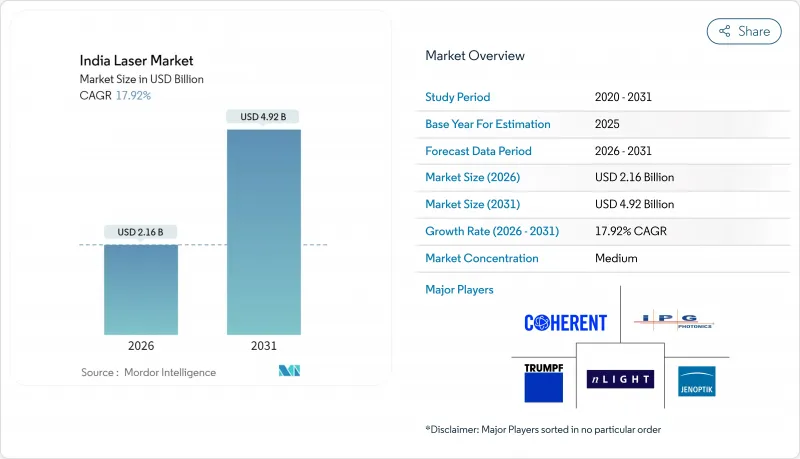

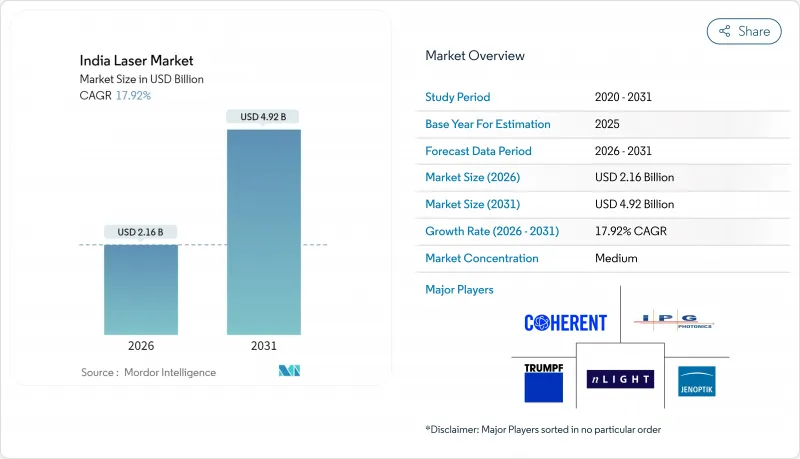

2026년 인도의 레이저 시장 규모는 21억 6,000만 달러로 추정되며, 2025년 18억 3,000만 달러에서 성장할 것으로 예상됩니다. 2031년 예측은 49억 2,000만 달러에 이르고, 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 17.92%로 확대될 전망입니다.

이 성장 전망은 정부의 생산연동형 인센티브(PLI) 제도, 반도체 제조 공장에 대한 재정 지원, 산업용 자동화 라인의 도입 기반 확대에 의해 뒷받침되고 있습니다. 클러스터형 전자기기 제조의 급증, 전기자동차 배터리 용접의 수요 급증, 수입 레이저 기기에 대한 정책 주도의 세제 우대 조치가 잠재 고객층의 확대에 기여하고 있습니다. 대규모 최종 사용자는 처리량을 향상시키기 위해 기존 CO2 및 Nd:YAG 시스템에서 고출력 파이버 플랫폼으로 전환하고 있으며, 중소기업은 자본 장벽을 극복하기 위해 레이저 가공 서비스 제공업체를 활용하고 있습니다. 국제 벤더는 애프터서비스 지원의 현지화를 강화하고, 국내 제조업체는 수직 통합형 기계를 도입하고 있으며, 이러한 동향이 더하여 기술 확산이 엔지니어링 거점 전체에서 강화되고 있습니다.

전자기기 생산량은 2025년 11조 루피(1,320억 달러)에 달하였으며, 지난 10년간 5배로 급성장했습니다. 부품 수준의 지원책이 현지 저항기 및 커패시터 생산 라인을 뒷받침하고 있습니다. 돌레라(구자라트 주)와 호수르-오라가담 지역(타밀 나두 주)에 클러스터를 집중함으로써 물류 사이클이 단축되어 저스트 인 타임 레이저 절단 마킹 서비스가 가능해졌습니다. 중소기업은 공동 작업장을 통해 경제적인 접근성을 확보하며, 주요 OEM 제조업체는 섀시 트리밍 및 하우징 용접을 위해 수kW급의 파이버 벤치를 통합하고 있습니다. 서비스 밀도가 높아지면 다운타임이 줄어들고 고출력화로의 업그레이드가 촉진됩니다. 그 결과, 시장 전체에서 중 및 고출력 파이버 광원에 대한 수요가 꾸준히 증가하고 있습니다.

