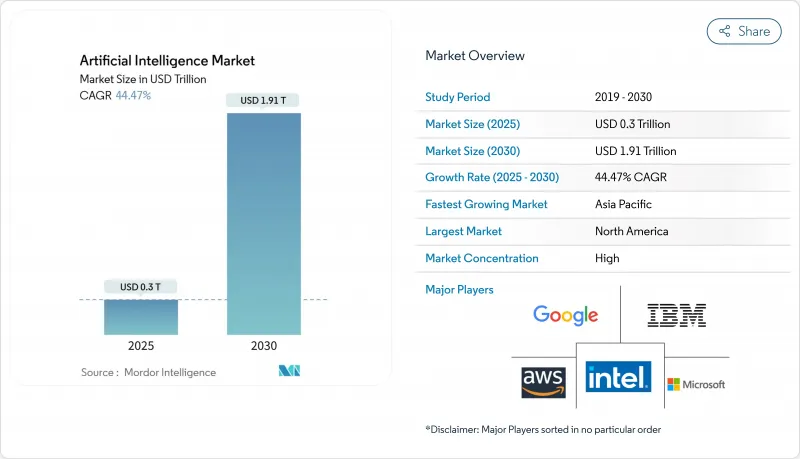

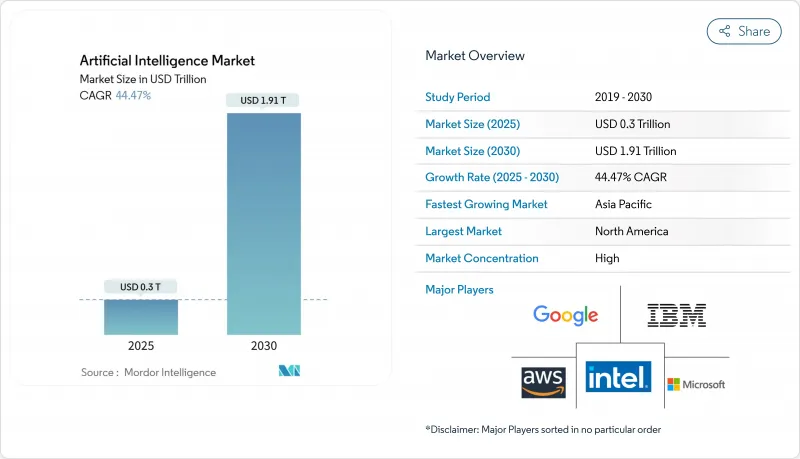

인공지능 시장은 2025년 3,060억 4,000만 달러에서 2026년 4,344억 2,000만 달러로 성장하고 2026년부터 2031년에 걸쳐 CAGR 41.95%로 성장을 지속하여 2031년까지 2조 5,031억 3000만 달러를 달성할 전망입니다.

주권 AI 프로그램과 기업의 비용 최적화 및 급속한 하드웨어 혁신을 통해 이 기술은 실험적인 파일럿 단계에서 핵심 생산 워크플로로 전환하고 있으며, 모든 주요 부문에서 지속적인 수요를 촉진하고 있습니다. 대기업은 총 소유 비용과 데이터 거버넌스를 직접 관리하기 원하므로 온프레미스 도입이 다시 주목을 받고 있습니다. 동시에 클라우드 하이퍼스케일러는 새로운 용량에 많은 투자를 하고 있으며 개발 환경에 쉽게 접근할 수 있습니다. GPU의 발전, 에너지 효율적인 아키텍처, 하드웨어와 소프트웨어 스택 간의 긴밀한 통합으로 가치 실현까지의 시간이 단축되고 경쟁 차별화가 선명해지고 있습니다.

정부 자금이 지역 생태계를 형성하고 있습니다. 인도의 'IndiaAI Mission'은 현지 언어 요구를 충족하는 국산 대규모 언어 모델에 10,372캐롤 루피(1억 2,450만 달러)를 투입하고 있습니다. 일본은 AI와 반도체 능력에 10조엔을 동원해, 자립에 대한 장기적인 헌신을 나타내고 있습니다. 이러한 투자는 현지화 규정을 준수할 수 있는 국내 하드웨어 공급업체와 시스템 통합사업자에 대한 보장된 수요를 생성합니다.

