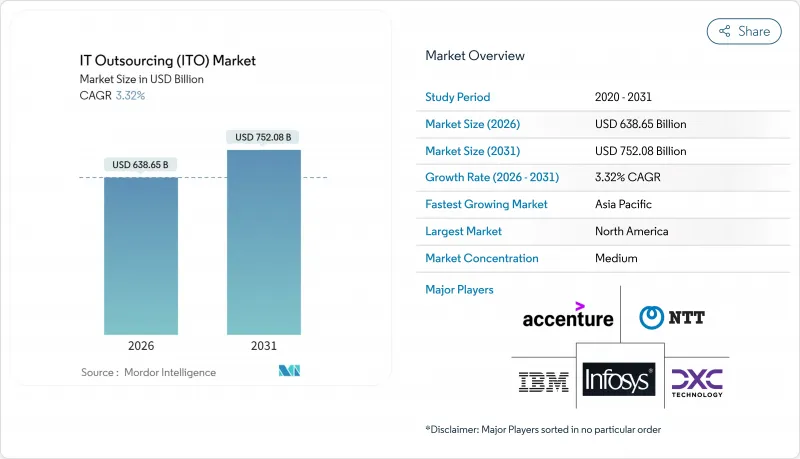

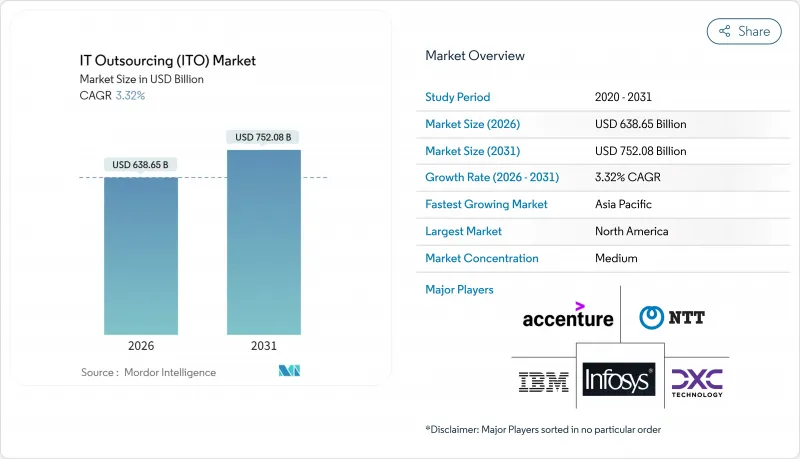

IT 아웃소싱(ITO) 시장은 2025년 6,181억 3,000만 달러로 평가되었으며, 2026년 6,386억 5,000만 달러에서 2031년까지 7,520억 8,000만 달러에 이를 것으로 예측됩니다.

예측기간(2026-2031년)의 CAGR은 3.32%로 예상됩니다.

이 예측 채널은 생성형 AI에 의한 자동화가 노동 집약적인 제공 모델을 변화시키고 새로운 AI 대응 서비스를 촉진하는 한편, 기존 인원 의존형 계약을 축소시킴으로써 산업의 성숙도를 반영하고 있습니다. 지정학적 긴장이 증가함에 따라 기업은 주권 클라우드 의무와 데이터 거주 제도에 대한 대응으로 딜리버리 거점의 다양화를 추진하고 있으며, 많은 바이어들이 리스크 경감을 위해 해외, 니어쇼어, 온쇼어의 센터를 조합하는 경향이 있습니다. 세계적으로 480만명에 달하는 사이버 보안 인력 부족은 매니지드 탐지 및 대응 서비스에 대한 프리미엄 수요를 낳고 있습니다. 산업 재편도 가속화되고 있으며 코그니전트가 벨칸을 13억 달러에 인수하고 캡 제미니가 WNS 인수를 위해 협상을 실시하는 등 최근의 사례는 대기업이 틈새 전문 기업을 흡수하고 AI 능력의 강화와 서비스 포트폴리오의 확충을 도모하는 움직임을 보여줍니다. 기업이 하이브리드 및 멀티클라우드 환경을 관리하는 데 어려움을 겪으면서 클라우드 관리 서비스가 중요성을 높이고 있으며, 측정 가능한 비즈니스 성과와의 연동성을 통해 성과 연동형 가격 설정이 지지를 받고 있습니다.

