원 분배를 용이하게 합니다. 그러나 Wi-Fi 7이 6GHz 대역 채널을 개방하고 결정론적 스케줄링을 개선함에 따라 무선 장치 시장은 2031년까지 연평균 7.22% 성장할 것으로 전망됩니다. 초기 Dante-over-Wi-Fi 프로토타입은 5ms 미만의 지연 시간을 보여주며 이더넷과의 성능 격차를 좁히고 있습니다.

배터리 기술 혁신으로 휴대용 PA 박스의 중간 음압 수준(SPL) 작동 시간이 40시간으로 연장되어 야외 적용 사례가 확대되고 있습니다. 클라우드 데이터기반 기반의 주파수 조정 관리 앱은 배포를 간소화하여 자원봉사 운영자의 전문성 장벽을 낮춥니다. 위조 RF 모듈이 복잡성을 가중시키지만, 업계 단체의 교육 프로그램은 표준화된 스캐닝 프로토콜을 통해 간섭 완화에 기여합니다. 통합업체들이 유무선 생태계를 융합한 장애 복구 아키텍처를 설계함에 따라 유무선 시스템이 공존하며, 프로페셔널 오디오 시장이 신뢰성과 유연성 기대를 동시에 충족시킵니다.

북미는 2025년 프로페셔널 오디오 시장의 33.12%를 차지했으며, 이는 지속적인 기술 업데이트가 필요한 아레나, 대형 교회, 방송 시설이 세계에서 가장 밀집해 있기 때문입니다. FCC 스펙트럼 재할당은 무선 장비 교체를 촉진하는 반면, 접근성 법규는 공연장에 보조 청취 송신기 도입을 요구합니다. 기업 부동산 팀은 AES67 네트워크를 통해 실내 및 원격 음성을 통합하는 회의실 현대화를 최우선 과제로 삼고 있습니다. 캘리포니아와 일리노이의 지역 제조 클러스터는 세계의 공급망 차질 시 납기 단축을 통해 지역적 회복탄력성을 강화합니다.

아시아태평양은 가장 빠른 성장 속도를 기록하고 2031년까지 연평균 복합 성장률(CAGR) 7.22%로 확대합니다. 중국과 인도의 국립 경기장 계획은 설계 단계부터 Dante Native의 공공 방송 시스템을 통합합니다. 중국의 '귀 경제'는 소비자용 시설에 경쟁상의 차별화 요인으로 프리미엄 오디오의 채택을 의무화함으로써 조달 형태를 형성하고 있습니다. 인도의 통합업체는 조립 현지화를 촉진하는 정부의 우대 조치로 수입 부품의 관세 인하의 혜택을 받고 있습니다. 이 지역의 크리에이티브 레이어의 급증은 합리적인 가격의 스튜디오 인터페이스에 대한 수요를 자극하고 Gig Economy의 뮤지션과 포드 캐스터 레이어에서 프로페셔널 오디오 시장의 기반을 확대하고 있습니다. 환율 변동은 계획적 위험으로 남아 있지만, 제조업체는 가능한 한 계약을 달러로 설정하여 위험 회피를 도모합니다.

유럽은 문화 기관과 기업 캠퍼스 전반에 걸쳐 안정적인 수요를 보여줍니다. 유산 극장 리모델링은 EU 지속가능성 목표에 부합하도록 재활용 가능한 스피커 캐비닛과 저전력 앰프를 우선시합니다. 브렉시트는 이중 인증 비용을 유발하지만, 동시에 유럽 본토 유통업체들이 완충 재고를 보유하도록 동기부여하여 공급 연속성을 유지합니다. 프로라이트+사운드(Prolight + Sound) 같은 독일 무역 박람회는 제품 가시성을 높이는 반면, 영국 방송 부문은 ST 2110 호환 콘솔 채택을 가속화합니다. 따라서 유럽의 프로페셔널 오디오 시장은 대규모 생산 능력 증대보다는 규제 준수 및 친환경 설계를 통해 진화하고 있습니다.

The professional audio market was valued at USD 12.50 billion in 2025 and estimated to grow from USD 13.26 billion in 2026 to reach USD 17.82 billion by 2031, at a CAGR of 6.1% during the forecast period (2026-2031).

Demand shifts from equipment ownership to experience-driven solutions, live-event resurgence, and enterprise hybrid-work upgrades form the core growth pillars. Networked protocols such as AES67 and Dante reduce interoperability barriers, encouraging facilities to refresh legacy infrastructure.

Supply chain redesigns that minimize semiconductor exposure and a pivot toward software-defined features strengthen recurring revenue streams. Meanwhile, convergence of building systems with audio, evidenced by Acuity Brands' acquisition of QSC, signals new competitive dynamics where lighting, HVAC, and sound platforms interconnect.

Ticket volumes at major concerts increased 26% year over year in 2024, spurring rental firms and venues to replace aging arrays with cardioid sub-array systems that meet stricter noise ordinances while preserving punch. Festival operators monetize premium sound zones that tie experiential marketing to sponsorship revenue, as seen at Ultra Music Festival 2025. Hybrid corporate shows need low-latency bridging between onsite and virtual audiences, driving sales of scalable digital consoles. Sphere Entertainment's 167,000-speaker install illustrates how immersive architecture elevates brand engagement. The professional audio market therefore sees elevated demand for flexible loudspeaker configurations and high-density wireless channels that streamline quick show turnovers.

