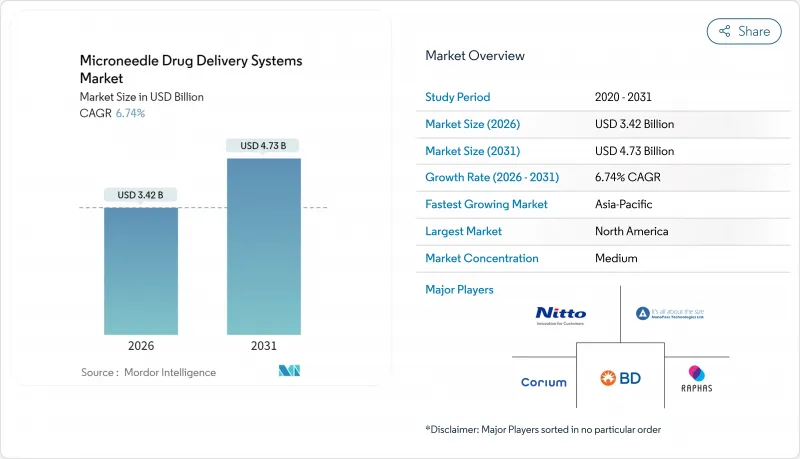

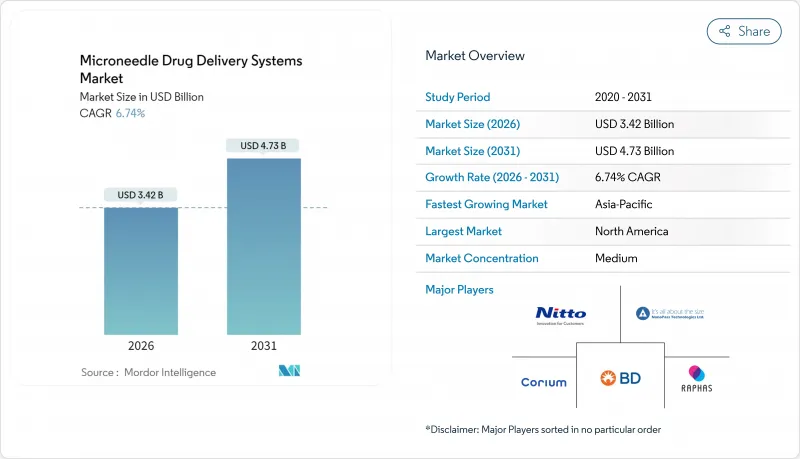

마이크로니들 약물 전달 시스템 시장은 2025년 32억 달러에서 2026년 34억 2,000만 달러로 성장하고 2026년부터 2031년에 걸쳐 CAGR 6.74%로 성장을 지속하여 2031년까지 47억 3,000만 달러에 달할 것으로 예측되고 있습니다.

이 확장은 콜드체인 물류를 필요로 하지 않는 내열성 백신 패치에 의해 추진되어 자원이 제한된 환경에서의 접근 확대로 이어집니다. 기타 성장 요인으로는 만성 질환의 유병률 증가, 복합 제품에 대한 규제의 명확화, 주요 장치 제조업체의 생산 능력 향상 등이 있습니다. 경쟁 우위는 확장 가능한 롤 투 롤 제조 기술, 정밀한 약물 충전 기술, 디지털 치료와의 통합에 점점 의존하고 있습니다. 한편, 패치당 약물 함량의 제한이나 환자 간 피부 미생물총의 차이 등의 기술적 위험은 나노입자 봉입 기술이나 실시간 용량 피드백 시스템에 의해 줄어들고 있습니다. 그 결과 마이크로니들 약물 전달 시스템 시장은 틈새 조사 단계에서 의약품 및 화장품 가치 체인 전반적인 주류 도입으로 이행하고 있습니다.

당뇨병이나 자가면역질환의 환자 수가 증가함에 따라 자가투여 가능한 무통요법의 필요성이 높아지고 있습니다. 무작위화 시험을 통해 마이크로니들에 의한 아달리무맙의 생물학적 이용능력이 피하 주사와 동등하고 국소 반응을 40% 감소시키는 것으로 나타났습니다. 의료 현장의 인력 부족 현상은 의료 종사자의 감독 없이 환자의 복약 준수를 유지하는 가정용 패치에 대한 수요를 더욱 높입니다. 이러한 인구동태와 업무 부하의 압력이라는 요인이 더해 마이크로니들 약물 전달 시스템 시장은 꾸준한 성장이 예상됩니다.

