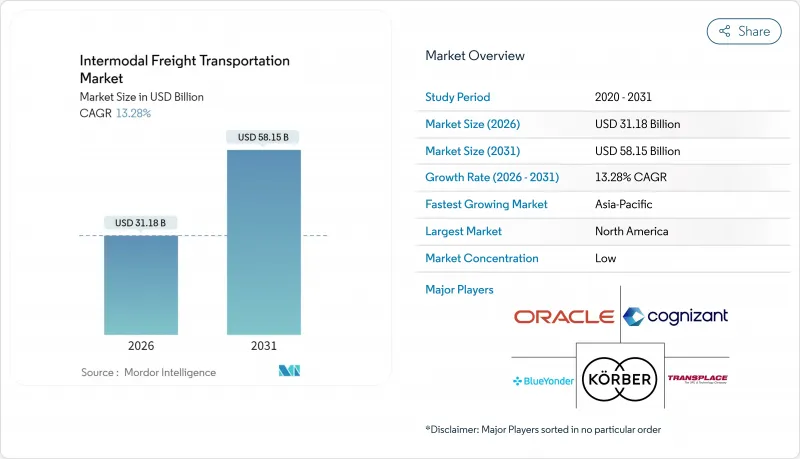

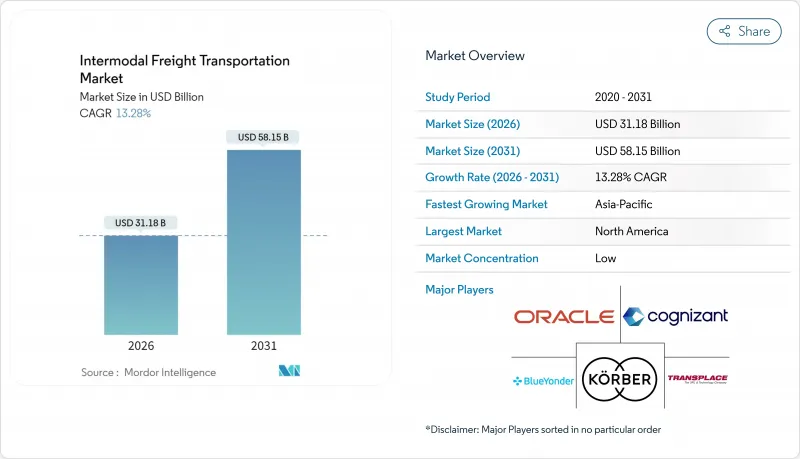

2026년 인터모달 화물 운송 시장 규모는 311억 8,000만 달러로 추정되며, 2025년 275억 2,000만 달러에서 성장하여, 2031년에는 581억 5,000만 달러에 이를 것으로 예측됩니다.

2026-2031년에 걸친 연평균 복합 성장률(CAGR)은 13.28%를 나타낼 전망입니다.

전자상거래량 증가, 공급체인의 디지털화 가속, 시책주도의 탈탄소화 목표가 함께 운송수단의 선택을 재구성하고 통합물류 솔루션에 대한 수요를 촉진하고 있습니다. 라레도와 몬테레이를 연결하는 100억 달러 규모의 자동화 철도 회랑과 일대일로 사업을 포함한 인프라에 대한 공공 지출과 대규모 철도 투자는 잠재력을 드러내면서 대륙 간 무역 흐름을 재편하기 시작했습니다. 기술 도입으로 실시간 가시성이 확대되고 체류시간이 단축되어 자산 가동률이 향상되는 한편 지속가능성 요구가 철도 및 도로와 해상 및 철도 조합의 경제적 합리성을 강화하고 있습니다. 경쟁 차별화는 순수한 자산 규모에서 단일 멀티모달 플랫폼 내의 소프트웨어, 분석 및 인증된 저탄소 서비스를 통합적으로 운영하는 능력으로 전환하고 있습니다.

클라우드 기반 물류 플랫폼의 보급으로 운송업체, 터미널 및 화주가 통합된 데이터 생태계로 연결되어 연간 수십억 건의 거래를 처리하고 있습니다. 예측 분석에 의해 체류 시간이 두 자릿수 단축되어, 철도, 도로 및 해상 구간 전체에서의 자산 가동률 향상을 뒷받침하는 동적 라우팅이 실현되고 있습니다. IoT가 장착된 스마트 컨테이너는 온도, 습도, 위치 데이터를 전송하여 화물의 무결성을 강화하고 보험 비용을 절감합니다. 블록체인 대응 기록은 변조가 불가능한 납품 증명을 제공하고 운송 모드 간의 기존 분쟁을 해결합니다. 반면에 API가 풍부한 아키텍처는 기존 EDI 표준과의 통합을 용이하게 합니다. 이러한 디지털 기반이 결합되어 인터모달 화물 운송 시장은 대규모로 준실시간 경로 변경이 가능한 데이터 구동 네트워크로 변모하고 있습니다.