기업은 모놀리식 시스템을 마이크로서비스, 컨테이너, 서버리스 기능으로 재구축하고 있으며, 따라서 플랫폼 엔지니어링, Kubernetes 오케스트레이션, 이벤트 중심 설계의 대규모 이슈가 탄생하고 있습니다. 공급자는 특히 금융 서비스, 의료 등 컴플라이언스가 복잡해지는 고도로 규제된 산업에서 노동에 대한 과금이 아니라 성능, 비용 목표, 확장성을 보장하는 성과 기반 계약을 점점 제공하게 되었습니다. 기술적 변화는 문화적 변화의 관리를 수반하며, 사내 팀에서는 쉽게 도입할 수 없는 애자일 프로세스에 대해서는 외부 파트너가 조언하는 경우가 주로 나타나고 있습니다.

생성형 AI는 지능형 라우팅 및 자체 복구 스크립트를 통해 레벨 1 티켓의 양을 최대 40% 줄이고 평균 해결 시간을 25% 단축합니다. 가상 어시스턴트는 현재 여러 시스템에 걸친 컨텍스트를 파악하고 맞춤 응답을 제공하며 사용자가 장애를 인식하기 전에 사고를 예측합니다. 그러나 컨텍스트 결정이 필요한 복잡한 보안 문제의 경우 공급자는 자동화와 인간 모니터링을 결합해야 합니다.

사이버 사고가 증가함에 따라 보험료가 상승하고 보상 범위가 좁아짐에 따라 기업은 프로젝트 비용을 높이는 암호화, 액세스 모니터링 및 분리 개발 영역을 추가해야 합니다(EY). 구매자는 현재 벤더에 대해 더 높은 보험 한도를 유지하고 정기적으로 침투 테스트를 실시하도록 요구하고 있으며, 이러한 장애물은 중소 벤더를 불리하게 만들고 산업 재편을 가속화하고 있습니다.

2025년 인프라 아웃소싱은 IT 아웃소싱(ITO) 시장의 45.05%를 차지했습니다. 이는 지속적인 모니터링과 규제 준수를 필요로 하는 장애 허용 데이터센터 운영에 대한 기업의 의존도가 높아지기 때문입니다. 그러나 클라우드 관리 서비스는 3.44%의 연평균 복합 성장률(CAGR)로 시장을 견인하고 있습니다. 이는 AWS, Azure, Google Cloud 등 프라이빗 환경을 가로지르는 하이브리드 환경의 복잡성에 직면하고 있기 때문입니다. 공급업체는 현재 비용, 대기 시간 및 컴플라이언스 요구 사항에 따라 워크로드를 순서화하는 통합 관리 플랫폼을 번들로 제공하며 기존 인프라 관리와 신흥 멀티 클라우드 오케스트레이션의 경계를 모호하게 만듭니다.

애플리케이션 개발 및 유지보수 수요는 로우코드와 AI 지원 개발에 의해 재구성되고 있으며, 벤더는 도메인 지식과 통합 전문성에 의한 차별화를 요구받고 있습니다. 엣지 컴퓨팅과 AI 모델 수명 주기 서비스는 '기타' 범주에 자리잡고 있으며, 성장의 여지와 높은 이익률 기회를 나타냅니다. 클라우드 도입이 진행됨에 따라 기존 기업은 AI 구동의 자가 복구 기능으로 보장된 서비스 수준 목표를 달성하는 자동화된 사이트 신뢰성 엔지니어링 서비스로 전환하여 가격 압축으로부터 인프라 수익원을 보호하고 있습니다.

2025년에도 복잡한 레거시 환경을 유지하기 위한 깊은 아키텍처 지식을 보유한 대기업이 매출의 67.25%를 차지하였습니다. 그러나 중소기업(SME)은 3.96%의 연평균 복합 성장률(CAGR)로 더욱 빠르게 확대되고 있습니다. 성과연동형 계약은 IT 지출을 직원 수가 아닌 구체적인 비즈니스 성과에 연동시켜 중소규모 기업에 의해 뒷받침됩니다. 클라우드 네이티브 벤더는 셀프 서비스 포털과 자동 프로비저닝을 통해 진입 장벽을 줄이고 한때 포춘지 선정 500대 기업의 예산 규모로만 이용할 수 있었던 AI, 분석, 사이버 보안 기능을 중소기업에도 온디맨드로 제공합니다. 이러한 기술의 민주화는 IT 아웃소싱의 총 잠재 시장을 확대하는 동시에 기존 공급자에게 이익률을 저하시키지 않고 경제적으로 축소 가능한 모듈화 및 표준화된 서비스 창출을 요구하고 있습니다.

