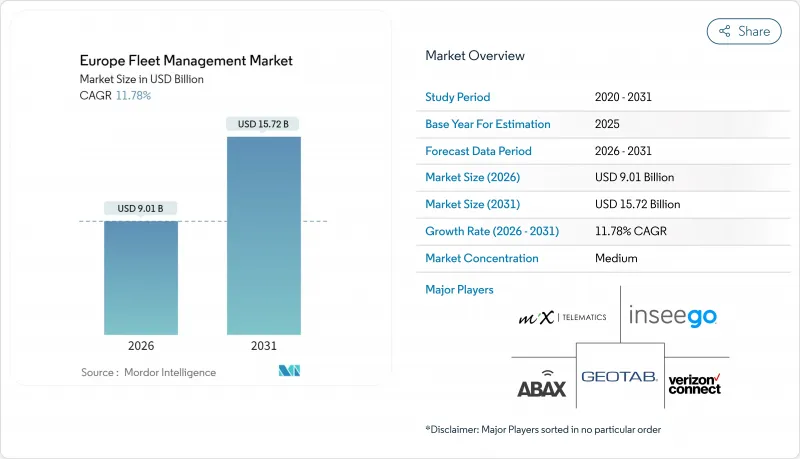

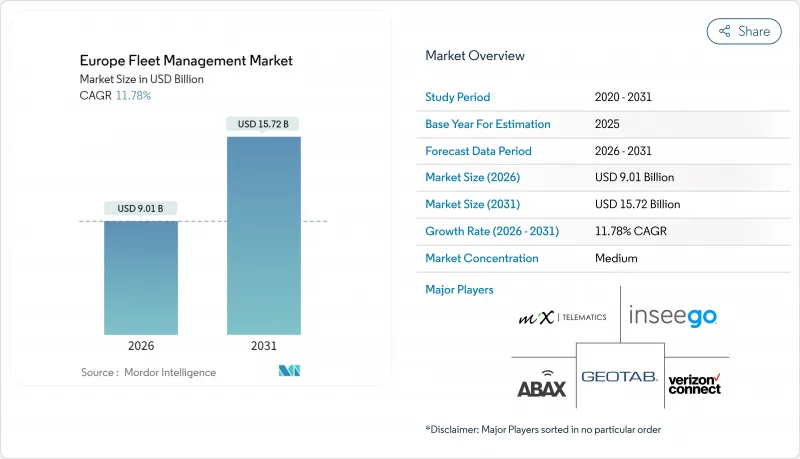

유럽의 플릿 관리 시장은 2025년 80억 6,000만 달러로 평가되었으며, 2026년 90억 1,000만 달러에서 2031년까지 157억 2,000만 달러에 이를 것으로 예측됩니다.

예측기간(2026-2031년)의 CAGR은 11.78%로 예상됩니다.

규제 압력 증가, 커넥티드카 아키텍처의 보급, 라스트마일 물류의 격화가 함께 대응 가능한 수요를 확대하고 있습니다. 2025년에 시행되는 EU 스마트 타코그래프 2단계 제도는 실시간 데이터 전송을 의무화하고 텔레매틱스를 임의의 효율화 도구에서 컴플라이언스 요건으로 전환시킵니다. 전자상거래량 증가는 도시 배송의 주행거리를 증가시켜 사업자는 상세한 경로 최적화와 운전자 행동 분석을 추진하고 있습니다. 동시에 모바일 IoT 통신 요금의 저하와 eSIM의 보급에 의해 연결 비용이 줄어드는 한편, 5G의 도달범위 확대에 의해 AI 영상 안전 모니터링 등의 고대역 용도가 가능해집니다. 자동차 제조업체는 자동차 데이터 스트림의 수익 창출을 위해 API(Application Programming Interface)를 개방하고 있으며, 이를 통해 플릿 사업자는 임베디드 텔레매틱스에 직접 액세스할 수 있습니다. 마지막으로, 각국의 탄소 저감 목표와 저배출 구역의 도입은 전기화를 가속화하고 있으며, 이는 에너지와 자산의 보다 엄격한 조정을 요구합니다.

2025년 6월부터 시행되는 본 의무화로 3.5톤 이상의 상용차는 위치정보와 운전시간 데이터를 지속적으로 전송하도록 의무화되어 정기적인 데이터 다운로드에서 실시간 모니터링으로 시스템이 이행하게 됩니다. 1,500유로에서 1만 5,000유로의 자동 벌금이 설정되기 때문에 사업자는 통합 텔레매틱스 시스템의 도입을 강요받게 됩니다. 독일의 주요 물류기업은 이미 서비스 중단을 피하기 위해 도입을 완료하고 있으며, 공급업체에 따르면 소규모 플릿도 단독 타코그래프가 아닌 여러 차량용 구독 모델을 요구하는 경향이 있습니다. 사업자가 전체 차종에서 통일된 관리 화면을 선호하기 때문에 수요는 소형 밴이나 상용차 풀에도 파급되어 플랫폼 전체의 도입률을 높이고 있습니다.