B2C 소포 수요는 총 상품 무역량을 웃도는 속도로 성장을 계속하고 있으며, 화주는 속도와 비용의 균형을 맞추는 허브 앤 스포크형 인터모달 솔루션으로 포인트 투 포인트 풀 트랙 운송으로부터 이행하도록 요구받고 있습니다. 아마존 단독으로만 2024년 중에 북미에서 15개의 신규 인터모달 시설을 개시하여 평균적인 '미들 마일' 구간의 단축을 도모했습니다. 2일 배송에 대한 기대와 확대되는 크로스보더 주문에 의해 500-1,500마일의 최적 거리대에서 철도 운송 회랑을 통한 화물량이 증가하고 있습니다. 옴니채널 소매업체도 재고 재배치 빈도를 높이고 있으며 운전자금을 높이지 않고 재고를 배치하는 민첩한 운송 모드로의 전환 수요가 증가하고 있습니다.

주요 미국 게이트웨이의 평균 컨테이너 체류 시간은 2019년 3.8일에서 2024년에는 5.2일로 늘어났습니다. 중국산 기기에 대한 관세와 국내 제조 능력의 제한으로 인해 공급량은 필요량의 78%에 머물고 있습니다. 컨테이너 반환 지연으로 인터모달 사업자는 하루에 약 150달러의 벌금을 부담하고 이는 장거리 트럭 운송과의 비용 경쟁력을 저하시킵니다. 자동화 프로젝트는 개선을 약속하지만, 다년간의 도입 기간을 필요로 하기 때문에 이 병목 현상은 단기적인 위험 요인으로 주목받고 있습니다.

소프트웨어 수익의 CAGR은 13.43%로 확대될 것으로 전망되어 인터모달 화물 운송 시장에서 2025년 매출의 60.42%를 차지하는 여전히 대규모인 서비스 범주를 뛰어넘는 성장세를 보이고 있습니다. 블루욘더의 AI 플랫폼은 이미 연간 20억 건 이상의 운송 판단을 처리하고 있으며 운송 경로 선택, 적재 통합, 운송 능력 예측을 강화하고 있습니다. 클라우드 도입 모델은 진입 장벽을 낮추어 중견 규모의 화주가 거액의 자본 지출 없이 견고한 운송 관리 시스템(TMS)과 창고 관리 시스템(WMS) 기능을 도입할 수 있도록 하고 있습니다.

서비스 제공업체는 소프트웨어 배포의 위험을 줄이고 지속적인 최적화를 추진하는 컨설팅, 배포 지원 및 매니지드 서비스를 패키징하여 우위를 유지하고 있습니다. Oracle은 2024년 Cerner 공급망 자산의 인수를 통해 의료 부문에서의 존재감을 강화했으며 코그니전트와 Microsoft Azure의 제휴는 제약 산업을 위한 멀티테넌트 시각화 옵션을 확대했습니다. FDA 및 DOT 규제 요건을 충족하는 컴플라이언스 모듈은 전문 소프트웨어에 대한 수요를 높이고 구독형 가격 설정은 공급업체의 수익 기반을 안정화시키고 있습니다. 소프트웨어와 연동하는 인터모달 화물 운송 시장 규모는 지속가능성 보고와 주문형 운송력 조정에 예측 분석이 필수적이 됨에 따라 확대될 것으로 예측됩니다.

2025년의 운송 모드별 매출에서 항공 및 도로의 조합이 45.62%를 차지했지만, 철도 및 도로 서비스는 2031년까지 연평균 복합 성장률(CAGR) 13.51%로 확대될 것으로 예상되어 인터모달 화물 운송 시장의 매출 구성을 변화시키고 있습니다. 지속적인 디젤 가격의 변동성과 40%의 연료 효율 우위로 인해 500마일이 넘는 운송에서는 철도가 유력한 선택이 되었습니다. 로스앤젤레스와 시애틀을 연결하는 30억 달러 규모의 북태평양 녹색 회랑 전기 철도 프로젝트가 이러한 전환을 뒷받침합니다.