IT 아웃소싱(ITO) 시장은 서비스 유형(인프라 아웃소싱, 애플리케이션 개발 및 유지보수 등), 조직 규모(중소기업 및 대기업), 딜리버리 장소(온쇼어, 니어쇼어 등), 최종 사용자 산업(은행, 금융 서비스 및 보험(BFSI), 의료 및 생명과학 등), 지역별로 세분화됩니다. 시장 예측은 금액(달러) 기준으로 제공됩니다.

북미의 점유율 24.12%는 경험이 풍부한 공급자를 필요로 하는 AI와 클라우드 근대화 이니셔티브의 주요 도입 지역으로서의 지위를 나타내고 있습니다. 미국 기업은 거래당 비용과 수익 향상 지표를 규정하는 성과 기반 조건을 향해 레거시 계약의 재협상을 진행하고 있으며, 이를 통해 노동력 중재의 위험을 줄이고 있습니다. 캐나다 기업은 엄격한 개인정보 보호법을 준수하기 위해 제로 트러스트 보안 프레임워크와 소버린 클라우드 인스턴스를 선호합니다. 멕시코의 니어쇼어 센터는 애자일 포드와 DevOps 능력을 확대하고 프로젝트 지연을 줄여 미국 고객과의 문화적 무결성을 높입니다.

아시아태평양의 CAGR 3.66%는 인도의 지속적인 이점과 ASEAN의 기여 확대에 기인합니다. 베트남, 인도네시아, 말레이시아는 정부의 인센티브와 학술 연계를 통해 엔지니어 인재 육성 파이프라인을 강화하고, 애플리케이션 개발 테스트의 2차 거점으로서의 지위를 확립하고 있습니다. 일본과 한국은 차세대 네트워크 운용과 엣지 클라우드 오케스트레이션을 아웃소싱해 국내 인력 부족을 상쇄했습니다. 호주에서는 매니지드 사이버 보안과 클라우드 FinOps 서비스에 대한 수요가 증가하고 있습니다.

유럽에서는 엄격한 데이터 보호 규정과 디지털 주권에 대한 강한 관심이 나타나고 있습니다. 현지 제공업체는 하이퍼스케일러와 제휴하여 지역별 소버린 클라우드를 배포합니다. 독일, 프랑스, 네덜란드는 국내 데이터 처리를 견지하면서 부문별 클라우드 이행을 추진하고 있습니다. 영국은 브렉시트 후에도 금융 서비스 아웃소싱의 거점으로 탄력성 테스트와 운영 리스크 관리에 중점을 두고 있습니다. 동유럽의 소프트웨어 엔지니어링 클러스터는 하이엔드 R&D 아웃소싱을 제공하면서 서유럽 고객과의 다양화 계약을 통해 지정학적 불확실성을 회피하고 있습니다.

The IT outsourcing market was valued at USD 618.13 billion in 2025 and estimated to grow from USD 638.65 billion in 2026 to reach USD 752.08 billion by 2031, at a CAGR of 3.32% during the forecast period (2026-2031).

The measured trajectory mirrors the sector's maturation as generative AI automation reshapes labor-intensive delivery models, spurring new AI-enabled services while compressing traditional headcount-driven contracts. Geopolitical tensions are prompting enterprises to diversify sourcing footprints in response to sovereign-cloud mandates and data-residency rules, leading many buyers to blend offshore, nearshore, and onshore centers for risk mitigation. The cybersecurity talent shortfall of 4.8 million positions worldwide is creating premium demand for managed detection and response offerings. Consolidation is accelerating: recent deals such as Cognizant's USD 1.3 billion Belcan purchase and Capgemini's negotiations to acquire WNS illustrate how scale players absorb niche specialists to deepen AI capabilities and broaden portfolios. Cloud-managed services are gaining prominence as enterprises struggle to govern hybrid, multicloud estates, while outcome-based pricing gains favor for its alignment with measurable business results.