2030년까지 500GWh를 넘을 것으로 예상되는 리튬 이온 배터리 셀 수요의 확대를 이용하여 OEM 제조업체는 구리 및 알루미늄 접합용으로 마이크로초 펄스 파이버 용접기의 도입을 추진하고 있습니다. 라이트 메카닉스 등의 국내 통합업체는 원통형, 각형 및 파우치형 셀의 접합에 대응하는 턴키식 용접 장치를 도입하여 지역 공급망의 강화에 공헌하고 있습니다. 자동차 산업의 티어 1 벤더는 다공성을 줄이고 전기적 무결성을 높이기 위해 레이저 기반 부스바 용접을 채택합니다. 전지 조립 계약 업체는 3-6kW 스캐너에 대한 설비 투자를 확대하고, 이는 트레이닝과 서비스 인프라의 선순환으로 이어져 인도의 레이저 시장의 고객 기반을 확대하고 있습니다.

엔트리 레벨인 1-6kW 커터는 400만 루피(약 480만엔), 통합형 30kW 라인은 4캐롤 루피(약 4,800만엔)에 가격대가 형성되어 있습니다. 6,300만개 회사에 이르는 중소 영세기업(MSME)은 이러한 지출에 대한 담보가 부족한 경우가 많으며, 냉각장치와 배연장치의 추가 비용으로 총 지출이 최대 50% 증가하는 과제에 직면하고 있습니다. 리스와 공유 용량 모델이 도입을 용이하게 하고 있지만, 지방 도시로의 보급은 주요 도시에 뒤처지고 있어 인도의 레이저 시장의 단기적인 확대를 억제하는 요인이 되고 있습니다.

2025년 시점에서 파이버 플랫폼은 인도의 레이저 시장에서 40.95%의 점유율을 차지하였고 벽 콘센트의 효율과 낮은 유지보수성을 강점으로 리드를 확대할 것으로 예측됩니다. 초고속 파이버 기종은 18.45%라는 가장 높은 CAGR을 기록하여 유리 관통 전극의 가공이나 의료용 스텐트의 가공 분야에서 도입이 진행되고 있습니다. CO2 유닛은 포장 및 가죽 분야에서 여전히 중요하며, 고체 DPSS 헤드는 특수 파장 요구에 대응합니다. 엑시머 및 UV 라인은 웨이퍼 다이싱에 활용되지만 비용면에서의 과제가 남아 있습니다. 국내 OEM 제조업체는 기술 개발위원회(TDB)의 보조금을 활용해 갠트리를 국산화하면서 IPG나 TRUMPF 엔진을 조달하여 하이브리드형 밸류체인을 구현하고 있습니다. 이 메커니즘은 기술 이전을 가속화하고 인도의 레이저 시장에서 설치 단위 당 파이버 함량을 높입니다.

2차 통합자는 다이오드와 직접 반도체 발광 소자를 컴팩트한 코더에 통합하여 FMCG 라인용 제품을 개발하여 중소기업용 진입 장벽을 낮추고 있습니다. 빔 품질의 향상에 의해 박판 합금 절단에 대한 응용 범위가 넓어져, 파이버 레이저의 성장 궤도를 강화하고 있습니다. 연간 유지보수 계약 판매 시 동시 제공이 증가하는 가운데 구매자는 가동 시간을 확보할 수 있어 파이버 레이저의 우위성을 더욱 확고하게 하고 있습니다.

100W 이상의 시스템은 자동차 및 철도 차량 제조업체에 의한 후판 가공 수요를 배경으로 2025년 매출의 51.15%를 차지했습니다. 이 등급은 인도의 레이저 시장에서 인프라 정비의 진전에 연동하여 복합적으로 확대될 전망입니다. 1W 미만의 저출력기는 심장혈관 임플란트용 마이크로 절단 벤치를 뒷받침하는 의료 PLI 정책의 뒷받침으로 18.87%의 연평균 복합 성장률(CAGR)로 급성장 중입니다. 중출력 1-100W 기기는 보석 장식, 휴대폰 케이스, 명판 조각 분야에서 주력 장비로서의 지위를 유지하고 있습니다.

SLTL 그룹은 20W 마커에서 60kW 갠트리까지 광범위한 라인업을 제공하여 단일 브랜드 내에서 스케일업을 실현합니다. 2kW까지의 핸드헬드 용접기가 판금 가공 분야에 진입하여 기존 TIG 장치를 필요로 하는 현장 수리를 가능하게 합니다. 이러한 출력 카테고리의 민주화는 사용자 규모에 따라 점진적인 도입을 촉진하고 시장을 강화합니다.