산업용 IoT의 도입으로 매일 테라바이트 규모의 센서 데이터가 생성되고 기업은 AI 구동형 분석의 도입을 요구받고 있습니다. Siemens는 재무 업무에 머신러닝을 도입한 결과 송장 처리의 90%를 비접촉화함과 동시에 연간 565만 달러의 ROI를 달성했다고 보고하고 있습니다. 의료 영상, 자율주행차, 실시간 소매 거래도 데이터 홍수에 박차를 가해 확장 가능한 스토리지, 엣지 처리, 합성 데이터 생성 툴에 대한 수요를 높이고 있습니다.

NVIDIA는 2026년도 전망에서 H100의 지속적인 공급 부족을 지적했습니다. 이 제약에 의해 스팟 가격은 제조업체 희망 소매 가격(MSRP)을 30-50% 웃돌아 기업의 도입 사이클이 지연되고 있습니다. 전력 회사는 데이터센터의 전력 수요가 2026년까지 1,050TW(TWh)에 도달할 수 있을 것으로 예측하고 있으며, 이는 여러 주요 지역에서 계획된 증설 설계를 초과하는 규모입니다. 이로 인해 새로운 AI 클러스터 프로젝트 일정에 압력이 가해집니다.

소프트웨어는 2025년에 61.35%의 수익 점유율을 유지하여 인공지능 시장에서의 기반 역할을 강화했습니다. 그러나 기업이 실험 단계에서 본격적인 도입으로 중점을 옮기는 가운데 서비스 분야는 2031년까지 연평균 복합 성장률(CAGR) 40.85%로 급성장할 것으로 예측되고 있습니다. 대부분의 규제 산업에서는 단순한 라이선스가 아닌 컴플라이언스 요구사항을 해석하고 워크플로를 재설계할 수 있는 공급업체가 필요합니다. 따라서, 특히 의료 및 금융 서비스 분야의 도메인 특화형 프로젝트에 있어서, 유자격 인테그레이터의 부족이 서비스 제공업체의 고가격 설정을 가능하게 하고 있습니다.

컨설팅, 통합 및 매니지드 서비스 각 분야에서 수직 전문성을 가진 공급업체가 우선적으로 선택됩니다. 방사선 의학 분야에서는 데이터 거버넌스, 알고리즘 검증, 임상의 워크플로 재설계를 결합한 서비스 제휴를 통해 병원 그룹은 5년간 451%의 ROI를 달성했습니다. 하드웨어, 소프트웨어 및 권고 지원을 성과 기반 계약으로 패키징하는 전문 기업은 고객이 추상 모델 정밀도가 아닌 구체적인 생산성 목표로 프로젝트를 평가하는 가운데 밸류체인의 업스트림으로 전환하고 있습니다.

2025년 인공지능 시장 점유율의 43.72%를 차지하는 퍼블릭 클라우드는 기본 개발 환경으로서의 역할을 반영합니다. 그러나 조직이 생산 환경에서 대기 시간 최적화와 비용 가시성을 요구하는 가운데 하이브리드 모델은 2031년까지 연평균 복합 성장률(CAGR) 45.55%로 확대될 것으로 예측됩니다. 조기 도입 기업은 하이퍼스케일 클러스터에서 교육을 실시하고 실시간 응답을 위해 추론을 온프레미스 또는 엣지 장치로 푸시합니다. 자동차 제조업체는 이 아키텍처를 공장 현장에서 밀리초 수준의 비전 작업을 수행하면서 모델 재교육을 위한 클라우드의 신축성을 유지함으로써 입증하고 있습니다.

엣지 전개는 대역폭이 고액인 해양 시추장치나 소매매장 등 자원 제약이 있는 환경에서도 마찬가지로 중요합니다. 데이터 거주에 대한 엄격한 규제에 직면하는 금융 산업 및 공공 기관에서는 온프레미스 도입이 다시 증가하는 경향이 있습니다. 하드웨어 공급업체는 현재 정책에 따라 컨테이너를 클라우드, 온프레미스 랙 및 엣지 디바이스 간에 마이그레이션하는 오케스트레이션 소프트웨어를 번들로 제공하여 하이브리드 솔루션을 위한 인공지능 시장 규모가 상승세를 유지하고 있습니다.