China logged 747 million online audio users in 2024, generating a sector worth USD 68.86 billion, underlining how individual content creators influence professional purchasing decisions. Global podcast revenue surpassed USD 30 billion the same year, pushing microphone makers to launch USB-XLR hybrids that combine convenience with expandability. Visual brand aesthetics matter; larger broadcast-style microphones improve on-camera credibility, boosting uptake of units such as Shure's MV7i that integrate real-time voice processing. Mid-tier manufacturers capitalize by bundling software plug-ins alongside hardware, converting first-time buyers into subscription clients. This driver enlarges the addressable professional audio market by expanding the end-user base beyond traditional studios.

Lead times for DSP cores and RF transceivers extend past 60 weeks, forcing design teams to qualify substitute parts or strip advanced features. U.S. semiconductor imports reached USD 139 billion in 2024 amid tariff hikes that raised landed costs. Smaller audio brands compete against large tech firms for wafer allocation, often paying premiums or shrinking production runs. Component obsolescence accelerates, leading some vendors to sunset digital SKUs in favor of analog lines requiring fewer chips. The professional audio market thus faces margin compression until fab capacity aligns with demand.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Loudspeakers contributed 38.02% of the professional audio market size in 2025, confirming their centrality across touring, fixed install, and hybrid venues. Replacement cycles accelerated after pandemic-era downtime, with many arenas adopting cardioid sub-arrays that improve low-frequency directionality while complying with municipal noise codes. Meanwhile, wireless microphones advance at an 7.45% CAGR on the back of regulatory spectrum reallocations that compel users to retire analog UHF units. Manufacturers answer with encrypted digital platforms that fit within shrinking frequency bands, safeguarding performance in congested RF environments.

The loudspeaker segment drives value-added demand for amplification, rigging, and control software that elevate system performance through FIR-based beam steering. Vendors unlock software subscriptions that activate prediction modules, converting one-time hardware sales into recurring revenue. Microphone makers explore WMAS-based ecosystems, such as Sennheiser's Spectera, which delivers 64 channels inside a single 6 MHz block and illustrates how advanced modulation counters spectrum scarcity. Accessories like Dante breakout boxes and PoE-powered stage boxes fill integration gaps, rounding out wallet share captured by vendors inside the professional audio market.

Wired solutions retained 56.85% share of the professional audio market size in 2025 thanks to mission-critical applications that resist RF risk, including government chambers and broadcast studios. Cat6a cable and redundant ring topologies guarantee near-zero latency and facilitate power distribution through PoE++. Yet wireless units are forecast to post a 7.22% CAGR to 2031 as Wi-Fi 7 unlocks 6 GHz channels and improves deterministic scheduling. Early Dante-over-Wi-Fi prototypes demonstrate sub-5 ms latency, narrowing the performance gap against Ethernet.

Battery innovation extends runtime to 40 hours at moderate SPL for portable PA boxes, widening addressable outdoor use cases. Managed-frequency coordination apps powered by cloud databases simplify deployment, lowering expertise barriers for volunteer operators. Despite counterfeit RF modules adding complexity, educational initiatives by industry bodies help mitigate interference through standardized scanning protocols. Wired and wireless ecosystems coexist as integrators design fail-over architectures that blend both, ensuring the professional audio market satisfies reliability and flexibility expectations simultaneously.

The Professional Audio Market Report is Segmented by Product (Loudspeakers, Power Amplifiers, Mixing Consoles, Microphones, Headphones, and More), Connectivity (Wired, Wireless), End-User (Corporate, Venues and Events, Retail and Hospitality, Media and Entertainment, and More), Application (Live Sound Reinforcement, Recording Studios, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America accounted for 33.12% of the professional audio market in 2025, backed by the world's densest concentration of arenas, megachurches, and broadcast facilities requiring rolling technology refreshes. FCC spectrum reallocation compels wireless replacements, while accessibility laws push venues to adopt assistive-listening transmitters. Corporate real-estate teams prioritize conference-room modernization that unifies in-room and remote voices via AES67 networks. Regional resilience is reinforced by local manufacturing clusters in California and Illinois that shorten lead times during global supply disruptions.

Asia-Pacific records the fastest pace, advancing at a 7.22% CAGR through 2031 as national stadium programs in China and India embed Dante-native public-address systems from blueprint stages. China's "ear economy" shapes procurement by requiring consumer-facing venues to adopt premium audio as a competitive differentiator. Indian integrators benefit from government incentives that localize assembly, lowering tariffs on imported components. The region's creative-class boom fuels demand for affordable studio interfaces, expanding the professional audio market base among gig-economy musicians and podcasters. Currency fluctuations remain a planning risk, yet manufacturers hedge by denominating contracts in USD where possible.

Europe demonstrates stable demand across cultural institutions and corporate campuses. Renovation of heritage theaters prioritizes recyclable loudspeaker cabinets and low-power amplifiers to align with EU sustainability targets. Brexit spurs dual-certification costs but also motivates continental distributors to hold buffer stock, maintaining supply continuity. German trade fairs like Prolight + Sound drive product visibility, while the United Kingdom broadcast sector accelerates adoption of ST 2110-compatible consoles. The professional audio market in Europe thus evolves through regulatory compliance and green design, rather than large-scale capacity increases.