고부가가치 및 시간 엄수 화물에는 항공 및 도로 솔루션이 여전히 필수적입니다. 페덱스가 40억 달러를 투자한 멤피스 월드 허브 확대사업에서는 철도 연결이 추가되어 국내 운송 시간을 최대 반나절 가량 단축하고 항공 운송 속도와 철도의 경제성을 융합시켰습니다. 해상과 도로, 해상과 철도의 조합은 벌크화물과 장거리 노선에서 계속 활용되고 있습니다. 반면 로보틱스와 자율주행 트럭은 라스트마일의 노동 비용을 줄임으로써 향후 운송 모드의 점유율을 재조정할 수 있습니다.

아시아태평양은 2025년 매출의 29.33%를 차지하였으며, 13.69%의 연평균 복합 성장률(CAGR)로 성장이 예상되어, 인터모달 화물 운송 시장에서 가장 급속히 확대되는 지역으로서의 지위를 확고히 하고 있습니다. 중국 및 유럽의 급행 철도 서비스는 2024년에 1만 7,000개 이상의 운행을 기록했으며 고부가가치 화물의 해상 운송 스케줄을 10-15일 단축하였습니다. 인도의 전용 화물 회랑과 ASEAN 국경을 넘는 철도 연결은 베트남, 태국, 인도네시아의 생산 거점과 주요 항만을 동기화하여 네트워크의 도달 범위를 확대하고 있습니다.

북미는 수익 규모로는 2위를 차지하고 있으며 USMCA(미국, 멕시코 및 캐나다 협정)에 따른 무역 경로와 대규모 인프라 투자가 기반이 되고 있습니다. 이 지역에 속한 인터모달 화물 운송 시장 규모는 국경 통과의 효율화와 인터체인지 체류 시간의 단축을 도모하는 라레도-몬테레이 회랑과 캐나다 퍼시픽 캔자스시티사의 단선 철도망의 혜택을 누릴 전망입니다. 운전자 부족과 섀시 부족이 단기적인 성장을 억제하지만 정부 보조금과 민간 설비 투자에 의해 지원되는 장기적인 성장 궤도는 흔들리지 않습니다.

유럽에서는 배출량 감소와 크로스보더 표준화가 주요 초점입니다. 'Fit for 55' 탄소 규제와 250억 유로(273억 달러) 규모의 TEN-T 자금으로 1,500km 이하의 화물 운송에서 철도 중심의 경로로의 전환이 가속화되고 있습니다. 독일의 자동화 철도 터미널과 영국의 항만 정비는 브렉시트 후 무역 재편을 완화하는 역할을 합니다. 남미, 중동, 아프리카 등의 신흥 지역은 절대 규모로는 여전히 작지만 상품 운송 회랑이나 일대일로에 의한 인프라 투자 프로젝트에 따라 특정 부문에서의 기회가 존재합니다.

The intermodal freight transportation market size in 2026 is estimated at USD 31.18 billion, growing from 2025 value of USD 27.52 billion with 2031 projections showing USD 58.15 billion, growing at 13.28% CAGR over 2026-2031.

Rising e-commerce volumes, accelerating supply-chain digitalization, and policy-driven decarbonization goals are converging to reshape modal choices and propel demand for integrated logistics solutions. Public spending on infrastructure, including the USD 10 billion automated rail corridor between Laredo and Monterrey, as well as large-scale Belt and Road rail investments, has begun to unlock latent capacity while redirecting continental trade flows. Technology adoption is expanding real-time visibility, shrinking dwell times, and increasing asset utilization rates, while sustainability mandates reinforce the economic case for rail-road and maritime-rail combinations. Competitive differentiation is shifting from pure asset scale to the ability to orchestrate software, analytics, and certified low-carbon services within a single multimodal platform.

Widespread adoption of cloud-based logistics platforms now connects carriers, terminals, and shippers within unified data ecosystems that process billions of transactions per year . Predictive analytics reduces dwell times by double-digit percentages and supports dynamic routing that lifts asset-utilization rates across rail, road, and maritime legs. IoT-equipped smart containers transmit temperature, humidity, and location data, reinforcing cargo integrity and lowering insurance costs. Blockchain-enabled records offer immutable proof-of-delivery that resolves historic disputes among modal operators, while API-rich architectures ease integration with legacy EDI standards. Collectively, these digital building blocks are turning the intermodal freight transportation market into a data-driven network capable of near-real-time course correction at scale.