바늘 찔림 사고에 대한 우려 증가와 바늘 공포증은 기존의 피하 주사를 대체하는 안전한 대안 수요를 견인하고 있습니다. 2022년 10월에 발표된 연구조사에 의하면, 바늘 찔림이나 예리한 물체에 의한 부상의 전체적인 유병률은 25.2%로 추정되었으며 간호학생이 가장 높은 빈도로 경험하고 있습니다. 의료 종사자에게 있어 이러한 심각한 위험은 보다 안전한 약물 전달 수단의 긴급성을 초래합니다. 바늘 공포증도 현저하며 연구에 의하면 10대의 20-50%, 젊은 성인의 20-30%가 이 증상을 경험하고 있어 치료 회피나 약제 효과의 저하로 이어지고 있습니다.

대부분의 용해형 제제는 패치당 1-10mg의 약물만 함유할 수 있으며, 고용량의 생물학적 제제에는 제약이 있습니다. 다층 주조나 나노입자 봉입에 의해 용량은 향상되지만, 추가적인 검증 과제가 발생합니다. FDA의 2024년 초안 가이드라인에서는 일관된 약물 방출 프로파일에 대한 명확한 입증이 요구되며 개발 기간이 장기화될 수 있습니다.

용해형 제제는 날카로운 폐기물이 발생하지 않고 생분해됨으로 인해 2025년 마이크로니들 약물 전달 시스템 시장에서 점유율 33.12%를 유지했습니다. 한편, 하이드로겔형은 복잡한 투여 계획에 적합한 리저버식 약물 방출 특성에 의해 6.95%의 연평균 복합 성장률(CAGR)로 성장하고 있습니다. 고체 어레이는 피부 전처리 틈새 시장에서 계속 수요가 있으며, 중공 구조는 고비용 금형을 필요로 하는 대용량 투여를 가능하게 합니다. 포도당 센서와 연동하는 하이드로겔 시스템은 자동 인슐린 적정을 위한 후기 임상시험 단계에 있으며 파괴적 혁신의 가능성을 시사합니다.

신흥의 자동 코팅 라인과 공정 내 시각 검사에 의해 폐기율이 저하되어, 하이드로겔 유닛의 비용 격차 해소에 공헌하고 있습니다. FDA의 복합제품에 대한 지침이 성숙함에 따라 용해형 및 하이드로겔형의 규제상의 평준화가 기대되고, 마이크로니들 약물 전달 시스템 시장에 폭넓은 수익원이 열릴 전망입니다.

폴리머는 조정할 수 있는 기계적 특성과 확립된 성형 노하우로 2025년 마이크로니들 약물 전달 시스템 시장 규모의 29.55%를 차지했습니다. 탄수화물은 7.78%의 연평균 복합 성장률(CAGR)을 나타내며, 냉장 없이 백신의 효능을 유지하는 말토덱스트린 및 트레할로스 패치가 견인하고 있습니다. 실리콘은 단단한 고체 어레이에 필수적이며 금속은 특수 고강도 이용 사례에 사용됩니다. 규제 당국이 천연 유래 소재를 점점 권고하는 가운데, 탄수화물의 도입이 가속하고 있습니다.

제조 공정의 간편성과 저탄소 발자국은 특히 지속가능한 의료 솔루션을 요구하는 저소득 지역에서 탄수화물 어레이의 경제적 이점을 강화하고 있습니다. 이러한 변화는 마이크로니들 약물 전달 시스템 시장의 재료 구성을 다양화하는 기반이 되었습니다.

북미에서는 성숙한 지불자 구성과 조기 도입을 시도하는 임상의가 함께 차세대 패치의 프리미엄 가격 설정력을 확고히 하고 있습니다. 5,000만 달러 규모의 '패치 포워드' 프로그램 등 정부 보조금이 임상 응용을 가속시키는 한편, 민간 자본은 보스턴과 베이 지역에 집중하는 스타트업 활동을 뒷받침하고 있습니다.

아시아태평양의 높은 CAGR은 대규모 예방 접종 활동과 만성 질환의 사례 수로 인해 뒷받침됩니다. 중국과 인도공급망의 현지화 정책은 다국적 기업들에게 롤 투 롤 생산 라인의 지역 배치를 촉구하여 리드 타임 단축과 인건비 절감을 실현하고 있습니다. ASEAN의 조화된 의료기기 규정은 아직 개선의 여지가 있지만 중복시험 비용 절감이 예상되며 수출업체의 IFRS 위험을 줄일 것으로 기대됩니다.

유럽에서는 GAVI와 같은 기관을 통한 협력 조달 채널이 CE 마크 승인 취득 후의 대량 구매를 촉진합니다. 독일의 포장법(VerpackG)을 포함한 지속가능성 규제는 사용 후 폐기물을 줄이는 용해성 및 탄수화물 어레이를 뒷받침합니다. 라틴아메리카와 아프리카의 신흥 시장에서는 WHO의 감독하에 내열성 홍역 및 폴리오 패치의 시험 도입이 진행되어, 양산 확대가 기대됩니다.