2024년 유럽의 소매 매출액에서 차지하는 온라인 판매 비율은 13.4%에 달했으며 소포 배송 사업자에게 라스트마일 비용은 물류 지출의 41%를 차지하였습니다. 소비자가 익일 배송을 기대하는 가운데 소형 밴의 주행거리는 2024년 대비 23% 증가했습니다. Seur 등의 사업자는 AI 기반 스케줄 관리 도입 이후 경로 관련 비용을 15% 절감하면서 텔레매틱스의 구체적인 투자 효과를 실증하고 있습니다. 바르셀로나, 마드리드, 파리의 저배출 구역은 시간대 지정에 의한 접근 제한으로 더욱 복잡해지고 따라서 실시간 규제 데이터가 필수적입니다. 따라서 유럽의 플릿 관리 시장은 끊임없는 위치 정보, 교통 상황 및 규정 준수 정보를 제공해야 하는 전자상거래와 환경 압력의 수렴으로 이익을 얻고 있습니다.

GDPR(EU 개인정보보호규정)에서는 GPS 추적에 대한 직원의 동의가 명시적이고 철회 가능해야 하며, 2024년 독일의 여러 판결에서는 종합적인 모니터링이 노동자의 권리를 침해하는 것으로 나타났습니다. 중규모 플릿의 경우 법적 심사, 데이터 보호 책임자 및 소프트웨어 재설계에 소요되는 연간 비용은 약 12만 5,000유로에 달할 전망입니다. 다국적 사업자는 규제가 보다 엄격한 국경에 진입할 때 운전석 카메라의 스트리밍 등의 기능을 무효화해야 하는 경우가 있으며 이는 텔레매틱스의 효율성이라는 이점을 손상시키면서 도입 스케줄을 연장하게 됩니다.

클라우드 서비스는 2025년에 유럽의 플릿 관리 시장의 63.55%를 차지하였고, 종량 과금제와 자동 소프트웨어 업데이트를 원동력으로 2031년까지 연평균 복합 성장률(CAGR) 14.56%로 확대될 전망입니다. 도이체 텔레콤에 의하면, 멀티테넌트 아키텍처는 온프레미스형에 비해 서버 조달 및 보수 의무를 회피할 수 있기 때문에 총 소유 비용을 34% 절감합니다. 플릿 관리자의 경우 탄력적인 데이터 스토리지는 수동 스케일링을 필요로 하지 않으며 계절적인 데이터 양의 변동에 대응할 수 있습니다. 데이터 주권에 대한 우려로 일부 중요한 인프라는 프라이빗 서버로 제한되었지만, 클라우드 제공업체는 GDPR(EU 개인정보보호규정) 인증을 받은 EU 기반 데이터센터를 제공함으로써 컴플라이언스 격차를 채우고 있습니다.

엣지 컴퓨팅은 현재 클라우드 모델의 대안이 아닌 확장 기능으로 기능하고 있습니다. 시간 의존성이 높은 운전 지원 계산은 자동차 프로세서에서 수행되며 집계 분석, 보고 및 무선 업데이트는 중앙 허브를 통과합니다. 이 하이브리드 방식은 지연 및 거버넌스 요구 사항을 모두 충족하여 유럽의 플릿 관리 시장에서의 새로운 도입의 기본 아키텍처로서 클라우드의 지위를 확고히 하고 있습니다.

2025년 시점에서 유럽의 플릿 관리 시장의 점유율 26.72%를 차지한 부문은 자산 관리입니다. 이는 모든 사업자가 위치 정보와 가동률 데이터를 중시하고 있기 때문입니다. 한편, 안전 규정 준수 도구는 14.34%의 연평균 복합 성장률(CAGR)로 성장하고 있습니다. 이는 규제 당국과 보험 회사가 사고 방지에 금전적 인센티브를 연결하고 있기 때문입니다. 알리안츠는 플릿이 적극적인 운전자 모니터링을 입증했을 때 최대 15%의 보험료 할인을 제공하여 주행거리가 많은 택배 서비스로의 도입을 가속화하고 있습니다. 2050년까지 도로 사망 사고 수 제로를 목표로 하는 EU 비전 제로 프로그램은 AI를 활용한 피로 탐지나 사각 경보를 복수의 회원국에서의 영업 허가의 전제조건으로 지정하고 있습니다. 공급업체는 현재 안전 대시보드를 타코그래프 파일과 번들링하여 규정 준수 제출이 원활하고 검증 가능한지 확인합니다.