India Laser Market size in 2026 is estimated at USD 2.16 billion, growing from 2025 value of USD 1.83 billion with 2031 projections showing USD 4.92 billion, growing at 17.92% CAGR over 2026-2031.

The growth outlook is sustained by government production-linked incentive (PLI) schemes, fiscal support for semiconductor fabs, and a widening installed base of industrial automation lines. Surging cluster-based electronics manufacturing, fast-rising demand for electric-vehicle battery welding, and policy-driven tax relief on imported laser machines are expanding the total addressable customer pool. Large end users are upgrading from legacy CO2 and Nd: YAG systems to high-power fiber platforms to improve throughput, while small manufacturers tap contract laser service providers to overcome capital barriers. International vendors deepen localization for after-sales support, and domestic builders introduce vertically integrated machines, together reinforcing technology diffusion across engineering hubs.

Electronics output reached INR 11 lakh crore (USD 132 billion) in 2025 after a fivefold decade jump, and component-level schemes now underpin localized resistor and capacitor lines. Cluster concentration in Dholera (Gujarat) and the Hosur-Oragadam belt (Tamil Nadu) shortens logistics cycles, allowing just-in-time laser cutting and marking services. Small firms gain economical access through shared job-shops, while large OEMs integrate multi-kilowatt fiber benches for chassis trimming and enclosure welding. Service density lowers downtime, thus incentivizing higher-power upgrades. The outcome is steady demand acceleration for mid- and high-power fiber sources across the market.

Lithium-ion cell demand above 500 GWh by 2030 pushes OEMs to specify micro-second pulsed fiber welders for copper and aluminum joints. Domestic integrators such as Light Mechanics deploy turnkey benches that join cylindrical, prismatic, and pouch cells, fostering local supply resilience. Automotive tier-1 vendors embrace laser-based busbar welding to cut porosity and raise electrical integrity. Contract battery assemblers expand capex on 3-6 kW scanners, feeding a virtuous loop of training and service infrastructure that broadens the India Laser Market customer base.

Entry-level 1-6 kW cutters start near INR 40 lakh (USD 480,000) and integrated 30 kW lines top INR 4 crore (USD 4.8 million). MSMEs, 63 million strong, often lack collateral for such outlays and face added costs for chillers and fume extractors that raise total spend by as much as 50%. Leasing and shared-capacity models ease adoption, but penetration in tier-2 hubs lags metro centers, tempering short-term expansion of the India Laser Market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Fiber platforms held 40.95% of the India Laser Market share in 2025, with the subsegment expected to widen its lead on the strength of wall-plug efficiency and low maintenance. Ultrafast fiber varieties post the fastest 18.45% CAGR, finding uptake in through-glass vias and medical stent machining. CO2 units stay relevant in packaging and leather, while solid-state DPSS heads meet niche wavelength needs. Excimer and UV lines serve wafer dicing but remain cost-sensitive. Domestic OEMs utilize Technology Development Board grants to indigenize gantries while sourcing IPG or TRUMPF engines, illustrating hybrid value chains. This arrangement accelerates knowledge transfer and elevates fiber content per installation within the India Laser Market.

Second-tier integrators bundle diode and direct semiconductor emitters into compact coders for FMCG lines, lowering entry barriers for SMEs. Improved beam quality widens application to thin-sheet alloy cutting, reinforcing fiber's trajectory. With annual service contracts increasingly bundled at sale, buyers secure uptime, further entrenching fiber dominance.

Systems above 100 W captured 51.15% of 2025 revenue as automotive and rail car builders demand thick-plate throughput. The India Laser Market size for this tier will compound inline with infrastructure buildouts. Low-power machines under 1 W surge at 18.87% CAGR on medical PLI tailwinds that favor micro-cutting benches for cardiovascular implants. Mid-power 1-100 W tools remain workhorses in jewelry, mobile handset casing, and nameplate engraving.

SLTL Group offers a spectrum from 20 W markers to 60 kW gantries, ensuring buyers scale within a single brand. Handheld welders up to 2 kW enter sheet-metal fabrication, enabling point-of-use repairs that previously required TIG setups. This democratization of power categories fosters layered adoption across user sizes, deepening the market.

The India Laser Market Report is Segmented by Laser Type (Fiber, Solid-State, CO2, Diode, Excimer/UV, Ultrafast Fiber, and More), Power Output (Low, Medium, and High), Application (Material Processing, Medical, Communication, Defense, R&D, Electronics, and More), End-User (Automotive, Healthcare, Electronics, Aerospace and Defense, and More). The Market Forecasts are Provided in Terms of Value (USD).