본 AI 시장 보고서에서는 업계를 컴포넌트별(하드웨어, 소프트웨어, 서비스), 도입 형태별(퍼블릭 클라우드, 온프레미스, 하이브리드), 기술별(머신러닝, 심층 학습, 자연어 처리, 컴퓨터 비전, 생성형 AI, 상황 인식 컴퓨팅 등), 최종 사용자 산업(은행, 금융서비스 및 보험(BFSI), IT 및 통신, 의료 및 생명과학, 제조 등), 지역별로 구분하고 있습니다.

북미는 풍부한 벤처캐피탈, 성숙한 클라우드 에코시스템, 기업의 급속한 도입으로 2025년에도 37.12%의 점유율로 최대 실적을 유지했습니다. CHIPS 및 Science Act와 같은 연방 프로그램은 AI 대응 팹에 추가 자금을 투입하여 국내 하드웨어 공급을 지원하고 인공지능 시장을 강화하고 있습니다. 버지니아, 텍사스 및 오레곤의 고성능 컴퓨팅 클러스터는 저지연을 실현하기 위해 클라우드 사용 가능 영역 근처에 본사를 둔 소프트웨어 스타트업을 계속 모집하고 있습니다.

유럽의 성장 특성은 엄격한 데이터 프라이버시 규정과 대규모 정부 컴퓨팅 예산의 두 가지 요인으로 형성됩니다. GDPR(EU 개인정보보호규정) 호환 아키텍처는 공급업체에게 추론 워크로드를 지역 내로 지역화하도록 촉구하여 온프레미스 GPU 어플라이언스에 대한 수요를 창출하고 있습니다. 프랑스의 정부-민간 공동 프로젝트 'Mistral AI'는 2025년에 20억 유로의 평가액을 획득했으며 다국어 모델 트레이닝 확대를 위한 10억 달러의 자금 조달을 목표로 하고 있습니다. 독일과 북유럽 국가에서 유사한 프로그램은 야심찬 탄소 저감 목표와 부합하는 녹색 데이터센터의 설치에 초점을 맞추고 있으며, 인공지능 시장에서 두 자릿수의 지역 성장을 지속하고 있습니다.

아시아태평양은 2031년까지 연평균 복합 성장률(CAGR) 40.75%를 기록할 전망이며 세계에서 가장 빠른 성장이 예상됩니다. 중국의 국가 반도체 미션은 2030년까지 칩 및 관련 인프라에 1조 위안화를 배분하고 인도는 국가 AI 컴퓨팅에 1037억 2천만 루피를 할당해 국내 인테그레이터를 세계 시장으로 밀어 올리고 있습니다. 일본의 수조 엔 규모의 기금은 팹(반도체 제조 공장)의 업그레이드를 가속화하고 완만한 AI 규제가 상업화까지의 시간을 단축합니다. 싱가포르와 말레이시아를 포함한 동남아시아 국가들은 하이퍼스케일러를 지역 허브에 유치하는 데이터센터 세제 우대조치를 도입하고 있어 이 지역의 인공지능 시장의 규모는 더욱 확대될 전망입니다.

The artificial intelligence market is expected to grow from USD 306.04 billion in 2025 to USD 434.42 billion in 2026 and is forecast to reach USD 2,503.13 billion by 2031 at 41.95% CAGR over 2026-2031.

Sovereign AI programs, enterprise cost-optimization, and rapid hardware innovation are moving the technology from experimental pilots into core production workflows, fuelling sustained demand across every major sector. On-premise deployments are regaining traction because large organisations want direct control over total cost of ownership and data governance. At the same time, cloud hyperscalers are investing heavily in new capacity, ensuring that development environments remain easily accessible. GPU advances, energy-efficient architectures, and tighter integration between hardware and software stacks are shortening time to value and sharpening competitive differentiation.

Government funding is shaping local ecosystems. India's IndiaAI Mission is channeling INR 10,372 crore (USD 124.5 million) into indigenous large language models that meet local language needs. Japan is mobilising JPY 10 trillion for AI and semiconductor capacity, signalling a long-term commitment to self-reliance. Such investments create protected demand for domestic hardware vendors and systems integrators that can comply with localisation rules.