The microneedle drug delivery systems market is expected to grow from USD 3.20 billion in 2025 to USD 3.42 billion in 2026 and is forecast to reach USD 4.73 billion by 2031 at 6.74% CAGR over 2026-2031.

The expansion is propelled by thermostable vaccine patches that bypass cold-chain logistics, widening access in low-resource settings. Other growth catalysts include rising chronic-disease prevalence, regulatory clarity around combination products, and capacity additions by leading device manufacturers. Competitive advantage increasingly hinges on scalable roll-to-roll fabrication, precision drug-loading technologies, and integration with digital therapeutics. Meanwhile, technology risks-such as limited payload per patch and inter-patient skin-microflora variability-are being mitigated through nanoparticle encapsulation and real-time dose-feedback systems. As a result, the microneedle drug delivery systems market is transitioning from niche research to mainstream adoption across pharmaceutical and cosmetic value chains.

Growing diabetes and autoimmune caseloads amplify the need for self-deliverable, pain-free therapies. A randomized trial showed adalimumab bioavailability via microneedle delivery matching subcutaneous injection while cutting local reactions by 40%. Health-system labor shortages further elevate demand for home-use patches that keep patients adherent without clinician oversight. This confluence of demographics and workload pressure assures steady support for the microneedle drug delivery systems market.

The growing concern over needlestick injuries and the prevalence of needle phobia are driving the demand for safer alternatives to conventional hypodermic injections. According to a research study published in October 2022, the overall prevalence rate of injuries from needlesticks and sharp objects was determined to be 25.2%, with nursing students experiencing the highest frequency. This significant risk to healthcare workers has created an urgent need for safer drug delivery alternatives. The prevalence of needle phobia is also substantial, with studies showing that 20-50% of teenagers and 20-30% of young adults experience this condition, leading to treatment avoidance and reduced medication effectiveness.

Most dissolving formats hold 1-10 mg per patch, constraining high-dose biologics. Multilayer casting and nanoparticle encapsulation can raise capacity but introduce extra validation hurdles. The FDA's 2024 draft guidance now requires explicit demonstration of consistent drug-release profiles, stretching development timelines.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Dissolving formats retained 33.12% microneedle drug delivery systems market share in 2025 due to sharps-waste elimination and biodegradability. Hydrogel-forming types, however, are pacing at a 6.95% CAGR given their reservoir-style drug release that suits complex regimens. Solid arrays continue serving skin-pretreatment niches, while hollow configurations enable larger-volume delivery despite costlier tooling. Hydrogel systems linked with glucose sensors are in late-stage trials for automated insulin titration, signaling disruptive potential.

Emerging automated coating lines and in-process vision inspection lower scrap rates, helping hydrogel units close the cost gap. As FDA guidance on combination products matures, regulatory parity between dissolving and hydrogel types is expected, opening broader revenue streams for the microneedle drug delivery systems market.

Polymers contributed 29.55% of microneedle drug delivery systems market size in 2025 due to tunable mechanics and established molding know-how. Carbohydrates are charting an 7.78% CAGR, driven by maltodextrin and trehalose patches that keep vaccines potent without refrigeration. Silicon remains critical for rigid solid arrays, whereas metals serve specialty high-strength use cases. Regulators increasingly favor naturally derived substrates, accelerating carbohydrate adoption.

Process simplicity and lower carbon footprints strengthen the economic case for carbohydrate arrays, especially in lower-income regions striving for sustainable healthcare solutions. This shift underpins diversification within the microneedle drug delivery systems market material landscape.

The Microneedle Drug Delivery Systems Market Report is Segmented by Device Type (Solid, Hollow, Coated, Dissolving, Hydrogel-Forming), Material (Silicon, Metals, Polymers, Carbohydrates, Others), Application (Vaccination, Insulin Delivery, and More), End-User (Hospitals & Clinics, Pharmaceutical & Biotech Companies, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America's mature payor mix, coupled with early adopter clinicians, cements premium pricing power for next-gen patches. Government grants, such as the USD 50 million Patch Forward program, accelerate clinical translation, while private capital fuels start-up activity concentrated in Boston and the Bay Area.

Asia-Pacific's superior CAGR arises from large-scale immunization drives and chronic-disease caseloads. Supply-chain localization policies in China and India are prompting multinationals to site roll-to-roll lines regionally, tightening lead times and lowering labor costs. Harmonized ASEAN device rules, though nascent, are expected to trim duplicate testing expenses, lowering IFRS risk for exporters.

Europe's coordinated procurement channels through entities like GAVI spur volume buys once CE-mark approval lands. Sustainability regulations, including Germany's VerpackG, favor dissolving and carbohydrate arrays that shrink post-use waste. Emerging markets across Latin America and Africa are piloting thermostable measles and polio patches under WHO oversight, heralding future volume growth.