Enterprises are re-architecting monolithic systems into microservices, containers, and serverless functions, which opens sizable engagements for platform engineering, Kubernetes orchestration, and event-driven design. Providers increasingly deliver outcome-based contracts that guarantee performance, cost targets, and scalability rather than billing for effort, particularly in highly regulated verticals such as financial services and healthcare where compliance adds complexity. Cultural change management complements the technical shift, and external partners frequently guide agile processes that internal teams cannot easily instill.

Generative AI is cutting Level 1 ticket volumes by up to 40% and trimming mean-time-to-resolution by 25% through intelligent routing and self-healing scripts. Virtual assistants now grasp context across multiple systems, drive personalized responses, and predict incidents before users notice disruption. Providers must, however, pair automation with human oversight for complex security issues that demand contextual judgment.

Increasing cyber incidents raise premiums and narrow coverage, forcing enterprises to add encryption, access monitoring, and segregated development zones that inflate project costs EY. Buyers now demand providers carry higher insurance limits and submit to regular penetration tests, a hurdle that disadvantages smaller vendors and fuels consolidation.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Infrastructure outsourcing commanded 45.05% of the IT outsourcing market in 2025 due to enterprises' reliance on resilient data center operations that need continuous monitoring and regulatory compliance. Cloud-managed services, however, are pacing the field with a 3.44% CAGR as organizations confront the complexity of hybrid estates spanning AWS, Azure, Google Cloud, and private environments. Providers now bundle unified management platforms that sequence workloads by cost, latency, and compliance preferences, challenging the boundaries between traditional infrastructure management and emerging multicloud orchestration.

Demand for application development and maintenance is being reshaped by low-code and AI-assisted development, pushing vendors to differentiate through domain knowledge and integration expertise. Edge computing and AI model lifecycle services sit in the "Others" bucket and represent nascent yet high-margin opportunities. As cloud adoption rises, incumbents pivot to automated site-reliability-engineering services that deliver guaranteed service-level objectives using AI-driven self-healing, thereby protecting infrastructure revenue streams against price compression.

Large enterprises retained 67.25% of spending in 2025 as their complex legacy estates require deep architectural know-how, yet SMEs are expanding faster at a 3.96% CAGR. Outcome-based contracts resonate with smaller firms because they align IT spending to tangible business outcomes instead of headcount. Cloud-native vendors lower entry barriers with self-service portals and automated provisioning, giving SMEs on-demand access to AI, analytics, and cybersecurity capabilities once exclusive to Fortune 500 budgets. This democratization of technology widens the total addressable IT outsourcing market and pressures established providers to create modular, standardized offerings that scale down economically without compromising margin.

IT Outsourcing (ITO) Market is Segmented by Service Type (Infrastructure Outsourcing, Application Development and Maintenance, and More), Organization Size (SMEs and Large Enterprises), Sourcing Location (On-Shore, Near-Shore, and More), End-User Industry (BFSI, Healthcare and Life-Sciences, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America's 24.12% share confirms its status as the prime adopter of AI and cloud modernization initiatives that demand seasoned providers. United States enterprises are renegotiating legacy contracts toward outcome-based terms that stipulate cost-per-transaction or revenue uplift metrics, reducing labor-arbitrage exposure. Canadian firms prioritize zero-trust security frameworks and sovereign cloud instances to comply with stringent privacy acts. Mexican nearshore centers expand agile pods and DevOps capabilities, reducing project latency and enhancing cultural alignment for US clients.

Asia-Pacific's 3.66% CAGR stems from India's continued dominance and rising contributions from ASEAN economies. Vietnam, Indonesia, and Malaysia are nurturing engineering talent pipelines through government incentives and academic partnerships, positioning themselves as secondary hubs for application development and testing. Japan and South Korea outsource next-generation network operations and edge-cloud orchestration to compensate for local workforce gaps, and Australia increases demand for managed cybersecurity and cloud FinOps services.

Europe combines stringent data-protection mandates with an appetite for digital sovereignty. Local providers form alliances with hyperscalers to launch region-specific sovereign cloud zones. Germany, France, and the Netherlands drive sectoral cloud migration while insisting on in-country data processing. The United Kingdom, despite Brexit, remains a hub for financial-services outsourcing, emphasizing resilience testing and operational-risk controls. Eastern Europe's software-engineering clusters offer high-end R&D outsourcing but navigate geopolitical uncertainty through diversification agreements with Western European clients.