Industrial IoT rollouts generate terabytes of sensor data daily, pushing enterprises to adopt AI-driven analytics. Siemens reports 90% touchless invoice processing and USD 5.65 million annual ROI after embedding machine learning into its finance operations. Healthcare imaging, autonomous vehicles, and real-time retail transactions all add to the data deluge, driving up demand for scalable storage, edge processing, and synthetic data generation tools.

NVIDIA cited persistent H100 shortages in its FY 2026 outlook, a constraint that has inflated spot prices 30-50% above MSRP and slowed enterprise deployment cycles. Power utilities forecast that data-center electricity demand could hit 1,050 TWh by 2026, exceeding planned capacity additions in several major regions, which in turn pressures project timelines for new AI clusters.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Software retained 61.35% revenue share in 2025, reinforcing its foundational role in the artificial intelligence market. Yet the Services segment is forecast to race ahead at 40.85% CAGR through 2031 as enterprises shift focus from experimentation to full-scale implementation. Many regulated industries now require vendors that can interpret compliance mandates and redesign workflows, rather than merely deliver licenses. The scarcity of qualified integrators, therefore, enables service providers to command premium pricing, especially for domain-specific projects in healthcare and financial services.

Across consulting, integration, and managed-services lines, vendors with vertical expertise are preferred. In radiology, service partnerships that combine data-governance, algorithm validation, and clinician workflow redesign are returning 451% ROI for hospital groups over five years. Specialists that package hardware, software, and advisory support into outcome-based contracts are moving up the value chain as customers measure projects against concrete productivity targets rather than abstract model accuracy.

Public Cloud held 43.72% of artificial intelligence market share in 2025, reflecting its role as the default development environment. Hybrid models, however, are projected to compound at 45.55% CAGR to 2031 as organizations seek latency optimization and cost visibility in production. Early adopters run training on hyperscale clusters then push inferencing to on-prem or edge devices for real-time response. Automotive OEMs validate this architecture by executing millisecond-level vision tasks on factory floors while retaining cloud elasticity for model retraining.

Edge rollouts are equally important in resource-constrained settings such as offshore rigs or retail outlets where bandwidth is expensive. On-prem deployments are resurging within finance and public-sector agencies that face strict data-residency mandates. Hardware suppliers now bundle orchestration software that migrates containers across clouds, on-prem racks, and edge devices based on policy rules, ensuring the artificial intelligence market size for hybrid solutions remains on an upward trajectory.

The AI Market Report Segments the Industry Into by Component (Hardware, Software, and Services), Deployment Mode (Public Cloud, On-Premise, and Hybrid), Technology (Machine Learning, Deep Learning, Natural Language Processing, Computer Vision, Generative AI, and Context-Aware Computing and Others), End-User Industry (BFSI, IT and Telecommunications, Healthcare and Life Sciences, Manufacturing, and More), and Geography.

North America remained the revenue leader with 37.12% share in 2025 thanks to deep venture capital pools, mature cloud ecosystems, and rapid enterprise adoption. Federal programs such as the CHIPS and Science Act funnel additional funding into AI-ready fabs, supporting domestic hardware supply and reinforcing the artificial intelligence market. High-performance computing clusters in Virginia, Texas, and Oregon continue to attract software start-ups that co-locate near cloud availability zones for lower latency.

Europe's growth profile is shaped by the twin forces of strict data-privacy regulation and sizable sovereign compute budgets. GDPR compliant architectures push vendors to localize inference workloads inside regional borders, creating demand for on-prem GPU appliances. France's public-private initiative around Mistral AI gained a €2 billion valuation in 2025 and aims to raise USD 1 billion to scale multilingual model training. Similar programs in Germany and the Nordics focus on green-data-center footprints that align with ambitious carbon-reduction targets, sustaining double-digit regional growth for the artificial intelligence market.

Asia-Pacific is projected to register a 40.75% CAGR through 2031, the fastest worldwide. China's National Semiconductor Mission allocates RMB 1 trillion by 2030 for chips and supporting infrastructure, while India earmarks INR10,372 crore for national AI compute, propelling domestic integrators into global rankings. Japan's multi-trillion-yen fund fast-tracks fab upgrades and light-touch AI regulation that accelerates time to commercial deployment. Southeast Asian economies, including Singapore and Malaysia, are introducing data-center tax incentives that entice hyperscalers to anchor regional hubs, further enlarging the artificial intelligence market size in the region.