The Europe fleet management market was valued at USD 8.06 billion in 2025 and estimated to grow from USD 9.01 billion in 2026 to reach USD 15.72 billion by 2031, at a CAGR of 11.78% during the forecast period (2026-2031).

Rising regulatory pressure, the spread of connected-vehicle architectures, and intensifying last-mile logistics are together expanding addressable demand. The EU smart-tachograph Phase II rule that starts in 2025 compels real-time data transmission, turning telematics from an optional efficiency tool into a compliance requirement. E-commerce volume growth elevates urban delivery mileage, pushing operators toward granular route optimization and driver behaviour analytics. At the same time, falling cellular-IoT tariffs and eSIM adoption lower connectivity costs while 5G coverage enables high-bandwidth applications such as AI video safety monitoring. OEMs are opening application programming interfaces to monetize in-vehicle data streams, giving fleets a direct path to embedded telematics. Finally, national carbon-reduction targets and low-emission zones speed up electrification, which requires tighter energy and asset coordination.

The mandate enforced from June 2025 forces every commercial vehicle above 3.5 t to transmit location and driver-hours data continuously, replacing periodic data downloads with real-time oversight. Automatic fines structured between EUR 1,500 and EUR 15,000 leave operators' little choice but to install integrated telematics suites. Large German logistics firms have already completed rollouts to avoid service disruption, and suppliers report that small fleets now request multi-vehicle subscriptions rather than standalone tachographs. Because operators prefer a single pane of glass across all classes of vehicles, demand is spilling into light vans and company-car pools, lifting total platform adoption.

Online retail penetration climbed to 13.4% of European sales in 2024, and last-mile costs swallow 41% of logistics spend for parcel operators. Light vans now cover 23% more mileage than in 2024 as consumers expect next-day delivery. Operators such as Seur cut route-related costs by 15% after introducing AI-based scheduling, demonstrating tangible return on telematics. Low-emission zones in Barcelona, Madrid, and Paris add further complexity by restricting time-window access, making real-time regulatory data essential. The Europe fleet management market, therefore benefits from converging e-commerce and environmental pressures that require constant location, traffic, and compliance feeds.

Under GDPR, employee consent for GPS tracking must be explicit and revocable, and several German court cases in 2024 confirmed that blanket monitoring infringes worker rights. For medium fleets, annual spending on legal review, data-protection officers, and software redesign totals about EUR 125,000. Multinational operators must sometimes deactivate features such as driver-cam streaming when crossing borders with stricter rules, diluting the efficiency promise of telematics and extending deployment timelines.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Cloud services captured 63.55% of Europe fleet management market share in 2025 and are climbing at a 14.56% CAGR through 2031, propelled by pay-as-you-go pricing and automatic software updates. Deutsche Telekom observes that a multi-tenant architecture trims total cost of ownership by 34% relative to on-premises hosting because operators avoid server procurement and maintenance obligations. For fleet managers, elastic data storage accommodates seasonal volume swings without manual scaling. Data-sovereignty concerns confined some critical infrastructure fleets to private servers, yet cloud providers have responded with EU-based data centers that carry GDPR certification, closing the compliance gap.

Edge computing now operates as an extension of the cloud model rather than a replacement. Time-sensitive driver-assistance calculations run on in-vehicle processors, while aggregate analysis, reporting, and over-the-air updates flow through centralized hubs. This hybrid approach satisfies both latency and governance requirements, cementing cloud as the default architecture for new deployments within the Europe fleet management market.

Asset management held 26.72% of Europe fleet management market size in 2025 because every operator values location and utilization data. Safety and compliance tools, however, are advancing at a 14.34% CAGR because regulators and insurers tie monetary incentives to incident prevention. Allianz provides up to 15% premium discounts when fleets demonstrate proactive driver monitoring, accelerating adoption among high-mileage courier services. The EU Vision Zero program, which aims for zero road fatalities by 2050, positions AI-enabled fatigue detection and blind-spot alerts as pre-requisites for operating licenses in several member states. Vendors now bundle safety dashboards with tachograph files, ensuring compliance submissions are seamless and verifiable.

The Europe Fleet Management Market Report is Segmented by Deployment Type (On-Demand Cloud, On-Premises), Application (Asset Management, Information Management, and More), End-User Vertical (Transportation and Logistics, Energy and Utilities, and More), Fleet Size, Vehicle Type (Light Commercial Vehicles, Heavy Commercial Vehicles, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).