B2C parcel demand continues to grow faster than total merchandise trade, forcing shippers to shift from point-to-point full-truckload moves toward hub-and-spoke intermodal solutions that balance speed and cost. Amazon alone commissioned 15 new North American intermodal facilities during 2024 to shorten the average "middle-mile" hop. Two-day delivery expectations and enlarging cross-border order books channel higher volumes onto rail-road corridors within the 500-1,500-mile sweet spot. Omnichannel retailers also reposition inventory more frequently, raising demand for agile mode-switching that keeps shelves stocked without inflating working capital.

Average container dwell time at major U.S. gateways reached 5.2 days in 2024, up from 3.8 days in 2019, as chassis availability fell short of peak-season demand. Tariffs on Chinese-built equipment and limited domestic manufacturing capacity left supply at 78% of required levels. Intermodal operators incurred daily penalty fees near USD 150 for late container returns, undermining cost competitiveness versus long-haul trucking. Automation projects promise relief but require multiyear deployments, keeping this bottleneck on short-term risk radars.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Software revenues are growing at 13.43% CAGR, outpacing the larger services category that still accounts for 60.42% of 2025 turnover within the intermodal freight transportation market. Blue Yonder's AI platform already ingests over 2 billion shipment decisions each year, enhancing lane selection, load consolidation, and capacity prediction. Cloud deployment models lower entry barriers, enabling mid-market shippers to adopt robust TMS and WMS capabilities without heavy capital outlays.

Service providers maintain their lead by bundling consulting, implementation, and managed services that de-risk software launches and drive ongoing optimization. Oracle's 2024 acquisition of Cerner's supply-chain assets strengthened its healthcare footprint, while Cognizant's alliance with Microsoft Azure expanded multitenant visibility options for pharmaceuticals. Compliance modules covering FDA and DOT mandates elevate demand for specialized software, and subscription pricing stabilizes revenue streams for vendors. The intermodal freight transportation market size linked to software is set to widen as predictive analytics becomes indispensable for sustainability reporting and on-demand capacity orchestration.

Air-road pairings held 45.62% of 2025 modal revenue, yet rail-road services are advancing at a 13.51% CAGR through 2031 and shifting the revenue mix of the intermodal freight transportation market. Sustained diesel price volatility and a 40% fuel-efficiency edge make rail compelling for hauls over 500 miles. The USD 3 billion North Pacific Green Corridor electrified rail project connecting Los Angeles and Seattle underpins this pivot.

Air-road solutions remain irreplaceable for high-value, time-sensitive cargo. FedEx's USD 4 billion Memphis World Hub expansion added rail links that compress domestic transit by up to half a day, blending airspeed with rail economics . Maritime-road and maritime-rail combinations continue to serve bulk and long-distance lanes, while robotics and autonomous trucks may eventually rebalance mode shares by shrinking final-mile labor costs.

The Intermodal Freight Transportation Market is Segmented by Component (Software, Service), Transportation Mode (Rail and Road Transport, Air and Road Transport, and More), End-User Industry (Industrial and Manufacturing, and More), Container Type (Dry Containers, Refrigerated Containers, and More), Service Type (Transportation Planning, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia Pacific accounted for 29.33% of 2025 revenue and is poised to grow at 13.69% CAGR, firmly establishing itself as the fastest-expanding region in the intermodal freight transportation market. China-Europe Railway Express services tallied more than 17,000 trains in 2024, shaving 10-15 days off maritime schedules for high-value goods. India's Dedicated Freight Corridor and ASEAN cross-border rail links are synchronizing production bases in Vietnam, Thailand, and Indonesia with major seaports, broadening the network's reach.

North America ranks second by revenue, underpinned by USMCA-aligned trade lanes and extensive infrastructure investment. The intermodal freight transportation market size attached to the region will benefit from the Laredo-Monterrey corridor and the Canadian Pacific Kansas City single-line rail network, both of which streamline border crossings and reduce interchange dwell time. Driver shortages and chassis deficits temper near-term upside but do not derail the long-term growth trajectory supported by government grants and private capex.

Europe focuses on emission reduction and cross-border standardization. Fit for 55 carbon rules and EUR 25 billion (USD 27.3 billion) in TEN-T funding are accelerating a pivot to rail-centric itineraries for freight under 1,500 km. Automated rail terminals in Germany and port upgrades in the United Kingdom buffer post-Brexit trade realignment. Emerging regions such as South America, the Middle East, and Africa remain smaller in absolute terms yet present targeted opportunities along commodity corridors and Belt and Road-financed infrastructure tranches.